Debt Payoff Calculator India: Plan EMIs And Prepayments

Shlok Sobti

Debt Payoff Calculator India: Plan EMIs And Prepayments

Every loan you carry comes with a hidden cost, not just the interest rate on paper, but the total interest you'll actually pay over months or years of EMIs. Most borrowers in India never run the numbers beyond their monthly installment. They don't realize that even a small prepayment can shave off lakhs in interest and years from their tenure. A debt payoff calculator India borrowers can use changes that completely.

Whether you're juggling a home loan, personal loan, car loan, or credit card debt, knowing your exact payoff timeline gives you control. How much interest are you really paying? What happens if you increase your EMI by ₹2,000? What if you make one lump-sum prepayment this year? These are the questions that separate people who stay stuck in debt from those who crush it systematically.

This guide walks you through how to use a debt payoff calculator effectively, how EMIs and prepayments actually work under the hood, and how to build a realistic payoff plan. At Invsify, our AI-powered financial advisory helps you go beyond calculators, optimizing your entire financial picture, from debt reduction to wealth growth. But first, let's get your debt payoff strategy sorted step by step.

What a debt payoff calculator shows in India

A debt payoff calculator India borrowers use does more than just show your EMI. It maps out the full cost of your debt, including total interest paid, remaining tenure, and how different payment choices change both. When you enter your loan amount, interest rate, and current EMI, the calculator produces your exact payoff timeline down to the month. That single number, your total interest outgo, is often the wake-up call people need to start acting.

