Axis Mutual Fund Retirement Plan: Plans, NAV, Calculator

Shlok Sobti

Axis Mutual Fund Retirement Plan: Plans, NAV, Calculator

Planning for retirement isn't something you figure out the night before you stop working. It takes years of disciplined investing, and picking the right fund matters. The Axis Mutual Fund retirement plan is one option that consistently comes up for Indian investors looking to build a dedicated retirement corpus through mutual funds. With three distinct sub-plans, Aggressive, Dynamic, and Conservative, it offers flexibility based on your risk appetite and how close you are to retirement.

But choosing a plan is only half the battle. You also need to understand current NAV, historical returns, and how much you'd actually need to invest monthly to hit your retirement goal. That's where tools like retirement calculators come in, and where platforms like Invsify can help you cut through the noise with AI-powered, conflict-free advice tailored to your financial situation.

This article breaks down everything you need to know about Axis Mutual Fund's retirement plans, the plan types, their performance, how the calculator works, and what to watch out for before you invest.

Why retirement planning needs a dedicated strategy

Most people treat retirement as a distant problem, something to deal with after a promotion, after the kids finish school, or after the home loan is paid off. That mindset is costly. Inflation in India has averaged around 5-6% annually, which means the cost of living roughly doubles every 12 to 14 years. If you plan to retire in 25 years, the monthly expenses you have today could be three times higher by then. Starting late or investing in the wrong instruments makes that gap almost impossible to close.

Retirement is different from other financial goals

Unlike saving for a car or a vacation, retirement has no safety net if you fall short. You cannot take a loan to fund your living expenses at 65. The corpus you build must last 20 to 30 years after you stop earning, which means you need growth during the accumulation phase and stability during withdrawal. General savings accounts or fixed deposits rarely deliver both. That's why purpose-built options like the axis mutual fund retirement plan, which separates investors by risk profile and investment horizon, exist in the first place.

Retirement planning works best when your investment strategy actively adapts as you get older, shifting from high-growth assets toward capital protection.

Why a random mix of funds does not work

Picking a random set of equity and debt funds does not constitute a retirement strategy. Rebalancing, tax efficiency, and withdrawal sequencing all matter enormously over a 20-year horizon. Without a structured plan, you risk being too aggressive when markets fall near your retirement date, or too conservative when you still have decades of compounding ahead. A dedicated retirement fund handles much of this automatically, making it easier to stay on track without constant portfolio tinkering.

