Asset Allocation Definition: Strategies for Smart Investing

Shlok Sobti

Asset Allocation Definition: Strategies for Smart Investing

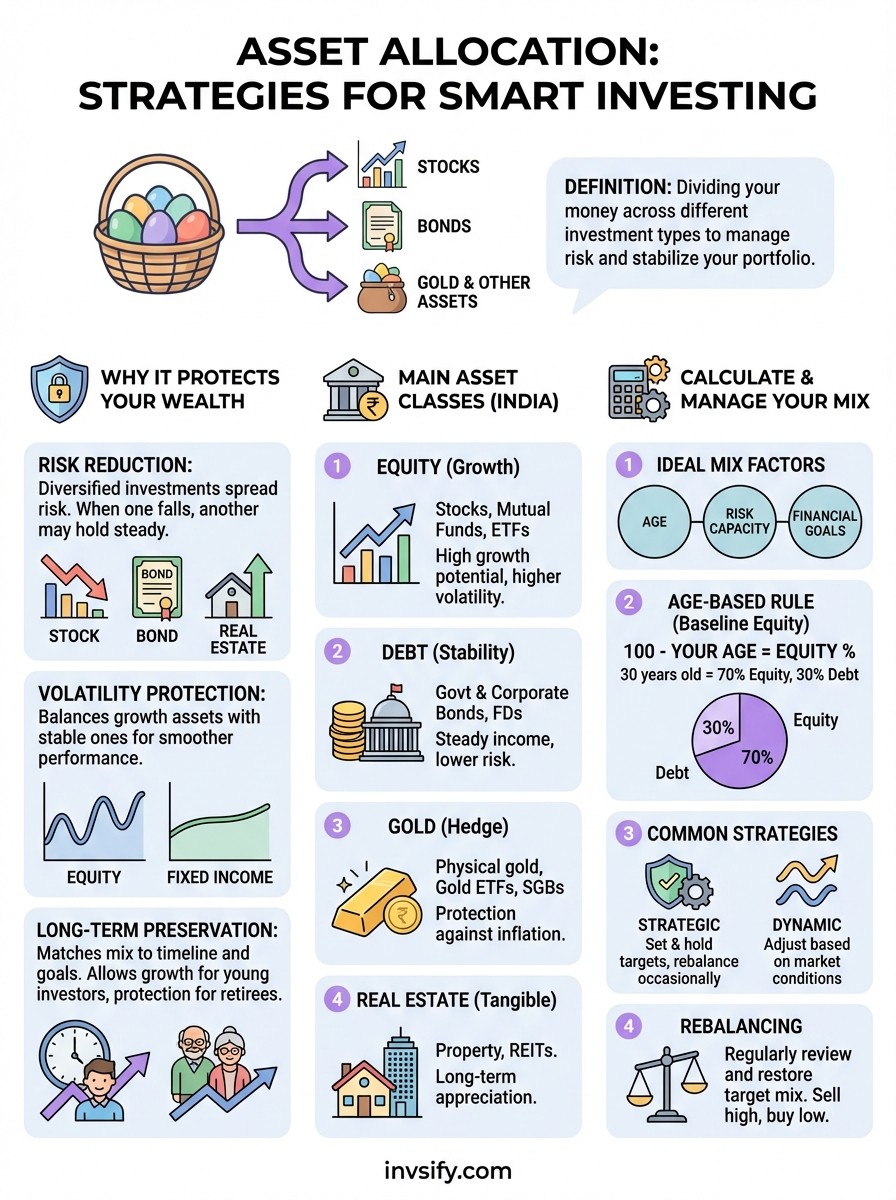

Asset allocation definition is straightforward. It means dividing your money across different types of investments like stocks, bonds, and gold. Think of it as not putting all your eggs in one basket. When one investment falls, another might rise. This strategy helps you manage risk while working toward your financial goals. Your portfolio becomes more stable because different assets behave differently during market ups and downs.

