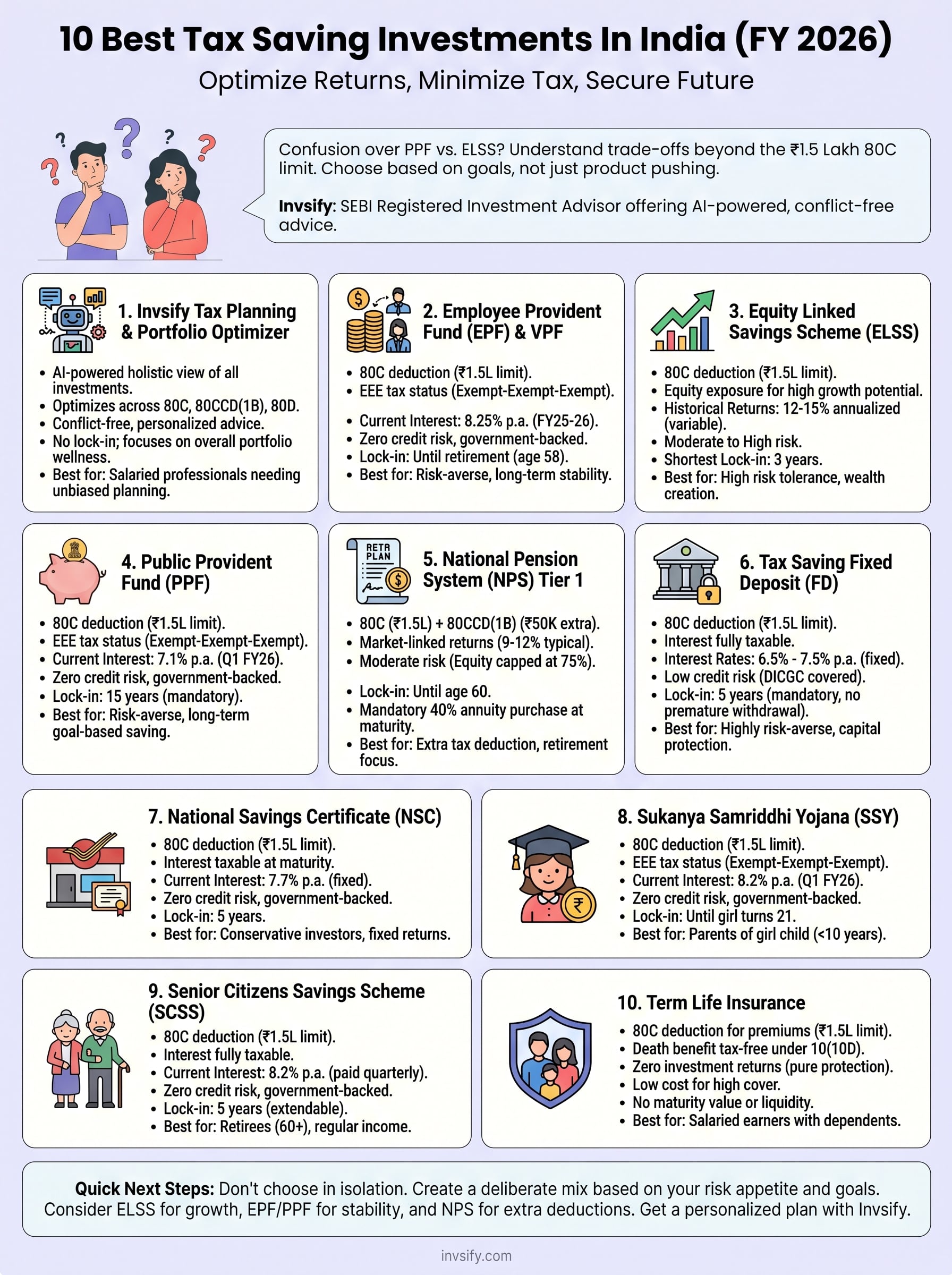

10 Best Tax Saving Investments In India: Save Tax (FY 2026)

Shlok Sobti

10 Best Tax Saving Investments In India: Save Tax (FY 2026)

Every financial year, salaried individuals across India scramble to figure out the best tax saving investments in India before the deadline hits. And every year, the same confusion shows up, PPF or ELSS? NPS or tax-saving FD? Most people end up picking whatever their bank relationship manager pushes, often without understanding the trade-offs between returns, lock-in periods, and actual tax benefits.

