Benefits Of Direct Mutual Funds: Lower Costs, Higher Returns

Shlok Sobti

Benefits Of Direct Mutual Funds: Lower Costs, Higher Returns

Every year, lakhs of Indian investors quietly lose a portion of their mutual fund returns to distributor commissions they never explicitly agreed to pay. The difference between a regular mutual fund plan and a direct one might look small on paper, often just 0.5% to 1.5%, but compounded over 10, 15, or 20 years, that gap turns into lakhs of rupees. Understanding the benefits of direct mutual funds is the first step toward keeping more of what your money earns, and it starts with knowing exactly where your returns are going.

Direct mutual funds cut out the middleman. No distributor commissions, no embedded fees eating into your NAV. The result? A lower expense ratio and a higher NAV compared to regular plans of the same scheme. For salaried individuals building long-term wealth, whether for retirement, a child's education, or financial independence, this cost advantage compounds significantly over time.

At Invsify, we exist to make this shift simple. As a SEBI Registered Investment Advisor, we provide conflict-free, AI-powered investment recommendations with zero distributor commissions baked in. Our goal is to help you invest in what's right for you, not what pays us more. This article breaks down exactly how direct mutual funds work, why they outperform regular plans, and how much you actually stand to save by making the switch.

Why direct vs regular plans matters for your returns

When you invest in a mutual fund, you pay an annual fee called the expense ratio. In a regular plan, this fee is higher because it includes a commission paid to the distributor who sold you the fund. You never see this fee on a bill. It gets deducted from the fund's NAV every day, silently reducing what your money earns. That's the core problem: you're paying for a service you may not be actively receiving, and the cost compounds against you year after year.

