Asset Allocation Vs Diversification: Differences & Examples

Shlok Sobti

Asset Allocation Vs Diversification: Differences & Examples

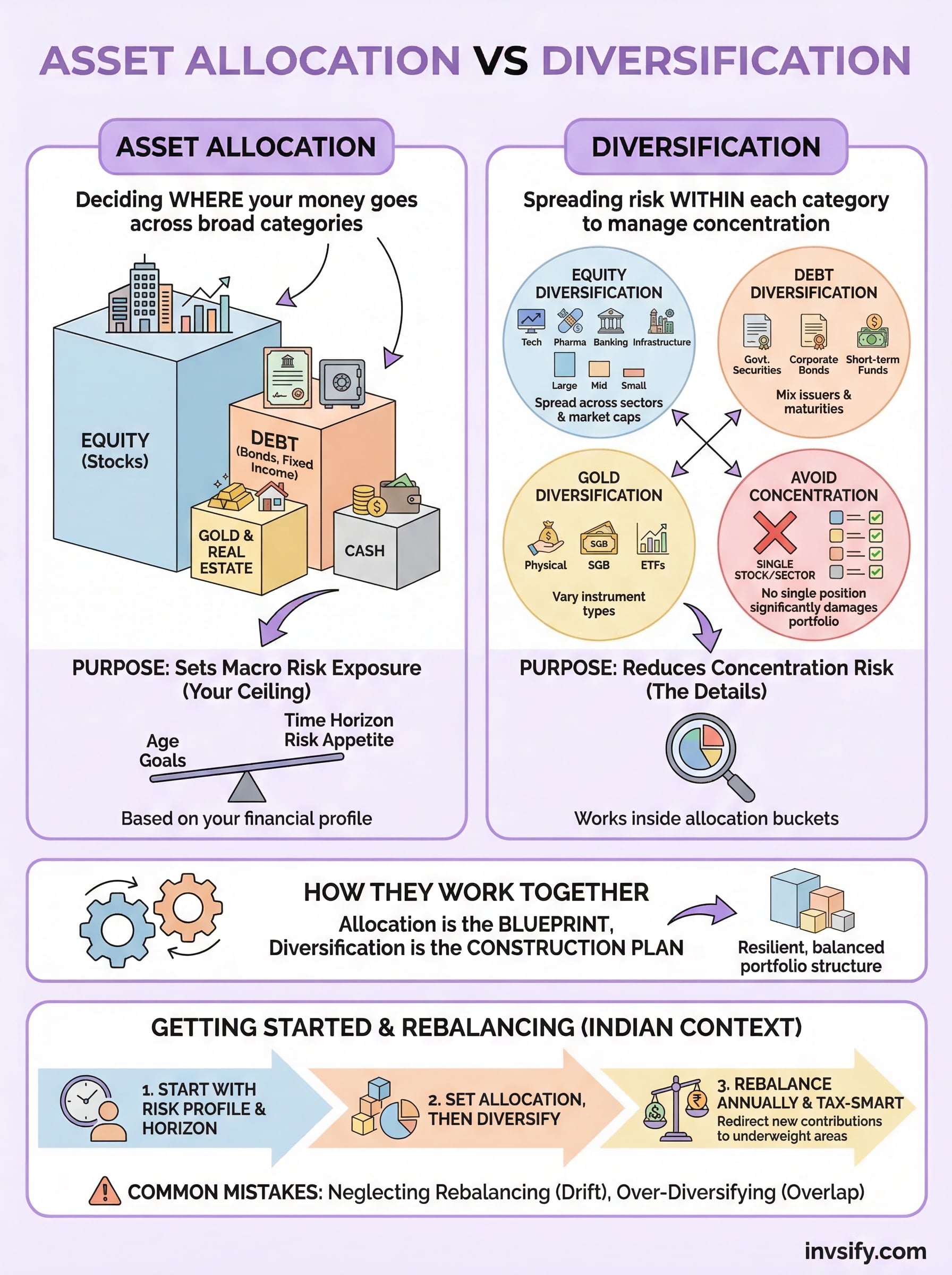

Most investors use the terms asset allocation vs diversification interchangeably, and that confusion can quietly cost them returns. Both strategies aim to manage risk, but they operate at fundamentally different levels of your portfolio. One decides where your money goes across broad categories like equity, debt, and gold. The other ensures you're not placing oversized bets within those categories.

Getting this distinction right matters more than most people realize. A portfolio that's allocated well but poorly diversified can still take a serious hit. And a diversified portfolio with the wrong allocation for your risk profile can underperform for years. The two concepts work together, but they're not the same, and treating them as such leads to blind spots in your investment strategy.

This article breaks down exactly how asset allocation and diversification differ, how they complement each other, and how to apply both with real examples. At Invsify, our AI-powered advisory platform helps Indian investors build portfolios that get both of these right, with conflict-free, data-backed recommendations tailored to your financial goals and risk appetite.