This guide walks you through everything you need to know about building a smart investment portfolio. You'll discover why asset allocation protects your wealth, learn about the main asset classes available in India, and find out how to calculate your ideal mix. We'll cover proven strategies, show you how to rebalance your portfolio, and help you take your first steps toward smarter investing. Whether you're new to investing or looking to optimize your current approach, you'll find practical insights to grow your money with confidence.

Why asset allocation protects your wealth

Your financial future depends on how well you protect your money from losses. Market crashes can wipe out portfolios that bet everything on one asset type, but diversified investments spread this risk across multiple categories. When stocks fall, bonds might hold steady or even rise. This balance keeps your wealth safer during turbulent times and helps you sleep better at night knowing your money isn't riding on a single bet.

Risk reduction through diversification

You reduce your exposure to any single investment failure when you split your money across different assets. Stock market drops hit portfolios hard when investors hold only equity, but those with bonds and gold experience smaller losses. The asset allocation definition centers on this principle: different investments react differently to the same economic events. When inflation rises, real estate might gain value while bonds lose purchasing power. This natural hedging protects your overall wealth from severe damage.

"Diversification is the only free lunch in investing."

Protection against market volatility

Your portfolio experiences fewer wild swings when you balance growth assets with stable ones. Equity investments can jump 30% in one year and drop 20% the next, creating stress and poor decisions. Adding fixed-income securities smooths these fluctuations because they typically move less dramatically. During the 2020 market crash, investors with mixed portfolios recovered faster than those holding only stocks. This stability lets you stick to your long-term plan instead of panicking and selling at the worst possible moment.

Long-term wealth preservation

You build lasting wealth by matching your asset mix to your timeline and goals. Young investors can afford more stock exposure because they have decades to recover from downturns. Those approaching retirement need capital protection through safer assets like bonds and cash equivalents. This strategic approach prevents you from taking unnecessary risks when you can't afford losses and maximizes growth when time is on your side.

Main asset classes in the Indian market

You have four primary investment categories to work with when building your portfolio in India. Equity investments include stocks listed on the NSE and BSE, mutual funds, and exchange-traded funds that offer high growth potential but come with increased volatility. Debt instruments cover government bonds, corporate bonds, fixed deposits, and debt mutual funds that provide steady income and stability. Gold serves as a traditional hedge against inflation, available through physical gold, gold ETFs, or sovereign gold bonds. Real estate rounds out your options through direct property ownership or Real Estate Investment Trusts (REITs). Understanding these categories helps you apply the asset allocation definition to your specific financial situation.

Equity for growth

Your growth portfolio relies on stocks and equity mutual funds that participate in company profits and market expansion. The Indian stock market offers access to thousands of listed companies across sectors like technology, banking, pharmaceuticals, and manufacturing. Index funds tracking the Nifty 50 or Sensex provide broad market exposure with lower fees than actively managed funds. Equity investments historically deliver 12-15% annual returns over long periods, but you must prepare for short-term volatility and occasional drops of 20-30% during market corrections.

Debt for stability

You build portfolio stability through government securities and corporate bonds that pay predictable interest regardless of market conditions. Government bonds like the 7.75% Savings Bond offer guaranteed returns with zero default risk backed by the Indian government. Debt mutual funds give you professional management and daily liquidity while generating 6-8% annual returns with significantly lower volatility than stocks.

How to calculate your ideal portfolio mix

Your ideal portfolio depends on three factors: your age, your risk capacity, and your financial goals. The asset allocation definition becomes practical when you apply these variables to determine how much belongs in each category. Start by evaluating your investment timeline because someone retiring in five years needs a completely different mix than someone with 30 years until retirement. Your risk tolerance matters equally since aggressive portfolios can cause sleepless nights if you panic during downturns and sell at losses.

