ET Money Retirement Calculator: How To Plan Your Corpus

Shlok Sobti

ET Money Retirement Calculator: How To Plan Your Corpus

Figuring out how much money you actually need to retire comfortably is one of the trickiest parts of financial planning. The ET Money retirement calculator is a popular starting point for many Indian investors trying to estimate their retirement corpus, and for good reason. It's free, easy to use, and gives you a quick snapshot of your future financial needs based on inputs like your age, expenses, and expected returns.

But here's the thing: a calculator gives you a number. It doesn't tell you what to do next, which funds to pick, how to allocate across asset classes, or when to rebalance. That's where the gap between planning and execution becomes real. At Invsify, we bridge that gap with AI-powered, SEBI-registered investment advisory that turns your retirement target into an actionable, personalized strategy, minus the hidden commissions.

In this guide, we'll walk you through how to use ET Money's retirement planning tools step by step, break down what the results actually mean, and show you how to move from a corpus estimate to a concrete investment plan that works for your income and goals.

What the ET Money retirement calculator does

ET Money doesn't give you a single retirement calculator. It gives you four separate tools, each designed to answer a different retirement planning question. Understanding what each one does before you start entering numbers saves you from making the wrong assumptions about your future corpus. The et money retirement calculator suite covers the general retirement corpus estimate, the NPS calculator, the EPF calculator, and the FIRE calculator, and each one works differently under the hood.

The four retirement planning tools available

ET Money separates its retirement tools by use case rather than bundling everything into one form. This structure is actually useful because different investors have different retirement vehicles, and lumping them all together would produce inaccurate estimates.

Tool | Primary use case | Key output |

|---|---|---|

Retirement Calculator | General corpus planning | Monthly investment needed |

NPS Calculator | National Pension System projections | Lump sum + annuity split |

EPF Calculator | Employee Provident Fund growth | Projected EPF balance at retirement |

FIRE Calculator | Early retirement planning | Target corpus for financial independence |

Each tool pulls from the same core logic: your current age, your retirement age, your expected expenses, and assumed rates of return. But the NPS and EPF calculators also factor in contribution rules specific to those schemes.

How the core retirement calculator works

The general retirement calculator is the one most people use first. You enter your current monthly expenses, your age, the age you want to retire, and how long you expect to live after retiring. The calculator then applies an inflation rate (typically 6%) to project what your monthly expenses will look like in the future.

The calculator doesn't just estimate your corpus at retirement. It also tells you how much you need to invest every month, starting now, to actually reach that number.

It assumes a pre-retirement return rate (usually around 10-12% for equity-heavy portfolios) and a post-retirement return rate (typically 7-8% for more conservative holdings). These defaults reflect realistic long-term market behavior for Indian investors, though you can adjust them.

What the NPS and FIRE calculators add

The NPS calculator goes a step further by breaking your projected corpus into two parts: the lump sum you can withdraw tax-free at retirement (up to 60% of the corpus) and the portion that must go into an annuity. This split matters because annuity returns in India are often lower than what you could earn through a self-managed withdrawal strategy.

The FIRE calculator works on a different principle entirely. Instead of targeting a retirement age, you enter your target monthly income and work backward to find the corpus you need to sustain that income indefinitely, using the 4% withdrawal rule as the baseline.