What Axis mutual fund retirement plan means

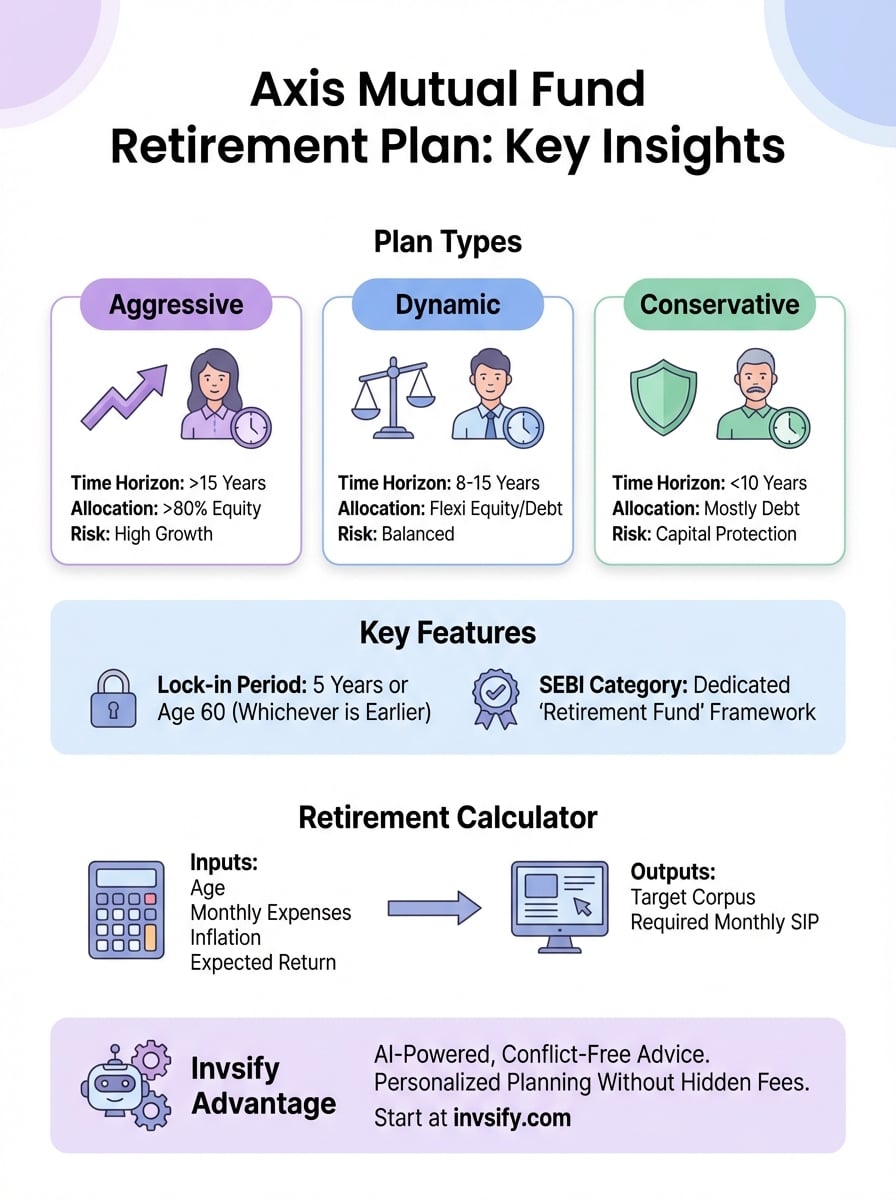

The Axis Mutual Fund retirement plan is a dedicated scheme that pools your money into a mix of equity and debt instruments, with the specific allocation depending on which sub-plan you choose. Unlike a standard equity or debt fund, its primary objective is retirement corpus creation, which shapes everything from how the fund is managed to the tax treatment you receive.

This fund falls under the SEBI-defined "Retirement Fund" category, which means it comes with a mandatory lock-in period of five years or until you turn 60, whichever is earlier.

How it differs from regular mutual funds

A regular mutual fund has no built-in purpose tied to your life stage. The Axis Mutual Fund retirement plan, by contrast, is designed with a long investment horizon in mind. The lock-in period discourages premature withdrawals, which helps you stay invested through market volatility instead of pulling out during a downturn. This structural discipline is something a typical equity fund simply does not enforce.

Beyond the lock-in, this fund is specifically categorized under SEBI's retirement fund guidelines, which means regulatory oversight is directly tied to long-term wealth preservation. Your investment benefits from a clear framework that standard funds do not operate within, giving you more predictability in how the fund behaves over time.

