Capital Gains Tax on Real Estate in India: Rates & Savings

Shlok Sobti

Capital Gains Tax on Real Estate in India: Rates & Savings

Selling property in India often comes with a hefty tax bill that catches many homeowners off guard. The capital gains tax on real estate in India can take a significant chunk of your profits, sometimes lakhs of rupees, if you're not prepared. With the 2024 budget bringing major changes to tax rates and indexation rules, understanding how these taxes work has become more critical than ever.

Whether you're selling an inherited flat, upgrading to a bigger home, or liquidating an investment property, knowing your exact tax liability, and the legal exemptions available to reduce it, can save you substantial money. The good news? Indian tax law offers several legitimate ways to minimize or even eliminate your capital gains tax burden through smart reinvestment strategies.

This guide breaks down everything you need to know: current STCG and LTCG rates, the new 12.5% versus 20% indexation debate, step-by-step calculation methods, and exemptions under Sections 54, 54EC, and 54F. At Invsify, we help investors navigate complex tax decisions with AI-powered insights and SEBI-registered advisory support, because optimizing your wealth means keeping more of what you earn.

Why capital gains tax matters when you sell property

When you sell property in India, the profit you make isn't entirely yours to keep. The government treats the difference between your selling price and purchase cost as income, taxing it under capital gains. This tax can reduce your net proceeds by 20% to 30% or more, depending on how long you held the property and your total income for that year. For a property sold at ₹1 crore with a ₹40 lakh gain, you could owe anywhere from ₹5 lakh to ₹12 lakh in taxes alone.

The financial impact on your actual profits

Your property's sale price looks impressive on paper, but capital gains tax on real estate in India directly reduces what lands in your bank account. If you bought a flat for ₹50 lakh in 2018 and sell it today for ₹85 lakh, your ₹35 lakh gain faces immediate taxation. Short-term capital gains (property held under 24 months) get added to your regular income and taxed at your slab rate, which can reach 30% for high earners. Long-term gains face either 12.5% or 20% depending on which method you choose after the July 2024 budget changes.

The difference between gross profit and net profit after tax often surprises sellers. A ₹50 lakh capital gain can shrink to ₹40 lakh or less once you account for taxes. Many homeowners discover this reality only when filing their income tax returns, leaving them scrambling for funds they assumed would be available for their next purchase or investment.

Understanding your tax liability before listing your property helps you set realistic expectations and plan your next move accordingly.

Timing decisions that affect your tax bracket

The 24-month holding period threshold separates short-term from long-term capital gains, and this distinction matters enormously for your tax bill. Selling one month too early can push your gains into the short-term category, where they get taxed at 30% plus surcharge and cess instead of the preferential 12.5% or 20% long-term rates. This single timing decision can cost you lakhs in unnecessary taxes.

Your overall income for the year also influences the final tax amount. Selling property in a year when you have high salary income or business profits pushes you into higher tax brackets, especially for short-term gains. Strategic sellers sometimes delay transactions to align with lower-income years or retirement, though this requires careful planning around market conditions and personal needs.

Planning ahead saves you lakhs

Proactive tax planning before you sign the sale deed opens doors to legitimate exemptions and deductions that can reduce or eliminate your capital gains tax entirely. Sections 54, 54EC, and 54F of the Income Tax Act provide specific conditions under which you can reinvest your gains tax-free, but these exemptions come with strict timelines and investment requirements that you must understand beforehand.

Documenting all eligible expenses like brokerage, registration fees, and improvement costs also reduces your taxable gain. Many sellers miss out on these deductions simply because they didn't maintain proper records or didn't know what qualified. The difference between claiming and not claiming these expenses can easily amount to ₹2-5 lakh in tax savings on a typical residential property sale.

Waiting until after the sale to think about taxes leaves you with limited options. By then, you've already triggered the tax event and missed the crucial windows for reinvestment that could have sheltered your gains. Planning six months ahead gives you time to explore all available strategies and execute them properly.