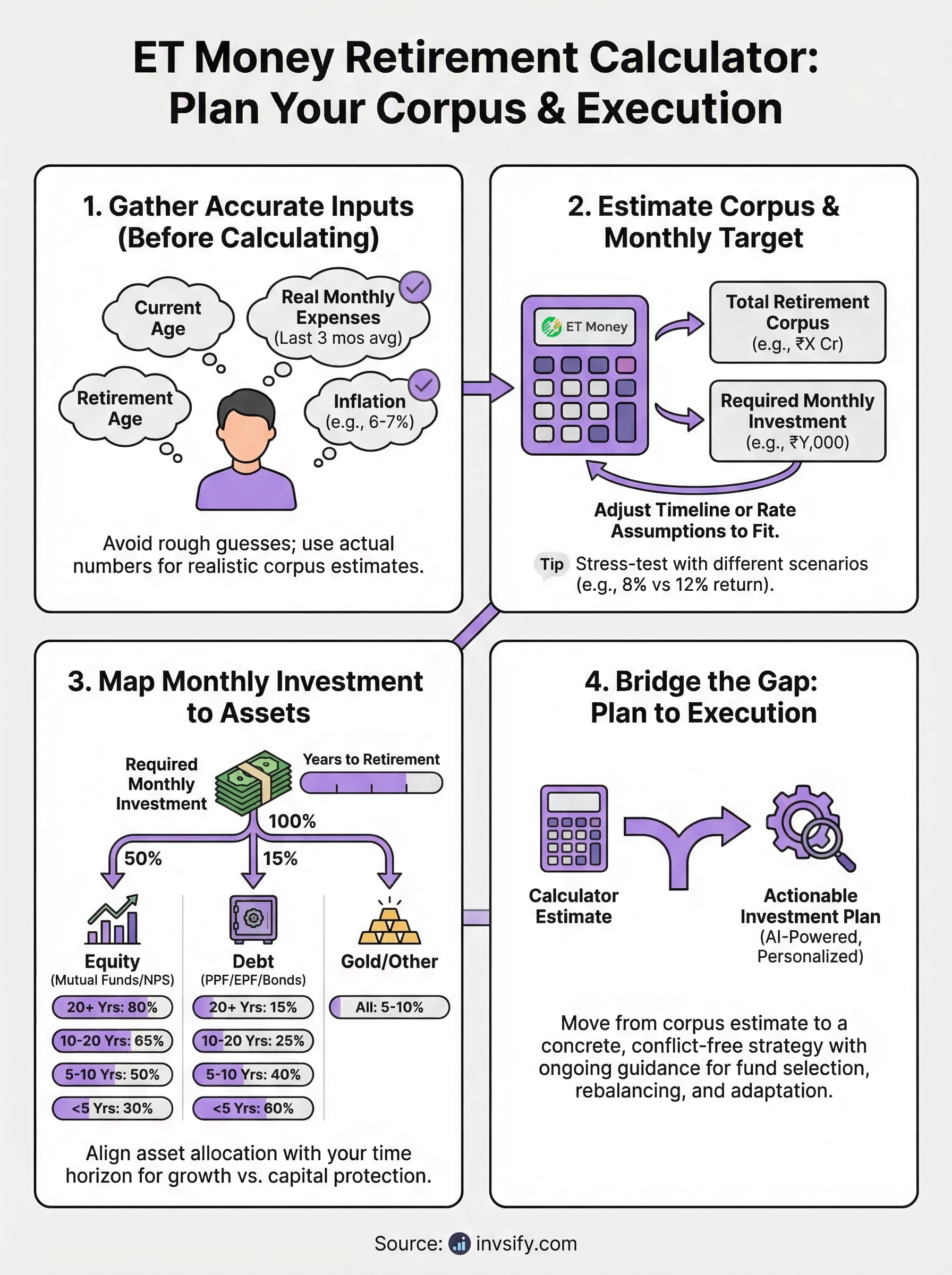

Step 1. Gather the inputs you need first

Before you open the ET Money retirement calculator, spend five minutes pulling together the numbers you actually need. Entering rough guesses here leads to a corpus estimate that's off by lakhs, sometimes crores, depending on your income level and timeline. Accurate inputs produce a useful output; vague inputs just give you a false sense of security.

Your personal financial baseline numbers

The calculator asks for facts about your current life, not projections. You need your current age, the age at which you plan to retire, and your current monthly household expenses (not income). Use your actual average monthly spend from the last three months, not what you think you spend. If you track expenses through a bank statement or app, pull the real figure rather than estimating.

Input | What to use | Common mistake |

|---|---|---|

Current age | Your actual age today | Using a rounded number |

Retirement age | Your genuine target, not default 60 | Accepting the default without thinking |

Monthly expenses | Last 3-month average household spend | Using only personal, not full household, expenses |

Life expectancy | 85 if healthy, 90 if being conservative | Underestimating how long you'll live |

Underestimating your monthly expenses is the single biggest reason retirement corpus estimates fall short in practice.

The rate assumptions you control

Beyond your personal facts, the calculator lets you set return rate assumptions and an inflation rate. Most people leave the defaults untouched, but these numbers carry a compounding effect over 20-30 years, so they deserve a second look. A pre-retirement return of 10-12% is reasonable for a diversified equity portfolio. Use 6-7% for inflation rather than the flat 6% default if you live in a metro city where costs rise faster. Post-retirement, drop your assumed return to 7-8% since your portfolio should shift toward safer, income-generating assets as you approach and enter retirement.

