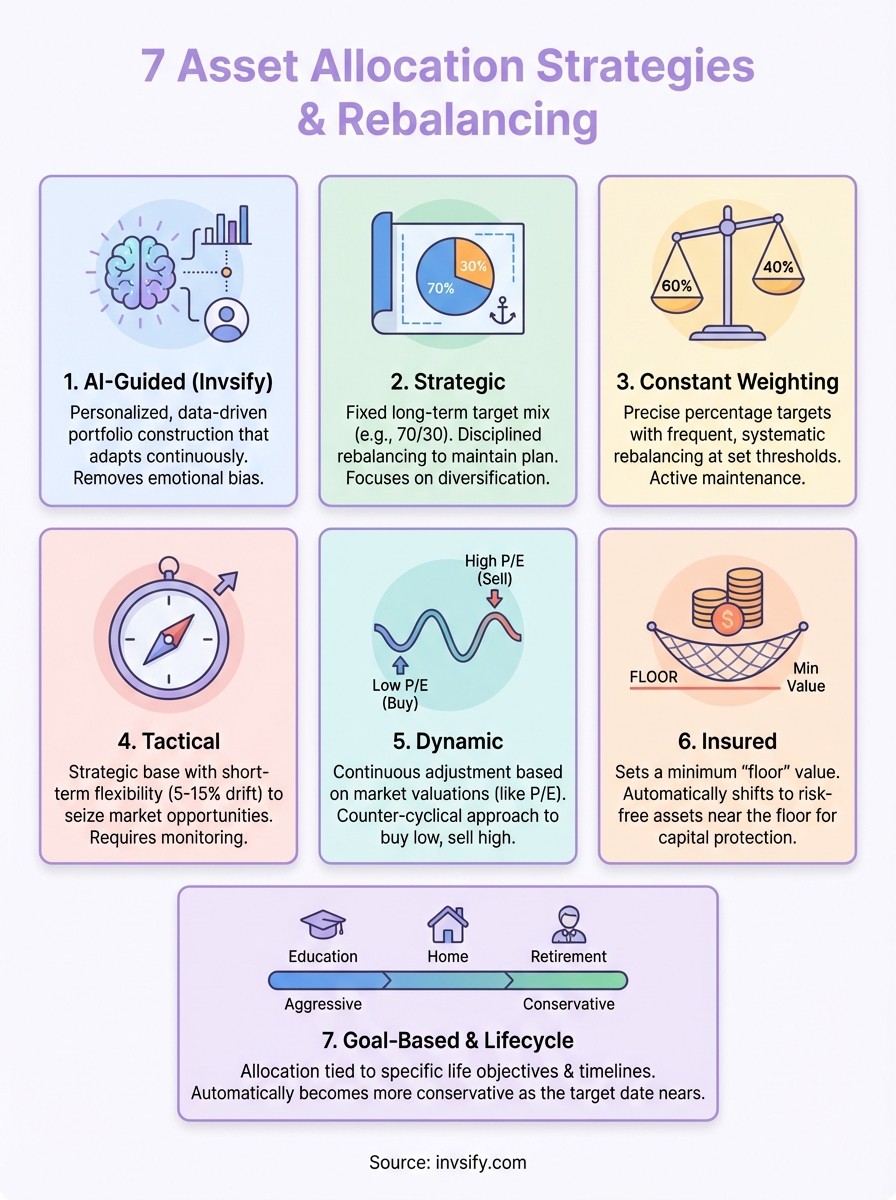

7 Asset Allocation Strategies With Examples And Rebalancing

Shlok Sobti

7 Asset Allocation Strategies With Examples And Rebalancing

You know you should diversify your portfolio. But spreading your money across different asset classes is just the starting point. The real question is how much goes where and when you should adjust that mix. Get this wrong and you might take on too much risk or miss out on growth opportunities that could set back your financial goals by years.

This guide breaks down seven asset allocation strategies used by investors across India. You'll see how strategic allocation differs from tactical approaches, why dynamic strategies respond to market conditions, and how newer AI powered methods are changing the game. Each strategy includes practical examples tailored for Indian investors, clear guidance on when to rebalance your portfolio, and honest advice about who benefits most from each approach. Whether you're building your first portfolio or optimizing an existing one, you'll find the framework that matches your risk tolerance, investment timeline, and financial objectives.