Here's the thing: Section 80C alone lets you claim up to ₹1.5 lakh in deductions, and when you layer in sections like 80CCD(1B) and 80D, the savings get even more significant. But not all tax-saving instruments are equal. Some grow your wealth aggressively, others protect your capital, and a few do both, depending on your risk profile and time horizon. Choosing the right mix matters more than just filling the ₹1.5 lakh quota.

At Invsify, we help salaried professionals cut through this noise with AI-powered, conflict-free investment advice as a SEBI Registered Investment Advisor. No hidden commissions, no product-pushing, just data-backed recommendations tailored to your financial goals.

In this guide, we break down the 10 most effective tax-saving investments available in India for FY 2026, comparing their returns, lock-in periods, risk levels, and tax treatment, so you can make a decision that actually works for your money, not someone else's commission structure.

1. Invsify Tax Planning and Portfolio Optimizer

Before diving into individual instruments, it helps to know what you're working with across your entire portfolio. Invsify's tax planning and portfolio optimizer gives you a single, AI-powered view of your investments, so you can make smarter, more deliberate decisions about where to allocate your tax-saving rupees each financial year.

What It Is

Invsify is a SEBI Registered Investment Advisor that combines AI-driven analysis with human support to help salaried professionals plan their taxes and manage their wealth. The platform maps your existing investments, calculates your Wealth Wellness Score, and recommends a personalized tax-saving strategy based on your income, risk profile, and financial goals, not on which product pays the highest commission.

Tax Benefit and Rules

Invsify itself is an advisory platform, not a tax-saving instrument. However, it helps you identify and optimize across all eligible deduction sections: 80C, 80CCD(1B), 80D, and more. The platform shows you exactly how much of your ₹1.5 lakh 80C limit is already utilized and where gaps exist, so you stop over-investing in low-return instruments out of habit.

Getting personalized advice from a SEBI Registered Investment Advisor means your tax plan is built around your actual financial situation, not a generic template.

Returns and Risk

Because Invsify guides you toward the right mix of instruments for your specific goals, your overall portfolio risk and return profile improves over time. Users who avoid high-fee distributors and follow conflict-free advice typically retain more of their investment returns due to lower cost structures and better-suited product selection.

Liquidity and Lock-in

There is no lock-in period for using the platform itself. You can access your portfolio dashboard, AI chatbot, weekly insights, and human support anytime. The lock-in periods that apply are those of the underlying instruments you invest in, which Invsify clearly flags before you commit.

Best for

Invsify works best for salaried professionals who want a clear, unbiased picture of their tax-saving options before choosing specific instruments. It is particularly valuable if you are currently relying on a bank relationship manager or self-managing investments without a structured plan.

2. Employee Provident Fund and Voluntary Provident Fund

EPF and VPF are among the most straightforward tax-saving instruments available to salaried employees in India, and many people already benefit from EPF without actively choosing it.

What It Is

EPF is a mandatory retirement savings scheme where both you and your employer contribute 12% of your basic salary each month. VPF is the voluntary extension of this, where you can contribute more than the mandatory 12%, up to 100% of your basic salary, under the same structure and interest rate.

Tax Benefit and Rules

Your EPF and VPF contributions qualify under Section 80C, within the overall ₹1.5 lakh annual limit. The scheme follows an EEE (Exempt-Exempt-Exempt) tax structure, meaning contributions, interest earned, and withdrawals are all tax-free, provided you complete five continuous years of service.

EPF's EEE status makes it one of the most tax-efficient instruments available to salaried professionals in India.

Returns and Risk

The current EPF interest rate is 8.25% per annum for FY 2025-26, declared by the EPFO. This is a government-backed, fixed return with virtually zero credit risk, making it one of the safer options on this list.

