Education Loan Interest Deduction Under Section 80E Guide

Shlok Sobti

Education Loan Interest Deduction Under Section 80E Guide

If you've taken an education loan, for yourself, your spouse, or your children, the interest you pay on it can reduce your taxable income. That's exactly what the education loan interest deduction under Section 80E of the Income Tax Act allows you to do. Yet, a surprising number of salaried individuals in India either don't know about this benefit or fail to claim it correctly, leaving real money on the table every year during tax season.

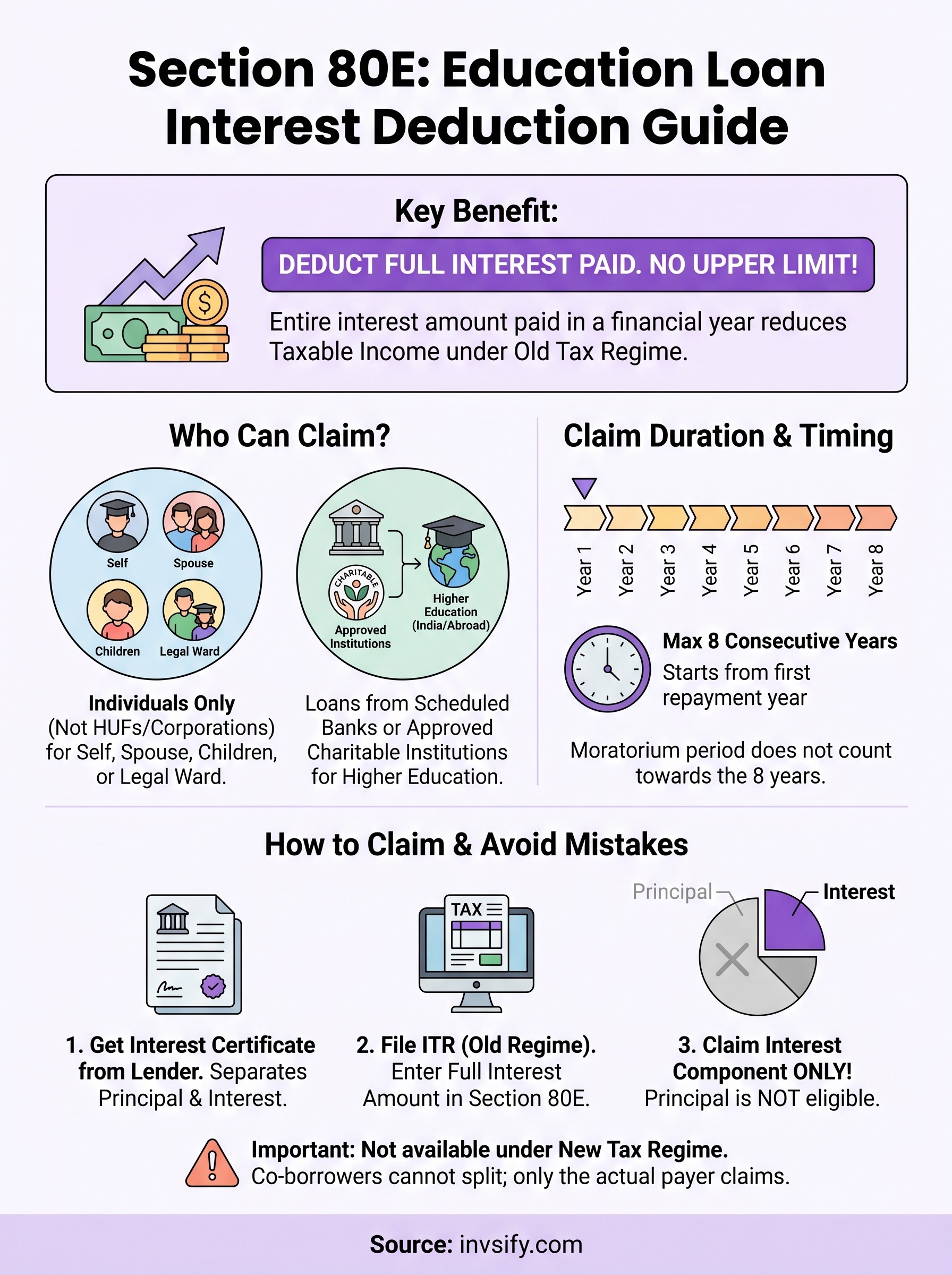

Section 80E is straightforward in principle: you pay interest on a qualifying education loan, and you get to deduct that entire interest amount from your gross total income. There's no upper limit on how much you can claim. But the details matter, who qualifies, what counts as a recognized institution, how long the deduction lasts, and why only the interest component (not the principal) is eligible. Getting these right is the difference between a smooth claim and a missed opportunity.

This guide breaks down everything you need to know about Section 80E, eligibility rules, claim duration, documentation, and common mistakes to avoid. At Invsify, our AI-powered advisory platform helps salaried Indians optimize their tax-saving strategies and build wealth with conflict-free, data-backed advice. Understanding deductions like 80E is one piece of that puzzle, and we're here to make sure you don't miss a single rupee in legitimate savings.

