The Key Difference Between Direct and Regular Mutual Funds

Shlok Sobti

The Key Difference Between Direct and Regular Mutual Funds

When you invest in mutual funds in India, you face a critical choice that affects every rupee you earn. The difference between direct and regular mutual funds comes down to who gets paid from your investment returns. Regular plans pay commissions to distributors and agents, while direct plans skip the middleman entirely. This single decision can create a wealth gap of lakhs of rupees over your investment journey.

You deserve to know exactly how these two options work and what they mean for your money. This article breaks down the expense ratio that quietly eats into your returns, shows you how to check which plan type you currently own, and reveals the hidden costs buried inside regular funds. You'll learn why direct plans consistently outperform their regular counterparts, how to switch your existing investments without triggering tax events, and which option makes sense for your financial goals. By the end, you'll have the clarity to make an informed decision that protects your wealth from unnecessary fees.

Why the expense ratio creates a massive wealth gap

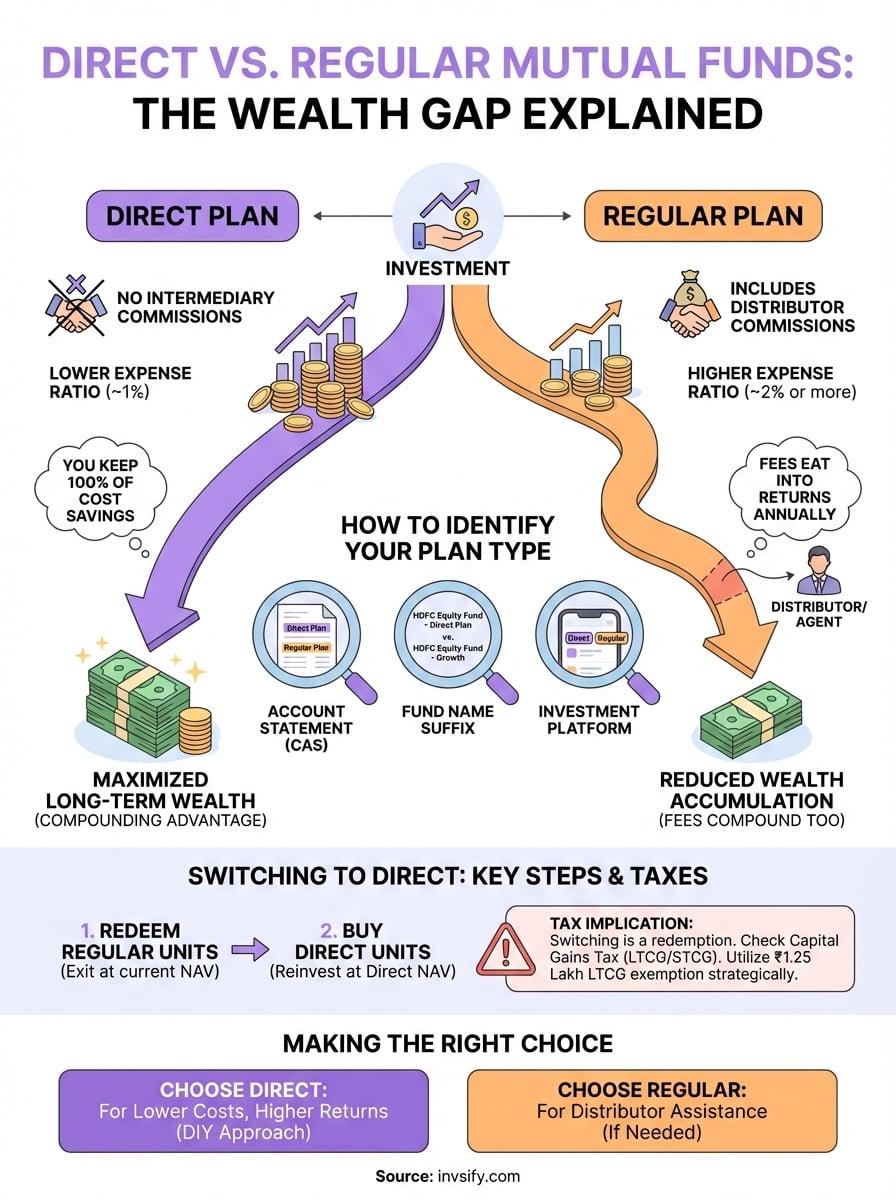

The expense ratio represents the annual fee you pay as a percentage of your total investment, and this seemingly small number has the power to multiply into enormous differences over time. In regular mutual funds, expense ratios typically run 0.5% to 1% higher than direct plans because they include commissions paid to distributors and agents. You might think that 1% sounds negligible, but this percentage gets deducted from your fund's returns every single year, creating a drag effect that reduces your wealth accumulation far more than most investors realize.