What asset allocation and diversification mean

Before you can apply either strategy, you need a working definition of each. Understanding asset allocation vs diversification as two separate tools, not one combined idea, gives you a clearer mental model for building a portfolio that actually holds up in different market conditions. Both strategies reduce risk, but they do it at different levels and through different mechanisms.

Asset allocation: how you divide your money across categories

Asset allocation is the process of deciding what percentage of your total investable money goes into each major asset class. The most common categories are equity (stocks), debt (bonds and fixed income), gold, real estate, and cash or liquid funds. The percentages you choose depend on your age, income stability, financial goals, and how much volatility you can handle emotionally and financially.

For example, a 30-year-old with a stable salary and a 20-year investment horizon might put 70% in equity, 20% in debt, and 10% in gold. A 55-year-old approaching retirement would likely flip that balance toward debt and gold to protect accumulated wealth. The logic behind this is straightforward: different asset classes react differently to the same economic event. When equity markets fall sharply, government bonds often hold steady or rise. When inflation spikes, gold tends to appreciate. Asset allocation takes advantage of this low correlation between asset classes to cushion your portfolio from extreme swings.

The right asset allocation is not a fixed formula. It's a personalized decision based on your specific financial situation, goals, and time horizon.

Diversification: how you spread risk within each category

Diversification operates inside each asset class, not across them. Once you've decided to put 70% of your portfolio in equity, diversification determines which stocks, sectors, or funds that equity portion flows into. Putting your entire equity allocation into a single company, or even a single sector like IT or pharma, concentrates your risk. A single bad quarter, regulatory change, or industry disruption can wipe out a significant portion of your portfolio if you've concentrated too heavily.

Proper diversification spreads your equity allocation across sectors like technology, banking, consumer goods, and infrastructure. It also spreads across market capitalizations, meaning a mix of large-cap, mid-cap, and small-cap stocks. Within debt, diversification means not putting everything into one type of instrument. You might hold a combination of government securities, corporate bonds, and short-duration debt funds rather than concentrating in one issuer or maturity.

The same principle applies to every asset class. Even within gold, you can diversify between physical gold, Sovereign Gold Bonds, and Gold ETFs, each with different liquidity profiles and tax treatment. Diversification within debt can also mean spreading across issuers with different credit ratings, which protects you if a lower-rated issuer defaults. The core idea is that no single position, sector, or issuer should be large enough to significantly damage your overall portfolio if it underperforms or fails.

Asset allocation vs diversification and how they work together

Think of asset allocation as the blueprint and diversification as the construction plan. One without the other leaves your portfolio either structurally unsound or poorly built. When you understand how asset allocation vs diversification interact, you stop treating them as separate tasks and start using them as a two-step process that builds genuine portfolio resilience. Allocation defines your risk exposure at the macro level, while diversification manages concentration risk within each layer.

How allocation sets the foundation

Your asset allocation decision comes first and carries the most weight. It determines how much of your portfolio can grow aggressively versus how much stays protected. A well-chosen allocation anchors your investment strategy to your actual financial goals, whether that's building a retirement corpus in 25 years or preserving capital for a goal three years away. Without a clear allocation framework, diversification has no structure to operate within.

Consider a simple example: if you put 80% in equity and 20% in debt, your portfolio behaves very differently from one split 50/50, even if both are equally well-diversified within each asset class. The allocation itself determines how much volatility you accept as a baseline, which is why getting this layer right matters before anything else.

Your allocation sets the ceiling on your risk. Diversification works within that ceiling to reduce unnecessary concentration.

How diversification fills in the details

Once your allocation percentages are fixed, diversification reduces the damage any single investment can do inside each bucket. If your equity allocation holds only two or three stocks, a bad earnings report from one company can move your entire portfolio. Spreading across 15 to 20 well-chosen stocks or a mix of diversified mutual funds significantly cuts that single-stock risk without changing your overall equity exposure.

Both strategies reinforce each other in practice. A portfolio with strong allocation but weak diversification still carries hidden concentration risk. One with good diversification but a mismatched allocation can underperform for years simply because the risk profile does not match your investment timeline. Both layers need to work correctly at the same time for your portfolio to perform as intended.

Why asset allocation and diversification matter in India

The Indian investment landscape presents specific conditions that make both asset allocation vs diversification decisions more complex and more consequential than in many other markets. You have access to a wide range of instruments, including equity mutual funds, Public Provident Fund (PPF), National Pension System (NPS), Sovereign Gold Bonds, and REITs, but that variety also means more room for poor choices if you approach your portfolio without a clear framework.

The unique challenges of the Indian market

India's equity markets can deliver strong long-term returns, but they also carry significant short-term volatility. Sector-specific swings are sharp, particularly in areas like PSU stocks, real estate, and banking. If your allocation leans too heavily on equities without proper diversification across sectors and market caps, a single regulatory shift or global sell-off can hit your portfolio harder than you expect.