The core numbers it calculates

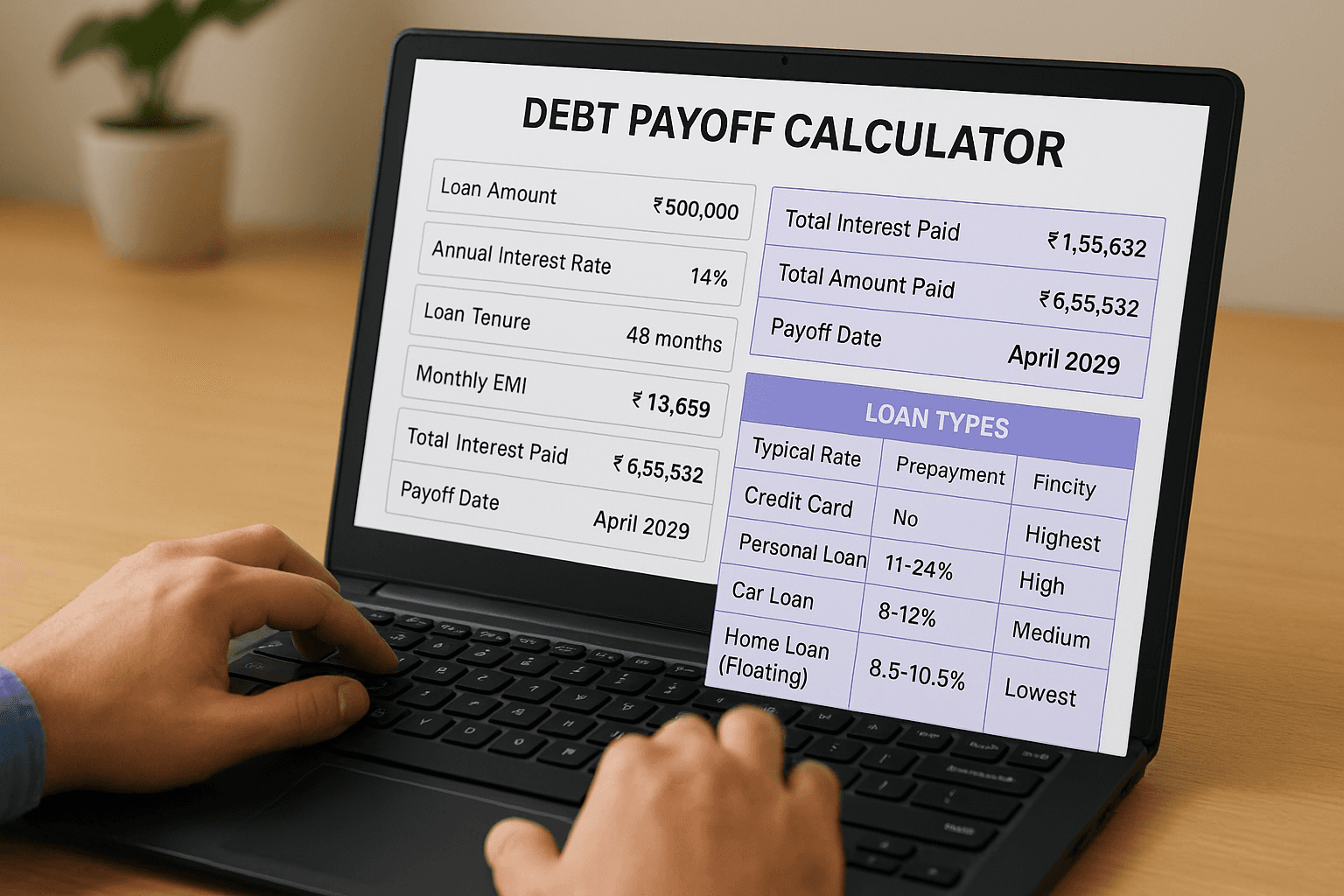

Most borrowers focus only on the monthly EMI because that's the number that hits their bank account. The calculator forces you to look at the bigger picture: total principal borrowed, total interest payable, number of EMIs remaining, and the final payoff date. These four numbers together tell a story your loan sanction letter never will.

Here's what a typical debt payoff calculator displays for a standard Indian personal loan:

Input | Example Value |

|---|---|

Loan Amount | ₹5,00,000 |

Annual Interest Rate | 14% |

Loan Tenure | 48 months |

Monthly EMI | ₹13,659 |

Total Interest Paid | ₹1,55,632 |

Total Amount Paid | ₹6,55,632 |

Payoff Date | April 2029 |

That ₹1,55,632 in interest represents 31% of your original loan amount going straight to the lender. Seeing that figure clearly, rather than just watching the EMI leave your account each month, is what motivates most borrowers to take concrete action faster.

Running this calculation before you make any prepayment decision gives you a solid baseline. Without one, every choice you make is a guess.

How prepayments change the picture

The real power of any debt payoff calculator shows up when you start changing inputs. Increasing your monthly EMI by even ₹1,000 can cut months off your tenure and reduce total interest by tens of thousands of rupees. A lump-sum prepayment works even harder because it directly reduces your outstanding principal, which is the exact amount the lender uses to calculate interest each month.

Take the same ₹5,00,000 loan from the table above. If you make a one-time prepayment of ₹50,000 at the end of year one, your total interest drops from ₹1,55,632 to roughly ₹1,18,000, saving you over ₹37,000 and cutting the tenure by approximately 5 months. No other action delivers that kind of return with so little risk on your end.

What Indian loan types look like in a calculator

Different loans in India carry different rules, and your debt payoff calculator inputs will vary depending on the product. Home loans from banks use a reducing balance method and allow prepayment without penalty on floating rate loans, per RBI regulations. Personal loans and credit cards work very differently. Credit card debt in India can carry annualized interest rates of 36% to 42%, which is why it always deserves to be the first debt you target aggressively.