Step 2. Estimate your retirement corpus in ET Money

Open the ET Money retirement calculator and navigate to the retirement planning section. With your baseline numbers ready from Step 1, enter your current age and target retirement age first. These two inputs define your investment timeline, and the calculator uses this gap to determine how aggressively your monthly contribution needs to compound toward your target corpus.

Enter your numbers in the right order

The calculator presents its fields in a logical sequence, so work through them top to bottom without skipping. Start with your current monthly expenses rather than your income. The tool then inflates this figure to project your future monthly need. Enter your assumed inflation rate next, followed by your expected pre-retirement return rate and your post-retirement return rate. Each number builds on the previous one, so accuracy here directly affects the corpus estimate.

Field | Suggested input | Why it matters |

|---|---|---|

Current monthly expenses | Actual 3-month average | Determines your future income need |

Inflation rate | 6.5-7% (metro), 6% (others) | Adjusts for cost of living growth |

Pre-retirement return | 10-12% | Sets your corpus growth expectation |

Post-retirement return | 7-8% | Determines withdrawal sustainability |

Life expectancy | 85-90 years | Prevents corpus from running out |

Always set your life expectancy to at least 85. Underestimating this number is how people run out of money before they run out of life.

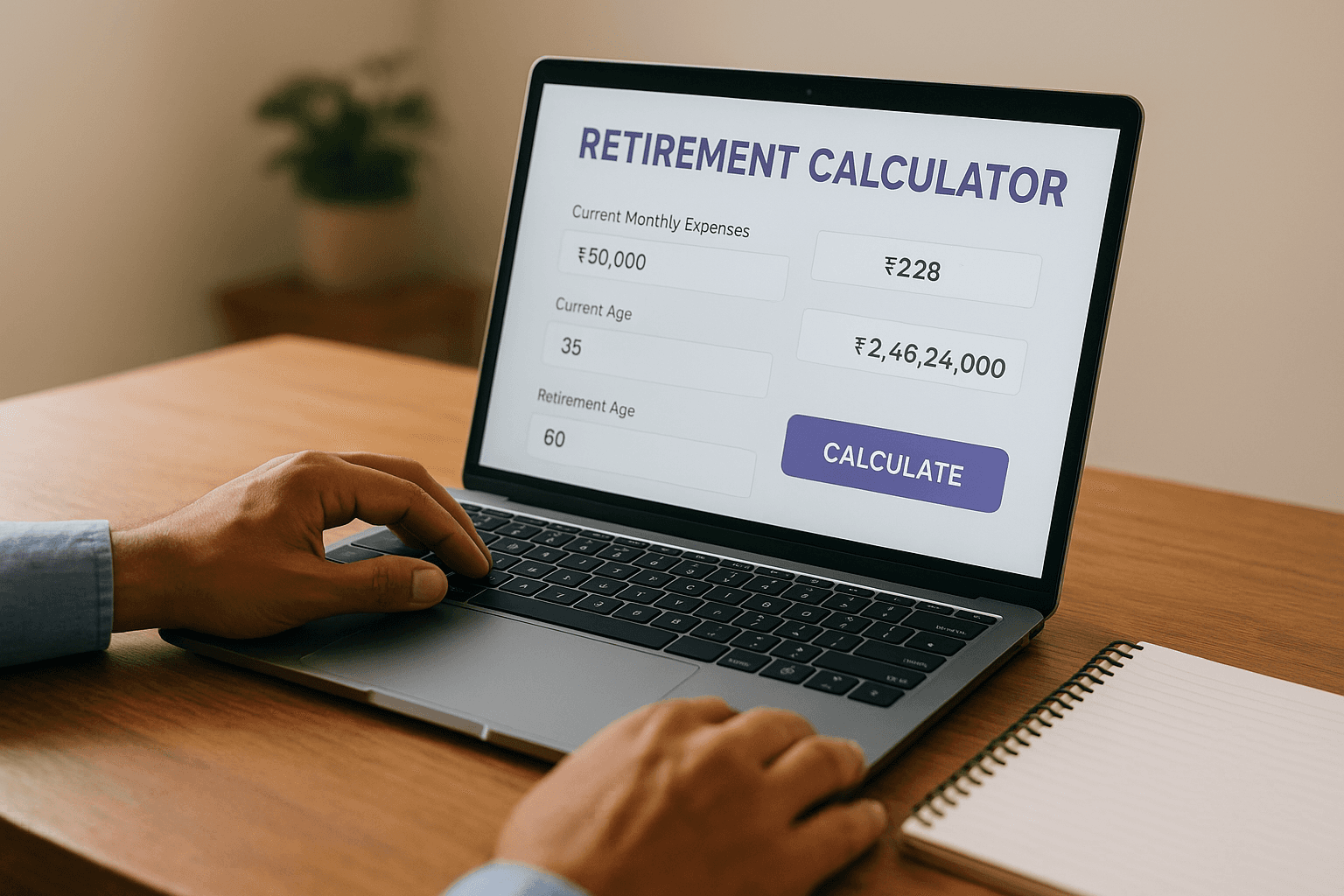

Read the output correctly

Once you hit calculate, the et money retirement calculator shows you two critical numbers: the total corpus you need at retirement and the monthly investment required to build that corpus from today. Focus on both figures, not just the corpus total. The monthly investment number tells you whether your current savings rate is on track or needs a serious adjustment. If the monthly figure looks out of reach, shift your retirement age by two to three years and recalculate. A small timeline change produces a meaningful reduction in your required monthly contribution.

Step 3. Convert your corpus into a monthly investment plan

The monthly investment figure the ET Money retirement calculator gives you is a target, not a prescription. Your job in this step is to take that number and distribute it across actual investment instruments that match your timeline, risk tolerance, and tax situation. A corpus estimate without an allocation plan is just a number sitting on a screen.

