Financial Literacy Explained: Meaning, Basics, And Benefits

Shlok Sobti

Financial Literacy Explained: Meaning, Basics, And Benefits

Most Indians learn how to earn money long before they learn how to manage it. Schools don't teach it, colleges skip over it, and by the time you're drawing a salary, you're expected to figure out taxes, mutual funds, and insurance on your own. That gap between earning and understanding is exactly what financial literacy explained in simple terms can bridge. It's not a skill reserved for chartered accountants or stock traders, it's a basic life skill that every salaried individual in India needs.

Without financial literacy, even a high income can lead to poor outcomes, unnecessary debt, missed tax-saving opportunities, and investments that quietly eat into your returns through hidden commissions. With it, you gain the ability to make confident, informed decisions about where your money goes and how it grows. That's a shift from guessing to knowing, and it changes everything about your financial future.

This article breaks down what financial literacy actually means, walks through its core components, budgeting, saving, investing, debt management, and explains why it matters more now than ever. Whether you're just starting your career or looking to optimize an existing portfolio, understanding these basics is the first step. And if you want to go beyond the basics, that's where a platform like Invsify comes in, offering AI-powered, conflict-free investment advice as a SEBI Registered Investment Advisor, designed to turn financial literacy into real financial action.

What financial literacy means in real life

Financial literacy, at its core, is the ability to understand and use financial concepts to make informed decisions about your money. That includes knowing how interest works, understanding the difference between a mutual fund and a fixed deposit, reading your payslip without confusion, and spotting when a financial product charges you more than it should. When financial literacy explained in textbooks sounds abstract, what it actually looks like in your daily life is far more practical: it's the difference between reacting to your finances and actively managing them with purpose.

It's not about knowing everything

One of the biggest misconceptions people carry is that you need to become a financial expert before you can make good money decisions. You don't. Financial literacy is not about memorizing tax codes or tracking every stock on the Nifty 50. It's about building enough knowledge in a few core areas so that you can ask the right questions, evaluate the options in front of you, and avoid the most common and costly mistakes.

Most financial mistakes don't come from ignorance of complex instruments. They come from a poor grasp of basic concepts like compounding, inflation, and the real cost of debt.

A person who understands how compound interest works against them inside a credit card balance and in their favor inside an equity mutual fund already has more practical financial knowledge than someone who blindly follows stock tips without understanding the underlying logic.

What financial literacy looks like day to day

Financially literate people don't necessarily earn more. They just tend to do a few specific things consistently and deliberately. They know where their money goes each month, not just roughly, but in enough detail to identify where it leaks. They separate spending into categories, track savings progress against clear goals, and set timelines that are tied to real numbers rather than vague intentions.

Such people also avoid making financial decisions based on social pressure or hearsay. Instead of buying an insurance policy because a colleague recommended it, or chasing last year's top-performing fund, they evaluate what a product actually costs, what it covers, and whether it fits their specific situation. That single habit alone can save lakhs over a career.

The gap between income and wealth

This is where financial literacy matters most for Indian salaried professionals. Many high earners in India accumulate surprisingly little real wealth over a 20 to 30-year career. A large salary does not automatically create a large net worth. What builds wealth is the consistent, informed application of financial principles: investing early, avoiding unnecessary debt, minimizing hidden fees, and protecting what you build along the way.

Without financial literacy, a 30% salary increment can disappear into lifestyle inflation within a year. With it, you redirect that same increment toward long-term goals like a home purchase, a retirement corpus, or your child's higher education in a way that actually compounds over time. That's the real-world difference financial literacy creates, not theory on a page, but measurable outcomes in your account.

Why financial literacy matters for Indian households

India's financial ecosystem has changed dramatically in the last decade. UPI payments, direct mutual fund platforms, and digital insurance have all made financial products more accessible than ever before. But accessibility without understanding is a trap. You can now invest in equities, take a personal loan, or buy a ULIP entirely through your phone in under ten minutes, and do it completely wrong, costing yourself significant money in the process. The speed of modern finance has outpaced the average Indian's financial education by a wide margin.