Here's a quick comparison of how common Indian loan types feed into a calculator:

Loan Type | Typical Rate | Prepayment Penalty | Priority to Pay Off |

|---|---|---|---|

Credit Card | 36-42% | None | Highest |

Personal Loan | 11-24% | 2-5% on outstanding | High |

Car Loan | 8-12% | Varies by lender | Medium |

Home Loan (Floating) | 8.5-10.5% | None (RBI rule) | Lowest |

Knowing your loan type changes how you model scenarios in the calculator. A floating-rate home loan prepayment is almost always penalty-free, so you can run aggressive projections without factoring in extra charges eating your savings. A fixed-rate personal loan, on the other hand, requires you to check your lender's foreclosure terms before you commit to any prepayment plan.

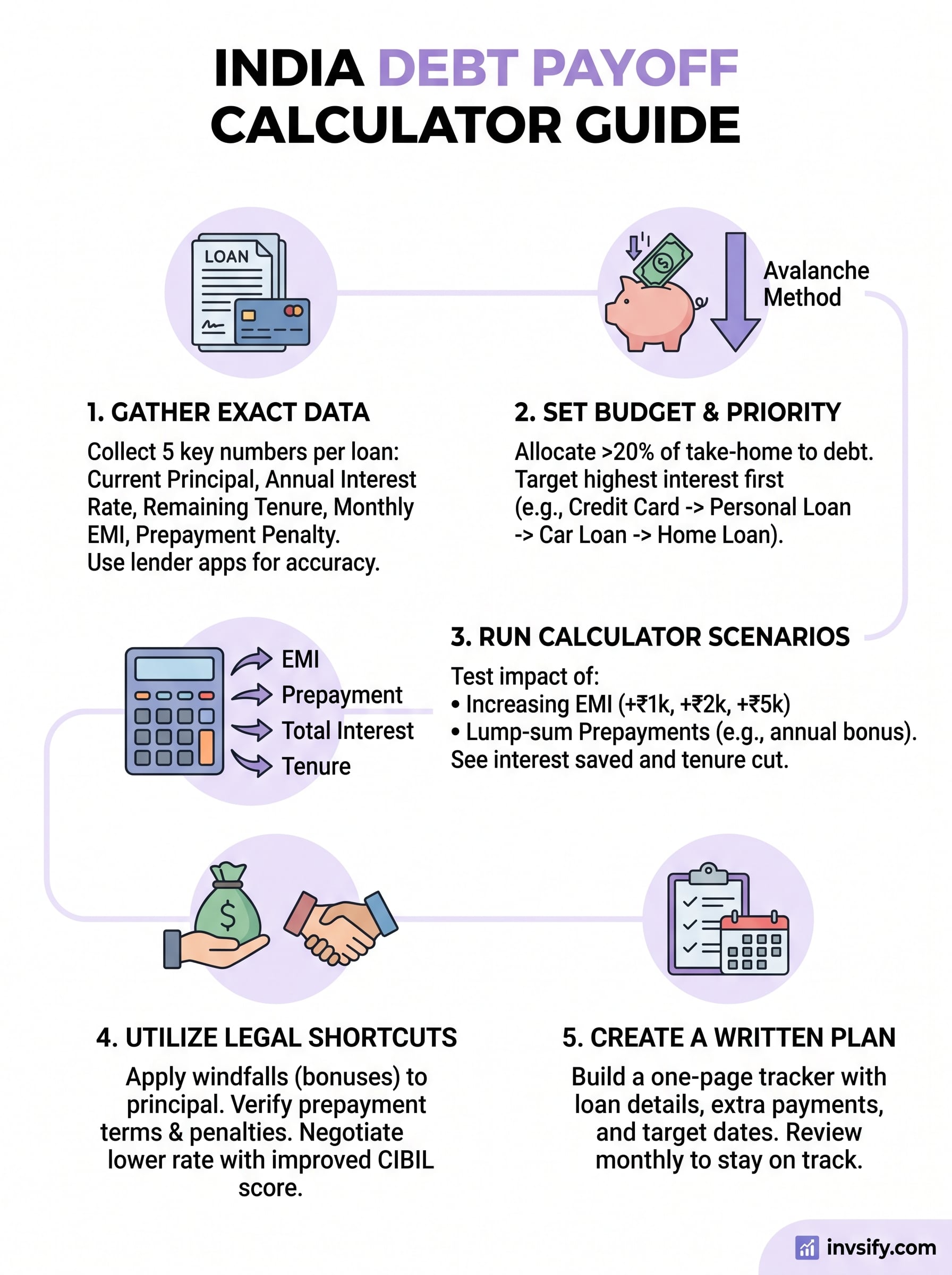

Step 1. Gather your loan and credit card details

Before you open any debt payoff calculator India tool, you need the right numbers in front of you. Feeding in rough or outdated figures will give you projections that look clean but reflect nothing about your actual situation. Spend 15 minutes pulling the exact details for every loan and credit card you carry, and your calculator results will be genuinely useful rather than decorative.

What you need from each loan account

Every loan requires five specific data points to run a meaningful calculation. Missing even one forces you to estimate, which undermines the entire exercise.

Here is what to collect for each loan or credit card before you begin:

Data Point | Where to Find It | Why It Matters |

|---|---|---|

Current outstanding principal | Loan statement or lender app | This is the base amount interest is calculated on |

Annual interest rate (%) | Loan agreement or lender portal | Even a 0.5% difference changes your total interest significantly |

Original or remaining tenure | Loan schedule or amortization table | Tells the calculator how many EMIs are left |

Monthly EMI amount | Bank statement or standing instruction | Confirms your current payment commitment |

Prepayment penalty (if any) | Loan agreement or customer care | Needed before you model lump-sum prepayments |

Collecting all five data points before touching the calculator saves you from running the same scenario three times with corrected numbers.

Where to find your current outstanding balance

Your outstanding principal balance is not the same as your original loan amount. If you took a ₹10,00,000 home loan two years ago and have been paying EMIs since, your current principal might be closer to ₹8,80,000, depending on your rate and tenure. You must use the current figure, not the original one, or every projection the calculator produces will be wrong from the first line.