1. AI guided asset allocation with Invsify

Modern technology transforms how investors approach portfolio construction. AI powered platforms analyze market data and your personal financial situation to recommend optimal asset mixes that adapt as conditions change. This approach removes guesswork and emotional decisions from the equation while maintaining the personalized attention your wealth deserves.

Overview

AI guided allocation uses machine learning algorithms to process vast amounts of market information and match it to your specific profile. The system evaluates your risk tolerance, investment goals, and time horizon to suggest a portfolio mix across equity, debt, gold, and other asset classes. Unlike traditional methods that rely on broad rules of thumb, this strategy continuously learns from market patterns and adjusts recommendations based on real-time data while keeping you in control of final decisions.

How it works

You start by completing a digital risk profiling assessment that captures your financial objectives and comfort with market volatility. The AI then generates a personalized Wealth Wellness Score and recommends your initial allocation. As markets move and your circumstances evolve, the platform monitors your portfolio daily and alerts you when rebalancing opportunities arise or when your allocation drifts from optimal ranges.

With AI powered insights, you make informed decisions backed by data rather than relying on instinct or outdated formulas.

Example for an Indian investor

A 35-year-old professional with moderate risk tolerance might receive an allocation of 65% equity funds, 25% debt instruments, and 10% gold. The AI selects specific mutual fund categories like large cap, mid cap, and balanced advantage funds based on current market valuations. When equity markets rise significantly, the system notifies you to trim equity exposure and shift proceeds into debt to maintain your target allocation.

Rebalancing approach

The platform tracks your portfolio drift automatically and sends rebalancing alerts when any asset class deviates more than 5% from target weights. You execute these adjustments through the app with AI recommended fund switches that minimize tax impact and transaction costs.

Who should use this strategy

This works best if you want professional-grade portfolio management without paying high advisory fees. Tech-comfortable investors who value data-driven decisions but lack time for constant market monitoring will find this approach fits their lifestyle. New investors benefit from structured guidance while experienced investors appreciate the analytical depth behind each recommendation.

2. Strategic asset allocation

Strategic asset allocation establishes a long-term portfolio blueprint and sticks to it through market cycles. This disciplined approach sets your target percentages for each asset class based on expected returns and holds those proportions steady over time. Think of it as your portfolio's constitution that guides decisions regardless of short-term market noise.

Overview

This method creates a fixed policy mix that reflects your financial goals and risk capacity. You determine target allocations for equity, debt, and other assets based on historical returns and your investment timeline. The strategy assumes that asset class diversification provides better risk-adjusted returns over decades than trying to time market movements or chase hot sectors.

How it works

You establish percentage ranges for each asset class rather than exact figures. A typical range might allocate 65 to 75% in equity and 25 to 35% in debt. This flexibility allows for minor market fluctuations without triggering constant adjustments. When price movements push your allocation outside these bands, you rebalance back to target levels by selling appreciated assets and buying underperforming ones.

Strategic allocation forces you to buy low and sell high through systematic rebalancing rather than emotional reactions.

Example for an Indian investor

Consider a 40-year-old planning for retirement who sets 70% equity and 30% debt as targets. She invests across large cap mutual funds, diversified equity schemes, and government securities. After a strong equity rally increases her stock allocation to 78%, she sells equity units and redirects proceeds into debt funds to restore the 70-30 balance.

Rebalancing approach

You review your portfolio every six to twelve months or when any asset class drifts beyond 5% of its target weight. Rebalancing transactions happen through predetermined calendar dates rather than market predictions. Tax implications matter here since selling appreciated equity funds held over one year attracts long-term capital gains tax in India.

Who should use this strategy

Strategic allocation suits long-term investors who want simple portfolio management without constant monitoring. Retirement savers and goal-focused investors benefit from this buy-and-hold discipline. You need patience to stick with the plan during market extremes when emotions tempt you to abandon your targets.

3. Constant weighting asset allocation

Constant weighting takes strategic allocation one step further with active portfolio monitoring and frequent adjustments. Instead of allowing your asset mix to drift within broad ranges, this method maintains precise target percentages through systematic rebalancing. You act as soon as price movements shift your allocation away from predetermined weights.

Overview

This approach demands vigilant portfolio tracking and regular intervention to preserve your chosen asset mix. The strategy recognizes that market movements constantly alter your portfolio composition even when you make no trades. Rising equity values naturally increase your stock exposure while stable debt holdings shrink as a percentage of total wealth.