The India-specific gap in financial education

No standard school curriculum in India covers personal finance in any meaningful way. Students graduate without understanding how income tax slabs work, what a credit score measures, or why an expense ratio matters inside a mutual fund. That gap does not close automatically when you enter the workforce. Most salaried professionals piece together financial knowledge from colleagues, social media groups, or whichever bank relationship manager calls them first, and none of those are reliable sources of unbiased guidance.

When your primary source of financial guidance is a product distributor who earns a commission on what you buy, you are not getting advice, you are getting a sales pitch.

This is precisely why financial literacy explained clearly and practically becomes so valuable for every Indian household. It gives you the ability to evaluate advice rather than simply follow it, which is a fundamentally different and far more empowering relationship with your own money.

What's at stake for your household

The financial decisions you make in your 20s and 30s compound for decades. Choosing a regular plan mutual fund over a direct plan, for example, can cost you several lakhs in excess commissions over a 15-year investment horizon. Buying an endowment policy instead of a term plan combined with a mutual fund is another common and expensive mistake that financially literate individuals consistently avoid.

Indian households also carry specific risks that make financial knowledge far more urgent. Joint family financial obligations, dependent parents without pensions, and the near-absence of a reliable social security net mean that your personal financial decisions affect more people than just yourself. A single poorly structured investment or an uninsured medical emergency can destabilize an entire household. Building a solid financial foundation is not a personal luxury in this context. It is a shared responsibility.