How capital gains tax works for real estate in India

The capital gains tax on real estate in India operates on a straightforward principle: you pay tax on the profit, not the sale price. When you sell property for more than what you paid, the government considers that profit as income from capital gains. The tax applies only to the difference between your purchase cost and selling price, after accounting for eligible expenses and adjustments. Your tax liability depends on how long you held the property and whether you qualify for any exemptions.

The basic tax trigger mechanism

The moment you execute a sale deed and transfer property ownership, you trigger a taxable event. This happens regardless of whether you receive the full payment immediately or in installments. The tax authorities consider the sale date as the date mentioned in the registration document, not when money actually enters your account. If you sell property in March 2026, you must report that capital gain in your income tax return for the financial year 2025-26, even if the buyer pays you in May 2026.

Joint ownership creates proportional tax obligations. When you co-own property with family members and sell it, each owner pays tax on their respective share of the capital gain based on ownership percentage. A husband and wife owning a flat 50-50 will each report half the total gain on their individual tax returns and pay tax accordingly.

Your capital gains tax becomes due in the year you transfer ownership, not when you receive payment.

How the government calculates what you owe

Your tax calculation starts with determining your acquisition cost, which includes the original purchase price plus expenses like registration fees, stamp duty, and any substantial improvements you made. The government then subtracts this adjusted cost from your selling price to arrive at your gross capital gain. From this figure, you can deduct selling expenses like brokerage and legal fees to get your net taxable gain.

The holding period decides whether your gain qualifies as short-term or long-term. Properties held for 24 months or less generate short-term capital gains, taxed at your applicable income tax slab rate. Holdings beyond 24 months qualify as long-term, where you choose between the 12.5% flat rate or 20% with indexation benefit, depending on which method results in lower tax after the July 2024 budget changes.

What counts as a real estate capital gain

A capital gain from real estate happens when you transfer property ownership for a price higher than what you paid to acquire it. The government defines this as any profit from selling land, buildings, residential flats, commercial spaces, or agricultural land (in certain cases). Your gain calculation includes not just the difference between buying and selling prices, but also accounts for expenses you incurred during purchase, sale, and improvement of the property. Understanding what qualifies as a taxable gain helps you accurately report your income and avoid disputes with tax authorities.

Types of property sales that generate gains

Residential properties like apartments, independent houses, and plots create capital gains when you sell them. You trigger capital gains tax on real estate in India whether you sell your primary home where you live or an investment property you rent out. Commercial real estate including offices, shops, warehouses, and industrial buildings also fall under capital gains taxation when transferred for consideration.

Inherited properties generate gains too, but your acquisition cost equals the previous owner's purchase price, not the market value when you inherited it. If your father bought land for ₹10 lakh in 2005 and you inherited it in 2020 when it was worth ₹50 lakh, your cost base remains ₹10 lakh. When you sell it for ₹80 lakh in 2026, your capital gain becomes ₹70 lakh, not ₹30 lakh.

Your capital gain calculation uses the original owner's purchase cost for inherited properties, which can significantly increase your tax liability.

What the government includes in your gain calculation

Your sale consideration includes the actual price you receive plus any benefits or perks the buyer provides. If someone pays you ₹1 crore cash plus takes over your ₹20 lakh outstanding home loan, your total sale consideration becomes ₹1.2 crore. Below-market sales to relatives also attract scrutiny, where tax authorities can substitute fair market value if your declared price seems artificially low.

Transfers that don't create taxable events

Gift transactions to specified relatives like your spouse, children, siblings, or parents don't generate capital gains for you. The recipient takes over your acquisition cost and holding period, so they'll pay tax if they eventually sell the property. Exchanges under court orders, property divisions during divorce settlements, and transfers to wholly-owned companies sometimes qualify for specific exemptions or deferral mechanisms under sections like 47 of the Income Tax Act, though you should verify your eligibility before executing such transfers.

