Capital Gains Tax on Mutual Funds in India: 2026 Rules

Shlok Sobti

Capital Gains Tax on Mutual Funds in India: 2026 Rules

Every rupee you earn from mutual fund investments doesn't fully belong to you, at least not until you understand capital gains tax on mutual funds in India. Whether you've held units for a few months or several years, the tax treatment differs significantly, and getting it wrong can cost you thousands in unnecessary payments.

The 2026 budget brought notable changes that every investor must account for. Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG) now follow updated rates and exemption limits that directly affect your actual returns. For equity funds, debt funds, and hybrid options, the holding period requirements and applicable tax slabs vary considerably, and misunderstanding them can lead to poor timing decisions or surprise tax bills.

At Invsify, our AI-powered advisory helps investors navigate these complexities with transparent, conflict-free guidance. This guide breaks down everything you need to know, from current tax rates to exemption thresholds and fund-specific rules, so you can plan your redemptions strategically and retain more of your gains. Here's exactly how mutual fund taxation works in 2026.

Why mutual fund capital gains tax matters

Your investment decisions become incomplete without factoring in taxes. You might see a 20% gain on your mutual fund statement, but after accounting for capital gains tax on mutual funds in India, your actual return could drop to 15% or even lower. The difference between what you see on paper and what lands in your bank account often surprises investors who ignore tax implications during both entry and exit decisions.

Direct impact on your net returns

Tax liability directly erodes the returns you've worked to build. When you redeem equity mutual fund units after five years, you pay 12.5% LTCG tax on gains exceeding ₹1.25 lakh per financial year under current 2026 rules. For someone with ₹5 lakh in gains, this translates to ₹46,875 in taxes, reducing your actual profit substantially. Short-term gains face even higher rates at 20%, which means half of a ₹1 lakh gain vanishes if you exit within one year.

Debt fund taxation hits harder since all gains, regardless of holding period, now face taxation at your income tax slab rate. If you fall in the 30% bracket, a ₹2 lakh gain from debt funds means ₹60,000 goes to taxes, leaving you with just ₹1.4 lakh. This makes the choice between equity and debt funds not just about risk appetite but also about understanding how taxation affects your final corpus.

Ignoring tax calculations during investment planning can reduce your effective returns by 20% to 40% depending on your tax bracket and fund type.

Timing decisions that cost money

Redeeming your units one day too early can cost you thousands in additional taxes. You face higher STCG rates if you exit equity funds before 12 months or debt funds before 36 months under the old regime, though 2026 rules have simplified some classifications. An investor who redeems ₹10 lakh worth of equity units on day 364 pays ₹2 lakh in STCG tax at 20%, while waiting just one more day would drop that to ₹1.09 lakh in LTCG tax, saving nearly ₹91,000 instantly.

Systematic Withdrawal Plans (SWPs) require even more careful planning since each withdrawal triggers a separate taxable event. Without understanding FIFO (First In, First Out) treatment, you might unknowingly withdraw newer units that haven't completed their holding period, pushing you into higher short-term tax brackets unnecessarily.

Tax planning reduces overall liability

Strategic planning allows you to minimize taxes legally while maximizing actual returns. You can time redemptions to stay within the ₹1.25 lakh annual LTCG exemption limit, spreading larger exits across multiple financial years. An investor with ₹5 lakh in gains could redeem ₹2.5 lakh in March 2026 and another ₹2.5 lakh in April 2026, utilizing exemptions across two financial years and saving approximately ₹40,000 in taxes.

Tax-loss harvesting provides another opportunity to offset gains by booking losses strategically. If you have ₹3 lakh in gains from one equity fund but ₹1 lakh in unrealized losses from another, redeeming both reduces your taxable gains to ₹2 lakh, cutting your tax bill by ₹12,500. These opportunities exist throughout the year but require active monitoring and timely action.

Portfolio rebalancing decisions also become tax-efficient when you understand these rules. Instead of redeeming high-performing funds and triggering large tax bills, you can redirect new investments toward underweight categories, maintaining your target asset allocation without unnecessary tax consequences. This approach works particularly well when combined with systematic investment through SIPs, allowing you to adjust allocations gradually while minimizing taxable events.

How capital gains work in mutual funds

Capital gains taxation applies only when you sell or redeem your mutual fund units. Holding units for years without selling creates no tax liability, regardless of how much their value increases. You pay taxes based on the difference between your purchase price (acquisition cost) and the sale price (redemption value), multiplied by the number of units you sell. This mechanism differs fundamentally from dividend income, which faces taxation in the year you receive it, even without selling any units.