For most Indian borrowers, the fastest way to get this number is through your lender's mobile app or net banking portal. HDFC, SBI, ICICI, and most major banks display a real-time loan account summary listing outstanding principal, interest accrued to date, and your next EMI due date. For credit cards, your statement balance and the current outstanding shown in the app may differ slightly because of billing cycles, so always use the figure marked "total outstanding" on your most recent statement rather than any in-app estimate.

Step 2. Set your monthly payoff budget and priority

Once you have your loan details ready, the next thing you need is a clear monthly number to work with. This is the total amount you can direct toward debt repayment each month, beyond your existing EMI commitments. Without a fixed budget, you'll either create a cash crunch by overpaying or make no real progress by underpaying.

How much can you actually put toward debt each month

Start with your monthly take-home income and subtract every fixed expense: rent, groceries, utilities, insurance premiums, SIPs, and your current EMIs. Whatever remains is your discretionary cash. From that number, allocate a realistic portion to debt reduction. A common approach is to reserve at least 20% of take-home income for active debt payoff, but your exact figure depends on your expenses and goals.

Use this simple template before you run any scenario in a debt payoff calculator India tool:

Item | Amount (₹) |

|---|---|

Monthly take-home income | ________ |

Fixed expenses (rent, utilities, groceries) | ________ |

Current EMI obligations | ________ |

SIPs and other savings commitments | ________ |

Available for extra debt payments | = Income minus all above |

Fill in your real numbers here. That final "available" figure becomes your monthly payoff budget for every scenario you run in the next step.

Which debt to target first

With your budget set, you need to rank your debts by priority. Two strategies dominate this decision: the avalanche method and the snowball method. The avalanche method targets the highest-interest debt first, which saves the most money over time. The snowball method targets the smallest balance first to build momentum. For most Indian borrowers carrying credit card debt alongside a personal or home loan, the avalanche method is the stronger financial choice because credit card rates of 36% to 42% annualized sit so far above everything else.