The cost that hides inside your fund

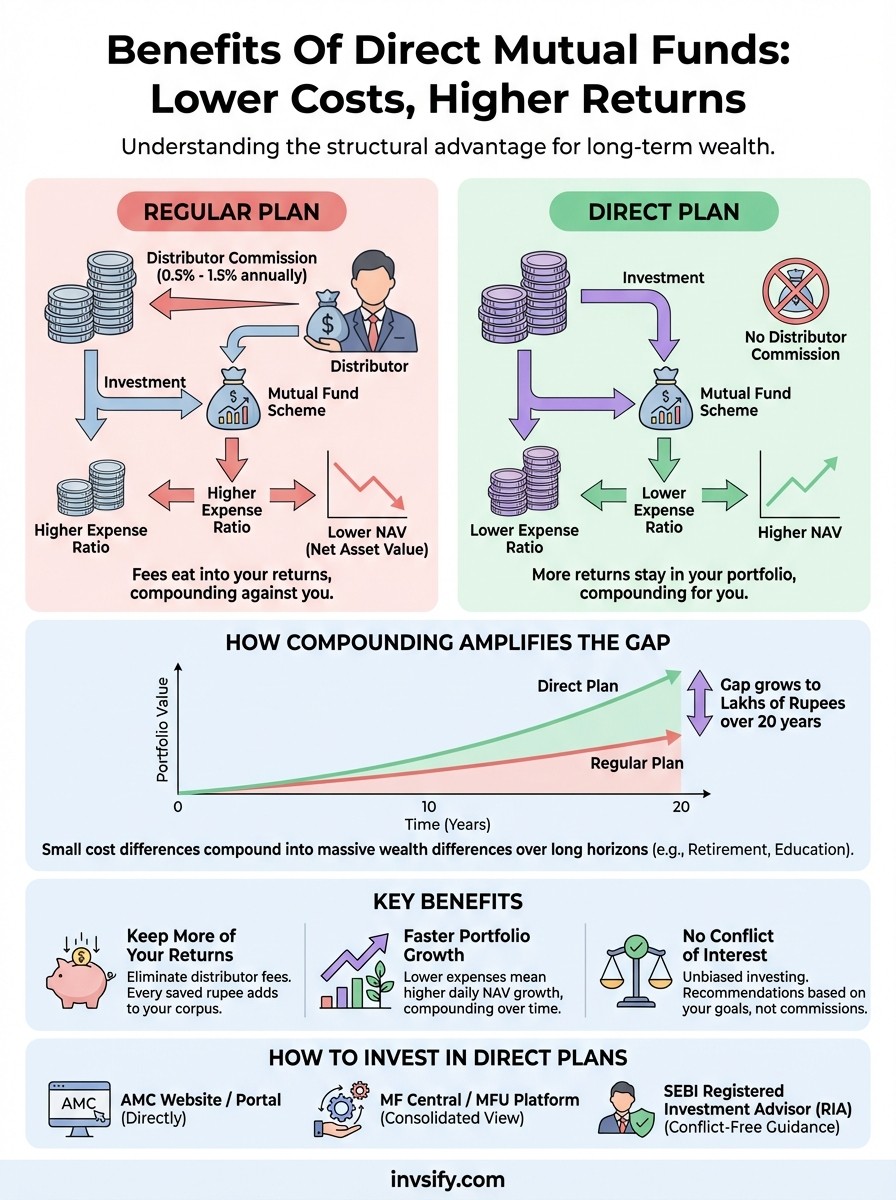

Every mutual fund scheme in India offers two versions: a regular plan and a direct plan. They hold the exact same underlying portfolio and are managed by the same fund manager. The only structural difference is the expense ratio. Regular plans carry a higher expense ratio because the distributor's trail commission gets embedded into it. Direct plans eliminate that commission entirely, which is why they always carry a lower expense ratio and a higher NAV than their regular counterparts within the same scheme.

SEBI mandates that AMCs disclose expense ratios, so you can verify this difference yourself on any AMC website or the AMFI portal. For an actively managed equity fund, the gap between a regular and direct plan typically ranges from 0.5% to 1.5% per year. That number sounds modest until you run the math over a long investment horizon.

A 1% annual difference in expense ratio can reduce your final corpus by 20% to 25% over a 20-year investment period.

How compounding amplifies the gap

Compounding works in both directions. When your returns are slightly higher each year, those extra returns also compound. Over a 10-year period, a 1% annual cost difference on a ₹10 lakh investment growing at 12% annually leaves you with roughly ₹31 lakhs in a direct plan versus around ₹28.4 lakhs in a regular plan. That's a gap of nearly ₹2.6 lakhs from a single percentage point. Extend that to 20 years, and the same gap grows to well over ₹15 lakhs on that one investment alone.

This is precisely why understanding the benefits of direct mutual funds matters most for long-term investors. Salaried individuals investing through monthly SIPs for goals like retirement or a child's education are doing exactly the kind of investing where this cost gap causes the most damage. Small monthly contributions compounded over decades amplify both gains and losses in costs.

Why the gap isn't always obvious

Most investors never notice the regular vs. direct cost difference because distributors don't send you a bill. The commission comes out of the fund's NAV before you ever see your returns. If your fund returned 13% in a year and the distributor took 1%, you see 12% and assume that's the full market performance. You have no visible reference point to compare against, which is why millions of investors stay in regular plans for years without realizing how much they're giving away.

This lack of transparency is a structural design issue, not an accident. Regular plans are sold because they're profitable for distributors, not because they deliver better outcomes for investors. Switching to direct plans removes this conflict of interest completely and puts that annual cost difference back to work inside your own portfolio.