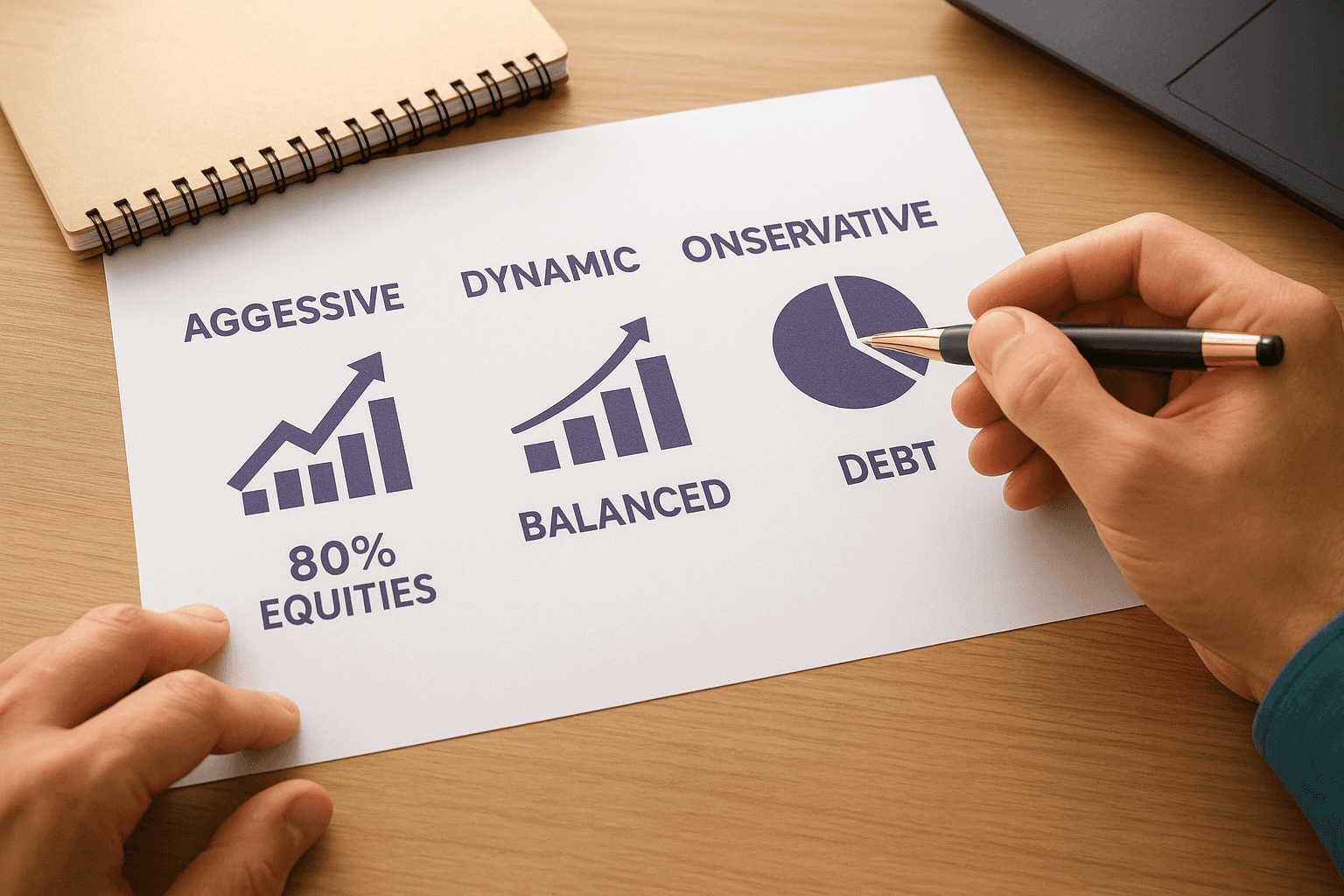

Aggressive, dynamic, and conservative plans compared

The axis mutual fund retirement plan comes in three variants, each targeting a different investor profile. Choosing the right one depends on how many years you have before retirement and how much short-term volatility you can stomach without making panic-driven decisions.

Aggressive plan: built for long horizons

Equities make up 80% or more of the Aggressive Plan, which gives it stronger long-term growth potential. This plan suits investors who are at least 15 to 20 years away from retirement and can ride out market corrections without losing sleep.

The longer your time horizon, the more market volatility works in your favor rather than against you.

Dynamic and conservative: matching your stage

Unlike the Aggressive Plan, the Dynamic Plan shifts its equity-debt allocation based on market valuations, reducing equity exposure when markets are expensive. This makes it a practical middle ground for investors who are 8 to 15 years from retirement.

The Conservative Plan focuses on debt instruments, keeping equity exposure minimal to protect your corpus. This plan suits investors within five to ten years of retirement who cannot afford significant losses before they stop working.

