Difference Between Saving And Investing: Risk, Returns, Time

Shlok Sobti

Difference Between Saving And Investing: Risk, Returns, Time

You've worked hard for your money. Now comes the real question: should you let it sit safely in a bank account, or put it to work in the market? Understanding the difference between saving and investing is one of the most important financial decisions you'll make, and getting it wrong can cost you lakhs over your lifetime.

Here's the truth: saving and investing serve different purposes. One protects your money for immediate needs; the other grows it for future goals. The confusion between these two often leads people to either take unnecessary risks with their emergency funds or miss out on wealth-building opportunities by keeping too much cash idle.

At Invsify, we help salaried individuals in India make smarter choices with their money through AI-powered, conflict-free financial advice. Whether you're just starting your financial journey or looking to optimize your existing portfolio, understanding when to save versus when to invest is foundational.

This article breaks down the key differences in risk, returns, and time horizons, so you can confidently decide how to allocate your money based on your actual financial goals.

Why the difference matters for your money

Getting the difference between saving and investing wrong affects your financial security in three critical ways. First, you risk losing purchasing power to inflation by keeping too much money in low-interest accounts. Second, you expose yourself to unnecessary market volatility by investing money you'll need within months. Third, you miss out on compounding returns that could add up to crores over your working life. Each of these mistakes compounds over time, making the early years of your career especially important for getting this balance right.

The opportunity cost of confusion

When you treat savings and investments the same way, you leave significant money on the table. Consider this: if you keep ₹10 lakhs in a savings account earning 3% annually, you'll have ₹13.44 lakhs after 10 years. Put that same amount in a diversified equity fund averaging 12% returns, and you'll have ₹31.06 lakhs. That's a difference of ₹17.62 lakhs for making the right choice with money you won't need immediately.

The cost of keeping long-term money in savings accounts isn't just low returns; it's the decades of compounding growth you can never recover.

Most salaried Indians keep 60-70% of their financial assets in savings accounts and fixed deposits, according to typical allocation patterns. This conservative approach feels safe but creates a hidden wealth trap. Your money loses value to inflation while appearing to grow in absolute terms, creating the illusion of progress without real wealth building.

The inflation trap you can't ignore

Inflation in India has averaged around 5-6% annually over the past two decades. When your savings account offers 3% interest and inflation runs at 6%, you're actually losing 3% of your purchasing power every year. That ₹10 lakhs today will only buy goods worth ₹7.44 lakhs in 10 years at 3% real loss per year.

Your emergency fund and short-term savings should accept this trade-off because liquidity and safety matter more than returns for immediate needs. But keeping money for goals five or ten years away in these accounts guarantees you'll fall short of your target. The difference compounds dramatically: a ₹50 lakh retirement goal requiring ₹2,500 monthly savings at 12% returns would need ₹4,400 monthly at just 4% returns, nearly double the commitment for the same outcome.