How it works

You set exact allocation targets for each asset class and establish tolerance thresholds that trigger rebalancing actions. When any holding exceeds or falls below its target by a specific margin, you immediately buy or sell assets to restore original proportions. This creates a disciplined system where appreciated assets get sold automatically and underperforming assets receive fresh capital.

Constant weighting enforces buy-low-sell-high discipline through mechanical rules rather than subjective judgment.

Example for an Indian investor

A 45-year-old maintains 60% equity and 40% debt with a 3% rebalancing threshold. When equity gains push the allocation to 63%, she sells equity fund units worth the excess amount and purchases debt instruments to return to 60-40 split.

Rebalancing approach

You monitor portfolio values weekly or monthly and execute trades whenever holdings breach threshold limits. Transaction costs and tax consequences require careful consideration since frequent rebalancing generates multiple taxable events throughout the year.

Who should use this strategy

This fits active investors who enjoy hands-on portfolio management and can track holdings regularly. You need discipline to execute rebalancing trades during market extremes when your instincts might resist selling winners or buying losers.

4. Tactical asset allocation

Tactical asset allocation adds flexibility to your long-term strategy by allowing temporary deviations from target weights. This method recognizes that market opportunities emerge that warrant short-term adjustments while maintaining your strategic foundation. You capitalize on favorable conditions without abandoning your core investment philosophy.

Overview

This approach blends strategic discipline with active management to capture market inefficiencies. You maintain baseline allocation targets but permit tactical shifts of typically 5 to 15% from those targets when research indicates specific asset classes offer exceptional value or risk. The strategy requires you to identify opportunities and act decisively while keeping exit plans clear for returning to strategic weights.

How it works

You establish core portfolio targets as your foundation then overlay tactical views based on market analysis. Research might reveal equity valuations reaching historic lows or debt yields spiking to attractive levels. Your tactical adjustments temporarily overweight undervalued assets and reduce exposure to overvalued ones. These moves last weeks to months rather than years, requiring you to monitor positions actively and recognize when opportunities expire.

Tactical adjustments let you profit from market dislocations while your strategic base keeps the portfolio anchored.

Example for an Indian investor

An investor with 70% equity and 30% debt targets notices mid-cap valuations dropping significantly during a market correction. She tactically increases mid-cap allocation to 80% equity (10% above target) by reducing debt holdings. After mid-caps recover and valuations normalize over six months, she reverses the tactical position and returns to her 70-30 strategic mix.

Rebalancing approach

You review positions monthly or quarterly to assess whether tactical bets remain valid. The rebalancing triggers when your analysis suggests opportunities have played out or when tactical positions exceed predetermined drift limits. Tax planning becomes crucial since tactical trading generates more frequent taxable events than passive strategies.

Who should use this strategy

Tactical allocation suits knowledgeable investors who understand market valuation metrics and can commit time to research. You need conviction to act against prevailing sentiment and discipline to exit positions once opportunities fade.

5. Dynamic asset allocation

Dynamic asset allocation continuously adjusts your portfolio mix in response to market conditions rather than adhering to fixed targets. This strategy recognizes that asset valuations fluctuate and optimal allocations should shift accordingly. You take a fluid approach that increases exposure when assets become cheap and reduces positions as prices climb.

Overview

This method treats your asset allocation as a moving target that responds to valuation metrics like price-to-earnings ratios, dividend yields, and price-to-book values. Most dynamic strategies follow a counter-cyclical approach where you buy more equity when valuations drop and shift to debt when stocks become expensive. The strategy operates on mean reversion principles, betting that valuations eventually return to historical averages.

How it works

Your portfolio manager or chosen fund tracks key valuation indicators for equity markets and applies predefined rules to adjust allocations. When equity P/E ratios fall below historical averages, the allocation shifts toward stocks automatically. As valuations rise to expensive levels, holdings rotate into safer debt instruments. These adjustments happen continuously without waiting for scheduled rebalancing dates.

Dynamic allocation removes emotional decision making by following objective valuation rules during market extremes.

Example for an Indian investor

A dynamic fund you hold starts the year with 60% equity and 40% debt allocation. When Nifty 50 valuations drop from 22 P/E to 18 P/E during a correction, the fund automatically increases equity to 75% based on valuation triggers. As markets recover and P/E climbs back to 24, the fund reduces equity to 50% and parks proceeds in government securities.