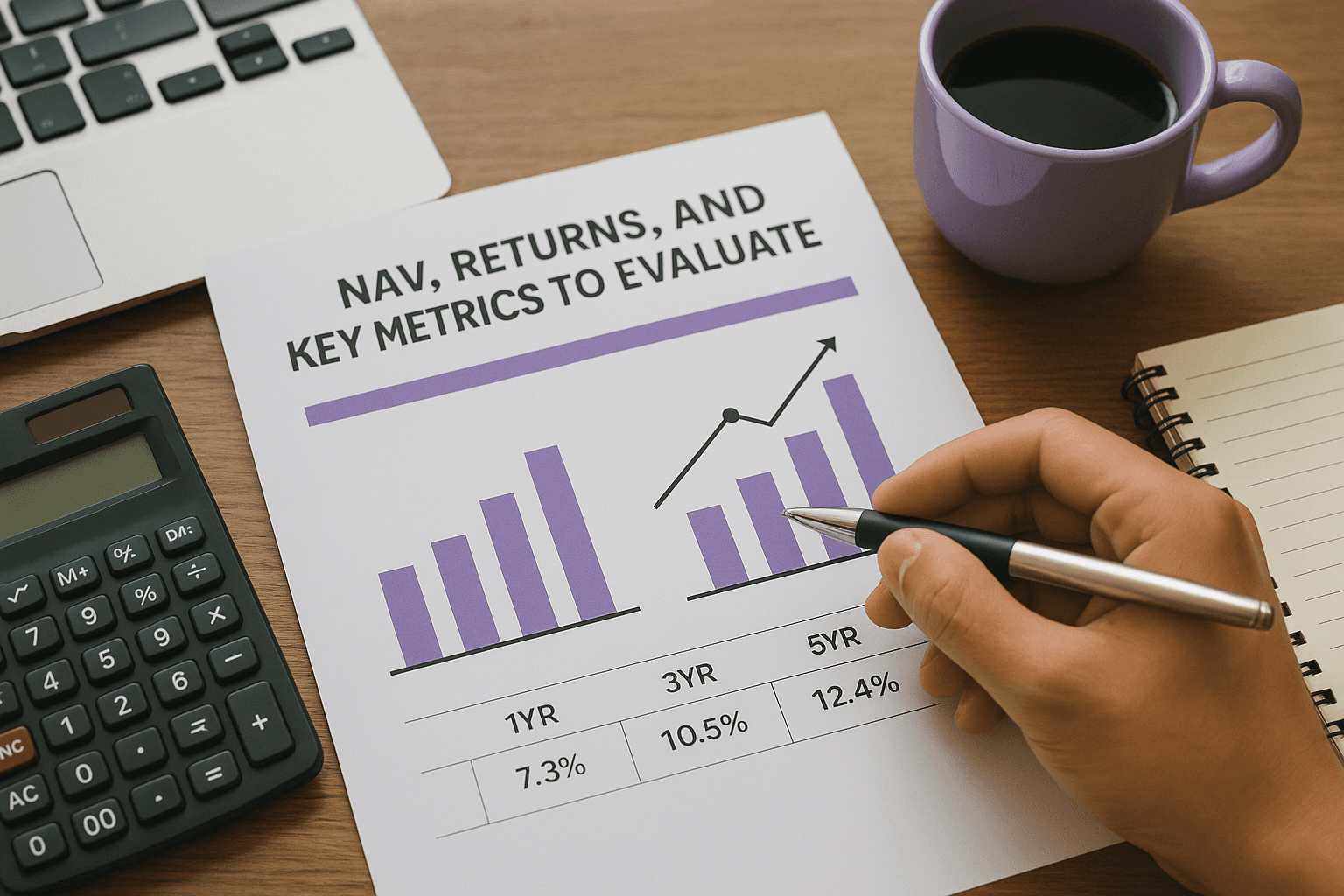

NAV, returns, and key metrics to evaluate

The NAV (Net Asset Value) of a mutual fund represents the per-unit price at which you buy or redeem your investment. For the axis mutual fund retirement plan, NAV updates daily based on the performance of the underlying portfolio. Tracking NAV alone gives you limited insight. You need to pair it with returns data and a few other metrics before making any decision.

What returns actually tell you

Historical returns show how each sub-plan has performed across 1-year, 3-year, and 5-year windows. The Aggressive Plan has delivered stronger long-term returns than the Conservative Plan, but it also swings harder during market corrections. Comparing returns over five years or more gives you a much more realistic picture than focusing on recent performance.

Always evaluate returns against the fund's benchmark index, not in isolation.

Other metrics worth checking

Expense ratio directly reduces your net returns, and a difference of even 0.5% compounds into a significant loss over a 20-year horizon. Alpha and Sharpe ratio tell you whether the fund earns returns proportionate to the risk it takes on. Before committing capital, verify these figures through your fund statement or the AMFI website.

How to plan and invest using a retirement calculator

A retirement calculator takes the guesswork out of investing by showing you how much you need to invest monthly to reach a specific corpus. For the axis mutual fund retirement plan, you input your current age, expected retirement age, monthly expenses today, and assumed inflation rate. The calculator then outputs a target corpus figure and the SIP amount required to get there.

Inputs that actually matter

Your expected monthly expenses in retirement and your assumed rate of return are the two variables that swing your result the most. A conservative return assumption of 10-12% for the Aggressive Plan gives you a more realistic target than using peak historical figures. Adjusting your inflation assumption to 6% rather than 4% also prevents you from underestimating your future needs.

Underestimating inflation is one of the most common reasons retirement plans fall short.

What to do with the output

Once you have your target SIP figure, cross-check it against your current income and expenses. If the number feels out of reach, starting smaller and increasing your SIP by 10% every year using a step-up feature can close the gap without straining your monthly budget significantly.

Your next steps

You now have a clear picture of how the axis mutual fund retirement plan works, what each sub-plan offers, and how to use a calculator to set a realistic SIP target. The next step is putting that knowledge to work. Pick the plan that matches your time horizon, set up a SIP you can sustain, and commit to increasing it annually as your income grows.

Retirement planning does not reward perfection. It rewards consistency. Starting with a smaller amount today outperforms waiting for the "right" time to invest a larger sum. Every year you delay shrinks your compounding window and forces a higher monthly contribution later.

If you want conflict-free, AI-powered guidance to help you decide which plan fits your situation and how much you actually need to invest, start your retirement planning with Invsify. You get personalized advice without the hidden fees that traditional distributors charge.