Financial Literacy For Beginners: A Complete Starter Guide

Shlok Sobti

Financial Literacy For Beginners: A Complete Starter Guide

Most Indians learn about money the hard way, through mistakes, missed opportunities, and advice from well-meaning relatives who may not have the full picture. Financial literacy for beginners isn't taught in schools, yet it determines everything from your daily spending habits to your long-term wealth accumulation.

The good news? You don't need a finance degree or hours scrolling through unreliable forums to get started. Understanding how to budget, save, manage debt, and invest can be broken down into clear, actionable steps that anyone can follow. What matters most is having access to trustworthy, conflict-free guidance that actually puts your interests first.

This guide walks you through the essential building blocks of personal finance, from creating your first budget to understanding how investments actually work. At Invsify, we believe smart financial decisions start with solid foundational knowledge. As a SEBI Registered Investment Advisor offering AI-powered financial guidance, we've built this starter guide to give you the confidence and clarity you need to take control of your money, minus the jargon and hidden agendas that typically come with financial advice.

What financial literacy covers for beginners

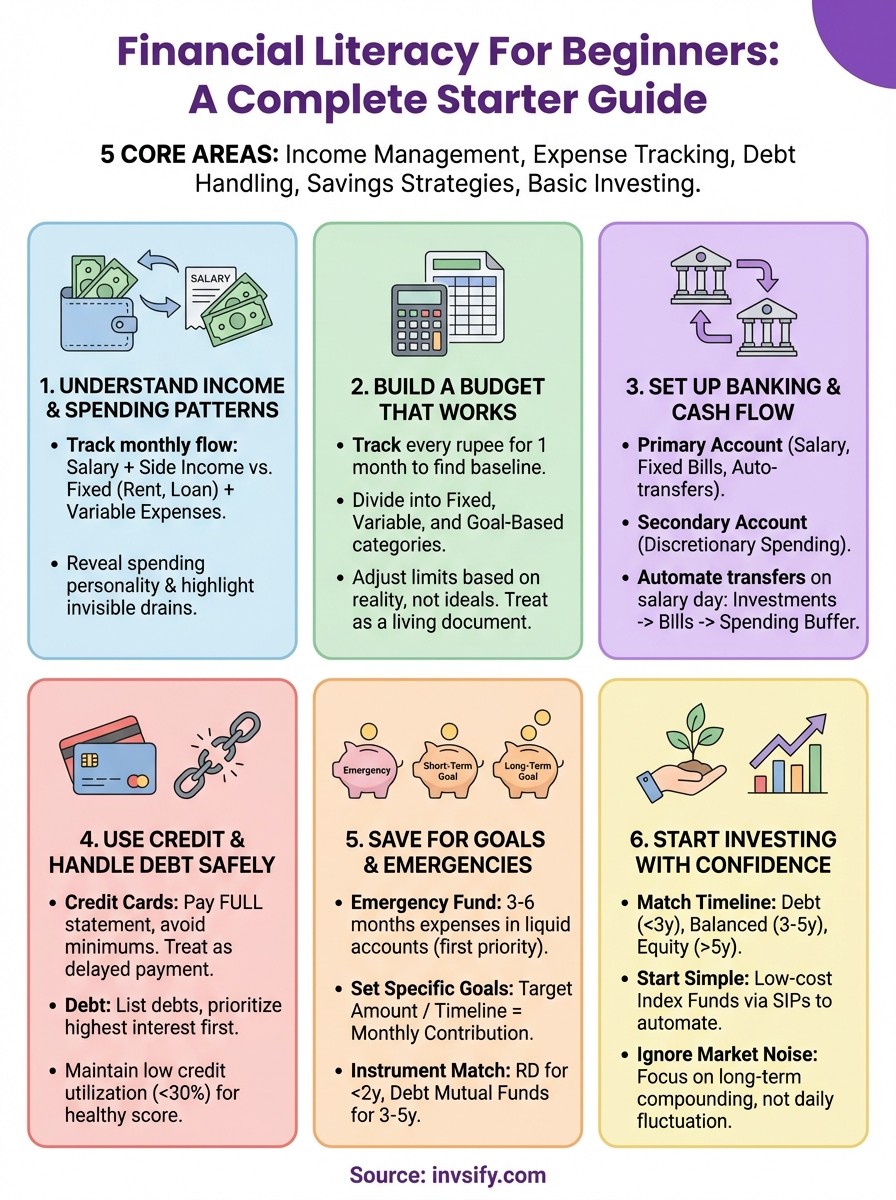

Financial literacy for beginners starts with understanding where your money comes from, where it goes, and how to make it work harder for you. The concept covers five core areas: income management, expense tracking, debt handling, savings strategies, and basic investing. You don't need to master everything at once, but knowing what falls under each category helps you build a complete financial foundation rather than patching together random advice from different sources.

Think of financial literacy as your personal money operating system. Just as you learned to use a smartphone by understanding its basic functions first, you build financial confidence by grasping fundamental concepts before moving to advanced strategies. The goal isn't to become a financial expert overnight but to develop enough practical knowledge to make informed decisions about your earnings, expenses, and future planning without depending solely on others who may have conflicts of interest.