Putting even ₹2,000 extra per month toward your highest-interest debt first can save you tens of thousands in interest within a single year.

Apply this priority order as your default starting point:

Credit card outstanding (highest rate, no prepayment penalty)

Personal loan (high rate, verify foreclosure charges first)

Car loan (mid-range rate, terms vary by lender)

Home loan (lowest rate, penalty-free on floating rate per RBI rules)

Direct your entire extra monthly budget to the top-priority debt while maintaining minimum payments on every other account. Once that debt clears, roll that freed-up payment into the next one on the list.

Step 3. Run EMI, tenure, and prepayment scenarios

With your loan data ready and your monthly budget set, you can start running the projections that show exactly what each decision costs or saves you. This is where any debt payoff calculator India tool earns its real value: not from a single static output, but from the multiple projections you generate by changing one variable at a time. Swap one number, record the result, then move to the next. This systematic approach stops you from making a move that feels productive but quietly costs you more over the full loan term.

Test what increasing your EMI does first

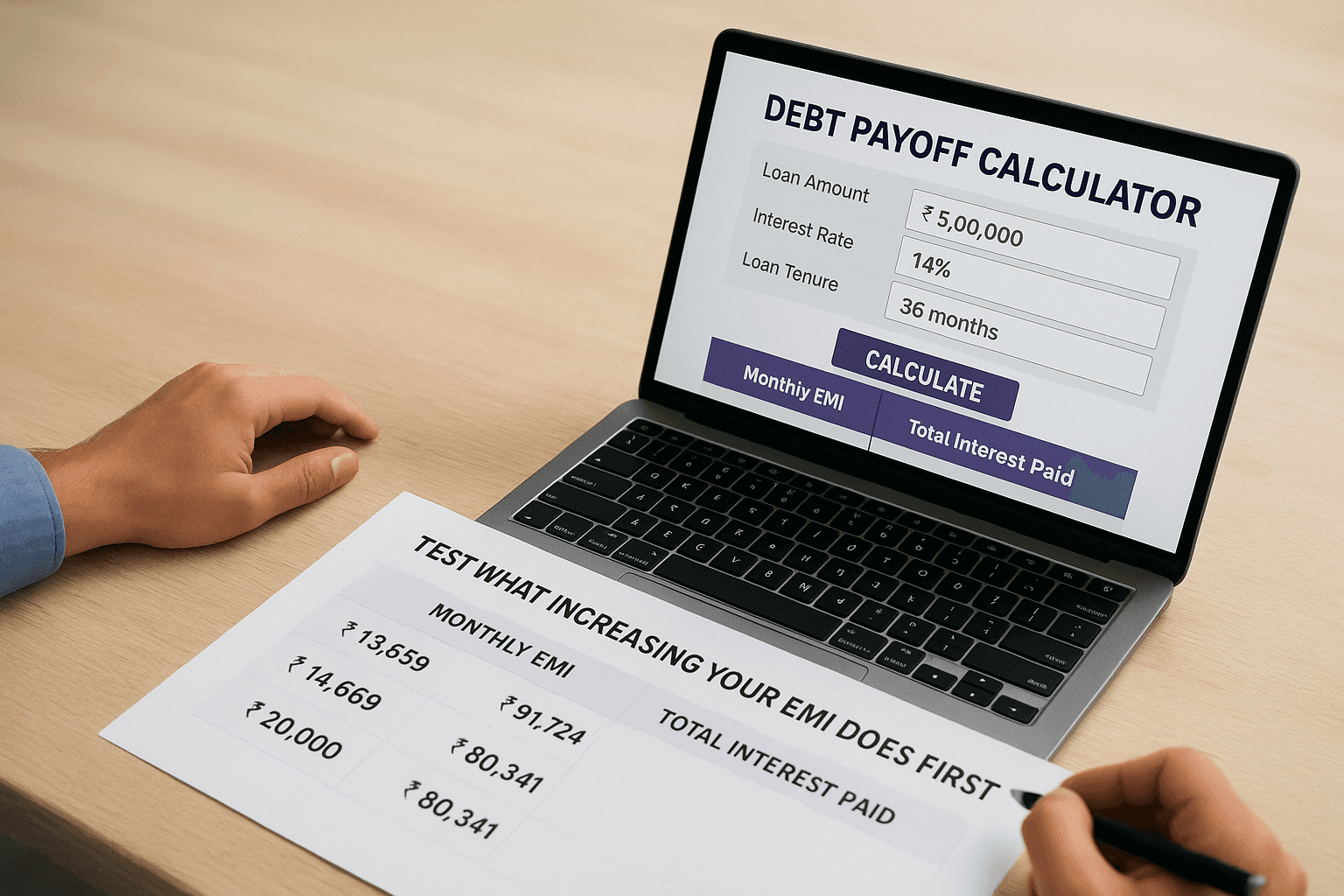

Start with the simplest variable: your monthly EMI amount. Most Indian lenders allow you to pay more than your scheduled EMI each month, and even a modest increase produces a measurable shift in total interest and remaining tenure. Open your calculator, enter your current outstanding principal, annual interest rate, and remaining months, then raise the EMI by ₹1,000, ₹2,000, and ₹5,000 separately and record the output for each.

Here is a practical scenario template based on a ₹5,00,000 personal loan at 14% with 36 months remaining:

Monthly EMI | Total Interest Paid | Tenure Remaining | Interest Saved |

|---|---|---|---|

₹13,659 (standard) | ₹91,724 | 36 months | - |

₹14,659 (+₹1,000) | ₹80,341 | 32 months | ₹11,383 |

₹15,659 (+₹2,000) | ₹71,018 | 29 months | ₹20,706 |

₹18,659 (+₹5,000) | ₹52,416 | 23 months | ₹39,308 |

Adding ₹2,000 per month saves over ₹20,000 in interest and closes your loan 7 months earlier, all without triggering any prepayment penalty in most standard personal loan agreements.

