Dynamic Asset Allocation Meaning: How It Works For Investors

Shlok Sobti

Dynamic Asset Allocation Meaning: How It Works For Investors

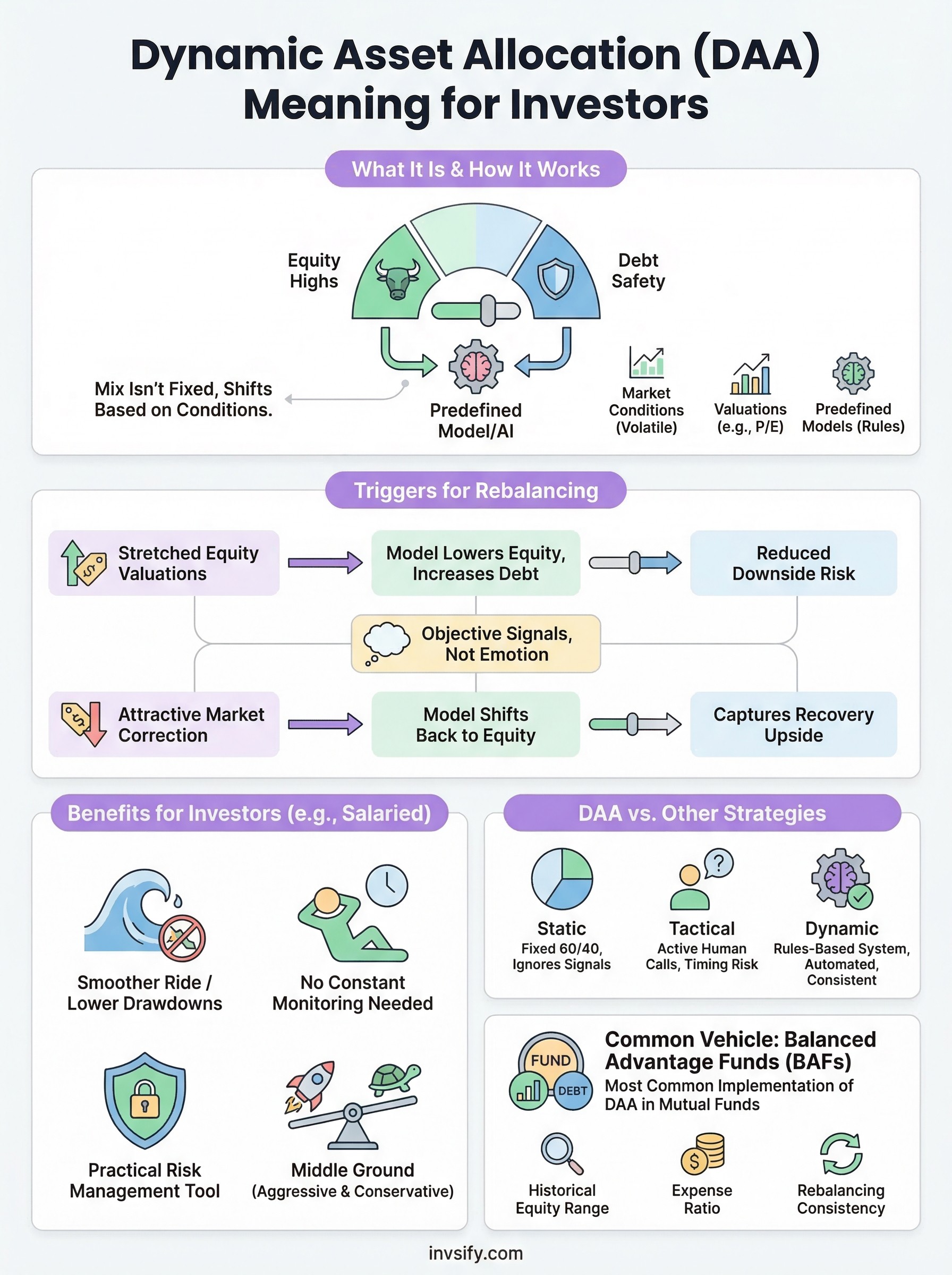

If you've ever watched your portfolio swing between equity highs and debt safety without knowing when to shift, understanding dynamic asset allocation meaning becomes essential. It's an investment strategy where the mix of assets in your portfolio isn't fixed, it shifts based on market conditions, valuations, or predefined models. Instead of you manually deciding when to move money from stocks to bonds (or vice versa), the strategy does the rebalancing for you.