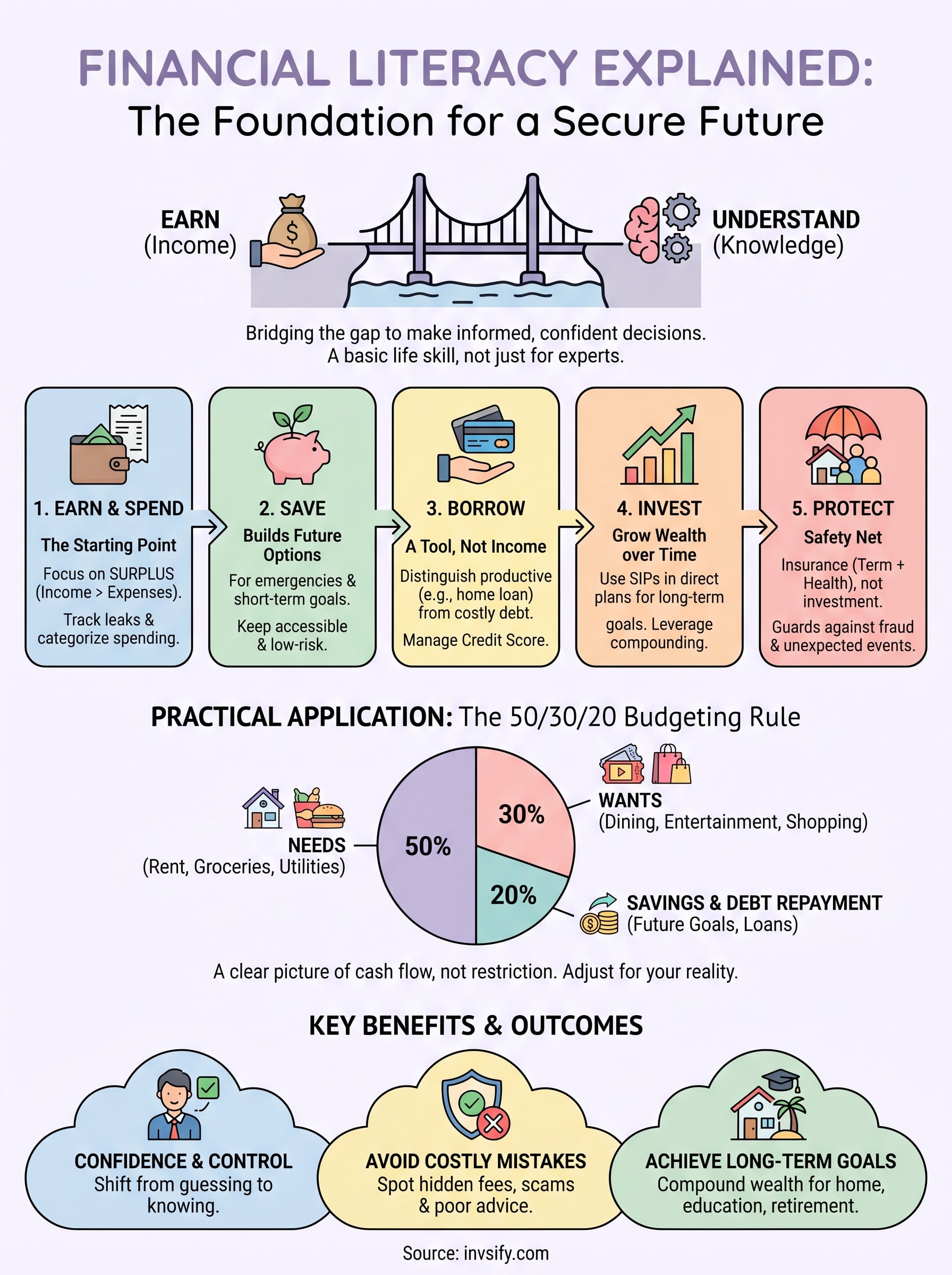

The basics: earn, spend, save, borrow, protect

Every framework for financial literacy explained in a useful way comes back to five core actions: earning, spending, saving, borrowing, and protecting. These are not sequential steps you complete once. They are ongoing activities that interact with each other every month throughout your financial life. Understanding how each one works, and how they connect, gives you a complete picture of where your money stands at any point in time.

Earn and spend: the foundation

Your income is the starting point for everything. How much you earn sets the ceiling on what is possible, but it does not determine your financial outcomes on its own. What matters is the gap between what you earn and what you spend, commonly called your surplus. A person earning ₹60,000 per month who spends ₹45,000 is in a stronger financial position than someone earning ₹1,20,000 who spends ₹1,15,000. Income creates potential. Spending decisions determine whether that potential becomes real wealth or quietly disappears.

Unexamined spending is where most households lose the most ground. Small recurring costs, unused subscriptions, and impulse purchases add up to surprisingly large amounts over a year. Most people who track their monthly expenses in detail for the first time are genuinely shocked by what they find.

The gap between your income and your expenses is the single number that determines how fast your financial life moves forward.

Save and borrow: two sides of the same picture

Saving is what converts your surplus into future options. When you save consistently, you build the ability to handle emergencies without taking on high-cost debt, invest toward long-term goals, and make large purchases without disrupting your monthly cash flow. Borrowing does the opposite: it pulls future income into the present. Used with intention, like a home loan at a reasonable interest rate, borrowing is a tool. Used carelessly, like rolling over a credit card balance every month, it is one of the fastest ways to erode your net worth.

Protect: the step most people skip

Protection means insurance coverage, not an investment product. Many salaried Indians hold endowment policies or ULIPs that attempt to combine coverage with returns and deliver neither particularly well. A straightforward term insurance plan paired with a comprehensive health cover gives your household a financial safety net that allows every other part of your plan to keep working even when something unexpected happens.

Skipping protection is a risk that can undo years of disciplined saving and investing in a single event. Building income, controlling spending, saving consistently, and borrowing responsibly all become fragile without the right coverage in place.

How to build a simple budget that works

A budget is not a restriction on your life. It is a clear picture of where your money goes so you can direct it where you actually want it to go. Many people avoid budgeting because they associate it with spreadsheets and rigid tracking, but a functional budget can be far simpler than that. The goal is not perfection; the goal is enough visibility into your cash flow to make deliberate choices rather than reactive ones. This is one of the most practical applications of financial literacy explained in action.