When you trigger a capital gain

You create a taxable event each time you redeem mutual fund units, switch from one fund to another, or when the fund house redeems units on your behalf. A SIP redemption, SWP withdrawal, or systematic transfer between schemes all count as separate taxable transactions. Even reinvested dividends don't escape taxation since the fund house pays dividend distribution tax before crediting your account, though this changed after 2020 when dividends became taxable in your hands at slab rates.

Switching between funds within the same AMC triggers capital gains tax on mutual funds in India just like a regular redemption. Many investors mistakenly believe internal transfers avoid taxation, but tax authorities treat switches as a sale of the original fund followed by a purchase of the new one. You report each transaction separately while filing returns.

Any transaction that reduces your units, whether through redemption, switch, or forced buyback, creates a capital gains tax liability based on the profit realized.

Calculating your actual gain

Your capital gain equals the Net Asset Value (NAV) at redemption minus the NAV at purchase, multiplied by units sold. An investor who bought 1,000 units at ₹50 NAV and redeemed them at ₹75 NAV realizes a ₹25,000 gain (₹25 per unit × 1,000 units). This calculation becomes more complex when you've made multiple purchases at different NAVs through SIPs, requiring FIFO treatment to determine which units you sold first.

How holding periods determine your tax rate

Tax authorities classify gains as short-term or long-term based on how long you held the units before redemption. Equity mutual funds require a 12-month holding period for long-term classification, while debt and hybrid funds need 36 months under older rules, though 2026 regulations have modified some categories. Redeeming units one day before completing the required holding period pushes your entire gain into the higher short-term tax bracket, potentially doubling your tax liability on large redemptions.

The holding period clock starts from the date of allotment, not the date you placed your purchase order. SIP investors track multiple holding periods since each monthly installment creates units with different purchase dates. This matters significantly when planning partial redemptions, as selling recently purchased units triggers higher STCG rates while older units qualify for lower LTCG treatment.