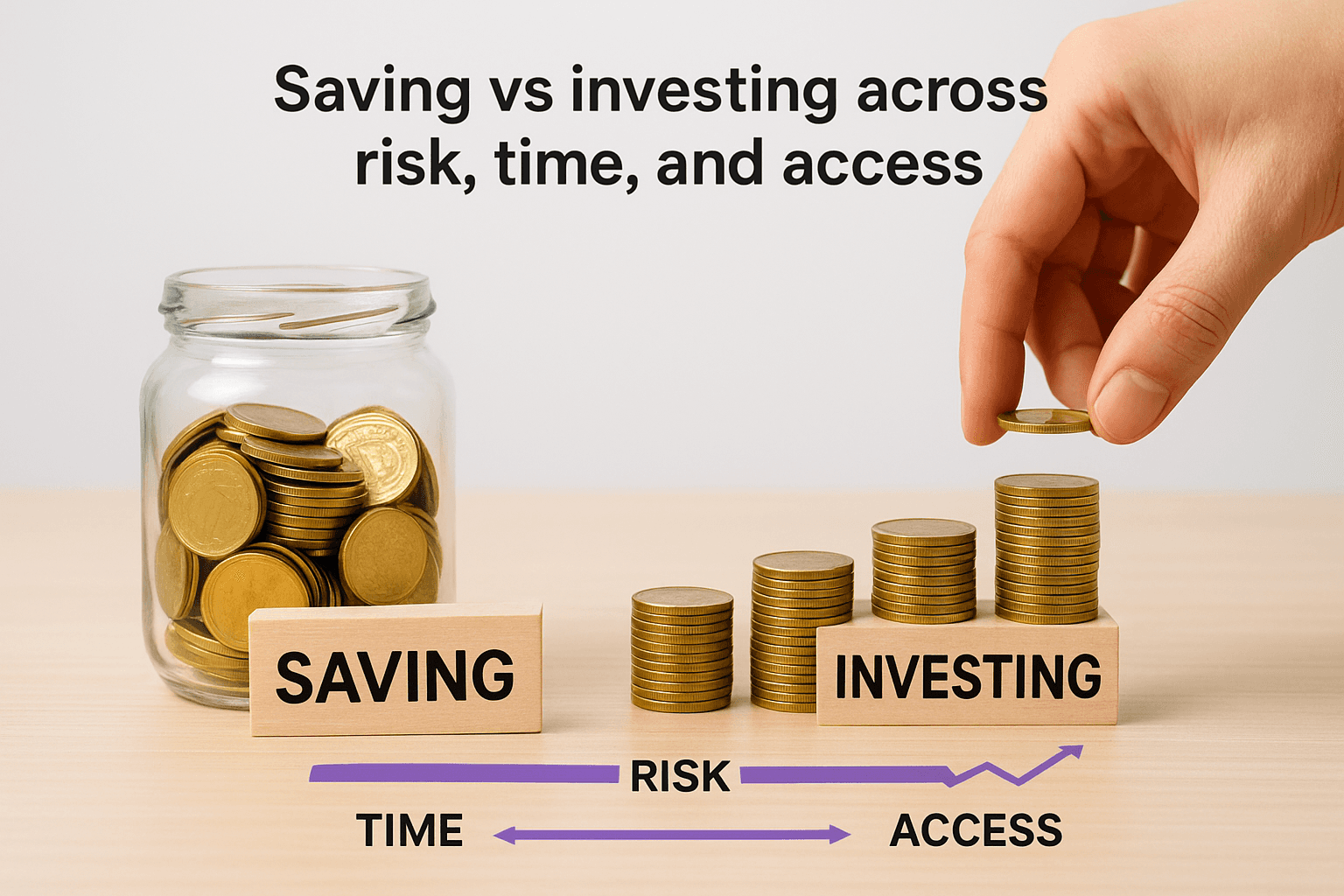

Saving vs investing across risk, time, and access

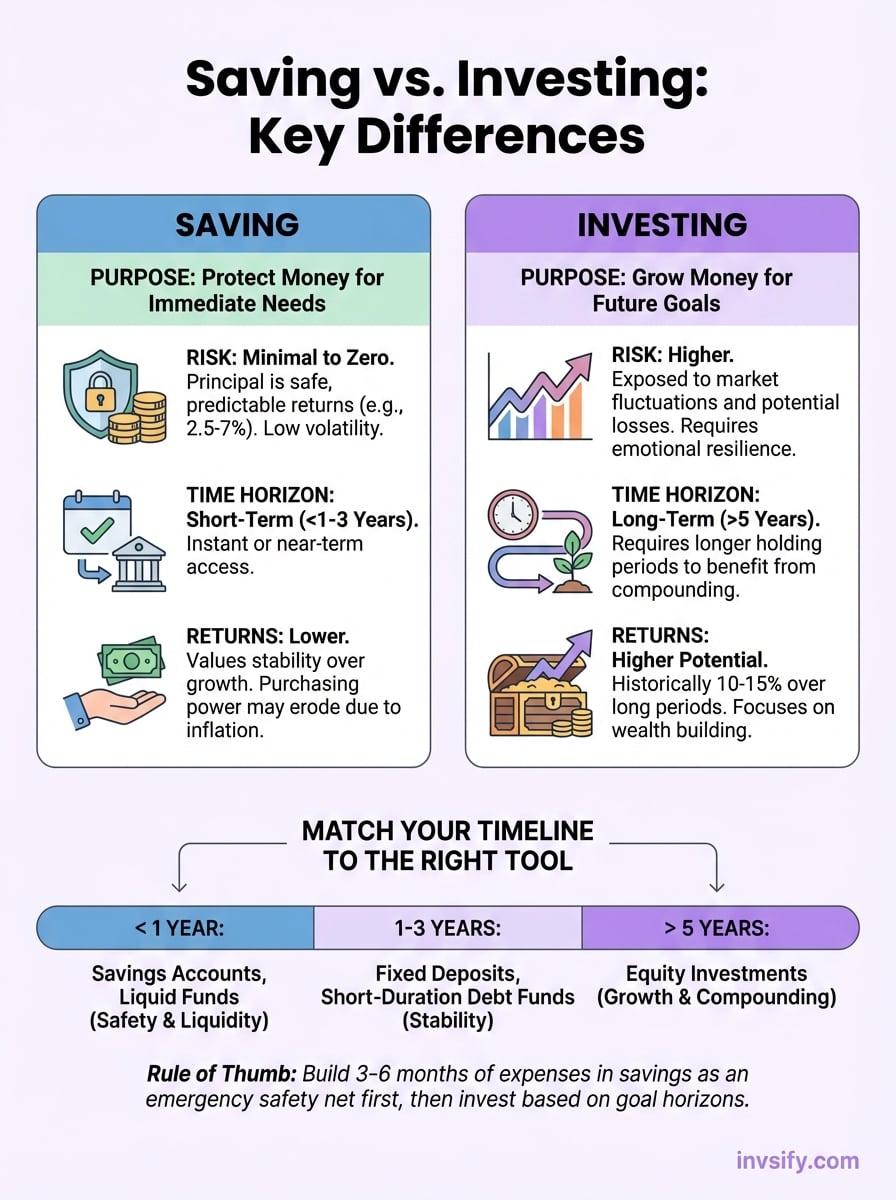

The difference between saving and investing breaks down into three practical dimensions that directly affect how you use each approach. Risk determines how much your money might fluctuate, time horizons dictate when you can access your funds without penalties or losses, and liquidity defines how quickly you can convert assets back to cash. Understanding these three factors helps you match the right financial tool to each specific goal.

Risk and volatility

Saving carries minimal to zero capital risk. Your principal remains intact, protected by deposit insurance up to ₹5 lakhs per bank account. Returns stay predictable and stable, typically ranging from 2.5% to 7% annually depending on the product type. You know exactly what you'll have at the end of each month.

Investing exposes you to market fluctuations and potential losses. Equity investments can swing 10-20% in either direction within months, while debt funds face interest rate risks. However, this volatility comes with higher expected returns of 10-15% annually over long periods. Your account balance changes daily based on market conditions, requiring emotional resilience during downturns.

The price of higher returns through investing is accepting short-term volatility that savings never require you to endure.

Time horizons and liquidity

Savings shine when you need immediate or near-term access to your money. Withdrawals happen instantly or within 1-2 business days without any loss to your principal. This makes saving ideal for goals within three years or emergency funds where timing uncertainty demands total flexibility.

Investments require longer holding periods to smooth out market volatility and realize compounding benefits. Selling equity investments within 1-2 years often means crystallizing losses or missing recovery periods. While you can technically withdraw anytime, doing so during market downturns forces you to lock in paper losses as real ones. Plan to hold investments for at least five years for equity and three years for debt instruments.

How to choose between saving and investing

You don't need complex formulas or financial expertise to decide where your money belongs. The difference between saving and investing becomes clear when you apply a simple framework based on when you need the money and what purpose it serves. Start by categorizing every rupee you earn into three time buckets: immediate needs (within 1 year), medium-term goals (1-5 years), and long-term objectives (beyond 5 years). This classification automatically tells you which financial tool matches each requirement.

Match your timeline to the right tool

Money you need within 12 months belongs in savings accounts or liquid funds where principal safety matters more than returns. This includes your monthly expenses, planned purchases, and any amount earmarked for short-term commitments. Between 1-3 years, consider fixed deposits or short-duration debt funds that offer slightly better returns while maintaining reasonable stability.

Your investment horizon determines your risk capacity, not your risk tolerance or market sentiment.