STCG vs LTCG for property and the 24-month rule

The capital gains tax on real estate in India splits into two distinct categories based entirely on how long you held the property before selling it. Short-term capital gains (STCG) apply when you sell within 24 months of purchase, while long-term capital gains (LTCG) kick in for properties held beyond this threshold. This classification determines not just your tax rate but also the exemptions and deductions available to you, making the 24-month mark a critical milestone in property ownership. Your holding period calculation starts from the date you acquired ownership, not when you paid for the property or moved in.

What separates short-term from long-term holdings

Short-term capital gains arise when you transfer property ownership within 24 months of acquiring it. The tax authorities count every month from your purchase date, so selling after 23 months and 29 days still qualifies as short-term. Your STCG gets added to your total income for the year and taxed at your applicable slab rate, which ranges from 5% to 30% depending on your earnings. High-income individuals face effective rates exceeding 35% after adding surcharge and cess.

Long-term holdings begin the moment you cross the 24-month threshold. Properties sold after holding them for 24 months plus one day qualify for preferential LTCG treatment. You pay either 12.5% or 20% with indexation benefit, whichever results in lower tax after the July 2024 budget changes. This dramatic rate difference between 30% and 12.5% explains why strategic sellers wait a few extra months to convert their gains from short-term to long-term status.

Crossing the 24-month threshold can slash your tax rate by more than half, saving you lakhs on the same profit amount.

Why the 24-month threshold matters for your tax bill

The classification directly impacts your net proceeds from the sale by changing both the tax rate and exemption eligibility. Selling a property with ₹30 lakh profit at 30% STCG rate costs you ₹9 lakh plus cess, while the same gain taxed at 12.5% LTCG saves you over ₹5 lakh. Exemptions under Sections 54 and 54F apply only to long-term gains, meaning short-term sellers lose access to reinvestment benefits that could eliminate their tax liability entirely.

How holding period calculation works in practice

Your holding period starts from the date mentioned in your purchase deed registration, not the agreement date or possession date. If you registered your property purchase on March 15, 2024, you must hold until March 16, 2026 to qualify for LTCG treatment. Inherited properties carry forward the original owner's purchase date, so property your parent bought in 2010 and you inherited in 2023 qualifies as long-term the moment you sell it.

Joint ownership doesn't split holding periods between co-owners. The registration date applies uniformly to all owners regardless of their individual share percentages. You cannot claim long-term treatment while your co-owner claims short-term on the same property sale.