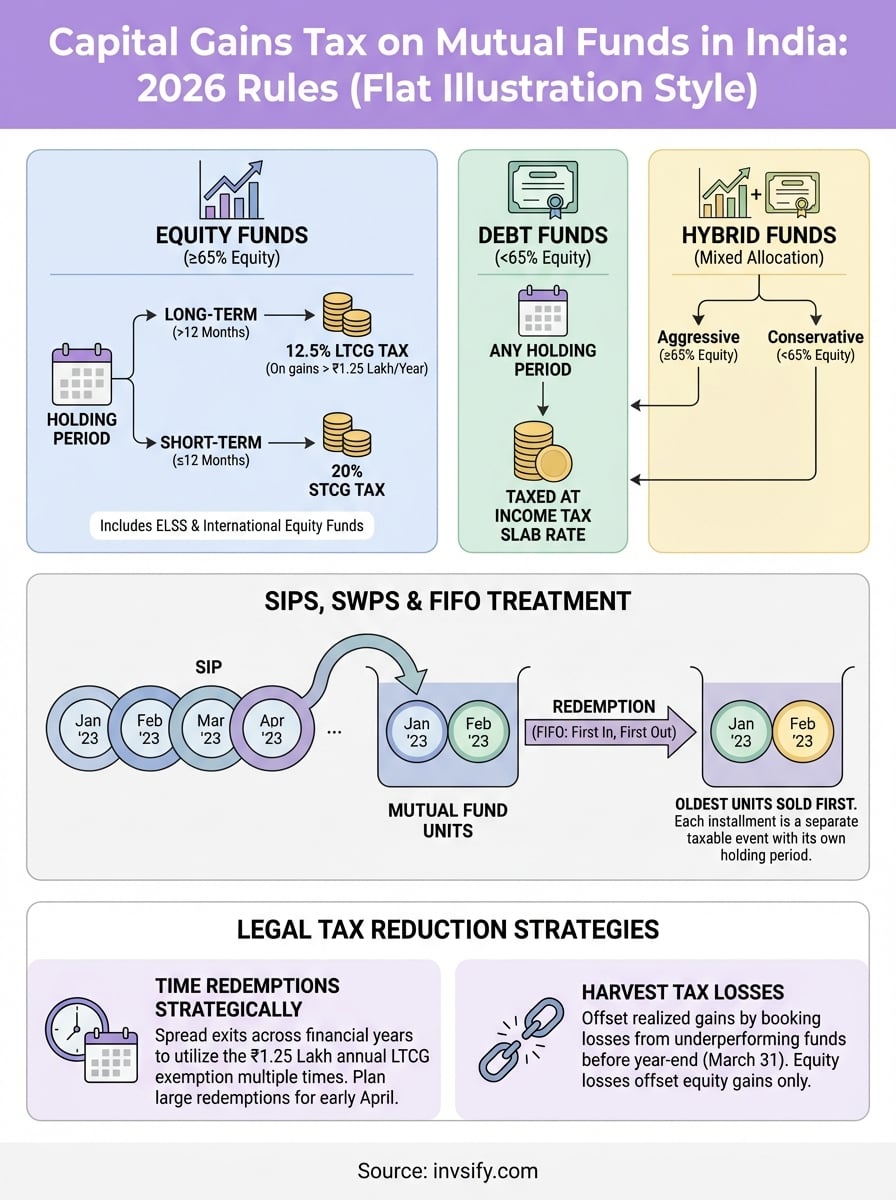

Equity, debt, and hybrid tax rules for 2026

The capital gains tax on mutual funds in India varies dramatically based on fund classification, with equity, debt, and hybrid categories each following distinct tax treatments. Your fund's asset allocation determines which rules apply, and a single percentage point difference in equity exposure can shift your entire tax liability. Understanding these 2026 classifications helps you choose funds strategically and plan redemptions to minimize taxes legally.

Equity mutual funds face simplified taxation

Equity mutual funds, those with 65% or more equity exposure, qualify for preferential tax treatment under current regulations. You pay 12.5% LTCG tax on gains exceeding ₹1.25 lakh per financial year after holding units for at least 12 months. Short-term gains from units held less than 12 months face a 20% tax rate, significantly higher than long-term treatment. An investor redeeming ₹10 lakh worth of equity units after 13 months pays approximately ₹1.09 lakh in LTCG tax, while redeeming at 11 months costs ₹2 lakh in STCG tax on the same profit.

Equity-linked savings schemes (ELSS) follow identical taxation despite their three-year lock-in period. The lock-in prevents redemption but doesn't affect tax treatment, you still pay 12.5% LTCG tax on gains above ₹1.25 lakh after completing 12 months from purchase. International equity funds investing primarily in foreign stocks also qualify for equity taxation if they maintain the 65% equity threshold, giving you access to global markets without sacrificing tax benefits.

Equity fund taxation rewards patience with significantly lower rates after just 12 months, cutting your tax liability nearly in half compared to short-term exits.

Debt mutual funds default to slab rates

Debt funds now face taxation at your applicable income tax slab rate regardless of holding period, following budget changes that eliminated indexation benefits. Someone in the 30% tax bracket pays ₹30,000 on a ₹1 lakh gain from debt funds, whether they held units for one month or five years. This uniform treatment removed the previous advantage of holding debt funds for 36 months to access lower LTCG rates with indexation.

Gold funds, international debt funds, and fund-of-funds investing in debt schemes all fall under this slab-based taxation. Your combined income determines the rate, meaning high earners face substantially higher taxes on debt fund gains compared to equity investors who benefit from fixed 12.5% LTCG rates.

Hybrid funds depend on equity allocation

Hybrid funds follow equity taxation rules if they maintain 65% or more equity exposure, giving you access to the preferential 12.5% LTCG rate. Aggressive hybrid funds typically cross this threshold, qualifying for equity treatment. Conservative hybrid funds with equity exposure below 65% face debt fund taxation at your slab rate, potentially doubling or tripling your tax liability depending on your income bracket. Balanced advantage funds that dynamically shift allocations require careful tracking, as falling below 65% equity even temporarily can reclassify your tax treatment upon redemption.

SIPs, SWPs, and FIFO tax treatment

Systematic Investment Plans (SIPs) and Systematic Withdrawal Plans (SWPs) complicate your capital gains tax on mutual funds in India because each transaction creates separate units with different purchase dates. You can't simply calculate one holding period when you've been investing monthly for years. Tax authorities require you to track every single unit individually, determining which specific units you sold during redemption and whether each qualifies for long-term or short-term treatment based on its unique purchase date.

FIFO determines which units you sell first

The First In, First Out (FIFO) method mandates that you sell your oldest units first when redeeming mutual fund holdings. If you started a SIP in January 2023 and redeem units in February 2026, the tax department assumes you sold units purchased in January 2023 first, then February 2023, and so on sequentially. This automatic ordering happens regardless of which specific units you intended to sell, removing any ability to cherry-pick newer or older units for tax optimization.

FIFO treatment typically works in your favor since older units have completed longer holding periods, qualifying more easily for LTCG rates instead of higher STCG taxation. An investor who ran a monthly SIP for three years and redeems 30% of total units will sell the first year's purchases, all of which easily cross the 12-month equity fund threshold for preferential tax treatment at 12.5%.

SIP investments create multiple tax events

Each monthly SIP installment purchases units at a different NAV, creating separate acquisition dates that you track independently for tax purposes. Your March 2024 SIP at ₹45 NAV and April 2024 SIP at ₹48 NAV represent distinct purchases with different cost bases. When calculating gains, you subtract each unit's original purchase NAV from the redemption NAV, multiplying by units sold from that specific purchase.

