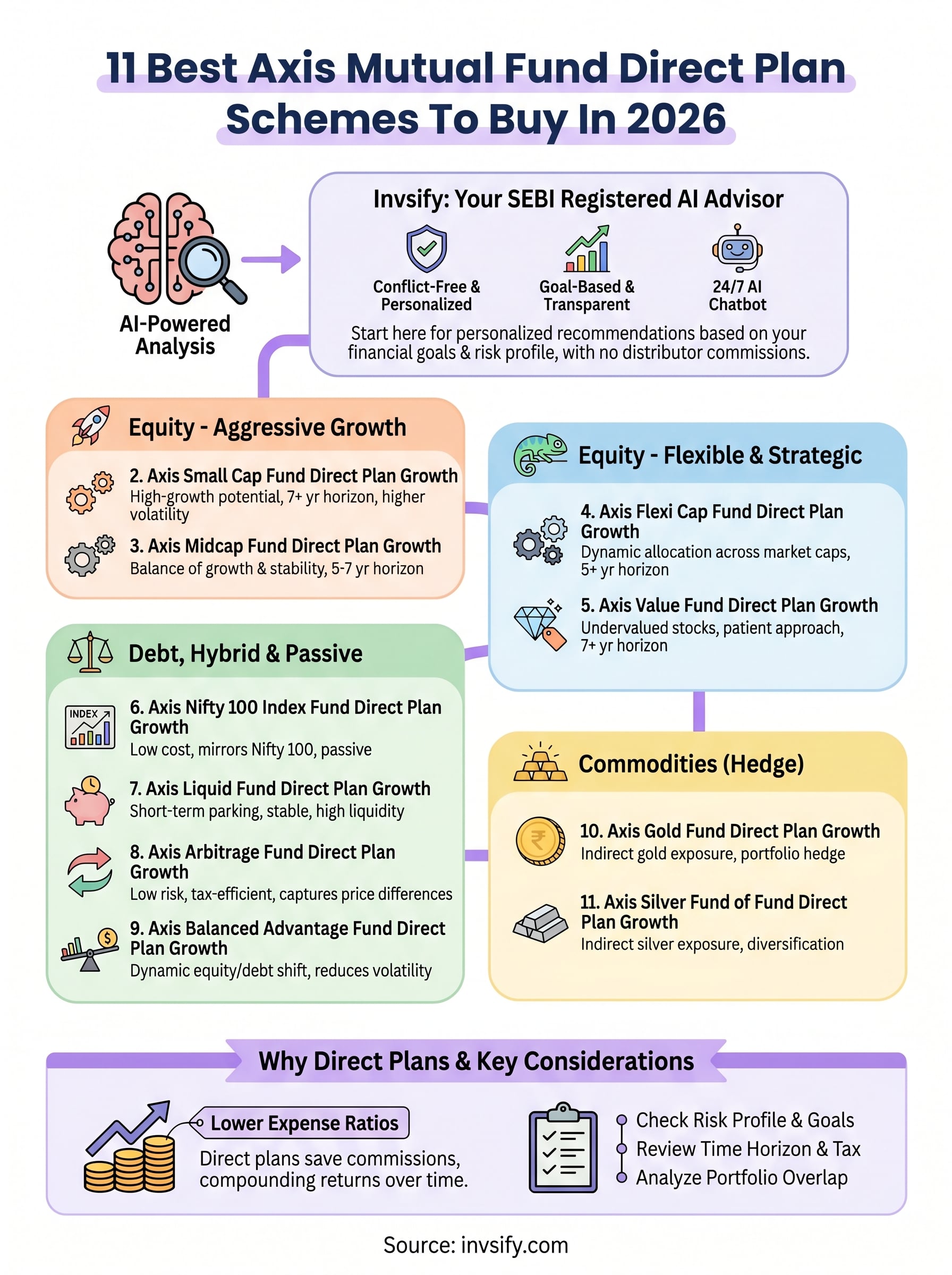

11 Best Axis Mutual Fund Direct Plan Schemes To Buy In 2026

Shlok Sobti

11 Best Axis Mutual Fund Direct Plan Schemes To Buy In 2026

Axis Mutual Fund is one of India's most recognized fund houses, managing assets worth over ₹2.7 lakh crore. Their direct plans, where you invest without a distributor, come with lower expense ratios, which means more of your money actually works for you. If you've been exploring Axis Mutual Fund direct plan options, you already know the lineup is extensive, spanning large-cap, mid-cap, small-cap, flexi-cap, ELSS, and debt categories.

