Components Of Financial Literacy: Beginner’s Guide In India

Shlok Sobti

Components Of Financial Literacy: Beginner’s Guide In India

Most Indians learn about money the hard way, through mistakes, missed opportunities, or advice from well-meaning relatives who may not have the full picture. Yet understanding the components of financial literacy can mean the difference between building lasting wealth and constantly playing catch-up with your finances.

Financial literacy isn't a single skill. It's a combination of essential building blocks, budgeting, saving, investing, debt management, and more, that work together to give you control over your money. When you understand each component, you stop making decisions based on guesswork and start making them based on clarity.

This guide breaks down every core pillar of financial literacy specifically for Indian readers. Whether you're a salaried professional just starting out or someone looking to strengthen your financial foundation, you'll walk away with a structured understanding of what it takes to manage money effectively. At Invsify, we believe smart financial decisions start with knowledge, and that's exactly what we're delivering here. Let's get into the specifics.

Why financial literacy matters in India

Financial literacy isn't an academic exercise. It directly affects every rupee you earn and every decision you make about money. In India, where family obligations run deep and inflation chips away at purchasing power year after year, the gap between those who understand the components of financial literacy and those who don't becomes obvious within a few years of starting work.

Your daily financial decisions add up fast

You make dozens of money choices every month. Some feel small, like signing up for a ₹999 subscription or splitting groceries on a credit card. Others carry weight, like choosing an EMI tenure for your two-wheeler or deciding how much rent you can afford. Family responsibilities add layers. Your parents may need medical support. Your sibling might ask for help with education costs. Each decision alone seems manageable, but compounded over months and years, they determine whether you build wealth or stay stuck in a cycle of paycheck-to-paycheck living.

Health emergencies hit hard in India. A single hospital stay without adequate insurance can wipe out years of savings. Credit card debt at 36-42% annual interest can snowball faster than most people realize. When you lack clarity on budgeting, saving, and debt management, these everyday choices quietly drain your financial security.

Saving alone won't beat inflation

Most Indians grow up hearing "save money" as the golden rule. You open a savings account or a recurring deposit and feel responsible. The problem? Inflation in India typically runs between 4% and 7% annually, while traditional savings instruments rarely keep pace. Your money sits in an account earning 3% interest, but your cost of living climbs 6% every year. Over a decade, you're losing purchasing power even while the number in your account grows.

Without investing, your savings slowly lose value against the rising cost of rent, groceries, education, and healthcare.

Investing introduces risk, but it also introduces the possibility of real wealth creation. Understanding how to balance safety with growth becomes critical when your goal is not just to preserve money but to actually build it.

The real cost of financial mistakes

Bad financial decisions carry steep price tags. You might buy an insurance policy from a relative who works as a distributor, only to discover it's an endowment plan with poor returns and high fees instead of the term insurance you actually needed. Or you take a personal loan without comparing rates, paying 16% when another lender offers 12%. You ignore your CIBIL score, then get rejected for a home loan at a crucial moment.

Underinsurance is another common trap. Many Indians carry ₹5 lakh health coverage when their actual medical costs in a serious illness could exceed ₹15 lakh. Avoidable interest, hidden charges, and mis-sold products bleed money that could have gone toward goals like a house, your child's education, or retirement.

Trusting the right sources for money advice

India's financial landscape is noisy. Social media influencers share stock tips without context. Unregistered advisors promise guaranteed returns that violate basic math. Your WhatsApp groups circulate half-truths about tax-saving schemes. When your financial decisions affect your health, stability, and family security, the source of your information matters.

Regulated advice from SEBI Registered Investment Advisors operates under transparency and fiduciary duty. Educational resources from credible institutions help you learn principles. Social media tips often lack accountability and context. Knowing the difference protects you from costly mistakes and builds trust in the decisions you make.