FIFO treatment means your earliest SIP investments get redeemed first, usually giving you longer holding periods and lower LTCG tax rates automatically.

Partial redemptions require careful calculation since you must determine exactly how many units from each SIP batch you sold. Someone with 100 units from 10 different SIP dates who redeems 250 units will sell all 100 units from the first SIP, all 100 from the second, and 50 units from the third, calculating separate gains for each batch at their respective purchase NAVs.

SWP withdrawals follow FIFO automatically

Systematic Withdrawal Plans trigger taxable events every month, with each withdrawal redeeming your oldest units first under FIFO rules. A monthly SWP of ₹10,000 might redeem 200 units in January, another 195 units in February at a different NAV, and so on. You calculate capital gains separately for each monthly withdrawal, tracking which specific unit batches each redemption touches and whether those units completed their holding period requirements.

SWPs become tax-efficient when your fund has aged sufficiently that all units qualify for LTCG treatment. An investor who starts a SWP after holding equity fund units for two years pays only 12.5% LTCG tax on gains since every withdrawn unit exceeds the 12-month threshold, maximizing after-tax income from systematic withdrawals.

How to reduce your mutual fund tax legally

You don't need elaborate schemes to cut your tax bill on mutual fund investments. Strategic planning using legitimate methods built into tax laws can save you thousands while keeping you fully compliant. Understanding capital gains tax on mutual funds in India and applying these techniques consistently reduces your liability substantially without any legal risk or complexity.

Time your redemptions around exemption limits

You completely avoid LTCG tax on the first ₹1.25 lakh of equity fund gains each financial year by utilizing the annual exemption intelligently. Instead of redeeming ₹5 lakh worth of units in one go, spread redemptions across multiple financial years to maximize exemption usage. An investor with ₹3.75 lakh in gains who redeems ₹2.5 lakh in March 2026 and ₹2.5 lakh in April 2026 saves approximately ₹15,625 in taxes by claiming exemptions twice rather than once.

Plan large redemptions for early April rather than late March to push gains into the new financial year. This simple timing adjustment gives you an entire year to use that financial year's exemption separately. Couples can double this benefit by splitting investments across both partners' accounts, effectively accessing ₹2.5 lakh in combined annual exemptions instead of just ₹1.25 lakh.

Harvest tax losses before year-end

Tax-loss harvesting lets you offset gains by deliberately booking losses from underperforming funds. If you have ₹2 lakh in realized gains from one fund but hold another fund with ₹80,000 in unrealized losses, redeeming the losing fund reduces your taxable gains to ₹1.2 lakh, saving ₹10,000 in taxes. You can repurchase the same fund immediately since mutual funds don't follow the wash-sale rules that apply to stocks.

Offsetting gains with strategic losses reduces your tax bill while letting you rebalance your portfolio simultaneously, creating a dual benefit.

Review your entire portfolio each December to identify loss-making positions you can book before March 31. Losses from equity funds offset only equity gains, while debt fund losses offset gains taxed at slab rates, so match your loss harvesting to the appropriate fund category for maximum benefit.

Choose tax-efficient fund categories

Equity funds with over 65% equity allocation automatically qualify for preferential 12.5% LTCG rates, making them far more tax-efficient than debt funds taxed at your income slab rate. High-income investors in the 30% tax bracket save 17.5 percentage points by choosing equity-oriented funds over pure debt options when both suit their risk profile.

Index funds and ETFs typically generate fewer capital gains distributions than actively managed funds since they trade less frequently. Lower portfolio turnover means you control when to realize gains through redemption rather than receiving forced distributions that trigger immediate tax liability regardless of your timing preferences.

Key takeaways and next steps

Understanding capital gains tax on mutual funds in India directly impacts your actual investment returns, often reducing paper gains by 20% to 40% depending on your tax bracket and fund type. You face 12.5% LTCG tax on equity fund gains exceeding ₹1.25 lakh annually after 12 months, while debt funds get taxed at your income slab rate regardless of holding period. Strategic timing of redemptions, utilizing annual exemptions across financial years, and harvesting tax losses can legally cut your tax bill by thousands without complex schemes.

Your next step involves reviewing your current portfolio to identify upcoming redemption opportunities and tax-saving strategies. Track your holding periods for each SIP installment to plan exits that qualify for LTCG treatment rather than higher STCG rates. Calculate potential tax liabilities before making large redemptions, and consider spreading exits across multiple years to maximize exemption benefits. Get AI-powered tax optimization insights from Invsify to automatically track your holdings, identify tax-saving opportunities, and execute redemptions at the most tax-efficient moments throughout the year.