But picking the right scheme isn't just about past returns. It requires looking at risk-adjusted performance, fund manager track record, portfolio composition, and how a fund fits your specific financial goals. That's exactly where most investors, especially those relying on random online tips, tend to stumble. A wrong pick can silently drag your wealth growth down for years.

At Invsify, we're a SEBI Registered Investment Advisor that uses AI-powered analysis to help you cut through the noise and invest in schemes that genuinely align with your risk profile and goals, without any hidden commissions eating into your returns. This list of 11 best Axis Mutual Fund direct plan schemes for 2026 is built on that same data-driven approach, giving you a clear starting point for smarter investing decisions.

1. Invsify AI advisor for Axis direct plans

Before you pick any specific scheme from this list, you need a reliable framework to evaluate your options. Invsify is a SEBI Registered Investment Advisor that uses AI-powered analysis to help you invest in Axis direct plans based on your actual financial goals, not someone else's commission incentive.

What it is

Invsify combines AI-driven portfolio analysis with conflict-free investment advisory to recommend the most suitable direct mutual fund schemes for your situation. Unlike a distributor who earns commissions from pushing certain funds, Invsify operates on a transparent advisory model where every recommendation is built around your financial interests.

You get a personalized Wealth Wellness Score, real-time portfolio tracking, and a conversational AI that's available 24/7. The platform covers the full range of Axis Mutual Fund direct plan categories, including equity, debt, hybrid, and commodity funds.

Who it suits best

Invsify works best for salaried individuals who want professional guidance without paying distributor markups embedded in regular plans. It suits both first-time investors who need direction and experienced investors looking to optimize an existing portfolio.

Investors shifting from regular to direct plans and needing expert support

People who want data-backed recommendations instead of forum tips

Those looking to align their investments with a tax-efficient, goal-based strategy

What to check before you commit

Review your current financial goals clearly before onboarding, whether that's wealth accumulation, capital protection, or tax saving. Invsify's risk profiling process works best when you input accurate information about your income, liabilities, and investment horizon.

The more honest your inputs during risk profiling, the more precisely the AI tailors its fund recommendations to your actual situation.

You should also check whether your existing investments have any lock-in periods or exit loads before making changes based on new recommendations.

Costs, fees, and taxes

Invsify charges a transparent advisory fee directly, rather than earning trail commissions from fund houses. Since you invest in direct plans, you skip the distributor commission layer that quietly reduces your returns in regular plans. Tax treatment depends entirely on the underlying fund category you choose, such as equity or debt classification, and your holding period.

How to get started online

Visit invsify.com, complete your KYC and risk profiling, and the AI generates personalized Axis fund recommendations within minutes. The entire process is digital, and you can use the AI chatbot anytime for ongoing queries or portfolio reviews.

2. Axis Small Cap Fund direct plan growth

The Axis Small Cap Fund direct plan growth option targets companies ranked below the top 250 by market capitalization. This fund has built a consistent track record by focusing on high-growth businesses that are still in early expansion stages, making it one of the more compelling small-cap offerings in the Indian market.

What it is

This fund invests a minimum of 65% of its corpus in small-cap stocks, with the flexibility to hold mid-cap and large-cap stocks for stability. As an axis mutual fund direct plan, it carries a lower expense ratio compared to its regular counterpart, which directly improves your net returns over a long holding period.

Choosing the direct plan over the regular plan in this category can save you anywhere from 0.5% to 1% annually in expense ratio, which compounds significantly over 10 or more years.

Who it suits best

This fund suits investors with a 7-plus year horizon who can tolerate sharp short-term volatility in exchange for higher long-term growth potential. It works well for salaried individuals in their 30s who have stable income and want aggressive wealth accumulation alongside more conservative holdings.

What to check before you commit

Check the rolling returns over 5 and 7-year periods, not just 1-year performance. Small-cap funds can deliver misleading short-term numbers. Also review the fund's portfolio concentration in specific sectors before investing.

Costs, fees, and taxes

The direct plan expense ratio typically sits below 0.5%. Exit load of 1% applies if you redeem within 12 months. Gains held beyond one year are taxed as long-term capital gains at 12.5% above ₹1.25 lakh.

How to get started online

You can invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website after completing your KYC.

3. Axis Midcap Fund direct plan growth

The Axis Midcap Fund direct plan growth targets companies ranked between 101 and 250 by market capitalization. Mid-cap stocks offer a balance between large-cap stability and small-cap aggression, giving you above-average growth potential with relatively better risk management than a pure small-cap allocation.

What it is

This fund maintains a minimum of 65% allocation in mid-cap stocks, with the remaining portion deployed across large-cap and small-cap companies depending on market conditions. As an axis mutual fund direct plan, it carries a lower expense ratio than the regular plan, which compounds meaningfully over a 5-plus year holding period.