Rebalancing approach

Adjustments occur automatically based on market valuations rather than calendar schedules or percentage drifts. The fund manager monitors indicators daily and executes trades when valuation thresholds breach predetermined levels. This eliminates manual intervention from your side.

Who should use this strategy

Dynamic asset allocation strategies work well if you want professional active management without making trading decisions yourself. Investors who believe in mean reversion and counter-cyclical positioning benefit most from this approach.

6. Insured asset allocation

Insured asset allocation protects your portfolio from falling below a predetermined floor value while allowing growth potential above that threshold. This strategy creates a safety net for your capital by setting a minimum acceptable portfolio value that triggers shifts into risk-free assets. You maintain upside participation when markets perform well but limit downside exposure when conditions deteriorate.

Overview

This method establishes a base portfolio value that represents your absolute minimum acceptable wealth level. Above this floor, you actively manage investments across equity and other growth assets to maximize returns. When your portfolio approaches the floor value, the strategy automatically shifts holdings into government securities or other capital-preservation instruments to lock in remaining wealth.

How it works

You define your minimum acceptable portfolio value based on essential financial needs or goals. Your portfolio manager invests aggressively in growth assets while holdings stay comfortably above this floor. As portfolio value declines toward the threshold, allocations gradually shift from equity to debt instruments. Once you hit the floor, your entire portfolio moves into Treasury bills or fixed deposits until market conditions improve.

Insured allocation lets you pursue growth opportunities while guaranteeing you never lose more than you can afford.

Example for an Indian investor

An investor with a Rs 50 lakh portfolio sets Rs 40 lakh as the floor value. She invests Rs 50 lakh in 70% equity and 30% debt initially. When markets drop and portfolio value reaches Rs 42 lakh, the strategy automatically moves holdings into government bonds to preserve the remaining capital.

Rebalancing approach

You monitor portfolio value daily or weekly against your floor threshold. Rebalancing happens automatically through predefined rules that shift asset mix as you approach the floor.

Who should use this strategy

This suits risk-averse investors who need capital protection guarantees while seeking growth. Retirees or those near major financial goals benefit from the downside protection this strategy provides.