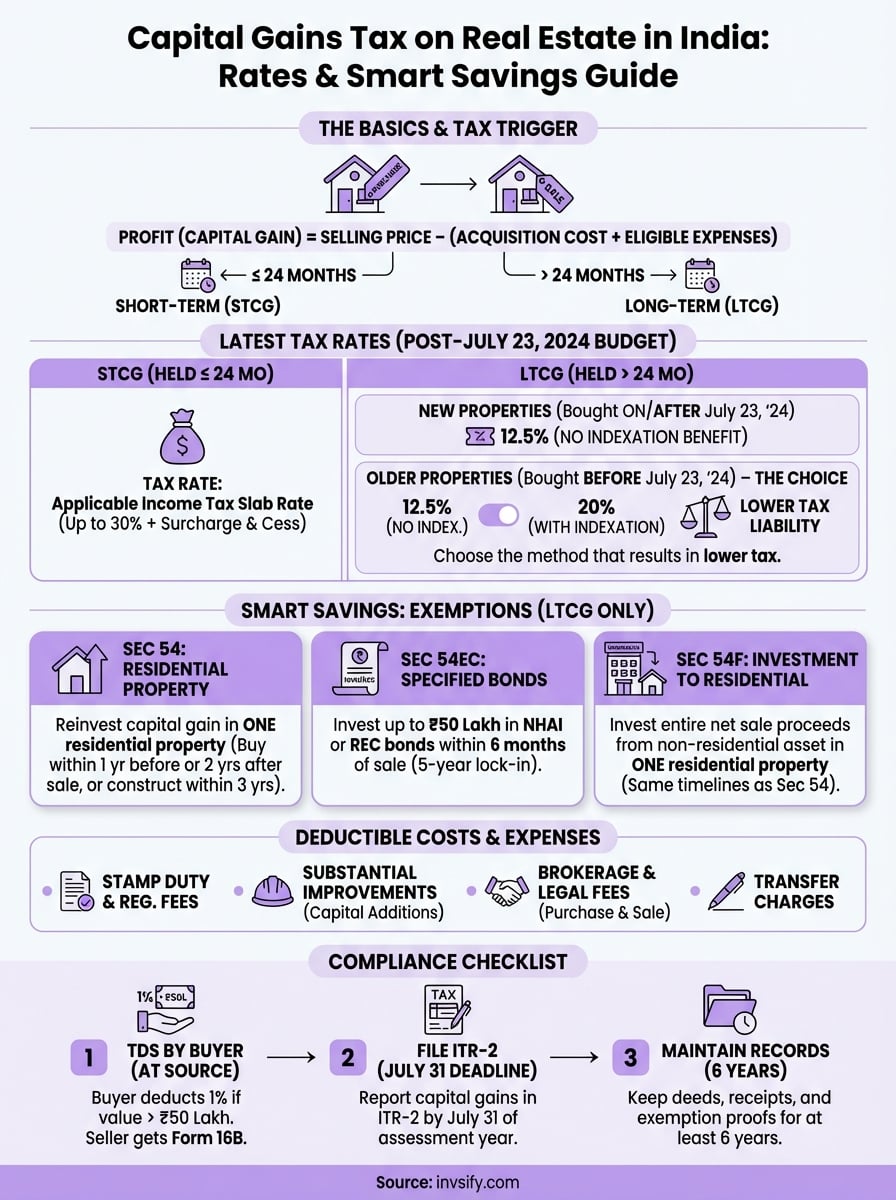

Latest tax rates and what changed after July 23, 2024

The Union Budget 2024 announced on July 23, 2024 brought significant changes to capital gains tax on real estate in India that fundamentally altered how you calculate your tax liability. The government revised both long-term and short-term capital gains rates while introducing a critical choice mechanism for properties purchased before July 23, 2024. These changes affect every property seller differently depending on when they bought their asset and how long they held it, making it essential to understand which rules apply to your specific transaction.

The new LTCG rate structure

Long-term capital gains from property sales now face a flat rate of 12.5% without indexation benefit as the default option. This replaces the previous 20% rate with indexation that adjusted your purchase price for inflation over the holding period. The government eliminated indexation to simplify tax calculations and reduce disputes over Cost Inflation Index values, though this change sparked immediate debate about whether sellers benefit or lose from the new structure.

Properties you purchased on or after July 23, 2024 must use the 12.5% rate without any indexation adjustment. You calculate your gain by simply subtracting your actual purchase cost from the selling price, deduct eligible expenses, and apply the 12.5% tax rate. This straightforward calculation removes the complexity of looking up inflation indices and making adjustments, but it also means you pay tax on nominal gains that include inflation-driven price increases.

The removal of automatic indexation means you now pay tax on inflation-adjusted gains unless you specifically choose the old method for pre-July 2024 properties.

What happened to STCG rates

Short-term capital gains rates remained unchanged at your applicable income tax slab rate, which ranges from 5% to 30% depending on your total income. High earners continue facing the maximum 30% rate plus surcharge and cess, pushing effective rates above 35% in some cases. The government focused its budget changes on long-term holdings rather than short-term transactions, maintaining the existing penalty for selling properties before completing 24 months of ownership.

The grandfathering provision for older properties

Properties you purchased before July 23, 2024 receive special treatment through a grandfathering clause that lets you choose between two calculation methods. You can either accept the new 12.5% rate without indexation or opt for the old 20% rate with full indexation benefit, selecting whichever method produces lower tax. This choice mechanism protects sellers who bought property years ago from sudden tax increases while giving recent buyers the benefit of simpler calculations.