Choosing the direct plan over the regular plan in this category can save you 0.5% to 1% annually, which translates into a significant rupee difference over a decade.

Who it suits best

Investors with a 5 to 7-year horizon who want more growth than large-cap funds offer but aren't ready for the full volatility of small-cap investing will find this fund well-suited to their needs. Salaried individuals in their mid-career phase building long-term wealth alongside an emergency fund can treat this as a strong core holding.

What to check before you commit

Review the fund's sector concentration and confirm that mid-cap stocks don't already dominate your existing portfolio. Also compare rolling 5-year returns against the Nifty Midcap 150 benchmark before committing fresh capital.

Costs, fees, and taxes

The direct plan expense ratio generally stays below 0.6%. An exit load of 1% applies on redemptions within 12 months. Long-term capital gains beyond ₹1.25 lakh are taxed at 12.5%.

How to get started online

Complete your KYC verification and invest through your SEBI Registered Investment Advisor or via the Axis AMC website directly.

4. Axis Flexi Cap Fund direct plan growth

The Axis Flexi Cap Fund direct plan growth gives the fund manager full flexibility to move allocations across large-cap, mid-cap, and small-cap stocks based on market conditions. This adaptability makes it one of the more versatile options within the Axis Mutual Fund direct plan lineup.

What it is

This fund maintains a minimum 65% allocation in equity across market capitalizations, with no fixed cap on how much goes into each segment. The fund manager actively shifts weights depending on where the strongest risk-adjusted opportunities exist at any given time. That dynamic approach distinguishes it from pure large-cap or mid-cap funds with rigid mandates.

A flexi-cap fund gives your portfolio a built-in buffer during market cycles since the manager can reduce small-cap exposure when volatility spikes and rotate into more stable large-caps.

Who it suits best

Investors who want equity market exposure without deciding the market-cap split themselves will find this fund a strong fit. It works well for salaried individuals with a 5-plus year horizon who prefer a single diversified equity fund over managing multiple category-specific funds.

What to check before you commit

Review the fund's historical allocation shifts across market caps to understand how actively the manager has moved weights. Compare those shifts against broader Nifty 500 benchmark performance to see whether the active calls added real value.

Costs, fees, and taxes

The direct plan expense ratio typically stays below 0.6%. An exit load of 1% applies on redemptions within 12 months. Long-term capital gains above ₹1.25 lakh are taxed at 12.5%.

How to get started online

Complete your KYC process and invest through your SEBI Registered Investment Advisor or directly through the Axis AMC website.

5. Axis Value Fund direct plan growth

The Axis Value Fund direct plan growth follows a value investing strategy, targeting stocks that are trading below their intrinsic worth relative to fundamentals. This contrarian approach means the fund often holds positions that the broader market is currently overlooking, betting on a price correction over time.

What it is

This fund invests a minimum of 65% of its corpus in value-oriented equities across market capitalizations, with the fund manager identifying stocks with strong underlying businesses that the market has temporarily mispriced. As an axis mutual fund direct plan, it carries a lower expense ratio than the regular plan version, letting you retain a larger share of the returns as the value thesis plays out.

Value funds tend to underperform during momentum-driven bull markets but often outperform significantly during market recoveries, which makes your holding period critical.

Who it suits best

This fund suits patient investors with a 7-plus year horizon who understand that value investing rewards discipline over timing. It works well for salaried individuals who want diversified equity exposure without chasing high-valuation momentum stocks that dominate other fund categories.

What to check before you commit

Review the fund's portfolio price-to-earnings ratio relative to the benchmark to confirm the manager is genuinely running a value strategy. Also check sector concentration since value funds can cluster heavily in cyclical sectors like banking, energy, or commodities depending on market conditions.

Costs, fees, and taxes

The direct plan expense ratio generally stays below 0.7%. An exit load of 1% applies on redemptions within 12 months. Long-term capital gains above ₹1.25 lakh are taxed at 12.5%.

How to get started online

Complete your KYC verification and invest through your SEBI Registered Investment Advisor or via the Axis AMC website directly.

6. Axis Nifty 100 Index Fund direct plan growth

The Axis Nifty 100 Index Fund direct plan growth takes a passive investing approach, replicating the Nifty 100 index rather than relying on active stock selection. This structure gives you broad exposure to the top 100 companies by market capitalization listed on the NSE, covering large-cap leaders and select mid-cap names within that universe.

What it is

This fund mirrors the Nifty 100 Total Returns Index by holding the same stocks in the same proportions. As an axis mutual fund direct plan, it carries one of the lowest expense ratios in the equity category since there's no active fund management overhead. Your returns closely track the index, minus a small tracking error.