This approach sits at the core of several popular mutual fund categories in India, particularly balanced advantage funds. For salaried investors looking to stay invested across market cycles without constant monitoring, it offers a practical middle ground between aggressive equity exposure and conservative debt parking.

At Invsify, our AI-powered advisory helps you evaluate whether dynamic asset allocation funds align with your risk profile and financial goals, with conflict-free, SEBI-registered guidance you can actually trust. In this article, we'll break down exactly how dynamic asset allocation works, what triggers the rebalancing, and how Indian investors can use it effectively.

Why dynamic asset allocation matters

Most investors in India set up a portfolio once and then leave it alone. That works fine in a stable market, but Indian equity markets are far from stable. Valuations swing hard, interest rate cycles shift, and global events can wipe out months of gains in days. A fixed 60-40 equity-to-debt split that worked in 2020 may expose you to serious downside risk in an overvalued bull market.

The cost of staying static

When you hold a fixed allocation through a full market cycle, you're essentially ignoring valuation signals. If equity markets run up significantly and your allocation stays at 70% equity, you're carrying more risk than you originally planned for. On the flip side, if you stay heavy in debt during a recovery, you miss the upside that equity delivers in the early stages of a bull run.

Staying static in a dynamic market doesn't mean you're being disciplined. It means you're ignoring information your portfolio should be acting on.

Research consistently shows that investor returns are often lower than fund returns because people tend to exit at lows and enter at highs. Dynamic asset allocation reduces this behavior gap by automating the rebalancing decision entirely.

Why it's particularly relevant for Indian investors

India's market moves through distinct cycles driven by corporate earnings, RBI rate decisions, and global liquidity flows. For a salaried investor with limited time to monitor markets, trying to time these shifts manually is unrealistic. Dynamic asset allocation meaning, in practical terms, is having a rules-based system do that work for you, adjusting equity and debt exposure based on objective signals rather than emotion or guesswork.

Some common signals that drive these adjustments include:

Price-to-earnings (P/E) ratios relative to historical averages

Debt market yields indicating interest rate direction

Momentum indicators tracking market trend strength

How dynamic asset allocation works

The mechanics behind dynamic asset allocation meaning are straightforward: a predefined model continuously monitors market signals and adjusts your portfolio's equity-to-debt split in response. When equity valuations appear stretched, the model reduces equity exposure and parks more in debt. When markets correct and valuations become attractive, it shifts back toward equity.

The signals that trigger allocation shifts

Fund managers or algorithm-driven systems track quantitative indicators to decide when and how much to rebalance. The most common signals include:

Price-to-Earnings (P/E) ratio compared to its long-term historical average

Price-to-Book (P/B) ratio signaling over or undervaluation

Momentum indicators tracking market trend direction

Debt yields reflecting interest rate movement

The rebalancing isn't guesswork. Every shift follows a defined rule, which keeps your portfolio aligned with market realities rather than your emotions.

How much equity can shift

In India, most dynamic asset allocation funds hold between 30% and 80% equity, depending on where the market stands. At peak valuations, equity drops to the lower band. At deep corrections, it moves toward the upper band.

No human judgment drives these moves at the individual investor level. The model handles it automatically, which is exactly why this approach suits salaried investors who lack the time to track markets daily.