Liquidity and Lock-in

EPF is effectively locked in until retirement (age 58), though partial withdrawals are allowed for specific needs like medical emergencies, home purchase, or education.

Best for

EPF and VPF work best for risk-averse salaried employees who want guaranteed, tax-free returns and are comfortable keeping the money locked in for the long term.

3. Equity Linked Savings Scheme Mutual Funds

ELSS funds are the only mutual fund category that qualifies for a tax deduction under Section 80C, which makes them a popular choice among investors who want market-linked growth alongside a tax break. When evaluating the best tax saving investments in India, ELSS stands out for combining aggressive wealth-building potential with one of the shortest lock-in periods in the 80C basket.

What It Is

ELSS funds are equity mutual funds that invest primarily in stocks across market capitalizations. You can invest either as a lump sum or through a monthly SIP, and each instalment is treated as a separate investment with its own three-year lock-in.

Tax Benefit and Rules

Investments in ELSS qualify for a deduction of up to ₹1.5 lakh under Section 80C. Returns are subject to Long-Term Capital Gains (LTCG) tax at 12.5% on gains above ₹1.25 lakh per year, so the tax treatment is not fully exempt like EPF or PPF.

ELSS is the only 80C instrument that gives you equity market exposure, making it the highest-return option in the deduction basket over the long term.

Returns and Risk

Historically, ELSS funds have delivered 12 to 15% annualized returns over ten-year periods, though returns vary with market conditions. Risk is moderate to high given the equity exposure.

Liquidity and Lock-in

The lock-in period is three years, the shortest among all 80C instruments.

Best for

ELSS works best for salaried investors with a higher risk tolerance who want wealth creation alongside tax savings and can stay invested for at least five to seven years.

4. Public Provident Fund

PPF is a government-backed savings scheme that remains one of the most trusted long-term wealth-building tools for salaried individuals in India. When people evaluate the best tax saving investments in India, PPF consistently ranks high because of its guaranteed returns and complete tax exemption.

What It Is

This scheme runs for 15 years and is administered by the Government of India through post offices and authorized banks. You can open a PPF account with as little as ₹500 per year, and the maximum annual contribution cap is ₹1.5 lakh.

Tax Benefit and Rules

Contributions qualify for a deduction under Section 80C, up to ₹1.5 lakh per year. Like EPF, PPF follows the EEE tax structure, meaning your contributions, interest earned, and maturity amount are all completely tax-free.

PPF's EEE status combined with government backing makes it one of the most tax-efficient instruments available in India.

Returns and Risk

The current PPF interest rate is 7.1% per annum for Q1 FY 2026, compounded annually and revised quarterly by the government. There is zero credit risk since the sovereign guarantee backs the entire scheme.

Liquidity and Lock-in

PPF carries a mandatory 15-year lock-in period. You can make partial withdrawals from year seven onward, and loans against the PPF balance are permitted between years three and six.

Best for

Salaried professionals who are risk-averse and want guaranteed, tax-free returns will get the most value from PPF. It suits those comfortable committing to a long investment horizon without needing the funds for at least a decade.

5. National Pension System Tier 1

NPS Tier 1 stands out among the best tax saving investments in India because it is the only instrument that allows deductions under both Section 80C and Section 80CCD(1B), giving you more room to reduce your taxable income beyond the standard ₹1.5 lakh limit.

What It Is

This is a government-regulated retirement savings scheme supervised by the Pension Fund Regulatory and Development Authority (PFRDA). You invest in a mix of equity, corporate bonds, and government securities, and your account stays portable across employers and locations, making it practical for salaried professionals who change jobs.

Tax Benefit and Rules

Your contributions qualify for a deduction of up to ₹1.5 lakh under Section 80C. On top of that, an additional ₹50,000 deduction is available under Section 80CCD(1B), which sits entirely outside the 80C limit, bringing your total NPS deduction potential to ₹2 lakh per year.

NPS is the only 80C-eligible instrument that also unlocks an extra ₹50,000 deduction through Section 80CCD(1B).

Returns and Risk

NPS delivers market-linked returns that are not guaranteed, typically ranging from 9 to 12% annualized depending on your chosen asset allocation. Equity exposure is capped at 75% under the active choice option, keeping overall risk at a moderate level.