Beyond 5 years, equity investments make sense because you have enough time to ride out market cycles and benefit from compounding. The longer your horizon, the more aggressively you can allocate toward growth assets. A 10-year goal can handle 70-80% equity allocation, while a 20-year retirement fund can go even higher without compromising your final outcome.

Your financial safety net comes first

Build 3-6 months of expenses in instantly accessible savings before investing anything. This emergency fund protects you from forced liquidation of investments during market downturns when you face unexpected costs. Calculate your monthly burn rate, multiply by six, and keep that amount in a savings account or overnight fund regardless of the opportunity cost.

Once your safety net exists, direct new savings toward investments based on your goal timelines. You're not choosing between saving and investing; you're doing both in the right proportion for your specific situation.

Real-life examples for common Indian goals

You understand the theory, but applying the difference between saving and investing to your actual financial goals makes the concept concrete. Let's look at scenarios most salaried Indians face, showing you exactly where your money should go based on timing and purpose. These examples use realistic numbers that reflect typical middle-class financial situations in India today.

Emergency fund and wedding in 18 months

Rajesh earns ₹8 lakhs annually and needs ₹5 lakhs for his wedding planned for next year. He also wants to build an emergency fund covering six months of expenses at ₹30,000 monthly. His wedding fund belongs entirely in a savings account or liquid fund because he cannot risk market volatility when the date is fixed. A 10% market correction right before his wedding would force him to either postpone or borrow.

Fixed-date goals with short timelines eliminate investment as an option, regardless of how attractive market returns appear.

His ₹1.8 lakh emergency fund also stays in instant-access savings, accepting 3-4% returns as the price of liquidity. These funds might earn less, but they prevent financial disasters that cost far more in interest and stress.