Dynamic asset allocation in mutual funds

In India, balanced advantage funds are the most common vehicle that applies dynamic asset allocation meaning in practice. These funds are regulated by SEBI and fall under the hybrid fund category, which means they can legally move between equity and debt across a wide range without triggering short-term tax implications for the fund itself. This structure makes them one of the most tax-efficient ways for salaried investors to stay invested across full market cycles.

Balanced advantage funds remove the burden of timing the market from you, letting the fund's model handle that decision systematically.

How balanced advantage funds adjust allocation

Each fund house uses its own proprietary model to decide how much equity to hold at any given time. Some rely primarily on P/E ratios, while others combine multiple indicators like P/B values and momentum scores. The resulting equity range typically sits between 30% and 80%, with the fund rebalancing automatically as signals change.

What to check before investing

Before picking a balanced advantage fund, you want to look at three key factors: the fund's historical equity range to understand how aggressively it moves, the expense ratio to assess cost drag on returns, and the consistency of the rebalancing model across multiple market cycles.

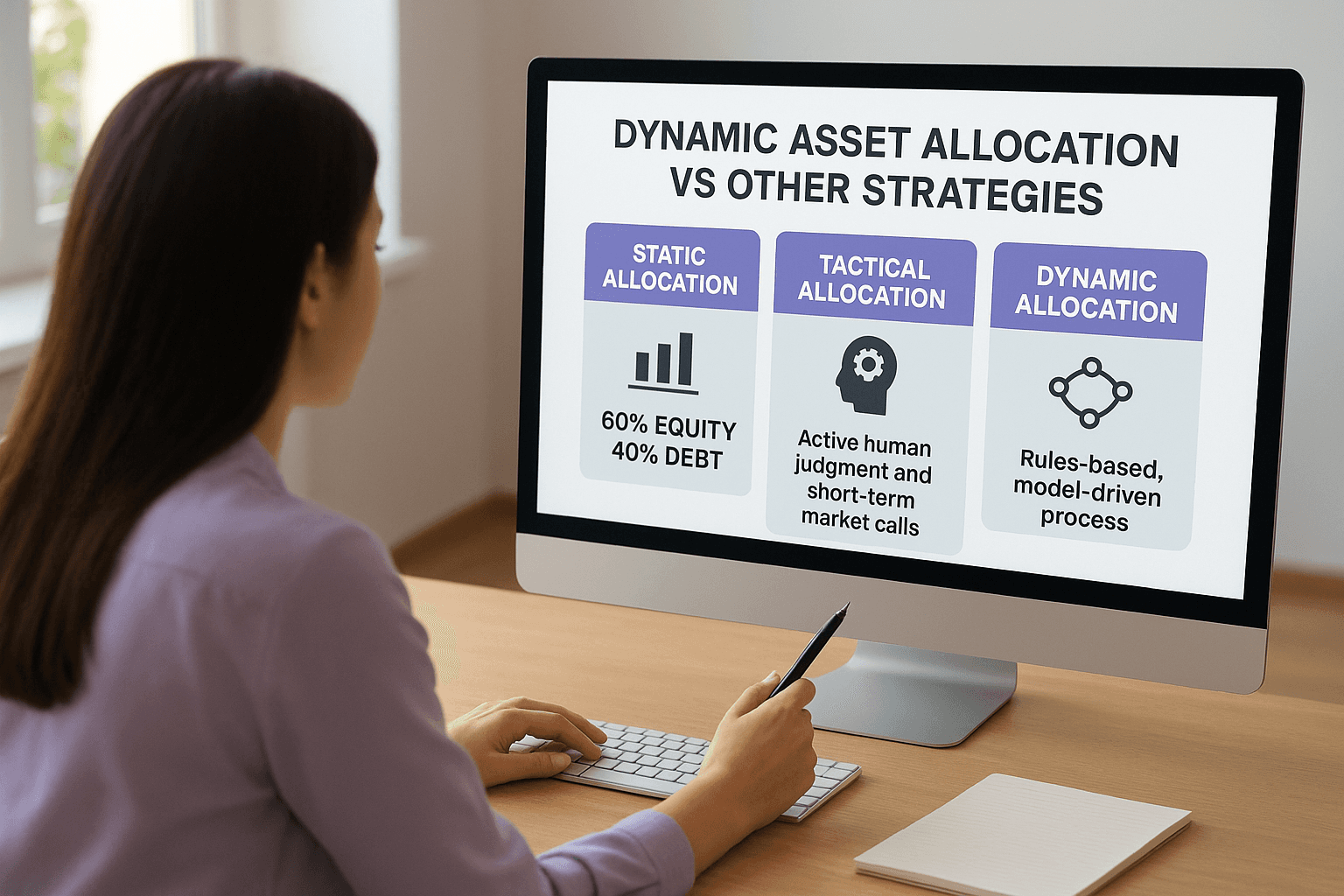

Dynamic asset allocation vs other strategies

Understanding dynamic asset allocation meaning gets clearer when you compare it directly against the other strategies you'll encounter. The three main approaches are static allocation, tactical allocation, and dynamic allocation, and each handles market shifts very differently.

Static allocation

With a static strategy, you set a fixed equity-to-debt ratio, say 60% equity and 40% debt, and rebalance periodically back to that same split regardless of market conditions. This works well in stable environments but leaves you exposed when valuations climb far above historical norms.

A static portfolio in an overheated market isn't conservative. It's just unresponsive.

Dynamic vs tactical allocation

Tactical allocation also adjusts the portfolio mix, but it relies on active human judgment and short-term market calls. A fund manager decides to shift allocation based on their market view, which introduces personal bias and timing risk. Dynamic allocation, by contrast, follows a rules-based, model-driven process that removes that discretion entirely.