Liquidity and Lock-in

The corpus is locked in until age 60. At maturity, you must use at least 40% to purchase an annuity, while the remaining 60% is available as a tax-free lump sum withdrawal.

Best for

NPS suits salaried professionals in the 30% tax bracket who want to push their total deductions beyond ₹1.5 lakh and are comfortable with a long retirement-focused investment horizon.

6. Tax Saving Fixed Deposit

Tax saving fixed deposits are one of the simplest instruments in the list of best tax saving investments in India, and every scheduled commercial bank in the country offers them. If you prefer predictable returns and are not comfortable with market-linked products, this option is worth a close look.

What It Is

A tax saving FD is a five-year fixed deposit offered by scheduled commercial banks and some post offices. You deposit a lump sum, and the bank pays you a fixed interest rate for the entire term without flexibility to exit early.

Tax Benefit and Rules

Your investment qualifies for a deduction of up to ₹1.5 lakh under Section 80C. However, the interest you earn is fully taxable at your applicable income slab rate, and TDS applies if your annual interest exceeds ₹40,000.

Tax saving FDs do not follow the EEE structure, so your net returns after tax are meaningfully lower than the stated interest rate suggests.

Returns and Risk

Interest rates typically range from 6.5% to 7.5% per annum depending on the bank, with senior citizens usually getting an additional 0.25% to 0.50% over the standard rate. Credit risk is low for deposits in scheduled banks covered under the DICGC insurance limit of ₹5 lakh.

Liquidity and Lock-in

The mandatory lock-in period is five years, and premature withdrawal is not permitted under any circumstances, unlike a regular FD.

Best for

Tax saving FDs work best for highly risk-averse investors who prioritize capital protection over returns and want a straightforward, one-time investment that requires no ongoing management.

7. National Savings Certificate

NSC is a fixed-income savings instrument offered by the Government of India through post offices. When you evaluate the best tax saving investments in India, NSC appeals strongly to conservative investors who want a government-backed option with predictable returns and zero market exposure.

What It Is

The National Savings Certificate is a post office savings scheme that you can purchase at any post office across India. You invest in fixed denominations starting at ₹1,000, with no upper investment limit, though the Section 80C deduction cap still applies at ₹1.5 lakh per year.

Tax Benefit and Rules

Your investment qualifies for a deduction of up to ₹1.5 lakh under Section 80C. The interest accrued each year is treated as reinvested and also qualifies for an additional 80C deduction, except in the final year when the maturity interest becomes taxable as income at your applicable slab rate.

The annual accrued interest on NSC counts as a fresh 80C investment each year, which partially offsets its otherwise taxable nature at maturity.

Returns and Risk

NSC currently offers 7.7% per annum, compounded annually but paid out only at maturity. There is zero credit risk since the sovereign guarantee backs the scheme entirely, making it one of the safest fixed-income options available.

Liquidity and Lock-in

The mandatory lock-in period is five years, and premature encashment is generally not permitted except in cases of the investor's death or a court order.

Best for

NSC works best for conservative investors who want a straightforward, government-guaranteed instrument with a five-year horizon and are comfortable with a taxable maturity payout.

8. Sukanya Samriddhi Yojana

Sukanya Samriddhi Yojana (SSY) is a government-backed small savings scheme designed specifically for the financial future of a girl child. It consistently appears among the best tax saving investments in India for parents who want to build a dedicated corpus for their daughter's education or marriage while earning tax-free, government-guaranteed returns.

What It Is

SSY is a post office and authorized bank scheme where a parent or legal guardian opens an account in the name of a girl child below the age of 10. You can open a maximum of two accounts per family, one for each eligible daughter. The minimum annual deposit is ₹250, and the maximum is ₹1.5 lakh per financial year.

Tax Benefit and Rules

Contributions qualify for a deduction of up to ₹1.5 lakh under Section 80C. The scheme follows the EEE tax structure, meaning your deposits, interest earned, and maturity withdrawals are all completely tax-free.