The compounding effect on your returns

Your returns compound over time, but so do your expenses. When you pay an extra 1% in fees each year through a regular plan, you lose not just that 1% today but also all the future growth that money would have generated. Consider a ₹10 lakh investment growing at 12% annually: a regular plan with a 2% expense ratio leaves you with 10% net returns, while a direct plan with a 1% expense ratio gives you 11% net returns. That single percentage point difference transforms into lakhs of rupees over a decade or more.

The mathematics work against you in regular plans because the fees get calculated on your entire portfolio value, not just your initial investment. Each year, as your corpus grows larger, you pay progressively higher absolute amounts in fees even though the percentage stays constant. A 1% fee on ₹10 lakh costs you ₹10,000 in year one, but by year 10, that same 1% could cost you ₹23,000 or more as your portfolio value increases.

The longer you stay invested, the wider the wealth gap becomes between direct and regular mutual funds.

Real numbers that show the wealth gap

Take a practical example with a ₹50,000 monthly SIP over 20 years in an equity fund. Assume the fund generates 12% returns before expenses. A direct plan with a 1% expense ratio would grow your investment to approximately ₹4.03 crore, while a regular plan with a 2% expense ratio would reach only ₹3.53 crore. The difference between direct and regular mutual funds in this scenario amounts to ₹50 lakh, money that simply went to pay distributor commissions instead of staying in your pocket.

You can see this impact even more clearly over longer periods. For someone investing ₹10,000 monthly for 30 years, the wealth gap exceeds ₹1 crore when comparing a regular plan at 2% expense ratio versus a direct plan at 1%, assuming the same underlying fund performance. This loss happens silently because the fees get deducted automatically before the NAV gets calculated, making them invisible in your account statements.

The wealth gap grows exponentially because compounding works in both directions. Just as your returns multiply over time, so do the costs of higher expense ratios. Every rupee you save in fees gets the chance to grow and compound for decades, which explains why financial advisors who charge transparent fees often recommend direct plans. Your choice today between regular and direct plans determines whether you build wealth for yourself or for intermediaries who add little value to your investment journey.

How to identify if you own regular or direct funds

You need to verify which plan type you currently own because many investors unknowingly hold regular plans without realizing they pay higher fees. The distinction between direct and regular mutual funds appears in multiple places across your investment records, and checking takes less than five minutes once you know where to look. Your account statements, fund names, and investment platforms all carry clear indicators that reveal whether you own the cost-efficient direct version or the commission-laden regular variant.

Check your account statement for the plan type

Your consolidated account statement (CAS) from NSDL or CDSL shows every mutual fund holding you own, and this document explicitly mentions whether each scheme follows the direct or regular structure. Download your CAS from the CAMS or Karvy website using your email ID and PAN number. Scroll to the holdings section where you see fund names, and look for the words "Direct Plan" or "Regular Plan" listed alongside each scheme. If you invested through a distributor or broker, the statement almost certainly shows regular plans unless you specifically requested direct versions.

Your account statement never hides the plan type, making it the most reliable source to verify your holdings.

Look for the suffix in the fund name

Fund houses append specific identifiers to distinguish plan types in official documentation and online portals. Direct plans carry suffixes like "Direct," "Direct Plan," or "Dir" immediately after the fund name. For example, you might see "HDFC Equity Fund - Direct Plan - Growth" versus "HDFC Equity Fund - Growth" for the regular version. The absence of the "Direct" label automatically means you own a regular plan, regardless of how you purchased the fund. Some Asset Management Companies (AMCs) use abbreviated versions in mobile apps, so watch for "DP" or similar shortened forms that indicate direct plans.

Use your investment platform to verify

Most investment platforms and apps display the plan type prominently in your portfolio section when you tap on individual fund holdings. Log into your broker account, mutual fund app, or the AMC's direct website and navigate to your portfolio or holdings page. Each fund listing typically shows not just the name but also tags or labels indicating "Direct" or "Regular" status. Platforms like the NSE website or BSE StAR also allow you to check your folio details by entering your PAN, revealing the exact plan variant you hold across different fund houses.