Why Section 80E matters for salaried taxpayers

For most salaried professionals in India, an education loan is one of the largest financial commitments they carry into their working years. Whether you borrowed to fund your own postgraduate degree or took a loan for your child's college education abroad, the monthly interest outflow can be substantial over a repayment period of several years. Section 80E gives you a direct way to reduce that burden by converting your interest payments into a tax deduction, effectively lowering the income on which the government taxes you.

The real cost of an education loan without tax planning

Education loans in India typically carry interest rates between 8% and 14% per annum, and for larger loans covering overseas studies, the total interest paid over the full repayment period can run into several lakhs of rupees. If you're a salaried individual in the 30% tax bracket, every rupee of interest you pay without claiming Section 80E is a rupee taxed at your highest slab rate. Over a loan tenure of seven or eight years, that adds up to a significant amount of money left unclaimed.

Consider a straightforward example. You pay Rs. 1,20,000 in education loan interest in a financial year. Under Section 80E, you can deduct that full amount from your gross total income. If you sit in the 30% slab, that translates to a tax saving of Rs. 36,000 in that single year alone. Multiply that across eight eligible years, and the total tax saving from this one deduction can comfortably cross Rs. 2,50,000 or more, depending on your loan size and the interest rate you're paying. That's real money, not a rounding error on your tax return.

Section 80E has no upper cap on the deduction amount, which makes it one of the most valuable yet underused benefits available to salaried taxpayers with education loans.

How Section 80E reduces your actual loan burden

The education loan interest deduction under Section 80E works differently from most other deductions under Chapter VI-A of the Income Tax Act. Deductions like 80C come with a hard ceiling of Rs. 1,50,000 per year. Section 80E places no such ceiling, which means if you paid Rs. 3,00,000 in interest in a financial year, you can deduct the entire Rs. 3,00,000 from your gross total income. This becomes especially powerful for large loans taken for professional degrees or international education, where interest amounts in the early years of repayment can be very high.

For salaried taxpayers filing under the old tax regime, this deduction directly reduces your taxable income before slab rates apply. It doesn't function as a rebate or a tax credit; it reduces the actual base on which your tax is computed. So the higher your income and tax bracket, the more valuable the deduction becomes in absolute rupee terms. If you've already maxed out your 80C limit through PPF, ELSS, or life insurance premiums, and you've covered health insurance under 80D, Section 80E is often the next logical step to further reduce your tax liability without parking additional money anywhere new. You simply claim the interest you're already paying on a loan you already have.

Who can claim Section 80E and which loans qualify

Section 80E applies to individual taxpayers only. Hindu Undivided Families (HUFs) and corporate entities cannot claim this deduction. If you're a salaried individual who has taken an education loan in your own name, or in the name of a family member you are legally responsible for, you can claim the deduction on the interest you actually pay during a financial year.

Who qualifies as an eligible borrower

You must be the actual loan borrower to claim the deduction. The Income Tax Act defines the eligible relationships clearly: you can claim if the loan was taken for your own higher education, or for your spouse, children, or a student for whom you are the legal guardian. Parents are explicitly covered under this definition, which makes Section 80E relevant not just for young professionals repaying their own student loans, but also for parents who took loans to fund a child's degree.

One point worth noting is that both spouses cannot claim the same loan's interest separately. Only the person who is actually making the repayments can claim the deduction in a given year.

Section 80E is available only to individuals, not HUFs, and only the person making the actual repayment can claim the deduction.

What counts as a qualifying loan

The education loan interest deduction under Section 80E is available only on loans taken from scheduled financial institutions or approved charitable institutions. This covers nationalized banks, private banks regulated by the Reserve Bank of India, and certain notified charitable organizations. Loans taken from friends, family members, or your employer do not qualify, regardless of how the money was used.

Beyond the lender, the purpose of the loan also matters. The loan must be taken specifically for higher education, which the Income Tax Act defines as any full-time course pursued after passing the Senior Secondary Examination, Class 12. This includes graduate and postgraduate programs in India and abroad, as well as professional and vocational courses across recognized fields. There is no restriction on the subject area, so engineering, medicine, management, law, and arts programs all qualify, provided the institution is recognized and the course meets the Act's definition of higher education.

How to claim the Section 80E deduction step by step

Claiming the education loan interest deduction under Section 80E does not require any special form or separate application to the Income Tax Department. You claim it directly through your Income Tax Return, and the process is simpler than most salaried taxpayers expect. The key is having the right document from your lender before you sit down to file.

Get your interest certificate from your lender

Your lender is the starting point. Before filing your return, contact your bank or financial institution and request an interest certificate for the relevant financial year. This document breaks down your total repayment into two components: the principal portion and the interest portion. Only the interest portion is eligible for the Section 80E deduction, so this certificate is what you'll use to determine the exact amount you can claim.