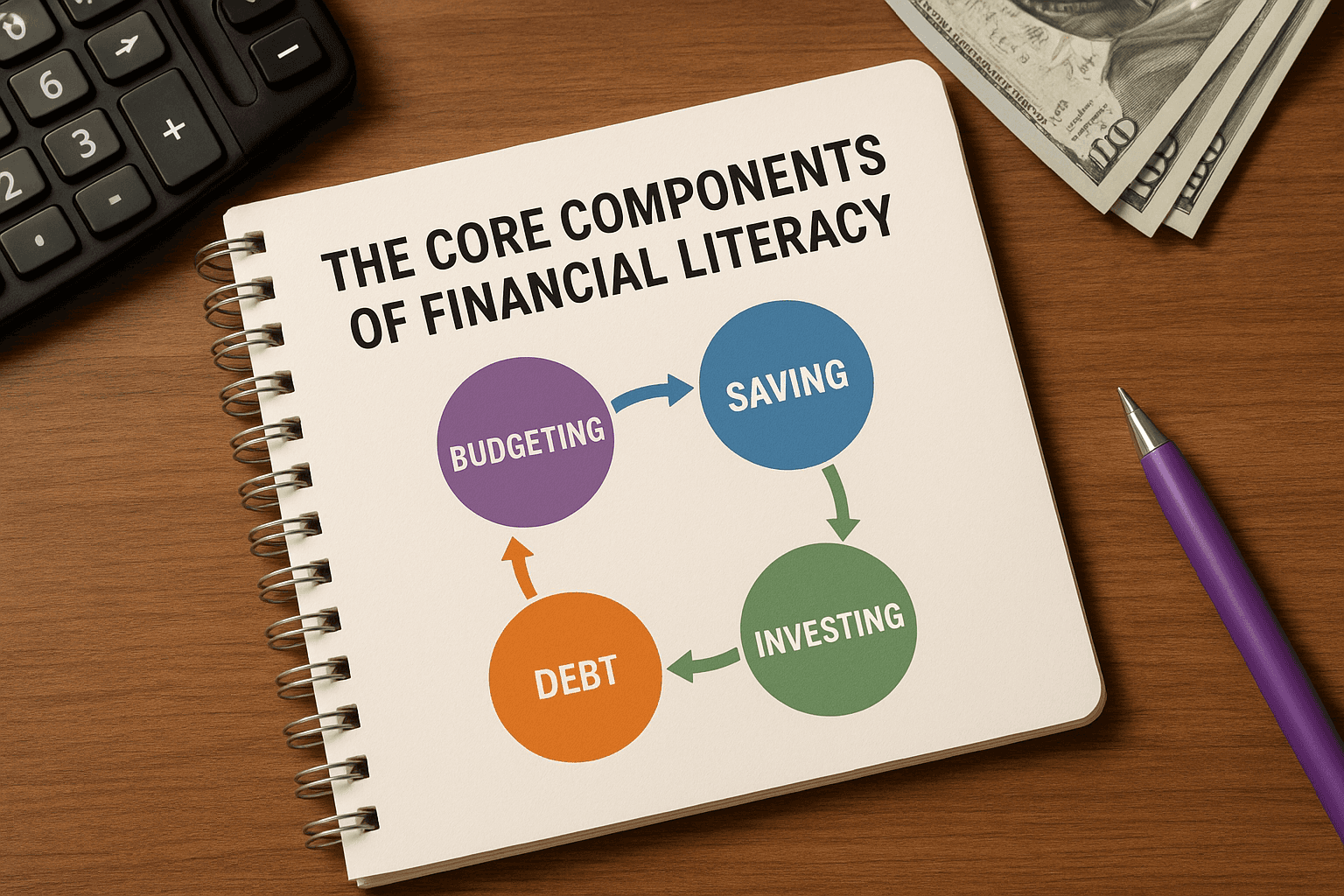

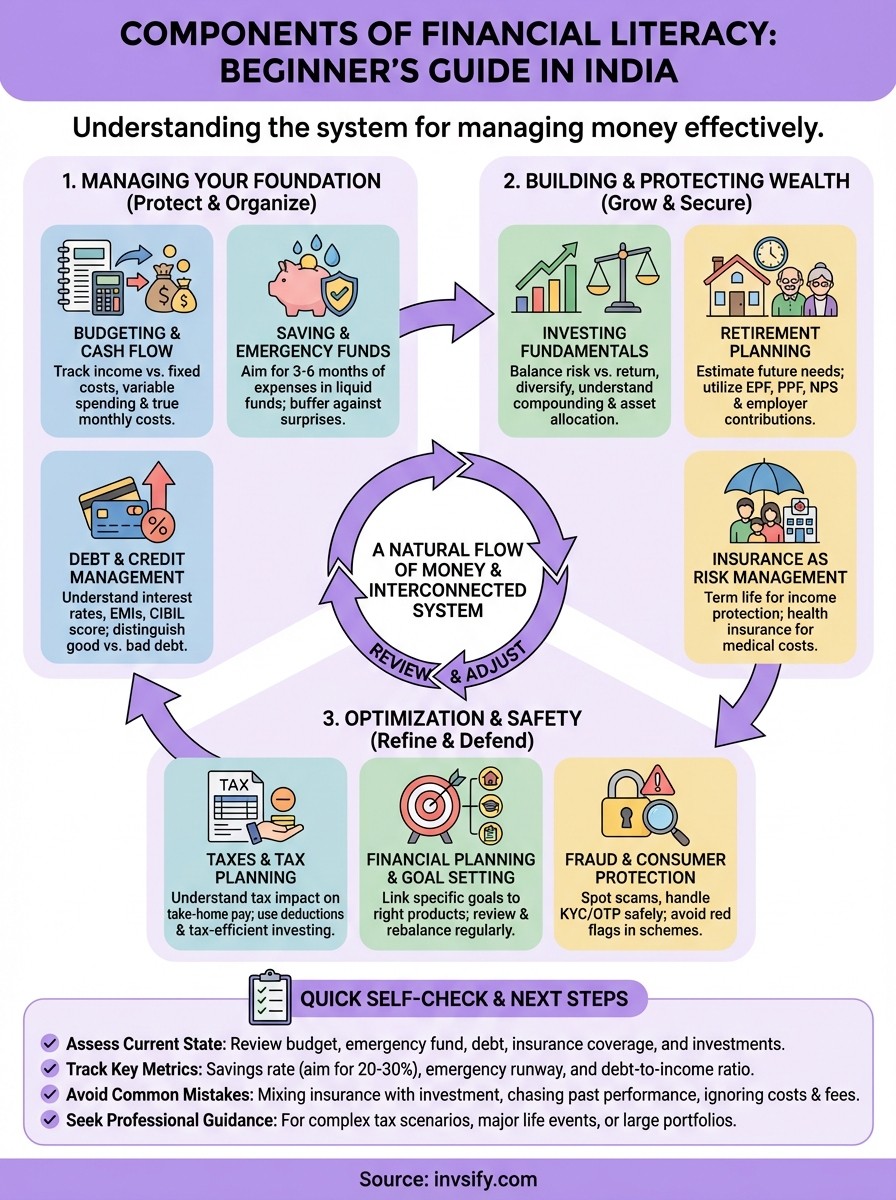

The core components of financial literacy

Understanding the components of financial literacy gives you a clear roadmap for managing money effectively. Each component builds on the others, creating a system that protects what you earn, grows what you save, and helps you reach your goals without unnecessary risk or cost. You don't need to master everything at once, but knowing what each piece does and how it fits into your financial life makes every decision clearer and more confident.

Managing your foundation

[Budgeting and cash flow](https://invsify.com/blog/personal-finance-basics) form the starting point. You track income against fixed costs like rent and EMIs, variable spending like groceries and entertainment, and the true monthly cost of annual expenses like insurance premiums. Saving and emergency funds give you a buffer against surprises. Most Indians aim for three to six months of expenses parked in a savings account or liquid fund. Debt and credit management means understanding interest rates, how EMI calculations work, what drives your CIBIL score, and distinguishing good debt like a home loan from bad debt like high-interest credit card balances. Banking and payments hygiene covers account structure, UPI safety practices, net banking controls, and avoiding hidden charges that eat into your balance.

Without a solid foundation in budgeting, saving, and debt control, every other financial goal becomes harder to reach.

Building and protecting wealth

Investing fundamentals introduce concepts like risk versus return, compounding, diversification, asset allocation, and time horizon. You learn why a balanced portfolio outperforms keeping everything in a savings account. Retirement planning involves understanding EPF, PPF, NPS, employer contributions, and estimating what you'll need decades from now. Insurance as risk management focuses on term life insurance to protect your family's income and health insurance to cover medical costs, while identifying common gaps like inadequate coverage or mixing insurance with investment.

Optimization and safety