Index funds work best when held long enough that the compounding advantage of a low expense ratio clearly separates your corpus from regular plan investors.

Who it suits best

This fund suits cost-conscious investors who prefer capturing market returns reliably over depending on active fund manager decisions. It works particularly well for:

First-time equity investors building a core passive allocation

Experienced investors seeking a low-cost anchor in a diversified portfolio

What to check before you commit

Review the fund's tracking error over the past 3 years to confirm it closely mirrors the Nifty 100. Also check how much overlap this fund creates with any existing large-cap or flexi-cap holdings in your portfolio before adding fresh capital.

Costs, fees, and taxes

The direct plan expense ratio stays below 0.25%, making this one of the most cost-efficient options in the lineup. Long-term capital gains above ₹1.25 lakh are taxed at 12.5% with no exit load after 30 days.

How to get started online

Complete your KYC process and invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website after linking your bank account.

7. Axis Liquid Fund direct plan growth

The Axis Liquid Fund direct plan growth invests in short-term debt and money market instruments with maturities up to 91 days. This structure makes it one of the most stable and accessible options for investors who need a parking space for surplus cash without locking it away.

What it is

This fund targets high-quality debt instruments including treasury bills, commercial papers, and certificates of deposit. As an axis mutual fund direct plan, the expense ratio stays significantly lower than regular plan variants, which matters more in a low-return debt category where every basis point counts.

In a liquid fund, even a 0.1% difference in expense ratio has a proportionally larger impact on your net return compared to an equity fund delivering 12% to 15% annually.

Who it suits best

This fund works best for salaried individuals who want a safer, more flexible alternative to a savings account for their short-term surplus funds. It suits investors building an emergency fund or holding cash between two equity investments.

What to check before you commit

Review the fund's credit quality profile to confirm it holds predominantly AAA-rated and sovereign instruments. Also verify the average maturity stays short, since longer maturities in a liquid fund can introduce unexpected interest rate sensitivity.

Costs, fees, and taxes

The direct plan expense ratio typically stays below 0.2%. Gains are taxed as short-term capital gains and added to your income if held under three years, so tax efficiency improves with longer holding periods.

How to get started online

Complete your KYC process and invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website.

8. Axis Arbitrage Fund direct plan growth

The Axis Arbitrage Fund direct plan growth captures price differences between the cash and futures markets for the same stock, locking in low-risk gains without taking directional bets on market movement.

What it is

This fund simultaneously buys stocks in the cash market and sells equivalent futures contracts, pocketing the price gap as profit. As an axis mutual fund direct plan, it carries a lower expense ratio than the regular plan, which matters here because arbitrage returns are already modest by design. The fund qualifies as an equity-oriented fund for taxation purposes since it holds over 65% in equity and equity-related instruments.

Arbitrage funds work best when market volatility is high, since wider price spreads between the cash and futures segments create more profitable opportunities for the fund manager.

Who it suits best

This fund suits conservative investors who want equity-like tax treatment without taking on meaningful stock market risk. It works particularly well for:

Salaried individuals in the 20% or 30% tax bracket seeking short-term parking with better post-tax returns than a savings account

Investors waiting to deploy capital into equity who want a low-risk holding zone

What to check before you commit

Review the fund's annualized returns over 1 and 3-year periods and compare them against liquid fund returns for the same window. Also confirm that arbitrage spreads in the market are wide enough to justify staying invested, since returns compress sharply during low-volatility periods.

Costs, fees, and taxes

The direct plan expense ratio typically stays below 0.4%. An exit load of 0.25% applies on redemptions within 30 days. Gains held beyond one year are taxed as long-term capital gains at 12.5% above ₹1.25 lakh.

How to get started online

Complete your KYC verification and invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website after linking your bank account.

9. Axis Balanced Advantage Fund direct plan growth

The Axis Balanced Advantage Fund direct plan growth dynamically shifts its allocation between equity and debt based on market valuations, reducing equity exposure when markets look expensive and increasing it when they offer better value. This built-in rebalancing makes it a compelling option within the axis mutual fund direct plan lineup for investors who want equity upside without full market exposure.

What it is

This fund uses a model-driven approach to determine equity and debt allocation at any given point, typically ranging between 30% and 80% in net equity depending on market conditions. The debt and arbitrage portion acts as a stabilizer during market downturns, smoothing out the volatility that a pure equity fund would deliver.

The dynamic allocation model removes the need for you to time the market yourself, which is where most individual investors tend to make costly mistakes.

