Early Retirement Planning In India: A Step-By-Step Guide

Shlok Sobti

Early Retirement Planning In India: A Step-By-Step Guide

Retiring at 40 or 45 instead of 60 sounds like a dream, until you realize it's mostly a math problem. Early retirement planning in India requires you to think differently about how much you save, where you invest, and how long your money needs to last. The standard retirement playbook doesn't apply here because you're compressing decades of wealth-building into a much shorter window while stretching your corpus across a potentially 40+ year retirement.

The good news? It's absolutely doable for salaried individuals in India, if you have a clear plan. From estimating your target corpus and choosing the right mix of EPF, NPS, mutual funds, and other instruments, to accounting for healthcare costs and inflation, every decision matters. The gap between "I want to retire early" and actually doing it comes down to structured execution, not wishful thinking.

This guide walks you through each step, calculating your retirement number, building your investment strategy, and stress-testing your plan for real-life scenarios. And if you want AI-powered, conflict-free advice to help you optimize this journey, that's exactly what we built Invsify to do: give you data-backed clarity on whether your wealth is truly on track for the retirement timeline you want.

What early retirement means in India

Early retirement in India does not mean the same thing it does in, say, the United States or Europe. In India, you are working with a different social contract: no universal social security, limited public healthcare, and a cultural expectation that families stay financially intertwined across generations. When you stop drawing a salary at 42, you are not just opting out of a job. You are choosing to fund every rupee of your life, your family's needs, and your healthcare costs from a corpus you built during roughly 15 to 20 years of earning.

The Indian definition: not just stopping work

Most people who pursue early retirement planning in India are not chasing total idleness. They want financial independence, meaning the point where work becomes optional, not mandatory. Some continue to consult, freelance, or run a small business after leaving their primary career. What changes is the pressure: you no longer need that income to survive. This distinction matters because it changes how you size your corpus. If you plan to earn even a modest Rs. 30,000 to Rs. 50,000 per month from passion projects post-retirement, your required savings number drops significantly.

Financial independence in India means your investments can sustain your lifestyle indefinitely, not that you will never earn again.

The typical retirement age gap you are closing

The standard retirement age in India sits at 58 to 60 years for most private-sector employees, and 60 years for central government employees. If you want to retire at 45, you are closing a 13 to 15-year gap on the earning side while simultaneously extending your retirement horizon by the same amount. A person retiring at 60 might need their corpus to last 25 years, assuming they live to 85. You need it to last 40 years or more, which fundamentally changes how aggressively you must save and how you must invest.

Key costs that are uniquely high in India

Two costs tend to surprise early retirees in India the most: healthcare and family obligations. Healthcare inflation in India runs at roughly 10 to 14% annually, well above general consumer price inflation. Your health insurance premium at 45 will look nothing like it does at 65, especially if you develop chronic conditions. Beyond that, many Indian families continue to support aging parents or fund children's education and weddings from their own pockets. These are not optional expenses you can simply cut. They are real, recurring financial commitments you must bake into your retirement plan from day one.

Here is a quick breakdown of cost categories that Indian early retirees consistently underestimate:

Healthcare: Annual premiums, out-of-pocket expenses, and long-term care costs

Family obligations: Parental support, children's higher education, and marriage expenses

Lifestyle inflation: Travel, hobbies, and urban cost of living increases over 40 years

Emergency buffer: Sudden home repairs, legal costs, or business losses from a side income