SSY is one of the very few instruments that combines government backing with full EEE tax exemption, making it highly efficient for long-term goal-based saving.

Returns and Risk

SSY currently offers 8.2% per annum for Q1 FY 2026, compounded annually. The sovereign guarantee eliminates all credit risk, making this one of the highest-yielding government-backed instruments available today.

Liquidity and Lock-in

The account matures when the girl turns 21, though partial withdrawals of up to 50% are permitted after she turns 18 for education expenses.

Best for

SSY works best for parents of daughters below age 10 who want a disciplined, long-term savings plan with full tax exemption and zero investment risk.

9. Senior Citizens Savings Scheme

The Senior Citizens Savings Scheme (SCSS) is one of the most relevant entries among the best tax saving investments in India for retirees and those approaching retirement. It gives older investors a structured, government-backed income stream while simultaneously reducing their taxable income.

What It Is

SCSS is a post office and authorized bank scheme available to Indian residents aged 60 and above. Individuals aged 55 to 60 who have opted for voluntary retirement can also open an account within one month of receiving their retirement benefits. The maximum deposit limit is ₹30 lakh per individual, and you can open multiple accounts subject to the overall cap.

Tax Benefit and Rules

Your SCSS investment qualifies for a deduction of up to ₹1.5 lakh under Section 80C. However, the interest earned is fully taxable at your applicable income slab rate, and TDS applies if your annual interest exceeds ₹50,000.

SCSS prioritizes income generation over tax efficiency, so it works best as part of a broader retirement plan rather than a standalone tax-saving move.

Returns and Risk

SCSS currently offers 8.2% per annum, paid quarterly, making it the highest-yielding government-backed scheme on this list. The sovereign guarantee eliminates all credit risk, giving retirees reliable quarterly income with no exposure to market fluctuations.

Liquidity and Lock-in

The mandatory lock-in period is five years, extendable by three years after maturity. Premature closure is permitted after one year, subject to a penalty deduction on the interest earned.

Best for

SCSS works best for retired individuals aged 60 and above who want the highest government-guaranteed quarterly income available alongside a Section 80C deduction.

10. Term Life Insurance

Term life insurance rounds out this list of the best tax saving investments in India not because it grows your wealth, but because it protects the financial future of everyone who depends on your income. The tax benefit is a secondary advantage, but it is real and worth factoring into your annual planning.

What It Is

A term life insurance policy pays a fixed death benefit to your nominees if you pass away during the policy term. You pay a regular premium, and if you survive the term, there is no maturity payout, which is what keeps premiums significantly lower compared to endowment or money-back policies.

Tax Benefit and Rules

Premiums you pay qualify for a deduction under Section 80C, up to the overall ₹1.5 lakh annual limit. The death benefit received by your nominees is fully tax-free under Section 10(10D), provided the annual premium does not exceed 10% of the sum assured.

Term insurance is the only instrument on this list where the primary purpose is income replacement, not investment returns.

Returns and Risk

Term insurance delivers zero investment returns since it is pure protection. The only "return" is the peace of mind that your family's financial obligations are covered if something happens to you.

Liquidity and Lock-in

There is no maturity value or liquidity with a standard term plan. Premiums are a committed annual expense for the duration of your chosen policy term.

Best for

Term insurance works best for salaried earners with dependents who want maximum life cover at the lowest possible premium cost.

Quick Next Steps

You now have a clear picture of the best tax saving investments in India and what each instrument actually delivers in terms of returns, risk, lock-in, and tax treatment. The next step is figuring out which combination fits your income level, risk appetite, and financial goals before the FY 2026 deadline closes.

Most salaried professionals benefit from a deliberate mix: ELSS for long-term growth, EPF or PPF for stability, NPS to push deductions beyond ₹1.5 lakh, and term insurance for income protection. The mistake most people make is picking instruments in isolation rather than looking at how they work together across your full portfolio.

Invsify makes this process straightforward. As a SEBI Registered Investment Advisor, the platform builds a personalized, conflict-free tax plan around your specific financial situation, with no hidden commissions or product-pushing involved. Start optimizing your tax-saving portfolio today and stop leaving deductions on the table this financial year.