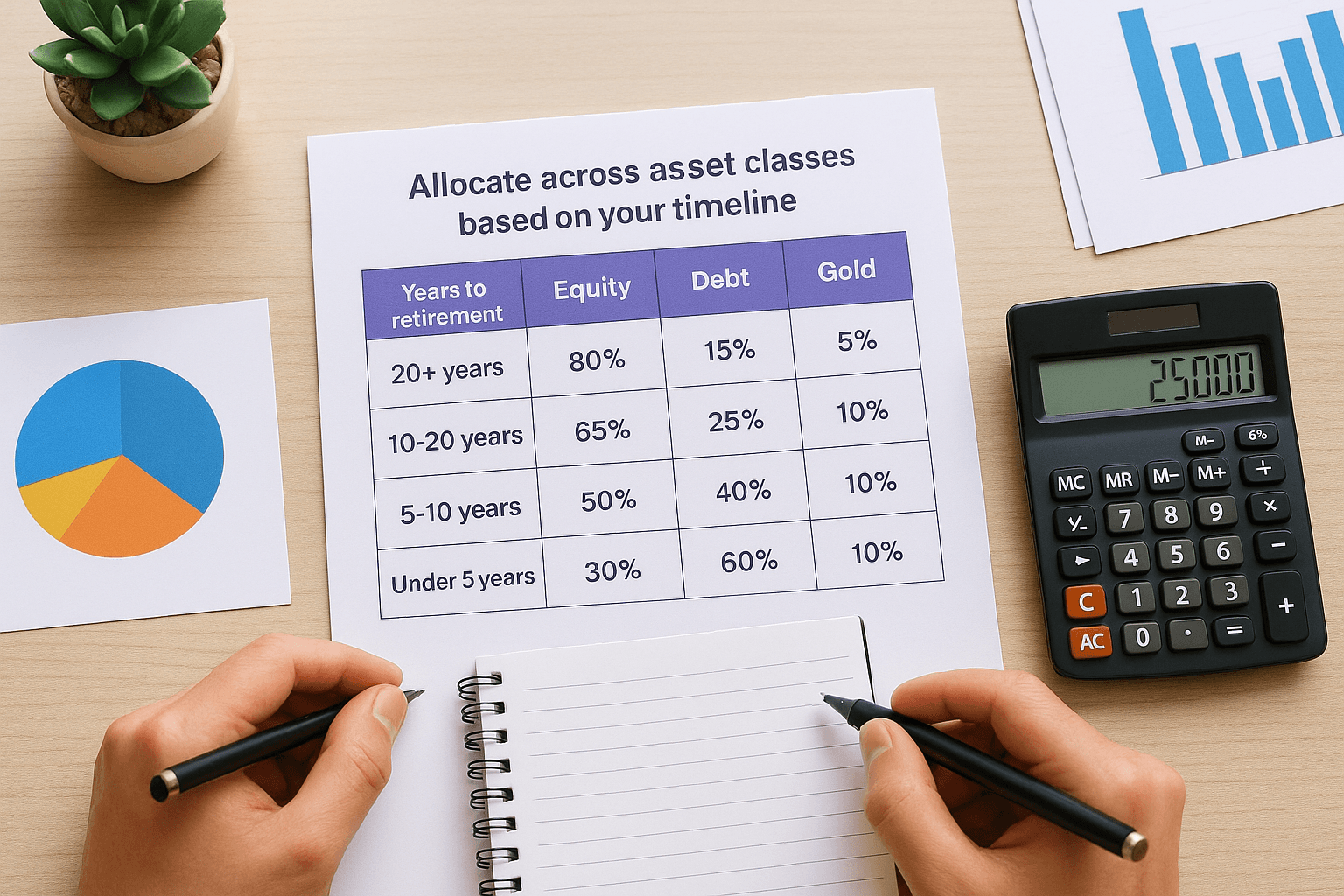

Map your corpus to actual investment vehicles

Once you know your required monthly investment amount, split it across instruments based on your years to retirement. Use the table below as a starting framework. Adjust the percentages based on your own risk profile, but keep equity exposure high if you have more than 15 years until retirement, because that time horizon is what turns compounding into a meaningful wealth-building tool.

Years to retirement | Equity (mutual funds/NPS) | Debt (PPF/EPF/bonds) | Gold/other |

|---|---|---|---|

20+ years | 80% | 15% | 5% |

10-20 years | 65% | 25% | 10% |

5-10 years | 50% | 40% | 10% |

Under 5 years | 30% | 60% | 10% |

The closer you are to retirement, the more your portfolio should protect capital rather than chase growth.

Allocate across asset classes based on your timeline

If your required monthly investment is, say, ₹25,000 and you have 22 years to retirement, you would direct roughly ₹20,000 into equity mutual funds through SIPs, ₹3,750 into debt instruments like PPF or EPF top-ups, and ₹1,250 into a gold fund. This concrete split stops you from treating the calculator output as a lump-sum target and helps you build a disciplined, month-by-month habit instead.

Revisit this allocation every two to three years or after a major income change. Your salary will grow, your expenses will shift, and your retirement timeline will shorten, all of which change the optimal split between growth and protection.

Step 4. Stress-test the result and avoid common mistakes

A single scenario from the et money retirement calculator gives you one possible future, but your actual retirement will depend on conditions that shift over decades. Before you commit to a monthly SIP amount, run at least two alternative scenarios using different return rate assumptions to see how sensitive your corpus estimate is to market conditions. This takes less than five minutes and prevents you from building a plan on overly optimistic assumptions.

Never treat the calculator's first output as final. One pessimistic scenario can reveal a funding gap that changes your entire strategy.

Run two alternative scenarios