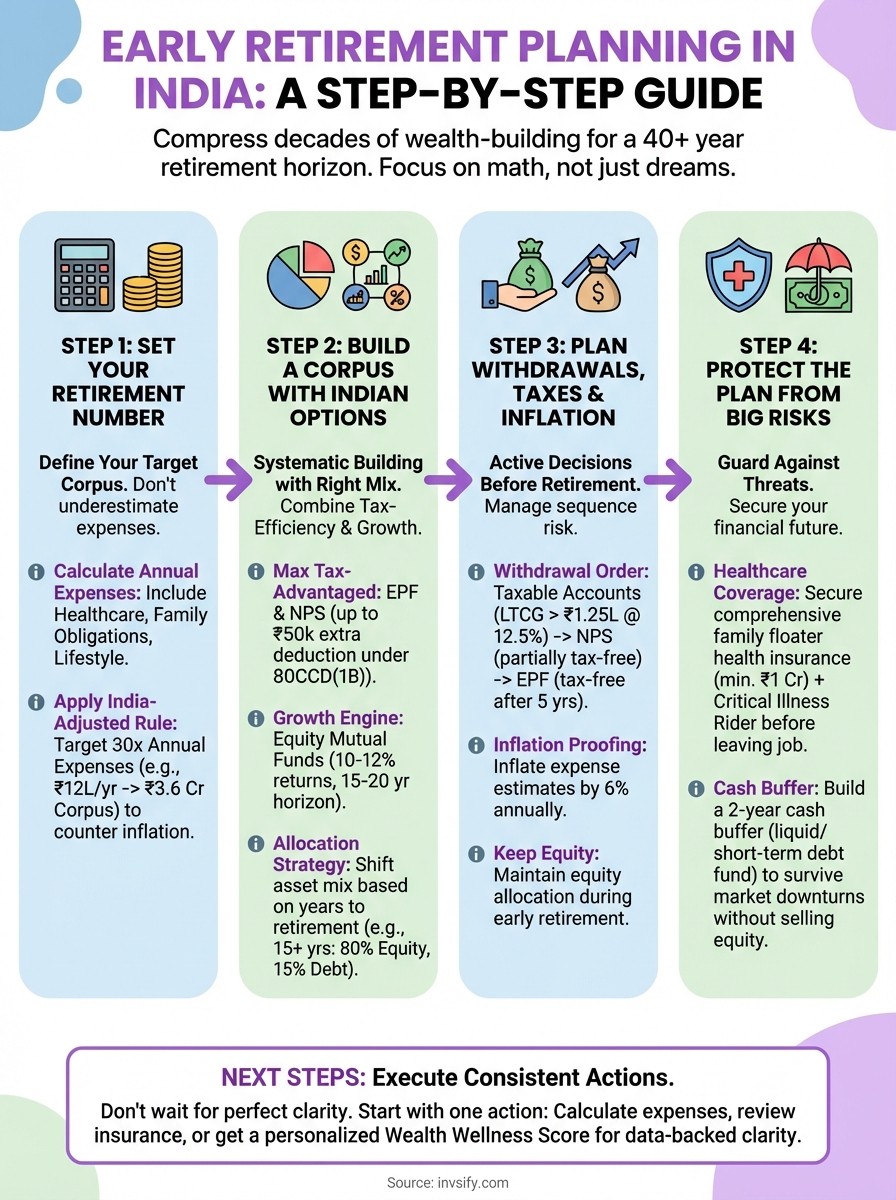

Step 1. Set your retirement number

Your retirement number is the total corpus you need before you can stop working. Most early retirees underestimate this figure because they calculate based on today's expenses without accounting for inflation or the length of retirement. In early retirement planning in India, the first concrete step is arriving at a specific number, not a vague sense that you need "a few crores."

Calculate your annual expenses first

Start by listing everything you spend today, then project what those costs will look like at your target retirement date. Add categories most people skip: healthcare premiums, parental support, children's education, and a buffer for irregular large expenses. Here is a simple template to get started:

Expense Category | Monthly Amount (Rs.) | Annual Total (Rs.) |

|---|---|---|

Household (rent/EMI, food, utilities) | ||

Healthcare (premiums + out-of-pocket) | ||

Family obligations (parents, kids) | ||

Lifestyle (travel, hobbies, subscriptions) | ||

Emergency buffer (5-10% of total) | ||

Total Annual Expense |

Fill this out honestly. Your total annual expense figure becomes the foundation for every calculation that follows.

Apply the 25x rule and adjust for India

The 25x rule states that your corpus should equal 25 times your annual expenses, which corresponds to a 4% annual withdrawal rate. For example, if your annual expenses are Rs. 12 lakhs, your base target corpus is Rs. 3 crore. However, India's healthcare inflation and longer retirement horizon push this higher.

For a 40-year retirement in India, many planners recommend targeting 30x to 33x your annual expenses instead of the standard 25x.

A more conservative and India-specific target is: Annual Expenses x 30 = Your Retirement Number. Using the Rs. 12 lakh example, that becomes Rs. 3.6 crore as your adjusted target. Revisit this number every two to three years as your income and lifestyle costs change.

Step 2. Build a corpus with Indian options

Once you have your retirement number, your next job is to build it systematically using the investment instruments available in India. The right mix depends on your age, risk tolerance, and target retirement date. Early retirement planning in India works best when you combine tax-efficient government schemes with higher-growth market instruments rather than relying on any single avenue.

Lock in the tax-advantaged foundations first

EPF (Employee Provident Fund) is non-negotiable if your employer offers it. You contribute 12% of your basic salary, your employer matches it, and the entire amount compounds tax-free at a rate the EPFO sets each year (recently around 8.25%). NPS (National Pension System) adds another layer: your Tier I contributions qualify for deductions under Section 80C and an additional Rs. 50,000 under Section 80CCD(1B). Max both before you invest anywhere else.

Maxing your NPS deduction under Section 80CCD(1B) saves you Rs. 15,000 in taxes annually if you are in the 30% bracket, effectively delivering a guaranteed 30% return on that portion before market performance even enters the picture.

Add equity mutual funds for long-term growth

After your tax-advantaged accounts are maxed, direct-plan equity mutual funds become your primary wealth-building engine. Over a 15 to 20-year horizon, a diversified equity portfolio has historically delivered 10 to 12% annualized returns in India. Index funds tracking Nifty 50 or Nifty Next 50 keep your expense ratio under 0.2%. Set up a monthly SIP and increase it by 10% each year in line with your salary increments.