Currency risk adds another layer. If part of your portfolio includes international funds or dollar-linked assets, rupee depreciation can distort your real returns in ways that aren't obvious when markets look stable. Getting your allocation right across domestic and international assets reduces this exposure without sacrificing growth potential.

India's mix of high-growth opportunities and structural volatility means your allocation decisions carry more weight here than in slower-moving developed markets.

Inflation, tax rules, and the Indian investor

Inflation in India has historically run higher than in developed economies, which means debt instruments with fixed returns can quietly erode your purchasing power if they dominate your allocation. You need equity exposure to stay ahead of inflation over the long term, which is why a balanced allocation remains critical even for conservative investors.

India's tax structure also directly affects how you diversify within asset classes. Equity held for more than one year attracts long-term capital gains tax at 12.5% beyond Rs 1.25 lakh, while debt fund gains are now taxed at your income slab rate. Knowing these rules helps you diversify across instruments in a way that optimizes your post-tax returns, not just your pre-tax ones.

How to choose asset allocation and diversify your holdings

Choosing your asset allocation before picking individual investments is the most important sequencing decision you'll make as an investor. When you approach asset allocation vs diversification as a two-step process, starting with the macro split and then filling in the details, your portfolio becomes easier to build and easier to maintain over time.

Start with your risk profile and time horizon

Your age and investment horizon are the two most reliable starting points for setting your allocation. A simple starting framework for equity exposure is to subtract your age from 100, or 110 if you have a higher risk tolerance. A 35-year-old might hold 65 to 75% in equity, with the rest split between debt and gold. This is a starting point, not a fixed rule. Your income stability, existing liabilities, and near-term financial obligations all adjust this baseline number.

Match your allocation to your actual financial situation, not to what sounds aggressive or conservative based on someone else's portfolio.

Once you fix your equity percentage, set your debt and gold split based on how much capital protection you need in the near term. If you have a large upcoming expense like home purchase funding or education costs arriving in three to five years, a higher debt allocation makes sense for that portion of your money.

Diversify within each asset class systematically

After locking in your allocation percentages, use a sector-spread approach for equities. Aim for exposure across at least four to five sectors, with no single sector exceeding 25 to 30% of your equity bucket. For most Indian investors, a combination of large-cap index funds, mid-cap funds, and one flexi-cap fund covers necessary diversification without overcomplicating the portfolio.

Spreading your debt allocation across multiple instruments also matters. Hold a mix of PPF, short-duration debt funds, and floating rate bonds to balance liquidity, safety, and yield across different interest rate environments. Within your gold allocation, Sovereign Gold Bonds offer better long-term value than physical gold for most investors due to the additional interest income and favorable tax treatment at maturity.

How to rebalance and avoid common portfolio mistakes

Rebalancing is the step most investors skip, and that oversight gradually shifts your portfolio away from your intended allocation. Markets move at different speeds, so your equity holdings can grow much faster than your debt over a strong bull run, pushing your actual allocation far beyond your target risk level without you doing anything. Rebalancing brings your portfolio back in line with your original plan.

When and how to rebalance

The simplest approach is to review your portfolio at least once a year, or whenever a single asset class drifts more than 5 to 10 percentage points away from your target. If your equity allocation was set at 70% and a strong market run has pushed it to 82%, you're now carrying more risk than your plan intended. Selling a portion of your equity gains and redirecting the proceeds into debt or gold restores your original balance and locks in some of those gains in the process.

A practical rebalancing method for Indian investors is to redirect new contributions toward underweight asset classes rather than selling existing holdings, which helps you avoid triggering capital gains tax unnecessarily. For example, if your equity bucket is overweight, direct your next few SIP contributions to your debt fund until the balance corrects.

Mistakes that quietly damage your portfolio

The most common mistake in asset allocation vs diversification decisions is treating them as one-time events. Your allocation needs to shift as your life circumstances change, because a 40-year-old carrying the same aggressive equity-heavy allocation they set up at 28 is taking on risk that their timeline no longer justifies.

Rebalancing annually takes less than an hour and protects years of compounding from a single market event catching you overexposed.

Another common error is over-diversifying within equity by holding too many mutual funds that overlap in their underlying holdings. Owning six large-cap funds does not give you six times the diversification because they likely hold many of the same stocks. Two to three well-chosen funds across different categories give you cleaner diversification with less redundancy and far easier tracking.

A simple way to get started

Getting asset allocation vs diversification right does not require a finance degree or hours of spreadsheet work. The practical starting point is to write down your current asset split across equity, debt, and gold, then compare it to where it should be based on your age and goals. That single exercise reveals most of the gaps worth fixing.

From there, check whether your equity holdings concentrate too heavily in one or two sectors or funds. If they do, redirecting your next few contributions toward underweight areas costs you nothing in tax and gradually improves your balance. Small, consistent adjustments matter more than a perfect portfolio built once and ignored.

If you want a faster path to a well-structured, conflict-free portfolio, start your investment journey with Invsify. The platform gives you AI-powered allocation recommendations and ongoing portfolio tracking tailored to your specific financial situation.