Direct vs regular plans: the differences that matter

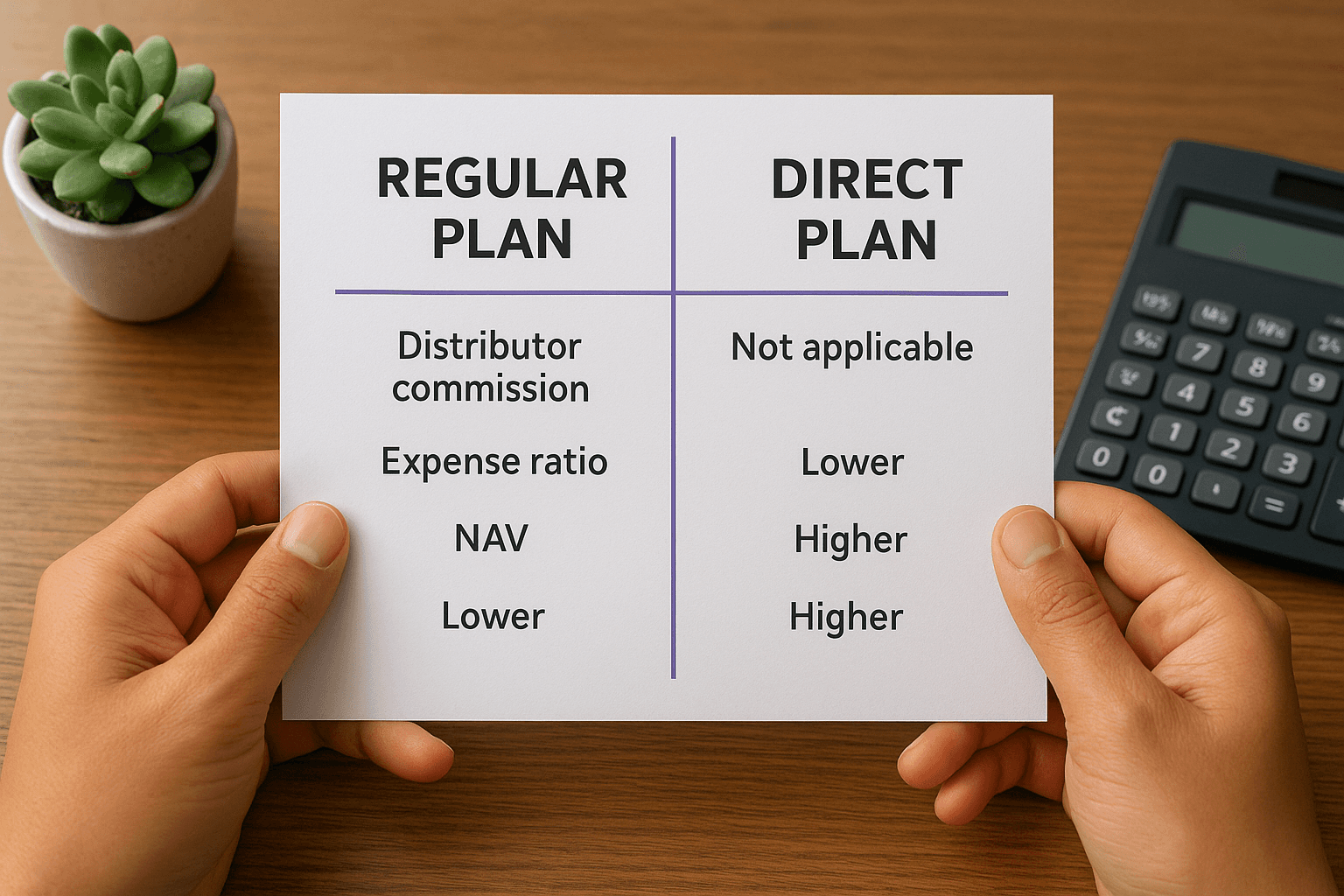

Both plans invest in the same fund, managed by the same team, holding the same stocks or bonds. The only structural difference is how the fund is distributed and what that costs you. In a regular plan, the AMC pays a trail commission to the distributor every year, typically between 0.5% and 1.5% of your invested amount, and that cost is embedded into the expense ratio. In a direct plan, no distributor exists in the chain, so that commission disappears entirely.

What this looks like in the NAV

Because direct plans carry a lower expense ratio, the fund retains more of its gross returns each day. That difference gets reflected in the NAV. Since both plans launched separately (SEBI mandated direct plans starting January 2013), their NAVs have diverged continuously. A direct plan's NAV is always higher than the regular plan of the same scheme on the same date, and that gap widens every year. You can verify this on any AMC's website or the AMFI portal.

The longer you stay invested, the wider the NAV gap grows, which means switching from regular to direct becomes more valuable the earlier you do it.

A side-by-side comparison

The table below captures the core differences clearly.