When you can choose 12.5% vs 20% with indexation

Your ability to choose between the 12.5% flat rate and 20% with indexation depends entirely on when you purchased your property. The July 23, 2024 budget changes created a clear dividing line that determines which calculation methods you can access. Properties you bought before this date receive the flexibility to compare both methods and select the lower tax, while purchases after July 23, 2024 must use the new 12.5% rate without indexation benefit. This choice mechanism significantly impacts your final capital gains tax on real estate in India, potentially saving you several lakhs depending on your specific circumstances.

Properties eligible for the calculation choice

You qualify for the dual-option choice only if you purchased your property on or before July 22, 2024. The exact purchase date comes from your registration document, not your agreement or booking date. Properties you inherited also follow the original owner's purchase date, so an inherited property bought by your parents in 2015 gives you access to both calculation methods when you sell today.

Investment properties, residential homes, and commercial real estate all receive the same treatment under this grandfathering provision. The government created this choice mechanism to protect sellers from unexpected tax increases on properties they bought under the old tax regime. Your holding period must still exceed 24 months to qualify for LTCG treatment, but once you meet this threshold, you can evaluate both calculation methods.

Sellers with pre-July 2024 properties get to calculate their tax both ways and pick whichever method costs less.

Deciding which method reduces your tax bill

Properties you held for many years generally benefit from the 20% rate with indexation because inflation adjustments significantly reduce your taxable gain. A flat purchased in 2010 for ₹30 lakh gets indexed up to around ₹60 lakh today, cutting your taxable profit in half. The 20% tax on this reduced gain often costs less than 12.5% on the full nominal profit.

Recent purchases favor the 12.5% flat rate since indexation provides minimal benefit over short holding periods. Property bought in 2022 for ₹80 lakh and sold today for ₹95 lakh sees only marginal indexation adjustment, making the lower 12.5% rate more attractive. You must calculate both scenarios using the actual numbers from your transaction to determine your optimal choice, as general rules don't account for your specific purchase price, sale price, and holding duration.

How to calculate capital gains on property step by step

Calculating capital gains tax on real estate in India requires you to follow a systematic process that determines your exact profit and applies the correct tax rate. You work through four main stages: establishing your selling price, computing your acquisition cost, applying indexation if you choose that method, and calculating the final tax amount. Each step involves specific numbers from your transaction documents, and accuracy at every stage directly affects your tax liability. Missing even one eligible expense or using wrong dates can inflate your tax bill by several lakhs.

Step 1: Determine your total selling price

Your sale consideration includes every rupee and benefit you receive from the transaction. Start with the price mentioned in your registered sale deed, then add any amounts the buyer pays directly to third parties on your behalf. If the buyer takes over your outstanding home loan of ₹15 lakh and pays you ₹85 lakh cash, your total sale price becomes ₹1 crore. You must also add any movable assets included in the sale like furniture or fixtures that the deed specifically values and transfers as part of the property deal.

Your total sale consideration includes every form of payment and benefit, not just the cash you receive in your account.

Step 2: Calculate your indexed acquisition cost

Begin with your original purchase price from your acquisition deed and add all capital improvement expenses you incurred during ownership. Registration fees, stamp duty, and brokerage you paid when buying also increase your cost base. For properties purchased before July 23, 2024, you can multiply this total cost by the Cost Inflation Index ratio for the year you sell divided by the index for the year you purchased. A property bought in 2015 for ₹50 lakh with ₹5 lakh improvements gives you a ₹55 lakh base cost, which indexation adjusts to approximately ₹92 lakh in 2026.

Step 3: Deduct selling expenses from your gain

Subtract your acquisition cost from your selling price to get your gross capital gain. From this figure, deduct all expenses you incurred to complete the sale including brokerage fees, legal charges for documentation, and transfer costs. Your net capital gain emerges after these final deductions and becomes the amount you multiply by your applicable tax rate.