Model a lump-sum prepayment as a separate test

After running the EMI increase scenarios, reset your calculator to the baseline numbers and test a one-time lump-sum payment instead. Enter realistic amounts from your available savings: ₹25,000, ₹50,000, or ₹1,00,000 in the prepayment field. Compare each result against the baseline to see exactly how much total interest that single payment removes from your loan.

Run this test twice for each amount using two different timing assumptions: once with the prepayment made at the end of month 12 and again at the end of month 24. The earlier payment always saves more because your outstanding principal is still high, giving the interest rate less base to work on. Seeing the exact rupee difference between the two timelines gives you a concrete deadline to target your lump-sum savings, rather than leaving it as a vague intention.

Step 4. Cut interest faster without breaking the rules

Once your calculator scenarios are on paper, the next move is to identify every legal shortcut that reduces your total interest without triggering penalties. Many Indian borrowers leave real savings untouched because they don't know which options their loan agreement actually allows. Running a fresh debt payoff calculator India projection after applying each strategy below shows you the exact rupee value of every move before you commit to it.

Send windfall income directly to your principal

Annual bonuses, tax refunds, and performance payouts are the fastest way to cut your outstanding principal without touching your monthly budget. When you receive any lump-sum windfall, direct the full amount, or a significant portion, to your highest-interest loan immediately. The earlier in your loan tenure you apply that payment, the more interest it removes because your lender calculates interest on your remaining principal balance each month.

Apply this priority order when a windfall arrives:

Clear any credit card outstanding in full first (36-42% annualized rate)

Apply the remainder to your personal loan principal if no lock-in period applies

Use anything left for a home loan prepayment, which is penalty-free on floating rate loans per RBI rules

Applying even one annual bonus to your outstanding principal can cut months from your loan tenure and save tens of thousands in interest without affecting your monthly cash flow.