Age-based allocation rule

You can use a simple formula to establish your baseline equity percentage: subtract your age from 100. A 30-year-old would allocate 70% to equity and 30% to debt using this approach. This method acknowledges that younger investors recover from market crashes more easily because time heals portfolio wounds. Older investors need capital preservation more than growth, so their equity exposure decreases as they approach retirement. Adjust this baseline up or down by 10-15% based on your personal comfort with volatility.

Risk capacity factors

Your financial situation determines how much risk you can actually handle beyond just age. Someone with stable employment and an emergency fund covering six months of expenses can afford more equity exposure than someone with irregular income. Outstanding loans, dependent family members, and upcoming large expenses like home purchases or education fees should push you toward safer allocations. Calculate your fixed monthly obligations and ensure your stable income assets generate enough to cover them comfortably.

Common strategies for asset allocation

You can choose from several proven approaches when implementing the asset allocation definition in your portfolio. Each strategy offers different benefits depending on your investment style and time commitment. Strategic allocation works best for hands-off investors who prefer stability, while dynamic allocation suits those comfortable making regular adjustments based on market conditions. Understanding these methods helps you select the approach that matches your personality and financial situation.

Strategic asset allocation

You set target percentages for each asset class and maintain them over long periods with this traditional approach. A typical strategic portfolio might hold 60% equity, 30% debt, and 10% gold, staying consistent through market cycles. This buy-and-hold strategy saves you from emotional decisions during volatility and reduces transaction costs since you make minimal changes. Investors using this method rebalance only when allocations drift significantly from targets, perhaps once or twice yearly.

"The stock market is a device for transferring money from the impatient to the patient."

Dynamic asset allocation

You actively adjust your portfolio mix based on market conditions and economic indicators with this flexible approach. When stocks appear overvalued, you shift more money into bonds or gold for protection. Market timing plays a larger role here, requiring you to monitor economic data, corporate earnings, and interest rate trends regularly. This strategy demands more effort but potentially captures better returns by avoiding overheated markets and buying during downturns.

Steps to rebalance your portfolio effectively

Your portfolio drifts from its target allocation over time as different assets grow at different rates. Stocks might surge 25% while bonds stay flat, pushing your equity percentage higher than intended. Regular rebalancing brings your allocations back to target levels, locking in gains from outperformers and buying more of underperformers at lower prices. This disciplined approach keeps your risk level consistent with your original plan based on the asset allocation definition you established.

Schedule regular reviews

You need consistent check-ins to monitor how far your allocations have drifted from targets. Most investors rebalance quarterly or semi-annually, though annual reviews work fine for hands-off portfolios. Set calendar reminders for specific dates like January 1st or your birthday so you never forget. Calculate the current percentage of each asset class and compare it to your target mix. Trigger rebalancing when any category drifts more than 5% from its target allocation.

"Rebalancing forces you to sell high and buy low automatically."

Execute rebalancing trades

You restore your target mix by selling overweight assets and buying underweight ones. Sell enough equity to bring it from 75% down to your 60% target, then use those proceeds to buy bonds or gold that have fallen below their targets. Tax implications matter in taxable accounts, so consider rebalancing within tax-advantaged retirement accounts first. Use new contributions to buy underweight assets instead of selling when possible, avoiding transaction costs and potential capital gains taxes.

Start your asset allocation journey

You now understand the asset allocation definition and how it protects your wealth through diversification across equity, debt, gold, and real estate. Building your portfolio mix requires calculating the right percentages based on your age, risk capacity, and financial goals. Regular rebalancing keeps your investments aligned with your targets and forces you to buy low while selling high automatically.

Taking your first step means assessing your current holdings and determining whether they match your intended allocation. Most investors discover significant gaps between their actual portfolio and what they should own. Professional guidance eliminates guesswork and helps you avoid costly mistakes that set back your financial progress.

Get personalized asset allocation recommendations from Invsify's AI-powered platform. Our SEBI-registered advisors combine smart technology with human expertise to build portfolios optimized for your specific situation. You'll receive conflict-free advice without hidden fees, transparent tracking tools, and ongoing support to keep your wealth growing steadily toward your goals.