Step 4: Apply the tax rate and calculate payment

For long-term gains on pre-July 2024 properties, calculate your tax both ways: multiply your unindexed gain by 12.5% and your indexed gain by 20%. You pay whichever amount turns out lower. Properties bought after July 23, 2024 use only the 12.5% rate on unindexed gains, while short-term gains get added to your total income and taxed at your slab rate.

What costs and expenses you can deduct legally

Reducing your capital gains tax on real estate in India starts with claiming every eligible expense you incurred during purchase, ownership, and sale of the property. The Income Tax Act allows you to add specific costs to your acquisition price and subtract selling expenses from your final gain, both of which directly lower your taxable profit. You must maintain proper documentation for all claimed expenses including receipts, invoices, and payment proofs, as tax authorities can demand verification during assessment. Missing out on legitimate deductions means you pay more tax than legally required, sometimes by several lakh rupees.

Purchase-related costs you can add to acquisition cost

Your acquisition cost includes much more than the price you paid the seller. You can add registration fees, stamp duty charges, and brokerage paid to agents during the purchase transaction. Legal fees for property verification, title search expenses, and documentation charges also increase your cost base. If you took a home loan, the processing fees and legal charges for the loan qualify as capital expenses, though the interest you paid during ownership does not.

Transfer charges paid to housing societies, membership fees, and utility connection deposits you paid when buying the property count as acquisition costs. Payment proofs through bank statements, receipts from registration offices, and broker invoices serve as documentation you need for claiming these deductions. Adding these expenses to your base cost reduces your capital gain by the same amount, directly lowering your tax liability.

Every rupee you add to your acquisition cost through legitimate expenses reduces your taxable capital gain by the same amount.

Improvement expenses that qualify as capital additions

Substantial improvements you made during ownership increase your cost base if they added lasting value to the property rather than covering routine maintenance. Construction of an additional room, installing an elevator in your building, or adding a swimming pool qualify as capital improvements. Renovation expenses that enhanced the property like upgrading electrical wiring, replacing plumbing systems, or adding modular kitchens also count.

Regular maintenance like painting, minor repairs, or replacing broken fixtures does not qualify. The distinction centers on whether your expense created a new asset or simply maintained the existing structure. You need bills and payment records showing contractor names, work descriptions, and amounts paid.

Sale expenses you subtract from final gains

Brokerage fees paid to agents for finding buyers reduce your capital gain directly. Legal charges for preparing sale documents, fees for obtaining clearance certificates, and expenses for property valuation also qualify as deductible selling costs. Any advertising expenses you incurred to market the property can be claimed as well.

Exemptions that can reduce or eliminate LTCG

The Indian tax code provides several powerful mechanisms to reduce or completely eliminate capital gains tax on real estate in India if you reinvest your proceeds according to specific rules. These exemptions apply exclusively to long-term capital gains, giving you legitimate ways to shelter your profits from taxation while channeling funds into new assets. You must meet strict conditions regarding investment timing, asset types, and holding periods to qualify for these benefits. Understanding each exemption's requirements before selling your property helps you plan reinvestment strategies that maximize tax savings while aligning with your financial goals.

Section 54: Buying another residential property

Section 54 exempts your entire long-term capital gain if you purchase or construct one residential property within specified time limits. You must buy the new property either one year before the sale date or two years after, or construct it within three years of selling your original property. The exemption amount equals either your full capital gain or the cost of your new property, whichever is lower. If you invest only ₹60 lakh in a new home but earned ₹80 lakh in gains, you pay tax on the remaining ₹20 lakh.

You can claim this exemption only once per transaction and the new property must be residential, not commercial. Selling the new property within three years of purchase attracts tax on the previously exempted gain, ensuring you genuinely intend to use the property rather than flip it for profit. You cannot claim Section 54 if you own more than one residential property on the purchase date of your new home, excluding the one you just sold.

Reinvesting your capital gains in another residential property within the allowed timeframe can eliminate your entire tax liability.