Verify prepayment terms before you commit any lump sum

Not every loan in India allows fee-free prepayments. Fixed-rate personal loans frequently carry foreclosure charges of 2% to 5% of the outstanding amount, and some lenders enforce a minimum lock-in period, typically 6 to 12 months, during which no prepayment is permitted. Paying a 4% fee on ₹3,00,000 outstanding costs ₹12,000 upfront, so you need to confirm that the net interest saved after that charge still makes the move worthwhile.

Request a written foreclosure statement from your lender listing the outstanding principal, applicable charges, and net payoff amount. Then plug those numbers back into your calculator to confirm your savings remain positive after deducting the fee.

Negotiate a lower rate if your credit profile has improved

Your CIBIL score when you took the loan may have been lower than it is today. If you've paid EMIs consistently for 12 months or more and your score has crossed 750, formally request a rate revision from your lender or explore a balance transfer to a competing lender offering a lower rate. A 1% rate reduction on a ₹10,00,000 loan saves roughly ₹60,000 to ₹80,000 over a remaining standard tenure, depending on how many months are left on your schedule.

Step 5. Turn the results into a simple payoff plan

Your calculator scenarios now give you specific numbers: how much interest each move saves, how many months each strategy cuts, and which loan costs you the most to carry. The final step is to convert those scattered projections into one written plan you can follow month by month without re-running everything from scratch each time. A plan on paper removes the friction that kills most debt payoff efforts before they gain traction.

Build a one-page payoff tracker

Take the best scenario from each loan that your debt payoff calculator India run produced and transfer it into a single tracking sheet. One row per loan, one column per month. This gives you a living snapshot of where every debt stands and how far each one has moved since you started.

Use this template as your starting structure:

Loan | Outstanding (₹) | Monthly Extra Payment (₹) | Planned Prepayment Month | Target Payoff Date |

|---|---|---|---|---|

Credit Card | ________ | ________ | ________ | ________ |

Personal Loan | ________ | ________ | ________ | ________ |

Car Loan | ________ | ________ | ________ | ________ |

Home Loan | ________ | ________ | ________ | ________ |

Fill in every row with your actual calculator outputs, not estimates. The "Planned Prepayment Month" column forces you to pick a concrete deadline for any lump-sum payment rather than leaving it as a vague intention that never lands.

Committing your payoff targets to a written tracker doubles the chance you follow through, because each number now carries a specific date rather than remaining an abstract goal.

Stick to the plan with a monthly review

Building the tracker is the easy part. Revisiting it every 30 days is what actually moves the numbers. Set a fixed date each month, ideally the day after your salary credit, to update your outstanding balances, confirm your extra payment went through, and check whether your target payoff date is holding.

During each review, ask yourself three questions. Did the extra payment go out as planned? Has your outstanding balance dropped as the calculator predicted? Is any debt ahead of or behind your projection? If a balance is running higher than expected, re-run that loan's scenario with your updated principal to get a corrected payoff date. Small course corrections every month prevent the kind of drift that leaves you 12 months later wondering why the debt hasn't moved.

You now have a payoff plan

You started with scattered loan balances and no clear picture of what they were costing you. Now you have a step-by-step framework: gather your exact loan details, set a realistic monthly budget, run your scenarios through a debt payoff calculator India borrowers can actually act on, apply every legal shortcut available, and track your progress with a written plan that updates monthly. Each step removes one more reason to delay.

Debt reduction is only part of building real wealth. Once your highest-cost loans are under control, the next move is putting that freed-up cash to work in a portfolio that grows faster than any EMI you're currently servicing. At Invsify, our AI-powered financial advisory helps you do exactly that, from optimizing your debt payoff sequence to building a tax-efficient investment strategy tailored to your income and goals. Start building your wealth plan with Invsify today.