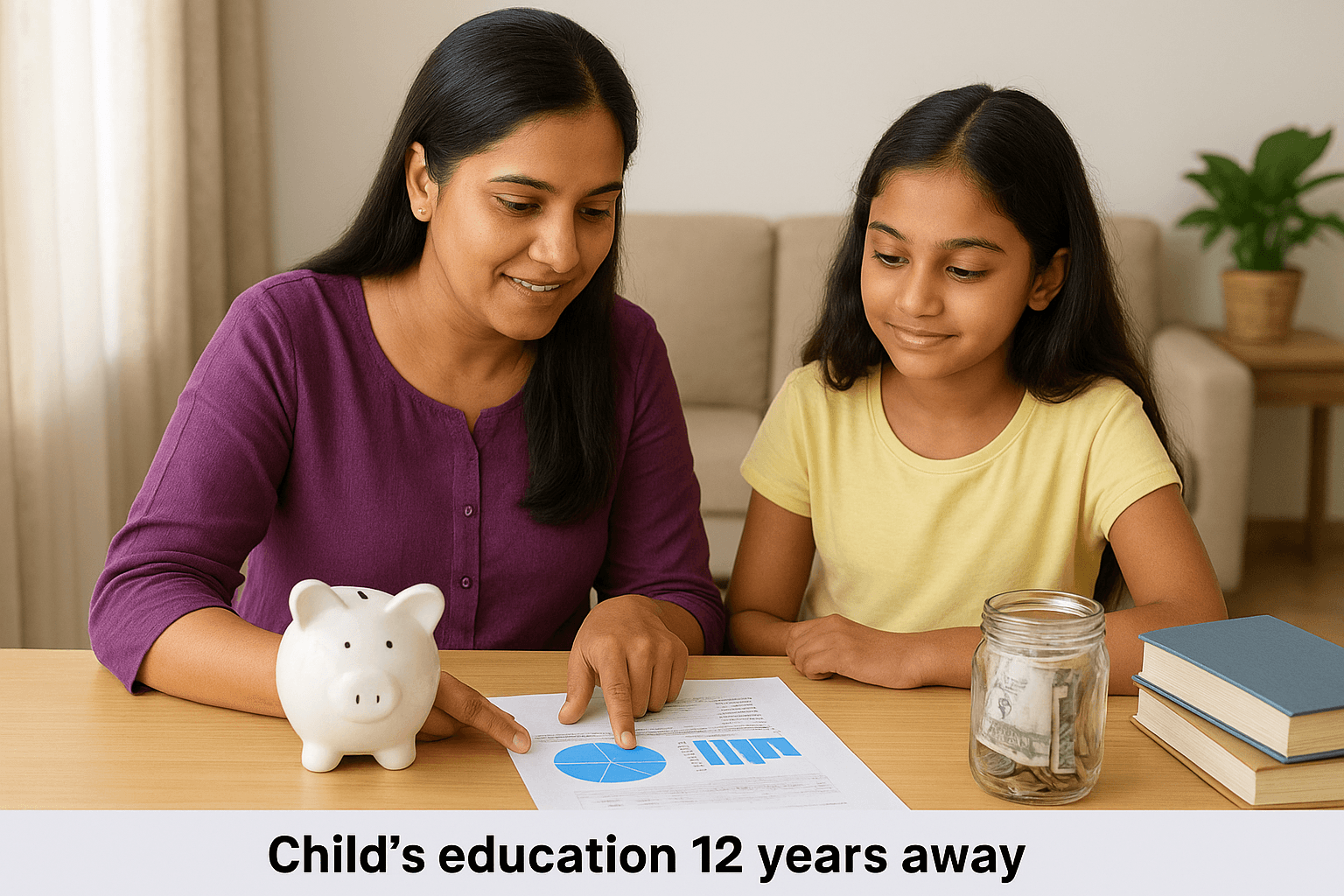

Child's education 12 years away

Priya wants to accumulate ₹25 lakhs for her daughter's engineering degree starting in 2038. This long timeline makes equity investments the clear choice. Monthly SIPs of ₹8,500 in diversified equity funds averaging 12% returns should reach her target, while the same goal through 6% fixed deposits would need ₹15,000 monthly, almost double the commitment.

She splits contributions into 70% equity funds and 30% debt instruments, rebalancing annually. As her daughter approaches college age, Priya will gradually shift toward debt to lock in gains. The twelve-year horizon absorbs market volatility while compounding works in her favor, demonstrating why long-term goals demand investment, not saving.

Common mistakes and simple rules of thumb

You'll make better financial decisions by avoiding the three mistakes most salaried Indians repeat. First, they invest emergency funds in equity markets, exposing themselves to forced selling during downturns. Second, they keep long-term retirement money in savings accounts, losing decades of compounding. Third, they confuse investment volatility with actual risk, pulling out during market corrections and crystallizing paper losses into permanent ones. These errors stem from misunderstanding the difference between saving and investing, not from lack of discipline or intelligence.

Treating all goals the same way

Your biggest mistake is using one financial product for goals with different timelines. When you put your emergency fund, vacation savings, and retirement corpus all in the same mutual fund or all in fixed deposits, you either accept too much risk or sacrifice too much return. Each goal demands its own allocation based on when you need the money and what happens if you fall short.

Match your money to your timeline, not your comfort level or what your colleague recommends.

Track each goal separately, even if you use similar investment vehicles. Your child's education fund and your retirement corpus might both use equity funds, but they need different risk levels and withdrawal strategies based on their distinct timelines.

Quick decision rules that work

Apply this simple framework: money needed within 1 year stays in savings accounts, period. Between 1-3 years, use fixed deposits or liquid funds. Beyond 3 years, start adding equity exposure, increasing the allocation as your timeline extends. By 5+ years, you can hold 60-70% in equity without taking excessive risk because time becomes your protection.

Rebalance annually by moving gains from equity to debt as goals approach. This locks in your growth while reducing volatility as deadlines near, automating the transition from investing back to saving for each specific target.

Next steps to balance saving and investing

You now understand the difference between saving and investing and how to apply it to your financial goals. Start by auditing your current money: calculate your emergency fund requirement, list every goal with its timeline, and match each rupee to the right product based on when you need it. This exercise takes 30 minutes but clarifies years of financial decisions.

Open separate accounts or funds for distinct goals so you never confuse your emergency buffer with your retirement corpus. Set up automatic monthly transfers that split your income according to your timeline framework: immediate needs go to savings, long-term goals flow into equity investments, and medium-term targets land in fixed-income products. Automation removes emotion from the equation and ensures consistent execution.

If you're unsure about product selection or optimal allocation percentages, get personalized AI-powered advice from Invsify that considers your specific income, goals, and risk capacity. Your financial success depends on implementation, not just understanding.