For a salaried investor in India who doesn't have time to evaluate fund manager calls, the rules-based nature of dynamic allocation provides more predictability. You know the model will respond to valuation signals consistently, without the emotional swings that often affect human-driven tactical decisions.

Common questions and pitfalls

A few misconceptions trip up investors when they first grasp dynamic asset allocation meaning. The most important thing to understand is that dynamic allocation is a risk management tool, not a return maximization strategy.

Does dynamic allocation guarantee better returns?

No, it doesn't. When equity markets rise sharply, a dynamic fund reduces its equity exposure as valuations stretch. That means it will often underperform a pure equity fund during sustained bull runs. The tradeoff is a significantly smoother ride with lower drawdowns during sharp corrections.

Dynamic allocation trades peak returns for a more consistent, lower-volatility experience across market cycles.

What mistakes do investors make?

The most common mistake is exiting the fund during a correction precisely when the model has shifted toward higher equity and is best positioned for recovery. Investors see short-term underperformance relative to a fixed equity fund and panic, locking in losses right before the rebound.

Another pitfall is ignoring expense ratios. Dynamic funds run more complex models and often carry higher costs than a simple index fund. If the fund you pick charges a high expense ratio without a strong track record of consistent rebalancing, the cost drag quietly erodes your returns over time.

A simple way to get started

Once you understand dynamic asset allocation meaning, the next step is figuring out where it fits in your own portfolio. For most salaried investors in India, a balanced advantage fund makes the most practical entry point. You don't need to pick the rebalancing triggers yourself or monitor valuations daily. The fund's model handles that automatically, letting you stay invested through market cycles without the stress of timing decisions.

Start by reviewing your current portfolio allocation and identifying how much volatility you're actually comfortable with. If you find yourself checking your portfolio every time markets dip, dynamic allocation is likely a better fit than a pure equity fund. The goal is to match your risk tolerance with a strategy that won't push you into panic-selling at the worst possible moment.

Get personalized, conflict-free guidance on dynamic allocation funds from Invsify's AI-powered advisory platform, and find the right fit for your financial goals.