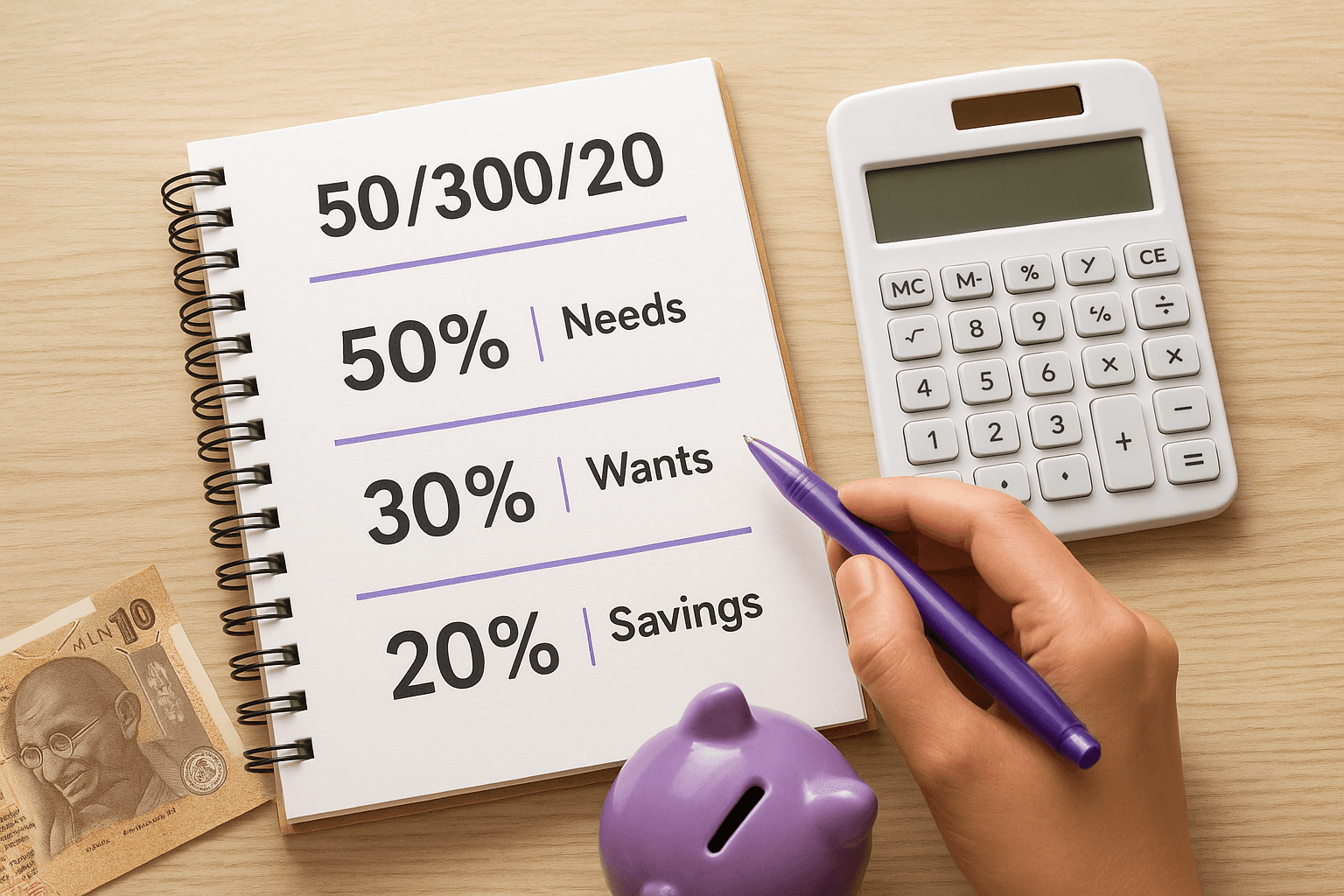

The 50/30/20 rule as a starting point

The 50/30/20 rule is one of the most widely used frameworks for personal budgeting. It divides your take-home income into three broad categories: 50% toward needs, 30% toward wants, and 20% toward savings and debt repayment. For a salaried professional in India, needs typically include rent, groceries, utilities, transport, and insurance premiums. Wants cover dining out, entertainment, subscriptions, and discretionary shopping. The 20% directed toward savings and goals is the portion that actually builds your future.

You don't need to follow this split precisely to benefit from it. The real value of this framework is that it forces you to categorize your spending and immediately shows you where an imbalance exists. If your needs consume 70% of your income, that signals a structural problem worth addressing, whether through reducing fixed costs, increasing income, or both.

A budget only works when it reflects your real numbers, not the numbers you wish were true.

Tracking your actual spending

Most people overestimate their savings rate and underestimate how much they spend on wants. Tracking your actual spending for one full month, before building any formal budget, gives you a far more honest baseline than estimating from memory. You can do this with a simple notes app, a spreadsheet, or a personal finance app. The tool matters far less than the consistency of recording every transaction during that period.

Once you have a month of real data, patterns become obvious. You'll likely find two or three categories where spending runs higher than expected. Fixing just those areas can free up a meaningful surplus each month, money that can then flow toward savings, investments, or reducing high-interest debt instead of disappearing without trace.

How to handle debt and credit responsibly

Debt is one of the most misunderstood parts of personal finance. Most people either avoid it out of fear or use it without understanding what it costs over time. Financial literacy explained in practical terms treats debt as a tool: useful in specific situations, dangerous when misapplied. Your ability to borrow responsibly and manage credit well directly shapes your net worth, your financial flexibility, and your capacity to qualify for lower rates when you genuinely need them.

Understanding the real cost of debt