Match your allocation to your timeline

Your asset mix should shift based on years left to retirement, not just your age. Here is a concrete allocation framework you can apply directly:

Years to Retirement | Equity (%) | Debt/Bonds (%) | Gold/Others (%) |

|---|---|---|---|

15+ years | 80 | 15 | 5 |

8-15 years | 65 | 25 | 10 |

3-8 years | 50 | 40 | 10 |

Rebalance your portfolio annually to stay within these target bands as market movements shift your actual allocation over time.

Step 3. Plan withdrawals, taxes, and inflation

Building a corpus is only half the job. How you draw down that corpus determines whether your money lasts 40 years or runs out in 25. In early retirement planning in India, withdrawal strategy, tax efficiency, and inflation-proofing are not afterthoughts. They are active decisions you need to make before Day 1 of retirement.

Structure your withdrawal order to minimize taxes

Your accounts carry different tax treatments, so the sequence in which you withdraw matters enormously. A poor withdrawal order can cost you lakhs in avoidable taxes over a decade. Follow this priority framework when drawing down your investments:

Start with taxable mutual fund accounts: Long-term capital gains (LTCG) on equity funds above Rs. 1.25 lakh are taxed at 12.5%, which is the lowest rate you will face on invested assets.

Use NPS corpus carefully: At age 60, 60% of your NPS corpus is tax-free. If you retire at 45, plan partial withdrawals within the scheme's allowed rules to avoid triggering unnecessary tax events.

Preserve EPF until at least 58: EPF withdrawals after five continuous years of service are fully tax-free. Pulling this corpus early without meeting the conditions creates a taxable event you want to avoid entirely.

Sequence risk in withdrawals is just as dangerous as market risk. Withdrawing from equity accounts during a downturn forces you to sell units at depressed prices, permanently shrinking your corpus in a way that cannot recover.

Account for inflation in your projections

India's consumer price inflation has averaged 5 to 6% annually over the last decade, but categories like healthcare and education run well above that. To keep your withdrawal plan grounded, inflate your annual expense estimate by 6% each year in your projections rather than holding costs flat.

Here is a concrete example: if you need Rs. 12 lakhs per year today, you will need roughly Rs. 38.6 lakhs per year in 20 years at 6% annual inflation. Your withdrawal amounts must rise alongside this, which means keeping a meaningful equity allocation throughout early retirement, not just in the years before it.

Step 4. Protect the plan from big risks

A well-built corpus can still unravel if you leave the plan exposed to risks you could have managed. Early retirement planning in India is not complete until you account for the threats that sit outside your investment spreadsheet: a medical emergency, a market crash in your first retirement year, or a gap in insurance coverage that wipes out five years of savings in a single event.

Guard against healthcare costs with the right coverage

Your health insurance strategy needs to be locked in before you retire, not after. Once you leave employment, your group health cover disappears. Buying individual coverage at 50 or 55, especially with pre-existing conditions, becomes dramatically more expensive or comes with exclusions. Buy a comprehensive family floater plan with a minimum cover of Rs. 1 crore while you are still employed and healthy, then add a super top-up plan to extend coverage at a lower premium. Pair this with a dedicated healthcare corpus, a liquid fund or fixed deposit of at least Rs. 10 to 15 lakhs, specifically earmarked for out-of-pocket expenses that insurance does not cover.

Minimum base health cover: Rs. 1 crore (family floater)

Super top-up: Rs. 50 lakhs to Rs. 1 crore additional cover

Dedicated healthcare liquid buffer: Rs. 10 to 15 lakhs

Critical illness rider: strongly recommended before age 45

Build a cash buffer to survive market downturns

Sequence-of-returns risk is the single biggest threat to a long early retirement. If markets fall 30% in your first two retirement years and you are selling equity units to fund living expenses, your corpus takes a permanent hit it may never recover from. The fix is a two-year cash buffer in a liquid fund or short-term debt fund, equal to roughly two years of annual expenses. This buffer lets you leave your equity portfolio untouched during downturns and gives markets time to recover before you need to draw from them again.

Keep your cash buffer separate from your emergency fund. These serve different purposes, and mixing them leaves both functions underfunded.

Next steps

Early retirement planning in India is not a single decision; it is a series of connected actions that build on each other. You now have the four steps that matter most: setting a concrete retirement number, choosing the right investment mix, structuring withdrawals to minimize taxes, and protecting your plan from the risks that derail most early retirees. The biggest mistake you can make at this point is waiting until everything feels perfectly clear before you start.

Pick one action from this guide and execute it this week. Calculate your annual expenses, check your NPS contribution limit, or review your health insurance cover against the benchmarks laid out in Step 4. Small moves made consistently compound into the financial independence you are aiming for. If you want a clearer picture of exactly where your wealth stands today and what it will take to hit your retirement target, get your personalized Wealth Wellness Score on Invsify and let the numbers guide your next move.