Who it suits best

This fund works well for conservative to moderate investors who want equity participation without the sharp drawdowns that come with pure equity funds. It suits salaried individuals approaching their mid-40s or 50s who want to grow wealth while gradually reducing risk as their financial goals near.

What to check before you commit

Review the fund's equity allocation history over the past 3 to 5 years to understand how aggressively the model shifts weights. Also check whether the fund's risk-adjusted returns justify its positioning against both pure equity and hybrid conservative peers.

Costs, fees, and taxes

The direct plan expense ratio typically stays below 0.8%. An exit load of 1% applies on redemptions within 12 months. Tax treatment follows equity fund rules since net equity usually stays above 65%.

How to get started online

Complete your KYC verification and invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website.

10. Axis Gold Fund direct plan growth

The Axis Gold Fund direct plan growth invests in units of the Axis Gold ETF, giving you indirect exposure to domestic gold prices without the hassle of physical storage or making charges. It tracks the price of 24-karat gold and reflects the return that gold generates in Indian rupee terms.

What it is

This fund is a fund of fund (FoF) structure that routes your investment through the underlying Axis Gold ETF. As an axis mutual fund direct plan, it carries a lower expense ratio than the regular variant, which helps since gold funds already operate on thin return margins. The fund qualifies as a non-equity fund for taxation purposes.

Gold funds work best as a portfolio hedge rather than a standalone wealth builder, since gold's long-term return tends to lag diversified equity over multi-decade periods.

Who it suits best

This fund suits investors who want gold exposure without managing a demat account to hold ETF units directly. It works well for salaried individuals who want to allocate 5% to 10% of their overall portfolio to gold as a hedge against inflation or currency depreciation.

What to check before you commit

Review your existing gold exposure across jewelry, sovereign gold bonds, or other gold funds before adding this. Also confirm that your overall portfolio allocation to gold doesn't cross 15%, since over-concentration reduces the diversification benefit gold is supposed to provide.

Costs, fees, and taxes

The direct plan expense ratio typically stays below 0.15%. Gains are taxed as short-term or long-term capital gains depending on your holding period, with long-term gains taxed at 12.5% after 24 months.

How to get started online

Complete your KYC process and invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website after linking your bank account.

11. Axis Silver Fund of Fund direct plan growth

The Axis Silver Fund of Fund direct plan growth gives you indirect exposure to domestic silver prices by investing in units of the Axis Silver ETF. It mirrors silver's price movement in Indian rupee terms without requiring you to handle physical storage or operate a demat account for ETF units.

What it is

This fund routes your capital through the underlying Axis Silver ETF, making it a fund of fund structure. As an axis mutual fund direct plan, the direct variant carries a lower expense ratio than the regular plan, which matters in a commodity-linked fund where returns are entirely price-driven rather than active management decisions. The fund qualifies as a non-equity fund for taxation purposes.

Silver plays a dual role as both a precious metal and an industrial commodity, which means its price can diverge sharply from gold depending on global manufacturing and technology demand cycles.

Who it suits best

This fund suits investors who want commodity diversification beyond gold within their portfolio. It works best for salaried individuals allocating a small portion of their overall portfolio, typically 5% or less, to silver as a supplementary hedge rather than a primary wealth-building vehicle.

What to check before you commit

Review your total commodity exposure across existing gold funds, sovereign gold bonds, and any silver holdings before adding this fund. Also verify that silver's industrial demand outlook aligns with your investment horizon, since silver prices tend to be more volatile than gold during economic slowdowns.

Costs, fees, and taxes

The direct plan expense ratio typically stays below 0.35%. Gains are taxed as short-term or long-term capital gains based on your holding period, with long-term gains taxed at 12.5% after 24 months.

How to get started online

Complete your KYC verification and invest through your SEBI Registered Investment Advisor or directly via the Axis AMC website after linking your bank account.

Next steps

Choosing the right axis mutual fund direct plan comes down to matching each fund's risk profile with your own financial goals, not chasing the best recent return number. Every scheme on this list serves a specific purpose, whether that's aggressive wealth accumulation through small-cap exposure, stable short-term parking via a liquid fund, or commodity hedging through gold and silver.

Before you invest, run an honest audit of your existing portfolio, your time horizon, and your tax situation. Picking funds without that foundation is how investors end up with overlapping holdings that don't actually reduce risk.

If you want personalized guidance built around your specific goals and income, Invsify's AI-powered advisory platform gives you conflict-free recommendations without the distributor commission layer that quietly erodes your returns in regular plans. Start your free risk profiling on Invsify and get a Wealth Wellness Score that tells you exactly where your portfolio stands today.