Feature | Regular Plan | Direct Plan |

|---|---|---|

Distributor commission | Included in expense ratio | Not applicable |

Expense ratio | Higher | Lower |

NAV | Lower | Higher |

Who handles transactions | Distributor or agent | You or a registered advisor |

Conflict of interest | Possible (distributor earns more for certain funds) | None |

SEBI regulation | Yes | Yes |

Where the real benefit shows up

The benefits of direct mutual funds become most visible when you compare long-term wealth accumulation. Both plans produce the same gross return from the market, but the direct plan keeps more of it in your account. For a salaried investor running a ₹15,000 monthly SIP in an equity fund over 20 years, the cost gap alone can translate to a difference of ₹20 to ₹30 lakhs in the final corpus, depending on the scheme. That's not a marginal improvement. That's a meaningful portion of a retirement goal lost solely to distribution costs you never saw.

Benefits of direct mutual funds

The benefits of direct mutual funds go beyond just saving on fees. When you invest in a direct plan, you gain a structural cost advantage that rebuilds itself every single day your money stays invested. Every basis point you save on expenses translates directly into higher NAV growth, which then compounds forward. For a long-term investor, especially a salaried individual building wealth through SIPs, this shift in structure is one of the most reliable ways to improve your final corpus without taking on any additional market risk.

You keep more of every rupee earned

Direct plans carry a lower expense ratio than regular plans because there is no distributor commission embedded in the fee. This means the AMC deducts less from your fund's gross returns each day before calculating the NAV. Over one year, the difference may look modest. Over ten or twenty years, it means thousands to lakhs of rupees staying in your portfolio rather than flowing to a distributor. You do not need to outperform the market to see this benefit. It kicks in automatically, every day, just by being in the direct version of a fund.

Your portfolio compounds faster over time

Because your expense ratio is lower, your NAV grows at a slightly higher rate each year in a direct plan compared to the regular version of the same scheme. That higher annual growth then compounds on itself. A direct plan investor and a regular plan investor holding the same fund, investing the same amount at the same time, will see a widening gap in portfolio value year after year, with no difference in market exposure, fund manager decisions, or portfolio holdings driving it. The only driver is cost, and it works in your favor from day one.

Over a 15-year SIP in an equity fund, a 1% annual cost saving can add 15% to 20% more to your final corpus compared to a regular plan.

You remove the conflict of interest from your investments

When you invest through a distributor, their income depends on which funds they sell. That creates a built-in incentive to steer you toward higher-commission products, regardless of whether those products fit your goals or risk profile. Direct plans eliminate that dynamic entirely. You make decisions based on what suits your financial objectives and risk appetite, not on what generates trail commission for an intermediary. Paired with a SEBI Registered Investment Advisor who charges a transparent fee, this structure gives you genuinely unbiased guidance.

When direct mutual funds may not be the best choice

Direct mutual funds offer a clear cost advantage, but that advantage only materializes if you use it correctly. For many investors, the challenge is not the structure of direct plans itself but the discipline, knowledge, and time required to navigate them without guidance. Knowing when direct plans work against you is just as important as understanding why they work.

If you rely on your distributor for financial planning

Many investors use their distributor as their primary source of financial guidance. They ask questions, get fund recommendations, and receive reminders to stay invested during market downturns. When you switch to direct plans without replacing that support structure, you lose those touchpoints entirely. Without a clear investment plan or an advisor helping you stay on track, there is a real risk of making reactive decisions, switching funds at the wrong time, or picking schemes based on recent performance rather than your actual goals.

If you are currently in this situation, the fix is not to stay in regular plans. It is to replace distributor support with a SEBI Registered Investment Advisor who charges a transparent fee and gives you conflict-free guidance alongside your direct plan investments.

If you don't have time to research and monitor funds

Switching to direct plans places the research responsibility on you. No one is tracking your portfolio, alerting you to fund manager changes, style drift, or underperformance relative to the benchmark. If you invest in direct plans and then ignore your portfolio for years, you may end up in an underperforming fund with no one flagging the issue. The benefits of direct mutual funds only show up consistently when someone is actively monitoring your portfolio and adjusting when the situation calls for it.

Direct plans work best when paired with either strong personal financial knowledge or guidance from a SEBI Registered Investment Advisor who charges a transparent, flat fee.

If you're investing for a short time horizon

The cost savings from direct plans compound most powerfully over long horizons. If you are investing a small amount for a goal that is two or three years away, the absolute rupee difference between a direct and regular plan may be modest. In those cases, the structure of your investment matters far more than the expense ratio gap.