The specific costs hidden inside regular mutual funds

Regular mutual funds embed multiple layers of charges that never appear as separate line items on your statements, yet these costs systematically reduce your wealth accumulation. Understanding the difference between direct and regular mutual funds requires you to examine the commission structure that operates invisibly within the expense ratio. Fund houses deduct these charges from the fund's assets before calculating the Net Asset Value (NAV), which means you never see them as explicit debits but you pay them nonetheless through lower returns compared to direct plans.

Distribution commissions that reward intermediaries

When you invest through a distributor, broker, or bank relationship manager, that intermediary receives an upfront commission of 0.5% to 1% of your invested amount directly from the Asset Management Company. This payment happens within 30 to 60 days of your investment, and you bear this cost through a higher expense ratio built into regular plans. The distributor earns this fee regardless of whether they provide ongoing advice, portfolio reviews, or any meaningful service after your initial purchase, creating a misalignment between their incentive to collect commissions and your need for genuine financial guidance.

Trail fees that continue year after year

Beyond the initial commission, distributors collect annual trail fees ranging from 0.5% to 0.75% of your total investment value for as long as you stay invested in regular plans. These recurring payments get deducted every single year from the fund's assets, and unlike performance-based fees, trail commissions flow to the distributor even when the fund underperforms or loses value. You continue paying these fees whether the distributor actively monitors your portfolio, provides market updates, or simply remains uninvolved after the first transaction.

Regular fund distributors earn ongoing commissions from your investments without any obligation to deliver continuous value.

Other embedded operating expenses

Regular plans also incorporate higher administrative and marketing costs compared to direct plans because fund houses pass these expenses to investors who require distributor networks. You pay for advertisement campaigns, sales team salaries, and branch operations through inflated expense ratios. These charges include transaction processing fees, registrar costs, and compliance expenses that get proportionally loaded onto regular plan holders, while direct plan investors share only the basic fund management costs without subsidizing the entire distribution infrastructure.

How direct plans deliver higher returns over time

The difference between direct and regular mutual funds manifests most powerfully in the cumulative returns you receive over extended investment periods, where even small percentage differences in expense ratios compound into substantial wealth creation. Direct plans consistently outperform regular plans because you keep 100% of the cost savings that would otherwise flow to distributors as commissions. This performance advantage stems entirely from the lower expense ratio, not from any difference in fund management strategy, portfolio composition, or market timing, meaning you get the exact same investment expertise while retaining more of your returns.

Lower expense ratios create permanent performance gains

Every rupee you save in annual fees through direct plans gets reinvested automatically and generates additional returns for decades to come. A direct equity fund charging 1% versus a regular plan at 2% delivers a full percentage point of extra returns every single year before compounding even begins to work its magic. These savings multiply exponentially because the money that stays in your account earns returns, which then earn returns on returns. For a ₹25 lakh investment over 15 years at 12% gross returns, the direct plan grows to approximately ₹1.37 crore while the regular plan reaches only ₹1.20 crore, creating a ₹17 lakh difference purely from avoided fees.

Direct plans transform what you would have paid in commissions into permanent additions to your investment corpus.

Tax treatment equalizes your comparison

Both plan types receive identical tax treatment under Indian income tax laws, eliminating any argument that regular plans might offer tax advantages to offset their higher costs. You pay the same long-term capital gains tax, short-term capital gains tax, and dividend distribution tax regardless of whether you own direct or regular variants. This tax parity means the lower expense ratio of direct plans translates directly into higher post-tax returns without any offsetting disadvantages, making the choice straightforward for investors who understand the mathematics.

NAV differences reflect your accumulated savings

Direct and regular plans of the same fund show different Net Asset Values (NAVs) that widen progressively over time because the lower expense ratio causes the direct plan's NAV to grow faster. You can observe this divergence by comparing NAVs on any fund house website, where a five-year-old direct plan might trade at ₹45 while its regular counterpart sits at ₹42, reflecting the accumulated impact of higher fees deducted from regular plan holders.