Take your base scenario output and create two variants: one where your pre-retirement return drops to 8% (a prolonged flat market) and one where inflation runs at 8% instead of 6%. Enter each set of numbers separately and note the difference in the required monthly investment. If the gap between your optimistic and pessimistic scenarios is more than ₹5,000-₹8,000 per month, your base plan carries meaningful risk and deserves a higher base contribution or an earlier start.

Scenario | Pre-retirement return | Inflation | Impact on monthly SIP |

|---|---|---|---|

Base (optimistic) | 12% | 6% | Lowest monthly requirement |

Moderate | 10% | 6.5% | 10-15% higher monthly need |

Conservative | 8% | 8% | 25-35% higher monthly need |

Three mistakes that skew your corpus estimate

Most people undermine a solid calculator output by making the same avoidable errors. Check your inputs against this list before finalizing anything.

Using current income instead of current expenses: The calculator needs your spending, not what you earn. Your income is irrelevant to your future withdrawal requirement.

Ignoring existing assets: If you already have ₹10 lakh in EPF or mutual funds, subtract its projected future value from your corpus target before calculating your fresh SIP amount.

Forgetting healthcare inflation: Medical costs in India rise faster than general inflation. Add ₹3,000-₹5,000 per month to your current expenses as a healthcare buffer before entering the expense figure.

Next steps

You now have a complete process for using the et money retirement calculator, from gathering accurate inputs to stress-testing your results against realistic market conditions. The calculator does its job well: it gives you a corpus target and a monthly investment figure to aim for. What it cannot do is build you a personalized portfolio, flag when your allocation drifts, or adjust your strategy as your income and life circumstances change.

That next layer of work is where most retirement plans either succeed or stall. Picking the right funds, deciding how much to hold in NPS versus direct mutual funds, and knowing when to shift from equity to debt all require judgment that a calculator cannot provide. If you want that kind of ongoing, conflict-free guidance backed by a SEBI-registered advisor, start your retirement planning with Invsify and get AI-powered recommendations built around your actual financial situation, not generic defaults.