Taxes and tax planning show how taxes reduce your take-home pay and how deductions, exemptions, and tax-efficient investing can help you keep more of what you earn. Financial planning and goal setting link specific goals like buying a home or funding education to the right products, with regular reviews and rebalancing. Fraud and consumer protection teaches you to spot common scams, handle KYC and OTP requests safely, and recognize red flags in schemes promising guaranteed returns above market rates.

How these components work together in real life

The components of financial literacy don't operate in isolation. They form an interconnected system where each piece supports the others, creating a natural flow that moves your money from earning to spending to protecting to growing. When you understand how these parts connect, you stop treating financial decisions as separate tasks and start building a coordinated strategy that works toward your actual goals.

A natural flow of money

Your financial life follows a predictable sequence. You earn income through salary or business. You spend on essentials and lifestyle choices. You protect what you've built with insurance and emergency funds. You save surplus money systematically. You invest those savings to beat inflation and grow wealth. Finally, you review and adjust based on changing goals, income, or market conditions. This flow becomes automatic when you set up the right structure, like direct transfers to savings accounts on salary day or SIPs that invest without you thinking about timing.

Sequencing your financial decisions

Certain steps need to come before others. You build an emergency fund before you start aggressive investing because liquidity matters when surprises hit. You secure term insurance and health coverage before placing risky bets on individual stocks. You clear high-interest credit card debt before focusing on long-term equity investments, since paying 40% interest costs more than most investments can earn. Trade-offs exist everywhere. More money toward an EMI means less for investing. Higher insurance premiums cut into your monthly budget but protect your family's future.