Section 54EC: Specified bonds investment

Section 54EC lets you invest your capital gains in specified bonds issued by NHAI or REC within six months of the sale. You can invest up to ₹50 lakh in these bonds and claim exemption for the invested amount. The bonds carry a five-year lock-in period, meaning you cannot redeem or transfer them before this period ends without losing the tax exemption.

These bonds offer fixed interest rates and serve as debt instruments rather than equity investments, making them suitable for conservative investors seeking guaranteed returns. You cannot pledge these bonds as collateral during the lock-in period, restricting your ability to leverage this investment.

Section 54F: For investment property sellers

Section 54F extends similar benefits to sellers of non-residential assets like commercial property or land who want to buy a residential home. You must invest your entire net sale proceeds, not just the capital gain, in a residential property within the same timeframes as Section 54. If you invest only part of the proceeds, your exemption gets proportionally reduced. This exemption requires you to own only one residential property besides the one you purchase with these proceeds.

TDS, return filing, and compliance checklist

Selling property triggers immediate compliance obligations beyond just calculating your capital gains tax on real estate in India. You must handle Tax Deducted at Source (TDS), file the correct income tax return form, and maintain specific documents for years after the transaction. Missing these requirements attracts penalties, interest charges, and potential notices from tax authorities. Your compliance journey begins when you sign the sale deed and extends through at least six years after filing your return, making systematic record-keeping essential from day one.

When the buyer must deduct TDS

Buyers purchasing property from you must deduct TDS at 1% of the sale consideration before making payment if the property value exceeds ₹50 lakh. This deduction happens at the time of payment, and the buyer deposits this amount with the government within 30 days of the end of the month in which they deducted it. You receive a Form 16B from the buyer showing the TDS amount, which you use to claim credit when filing your income tax return.

You can apply for a lower TDS or nil TDS certificate from your jurisdictional tax officer if your actual tax liability is zero or minimal due to exemptions under Sections 54, 54EC, or 54F. This application requires you to submit proof of planned reinvestment and estimated tax calculations before the sale transaction.

Obtaining a nil TDS certificate before selling prevents your funds from getting blocked with the government while you wait for refunds.

Filing your capital gains in ITR-2

You must file ITR-2 form to report capital gains from property sales, even if you have no tax liability due to exemptions. Your return filing deadline falls on July 31 of the assessment year following the financial year of sale. Properties sold between April 2025 and March 2026 require ITR-2 filing by July 31, 2026.

Schedule CG within ITR-2 captures your detailed capital gains calculation including acquisition cost, sale price, indexation benefit, and claimed exemptions. You must also report the TDS deducted by the buyer in the taxes paid section to claim credit for amounts already deposited on your behalf.

Documents you need to maintain

Your compliance file must contain the original sale deed, purchase deed, and payment receipts for both transactions. Registration documents, stamp duty receipts, and brokerage invoices establish your acquisition cost and selling expenses. If you claimed exemptions, maintain proof of reinvestment like the new property purchase agreement, construction bills, or bond purchase certificates from NHAI or REC.

Tax authorities can reopen assessments for up to six years if they suspect income concealment, making long-term document retention mandatory. You should keep bank statements showing fund transfers, Form 16B from the buyer, and ITR acknowledgment receipts in a secure location.

Key takeaways before you sell

Understanding capital gains tax on real estate in India before you list your property gives you the power to plan reinvestment strategies and maximize your net proceeds. The 24-month holding period, choice between 12.5% and 20% rates for older properties, and exemptions under Sections 54, 54EC, and 54F can collectively save you several lakhs in taxes. You need to maintain proper documentation from purchase through sale, including receipts for improvements and expenses that reduce your taxable gain.

Start planning your reinvestment options at least six months before selling. Calculate your expected tax liability using both methods if you bought before July 2024, explore exemption eligibility, and consider applying for a nil TDS certificate if exemptions eliminate your tax burden. Your compliance extends beyond payment to proper ITR-2 filing and maintaining records for six years.

Smart wealth management means keeping more of what you earn. Get AI-powered tax optimization insights at Invsify to navigate complex property sales with SEBI-registered advisory support.