Every loan carries a price beyond the principal you borrow. The interest rate, processing fees, and prepayment charges all combine to form the true cost of borrowing, and knowing that number before you sign is essential. A personal loan at 18% per annum costs far more than it appears once you account for compounding over a three-year repayment term. Always calculate the total amount you will repay, not just the monthly installment figure.

Borrowing without calculating the total repayment amount is one of the most common and preventable financial mistakes salaried professionals make.

Not all debt is equal. A home loan at 8.5% per annum that funds an appreciating asset is fundamentally different from a credit card rollover at 36% per annum that covers discretionary spending. Separating productive debt from costly debt helps you decide which balances to clear first and which borrowing decisions actually make sense for your specific situation. Prioritizing high-interest debt for repayment is almost always the right move.

How to manage your credit score

Your credit score tells lenders how reliably you repay what you borrow. In India, most lenders check your CIBIL score, which ranges from 300 to 900. A score above 750 typically earns you better interest rates and faster approvals. Three behaviors drive this number more than anything else: paying bills on time, keeping your credit utilization below 30% of your available limit, and avoiding multiple loan applications within a short period.

Paying your credit card balance in full each month is the most effective single habit for both protecting your score and eliminating expensive interest charges. If you carry a balance, even a small one, interest compounds daily on most cards in India, turning a modest shortfall into a significant liability within a few billing cycles. Treat your credit card as a payment tool, not as a substitute for income you have not yet earned.

How to start saving and investing for goals

Saving and investing are not the same thing, and treating them as interchangeable is one of the most common gaps in financial literacy explained across the board. Saving is setting money aside in a low-risk, easily accessible account for short-term needs and emergencies. Investing is putting money to work in assets that carry some level of risk but offer the potential for higher returns over a longer horizon. Knowing which one fits which goal is where this section begins.