Most scheduled banks issue these certificates automatically around March or April. If yours hasn't arrived by the time you're ready to file, call the branch or download it from your net banking portal. Keep this certificate safely as supporting documentation; the Income Tax Department may ask for it during scrutiny or assessment.

Do not rely on your EMI payment records alone. Only the interest component qualifies under Section 80E, and the certificate is the only document that clearly separates the two.

Report the deduction correctly in your ITR

Once you have the interest certificate, open your ITR form under the old tax regime (note: Section 80E deductions are not available if you opt for the new tax regime under Section 115BAC). In the deductions schedule, locate Chapter VI-A deductions and find the specific field for Section 80E. Enter the total interest amount exactly as stated on your certificate.

Your employer's Form 16 may or may not reflect this deduction depending on whether you submitted the certificate to your HR or payroll team during the year. If they missed it, you can still claim it directly while filing your return. The tax department processes the deduction regardless of whether it appears in Form 16, as long as you report it correctly in your ITR and hold the supporting certificate.

How much you can claim and for how long

The education loan interest deduction under Section 80E has two defining features that separate it from most other deductions: there is no upper limit on the amount you can claim, and the benefit runs for a fixed number of years. Understanding both together helps you plan your repayment strategy far more effectively.

The no-cap rule on deduction amount

Section 80E allows you to deduct the entire interest amount you pay in a financial year, with zero restriction on the maximum figure. Whether your annual interest outflow is Rs. 50,000 or Rs. 5,00,000, you can claim the full amount. This makes it especially valuable for loans covering professional degrees or international programs, where the borrowed amount and the corresponding interest are both significantly higher than a typical domestic undergraduate loan.

The absence of a deduction ceiling means Section 80E becomes more powerful as your loan size increases, which is the opposite of how most capped deductions work.

Your interest component tends to be highest in the early years of repayment, because EMIs are structured so that interest makes up a larger share of each payment at the start of the loan tenure. This means your annual deduction will be largest in the first two or three years after repayment begins, and it gradually decreases as the outstanding principal reduces.

The 8-year limit on claim duration

Your deduction window starts from the financial year in which you begin repaying the loan and runs for a maximum of eight consecutive years, or until you repay the loan in full with interest, whichever comes earlier. If you clear the loan in five years, your deduction period ends at five years. You cannot extend the window or carry it forward past the eighth eligible year.

This time limit makes early repayment planning matter. If you defer repayment unnecessarily, you risk losing some of your eligible deduction years entirely. Confirm your repayment start date with your lender, and make sure you begin claiming in the correct assessment year so you don't accidentally forfeit one of your eight years of legitimate tax savings.

Common mistakes, edge cases, and quick FAQs

Even straightforward deductions like the education loan interest deduction under Section 80E come with pitfalls. Most errors fall into two categories: incorrect loan classification and wrong tax regime selection. Knowing where taxpayers typically go wrong helps you avoid the same traps.

Mistakes that cost you the deduction

The most common error is claiming the full EMI amount instead of just the interest component. Your EMI includes both principal repayment and interest, and only the interest qualifies under Section 80E. If you enter your total annual EMI in the deduction field, you are overclaiming, which can trigger a tax notice. Always use the interest certificate from your lender as the source figure, nothing else.

A second significant mistake is opting for the new tax regime without realizing that Section 80E is not available under it. If you switched to the new regime for the lower slab rates without accounting for this deduction, you may have paid more tax than necessary. Run the numbers under both regimes before filing, especially if your annual interest outflow is high.

Switching to the new tax regime eliminates your Section 80E benefit entirely, so always compare your net tax liability under both regimes before making the choice.

Edge cases worth knowing

Two situations trip people up regularly. First, if both spouses are co-borrowers on the same education loan, only one person can claim the deduction in a given year, specifically the one who is actually making the repayment. Splitting the deduction between two ITRs is not permitted.

Second, the moratorium period on an education loan does not count as a repayment year. Your eight-year deduction window begins only when actual repayments start, so a two-year moratorium after graduation does not reduce your eligible claim years.

Quick FAQs

Can I claim Section 80E if my employer didn't include it in Form 16? Yes. You can add it directly in your ITR under the Chapter VI-A deductions section, provided you hold the interest certificate.

Does the course location matter? No. Loans covering studies in India or abroad both qualify, as long as the lender is a scheduled bank or an approved charitable institution and the course meets the definition of higher education under the Act.

Key takeaways

The education loan interest deduction under Section 80E is one of the most underused tax benefits available to salaried individuals in India. You can deduct your full annual interest payment from gross total income with no upper limit, and the benefit runs for up to eight consecutive years from when repayment begins. Only individuals qualify, only scheduled banks and approved charitable institutions count as valid lenders, and the deduction is available only under the old tax regime. Your principal repayment never qualifies, so always use the interest certificate from your lender to arrive at the exact claim figure. If you're a co-borrower, only the person actually making the repayments can claim it in a given year.

Tax planning goes well beyond a single deduction. If you want personalized, conflict-free advice on optimizing your full tax and investment strategy, start your wealth journey with Invsify and let AI-powered guidance do the heavy lifting for you.