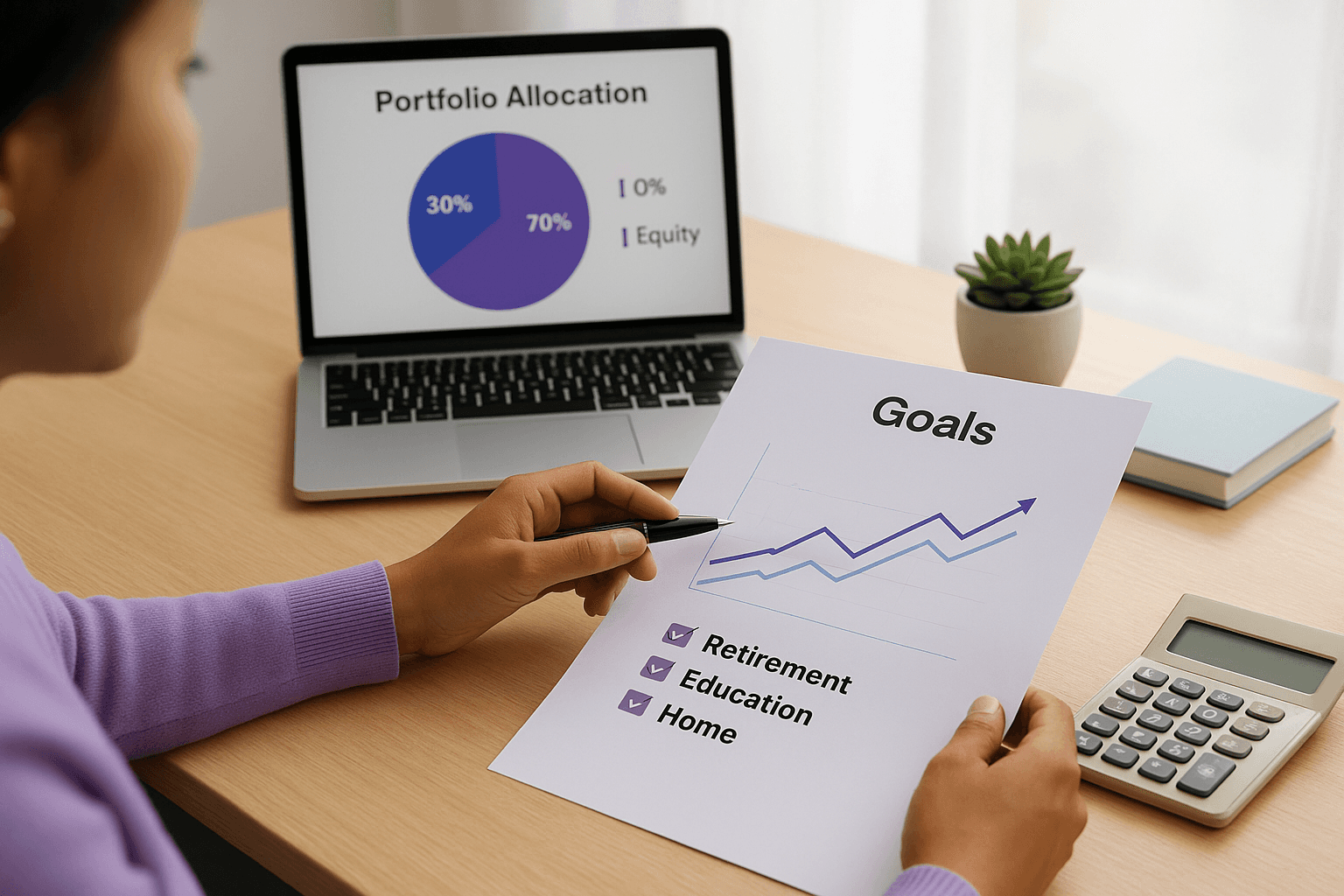

7. Goal based and lifecycle allocation

Goal based allocation ties your portfolio composition directly to specific life objectives and automatically adjusts as you approach target dates. This strategy recognizes that different goals require different risk profiles and investment timelines. Your asset mix evolves based on when you need the money rather than market conditions or arbitrary rules.

Overview

This approach maps each financial goal to a dedicated allocation strategy that becomes more conservative as your deadline approaches. Retirement funds start aggressively in equities during your 20s then gradually shift toward debt as you near retirement age. The strategy builds on the principle that time horizon determines appropriate risk levels since longer periods let you recover from market downturns.

How it works

You segment your portfolio into separate buckets for distinct goals like retirement, education funding, or home purchase. Each bucket follows an age-based or years-to-goal formula that reduces equity exposure systematically over time. A common rule subtracts your age from 100 to determine equity percentage, so a 30-year-old holds 70% stocks while a 60-year-old holds 40%.

Goal based strategies eliminate confusion about appropriate risk by anchoring decisions to concrete timelines and objectives.

Example for an Indian investor

A 35-year-old planning retirement at 60 invests in a lifecycle mutual fund targeting 2051 with current allocation of 80% equity and 20% debt. The fund automatically reduces equity by 2% annually as retirement approaches, reaching 30% equity and 70% debt by age 60 when withdrawals begin.

Rebalancing approach

Lifecycle funds execute automatic rebalancing quarterly or annually following predetermined glide paths that reduce risk over time. You make no manual adjustments since the fund handles all allocation changes based on your target date.

Who should use this strategy

This suits hands-off investors who want set-and-forget portfolio management aligned with specific life goals. First-time investors and those uncomfortable with active decision making benefit from the autopilot approach this strategy provides.

Final thoughts

Your choice among these asset allocation strategies depends on your investment timeline, risk capacity, and how actively you want to manage your wealth. Strategic allocation works if you prefer hands-off investing, while tactical and dynamic approaches suit those who can dedicate time to portfolio monitoring. Goal-based strategies remove complexity by tying decisions to specific objectives, and AI-guided methods combine professional-grade analysis with personal control.

The right strategy aligns with both your financial goals and lifestyle. You don't need to pick just one approach either. Many investors use strategic allocation as their foundation while applying tactical overlays for specific opportunities. Others segment their portfolio across multiple asset allocation strategies based on different time horizons.

Start by assessing your risk tolerance and timeline, then choose the framework that matches your situation. Get your personalized allocation recommendations from Invsify and let AI-powered insights guide your portfolio decisions while you stay in control.