Start with a goal, not a product

Before you open any investment account, define what you are investing for and when you will need the money. A goal without a timeline is just a wish. When you attach a specific number and a specific date, the math tells you exactly how much you need to invest each month to reach it. A 10-year goal for your child's undergraduate education in India looks very different from a 2-year goal to build a home down payment, and the right product for each is different as a result.

Choosing an investment product before you have a clear goal is like buying fuel without knowing where you're driving.

Short-term goals, typically under three years, generally call for safer instruments like liquid funds, recurring deposits, or short-duration debt funds that protect your principal while still offering modest growth. Long-term goals, those five years away or further, give you enough time to absorb market fluctuations and benefit from equity investments, where compounding genuinely builds significant wealth over time.

How to invest consistently over time

Consistency matters more than timing in long-term investing. A Systematic Investment Plan (SIP) in a direct plan mutual fund lets you invest a fixed amount every month without needing to monitor the market or pick the right entry point. Over a 10 to 15 year period, SIPs through direct plans can deliver substantially better outcomes than regular plans because they eliminate the distributor commission layer that quietly reduces your compounding base every year.

Your investment choices should also match your actual risk tolerance, not the risk tolerance you imagine you have when markets are calm. Build your portfolio around equity for long-term growth, debt for stability, and a liquid emergency fund that sits entirely outside your investment accounts. Keeping these three buckets separate prevents a medical expense or a job disruption from forcing you to sell long-term investments at the wrong moment.

How to protect your money and avoid scams

Protecting your money is one of the most underrated aspects of financial literacy explained in any practical guide. Most people focus on growing wealth and overlook the very real risk of losing it to fraud, misinformation, or poorly regulated financial products. India's financial sector has seen a sharp rise in investment scams, phishing attacks, and unauthorized advisors over the last five years, and the damage they cause is often permanent. Building defensive habits costs you nothing and protects everything you have worked to build.

Spot the warning signs before you invest

Scams targeting Indian investors tend to follow recognizable patterns. Any opportunity that promises guaranteed high returns with no risk is a warning sign regardless of how professional the pitch sounds. Legitimate investments carry risk, and any advisor or platform that claims otherwise is either uninformed or dishonest. Similarly, pressure to invest quickly, requests for your Aadhaar, PAN, or bank login credentials upfront, and offers that arrive through WhatsApp groups or unverified social media accounts are all red flags worth taking seriously.

If someone cannot show you a SEBI registration number when offering investment advice, stop the conversation immediately.

Verifying an advisor's credentials takes under two minutes. SEBI maintains a public registry of registered investment advisors on its official website, and checking that list before acting on any advice is one of the most direct protective steps available to you.

Protect your accounts and personal data

Strong account security is a part of financial self-defense that most people treat too casually. Never reuse the same password across your banking, investment, and email accounts, because a breach in one creates vulnerability in all of them. Enable two-factor authentication on every financial platform you use, including your mutual fund accounts, demat account, and net banking portal.

Phishing attacks in India increasingly arrive disguised as messages from major banks or regulatory bodies. These messages create urgency, asking you to verify your KYC or unfreeze your account through a link that captures your credentials. Your actual bank will never ask you to click a link and enter your full login details or OTP in one step. When a message pushes you to act immediately, treat that pressure itself as the signal to stop and verify through the bank's official app or registered helpline number directly.

Where to go from here

Financial literacy explained across this guide comes down to one core idea: the more clearly you understand how money moves, the better your decisions become. You now have a working framework covering budgeting, debt management, saving, investing, and protecting your wealth from fraud and poor advice. That foundation is worth more than any single tip you will find on a financial forum or in a WhatsApp group.

Knowing the principles is step one. Putting them into practice consistently, with reliable guidance behind you, is where most people need support. A SEBI Registered Investment Advisor removes the conflict of interest that comes with commission-based advice, so the recommendations you receive are built around your goals, not someone else's sales target. If you want AI-powered, transparent advice that turns what you have learned here into a real financial plan, start your wealth journey with Invsify and take the next step with confidence.