Prioritizing the right asset class and fund category for your goal will drive your outcome more than the plan type in a short window. For short-term goals, focus on that alignment first, and consider the direct versus regular decision as a secondary factor.

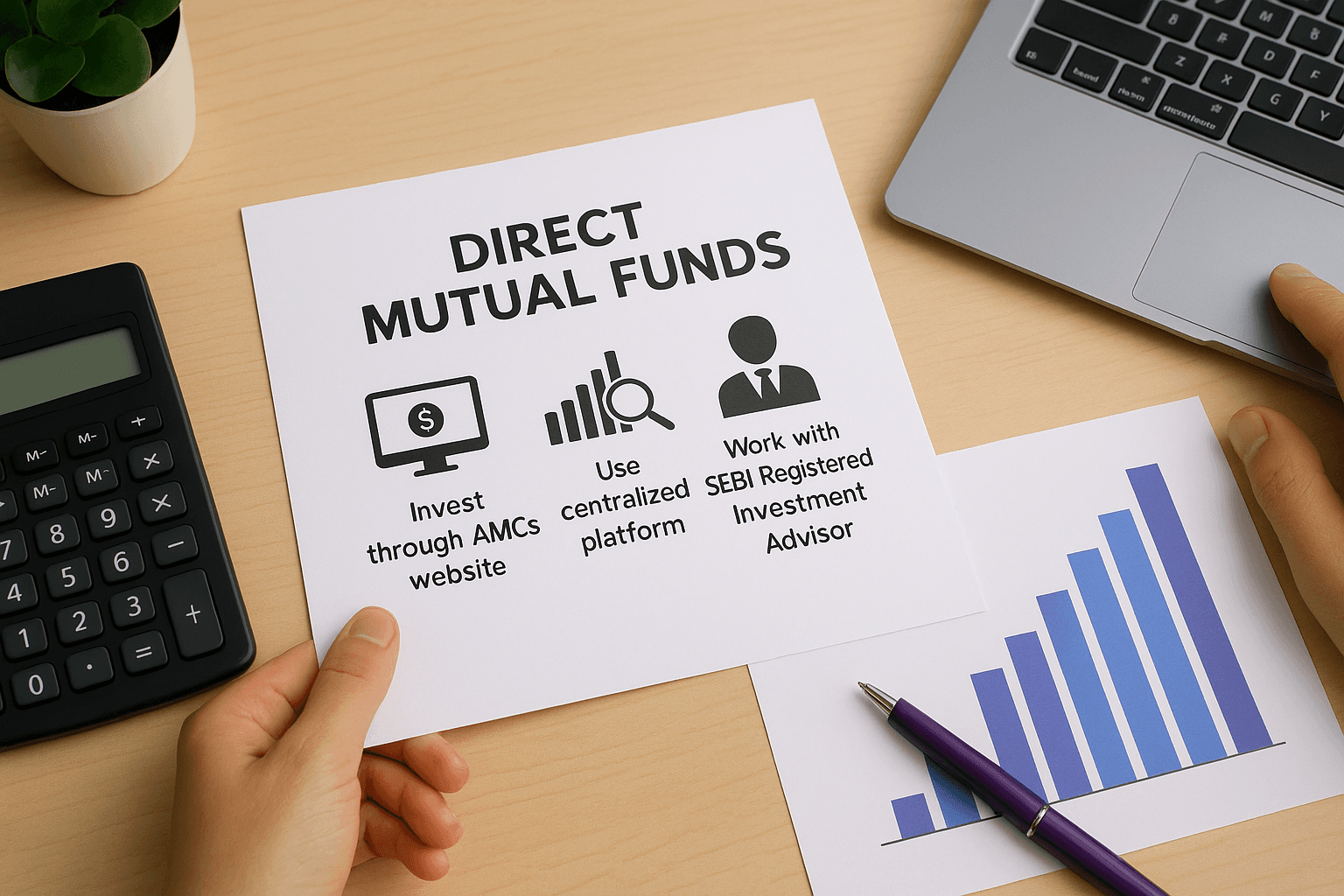

How to invest in direct mutual funds in India

Getting started with direct mutual funds in India is straightforward once you know the available routes. You have three main options: invest directly through the AMC's website, use a centralized platform like MF Central, or work with a SEBI Registered Investment Advisor who places you in direct plans. Each route gives you access to the same lower expense ratio and higher NAV, but they differ in how much support and convenience they offer.