The order in which you tackle financial goals determines whether you build a stable foundation or create fragile structures that collapse under pressure.

Goals and the components that serve them

Your life goals connect directly to specific literacy components. Buying a home requires budgeting for down payments, managing debt for the loan, and investing to build corpus. Funding your child's education involves long-term investing, tax planning through Section 80C, and insurance to protect the plan if something happens to you. Product choices like FDs, mutual funds, PPF, or NPS become tools you select after understanding principles, not before.

Common mistakes and myths to avoid

Even when you understand the components of financial literacy, common mistakes can derail your progress. These errors stem from misconceptions, incomplete information, or advice that sounds reasonable but works against your goals. Recognizing these traps helps you avoid costly detours and build wealth more efficiently.

Mixing products with goals

Many Indians treat insurance as an investment, buying endowment or ULIP policies that promise returns alongside coverage. These products typically deliver poor returns after fees and fail to provide adequate protection. You end up with weak insurance coverage and subpar investment growth when you could have bought term insurance for protection and invested the premium difference in mutual funds for better returns. Opening multiple savings accounts or fixed deposits creates an illusion of saving more, but without structured budgeting and automated transfers, you simply scatter money across accounts while missing investment opportunities that actually grow wealth.

Chasing performance instead of process

You see a mutual fund that returned 40% last year and immediately invest, ignoring that past performance doesn't guarantee future results. Timing the market feels smart but consistently underperforms systematic investing with proper asset allocation. Social media influencers share stock tips without disclosing conflicts or time horizons, leading you to buy high and sell low based on noise rather than strategy.

Chasing last year's winners and following unverified tips on social media replaces disciplined investing with gambling.

Ignoring costs and credit traps

Fees compound against you just like returns compound for you. Expense ratios, exit loads, and hidden charges in insurance or mutual funds eat into your gains. Paying your credit card's minimum due feels manageable, but revolving interest at 40% annually turns a small balance into a debt trap. BNPL schemes disguise spending as free money when they're actually short-term loans that encourage overspending. Underestimating health costs leaves you with insufficient insurance coverage and no emergency fund backup, turning medical emergencies into financial disasters that wipe out years of savings.

Quick self-check and next steps

You now understand the components of financial literacy that form the foundation of solid money management. The next step involves honest assessment. You need to identify which areas already work well and which need immediate attention. This self-check process takes less than 30 minutes but reveals exactly where you stand financially and what to tackle first.

Assess your current financial state

Start by reviewing each core component systematically. Do you track monthly income and expenses with a budget, or do you guess where money goes? Have you built an emergency fund covering three to six months of costs, or would an unexpected medical bill create panic? Check your debt situation. Do you know your CIBIL score and total outstanding balances? Look at insurance. Does your term life cover 10-15 times your annual income, and does your health policy actually cover major hospital expenses? Review your investing. Are you contributing to EPF, PPF, or mutual fund SIPs, or does all your money sit in a savings account? Finally, examine retirement planning and tax efficiency. This checklist shows gaps clearly without requiring expert help.

Track metrics that show progress

Numbers make progress visible. Calculate your savings rate by dividing monthly savings by monthly income. Aim for 20-30% consistently. Measure your emergency runway by dividing available emergency funds by monthly essential expenses. Track your debt-to-income ratio. Your total monthly EMI payments should stay below 40% of monthly income. Check insurance adequacy by comparing coverage amounts against actual needs and costs. Monitor portfolio diversification across equity, debt, and other asset classes based on your risk profile and goals.

These simple metrics tell you whether you're building financial security or just staying busy with money tasks that don't move you forward.

Know when professional guidance makes sense

Professional help becomes valuable in specific situations. Complex tax scenarios involving capital gains, multiple income sources, or business income require expertise. Major life events like marriage, home purchase, or starting a business benefit from structured planning. Large portfolios above ₹50 lakh need sophisticated asset allocation and rebalancing strategies. Confusion about risk tolerance, product fit, or conflicting advice signals the need for a SEBI Registered Investment Advisor who works on your behalf without commission conflicts.

Final thoughts

Understanding the components of financial literacy transforms how you handle money. You move from reacting to every expense and surprise to planning with clarity and confidence. Each component budgeting, saving, investing, debt management, insurance, retirement, and taxes works as part of a larger system that protects what you earn and grows what you save over time.

Progress starts with honest assessment and focused action. You don't need to master everything immediately. Pick one area where you see the biggest gap, whether that's building an emergency fund, clearing high-interest debt, or starting your first SIP. Improvement in one area naturally supports growth in others as your financial system strengthens.

Professional guidance accelerates your path when complexity increases or major life decisions loom. Invsify combines AI-powered insights with SEBI-registered expertise to help you make conflict-free financial decisions backed by transparent advice. Your financial future depends on the actions you take today.