How to switch your investments to direct plans safely

You can transition from regular to direct mutual funds without selling your existing holdings and triggering tax consequences, though the process requires you to redeem your regular plan units and purchase equivalent direct plan units in separate transactions. This switch counts as a redemption followed by a fresh investment, meaning you realize capital gains or losses based on your holding period at the time of switch. Understanding the difference between direct and regular mutual funds helps you weigh whether the long-term expense ratio savings justify any short-term tax impact from switching, particularly if you hold units with substantial unrealized gains.

Understanding the switch process mechanics

Fund houses treat switches between plan types as two distinct transactions that happen on the same day, where you exit the regular plan at the current NAV and enter the direct plan at its NAV. You cannot simply convert your existing regular plan folios into direct plan folios because regulatory guidelines require fund houses to maintain separate accounting for each plan type. The redemption value from your regular plan becomes immediately available for reinvestment into the direct plan variant of the same scheme, allowing you to maintain continuous market exposure without significant cash drag.

Step-by-step switching procedure

Start by logging into your fund house's website or app and locate the "switch" option within your portfolio holdings. Select the regular plan units you want to convert and choose the corresponding direct plan as the destination scheme. You can execute this switch online without visiting any branch or submitting physical forms, and the entire transaction typically completes within one business day. Some AMCs allow you to switch through their mobile apps, while others require you to use their web portals for plan-type switches.

Switching from regular to direct plans requires you to pay taxes on gains, but the long-term savings usually outweigh the immediate tax cost.

Tax implications you need to know

You pay long-term capital gains tax at 12.5% if you held equity funds for more than one year, while debt funds require three years of holding for long-term status. Any gains below ₹1.25 lakh per financial year on equity funds remain exempt from tax, which means you can strategically switch portions of your portfolio each year to use this exemption fully and minimize your tax liability while transitioning to lower-cost direct plans.

Making the right choice for your financial future

Your decision between plan types shapes how much wealth you actually accumulate versus how much you pay away in fees over your investment lifetime. The difference between direct and regular mutual funds boils down to whether you want to maximize your returns by avoiding unnecessary commissions or accept lower returns in exchange for distributor assistance. You need to evaluate your comfort level with making investment decisions, your willingness to research fund options independently, and whether you genuinely receive valuable ongoing advice that justifies paying higher expense ratios year after year.

When direct plans make the most sense

You should choose direct plans if you can identify quality mutual funds without needing a distributor's recommendation and feel comfortable monitoring your portfolio through online platforms. Direct plans work perfectly for investors who read fund fact sheets, understand basic asset allocation principles, and use online resources to research fund performance and portfolio composition. Most investors today access the same information that distributors use, making the intermediary redundant for anyone willing to spend a few hours learning the fundamentals of mutual fund investing.

Direct plans deliver maximum value when you take responsibility for your own investment decisions and portfolio reviews.

Situations where you might consider regular plans

Regular plans might suit you only if you genuinely lack the time or confidence to manage investments independently and receive comprehensive financial planning services that extend beyond basic product recommendations. Some fee-based advisors use regular plans but provide annual portfolio rebalancing, tax planning, insurance reviews, and estate planning guidance that justify their commission costs. You need to verify that your distributor actually delivers these services rather than simply collecting trail fees after the initial purchase.

Starting your direct plan journey

You can begin investing in direct plans by opening an account directly with any Asset Management Company through their website or mobile app, which takes approximately 10 to 15 minutes using your PAN, Aadhaar, and bank details. Most fund houses offer user-friendly platforms where you set up SIPs, make lump sum investments, and track your portfolio performance without paying any account opening or maintenance charges. Your existing KYC verification carries forward across all fund houses, eliminating repetitive documentation once you complete the process with one AMC.

Final thoughts on fund selection

The difference between direct and regular mutual funds ultimately determines how much wealth you keep versus how much you surrender to intermediaries who add minimal value. Every year you delay switching to direct plans costs you money that compounds into substantial losses over decades. You now understand the expense ratio mechanics, know how to identify your current holdings, and possess the knowledge to make informed decisions that protect your financial future.

Your next step involves taking action rather than simply absorbing information. Direct plans require no special expertise or advanced financial knowledge, just the willingness to spend a few minutes opening an account and selecting quality funds based on performance data available to everyone. Most investors find the process simpler than they imagined once they actually begin.

Technology has eliminated the traditional barriers that once made distributors necessary. Start your direct mutual fund journey with Invsify's AI-powered advisory to combine the cost advantages of direct plans with intelligent portfolio recommendations tailored to your financial goals.