Invest directly through the AMC website

Every Asset Management Company in India, whether it's HDFC Mutual Fund, SBI Mutual Fund, Mirae Asset, or any other, runs its own investor portal where you can invest in direct plans without going through a distributor. You create an account, complete your KYC using Aadhaar and PAN, choose the direct plan of the scheme you want, and set up a lump sum investment or a monthly SIP. This route works well if you already know which funds you want and are comfortable researching and monitoring them yourself.

Use MF Central or MFU for a consolidated view

If you want to invest across multiple AMCs from a single platform, MF Central and MFU (Mutual Fund Utilities) are SEBI-regulated platforms that let you do exactly that. MF Central, jointly operated by CAMS and KFintech, allows you to invest, track, and manage all your mutual fund holdings across fund houses in one place. You can select direct plans specifically during the transaction process. These platforms are free to use and do not charge distribution commissions, which means your investments stay on the direct plan track entirely.

MF Central is accessible at mfcentral.com and is a reliable, regulator-backed platform for managing direct plan investments across AMCs.

Work with a SEBI Registered Investment Advisor

The most practical route for most salaried investors is to access the benefits of direct mutual funds through a SEBI Registered Investment Advisor (RIA). An RIA is legally required to act in your interest, charge you a transparent advisory fee, and place you only in direct plans with no trail commission involved. You get fund selection, portfolio monitoring, and rebalancing guidance, without any conflict of interest built into the relationship. This approach captures the full cost advantage of direct plans while ensuring your investment decisions stay aligned with your actual financial goals.

How switching from regular to direct works

Switching from a regular plan to a direct plan of the same mutual fund scheme is not a transfer. It is a full redemption and fresh purchase in tax and regulatory terms. Your existing units in the regular plan get sold at the current NAV, and new units are purchased in the direct plan at its current NAV. This means the switch is a taxable event, and you need to account for short-term or long-term capital gains depending on how long you have held those units before acting.

Understanding the tax implications before you switch

Before you initiate any switch, check how long you have held your regular plan units. For equity funds, gains on units held for more than one year qualify as long-term capital gains and are taxed at 12.5% above ₹1.25 lakh per year. Gains on units held for under a year are taxed at 20% as short-term capital gains. For debt funds, all gains are added to your income and taxed at your applicable slab rate regardless of holding period. Running this calculation before switching helps you time the move in a tax-efficient way, often by switching units that have crossed the one-year mark first.

If your regular plan units have accumulated large unrealized gains, switching everything at once can trigger a significant tax liability, so stagger the switch where it makes financial sense.

How to execute the switch

You can initiate the switch directly on the AMC's investor portal by logging in, selecting the regular plan folio, and using the switch option to move to the direct plan of the same scheme. MF Central also supports this process across multiple AMCs from a single interface. Before confirming, verify that no exit load applies to your units, since some funds charge an exit load for units redeemed within one year. Once the switch processes, your new direct plan units start benefiting from the lower expense ratio immediately.

Setting up future investments correctly

After switching, ensure that any future SIP contributions or lump sum investments go into the direct plan folio and not the regular plan by default. Platforms and AMC portals sometimes default to regular plans during new transactions, so confirm the plan type at each step. This is where the benefits of direct mutual funds actually compound in your favor, but only when every rupee you invest going forward lands in the correct plan.

Wrap-up and next step

The benefits of direct mutual funds come down to one structural reality: lower costs compound in your favor every single day your money stays invested. By eliminating distributor commissions, direct plans give you a higher NAV, a lower expense ratio, and more of your own returns working for you over the long term. For salaried investors building wealth through SIPs over 10, 15, or 20 years, this difference is not cosmetic. It translates into lakhs of rupees that either stay in your portfolio or quietly flow out to an intermediary.

Knowing this is the starting point. Acting on it is what changes your outcome. The right move is pairing direct plans with conflict-free, SEBI-registered advisory support so your investments stay aligned with your actual goals without sacrificing guidance. If you are ready to make that shift, get started with Invsify and put your money to work without the hidden costs.