Understanding income and spending patterns

Your financial journey begins with knowing exactly how much money flows in and out each month. This includes your salary, any side income, bonuses, and gifts coming in, balanced against your fixed expenses like rent, utilities, and loan payments, plus variable costs like groceries, entertainment, and transportation. Most beginners skip this step and wonder why their bank balance never grows despite earning well.

Tracking these patterns reveals your spending personality and highlights where money disappears without you noticing. You might discover that small daily expenses add up to thousands monthly, or that you're spending disproportionately on categories that don't align with your actual priorities. This awareness forms the backbone of every other financial decision you'll make.

Building knowledge about financial products

Banks, NBFCs, and insurance companies offer dozens of products, but beginners need to understand only a handful initially. Savings accounts, fixed deposits, recurring deposits, and liquid funds form your basic toolkit for parking money safely. Each serves different purposes: savings accounts for daily transactions, FDs for guaranteed returns, RDs for disciplined monthly savings, and liquid funds for slightly better returns than savings accounts while maintaining easy access.

Credit cards and personal loans fall into another category entirely, one that requires careful handling. Understanding how interest compounds, what credit scores measure, and why minimum payments trap you in debt cycles saves you from expensive mistakes. Insurance products like term life and health coverage protect against catastrophic financial events, making them essential rather than optional once you start earning regularly.

Your financial literacy grows not from memorizing product features but from understanding which tools solve which specific problems in your life.

Learning risk management and protection

Risk isn't just about stock market crashes or business failures. For most Indians, the bigger risks involve medical emergencies, job loss, death of an earning member, or major home repairs that can drain savings built over years. Financial literacy teaches you to identify your specific vulnerabilities and address them systematically rather than hoping problems won't occur.

Emergency funds act as your first line of defense, covering three to six months of expenses without needing to sell investments or borrow at high interest rates. Insurance provides the second layer, transferring catastrophic risks to companies designed to handle them. Beginners often skip these boring topics and jump straight to investing, only to sell their investments at losses when unexpected expenses hit.

Grasping basic investment principles

Investing feels intimidating because the industry deliberately complicates it with technical terms and performance charts. However, the basics remain simple: you put money into assets that have potential to grow in value over time, accepting some risk in exchange for returns higher than inflation. Equity investments (stocks, mutual funds) offer growth potential but fluctuate in value, while debt investments (bonds, debt funds) provide steadier but lower returns.

Understanding concepts like compounding, diversification, asset allocation, and time horizon matters more than picking the hottest stock or fund. These principles determine whether your money grows substantially over decades or stagnates because you panic-sold during market dips. The difference between someone retiring comfortably and someone working indefinitely often comes down to grasping these fundamentals early and applying them consistently.

Why financial literacy matters in India

India's financial landscape differs dramatically from Western markets, yet most advice available online gets copied from American or European sources without accounting for our unique challenges. You face commission-driven distribution models, complex tax structures, family financial obligations, and rapid digitalization of banking that creates both opportunities and risks. Without solid financial literacy for beginners, you become vulnerable to products sold for the distributor's benefit rather than yours, losing potentially lakhs in hidden costs over your lifetime.

The stakes grow higher when you consider that most Indians lack workplace retirement benefits beyond EPF, making personal wealth building non-negotiable. You can't rely on pension systems or social security nets that exist in developed economies. Your financial decisions today directly determine whether you maintain dignity in retirement or burden your children financially, making knowledge about money management critical rather than optional.

The cost of financial ignorance in Indian markets

Walk into any bank branch or insurance office, and you'll encounter sales personnel trained to push high-commission products regardless of whether they suit your needs. ULIPs disguised as pure investments, endowment policies with pathetic returns, and regular mutual funds with embedded commissions drain your wealth silently. These products aren't necessarily bad, but they're often mis-sold to people who don't understand the fee structures, lock-in periods, or alternative options that would serve them better.

You might think comparing options before buying protects you, but product complexity makes genuine comparison nearly impossible without foundational knowledge. Sales pitches use jargon strategically, making inferior products sound sophisticated while simpler, better alternatives get dismissed as too basic. Financial literacy gives you the vocabulary and framework to ask the right questions and recognize when someone prioritizes their commission over your returns.

Building wealth without generational advantage

Previous generations could achieve financial security through government jobs, fixed deposits offering double-digit returns, and property appreciation in tier-1 cities. Your generation faces different realities: inflation consistently beats FD returns, real estate requires massive capital, and job security disappears across sectors. You need investment strategies that compound wealth faster than inflation while managing risk appropriately for your age and goals.

Financial literacy transforms you from someone reacting to money pressures into someone proactively building the life you want through informed choices.

Understanding concepts like equity allocation, tax-efficient investing, and goal-based planning matters more now than ever because traditional safe options no longer guarantee wealth preservation. The knowledge gap between those who understand modern financial tools and those still parking everything in savings accounts will define economic outcomes for your generation.

How to build a simple budget that works

Budgeting sounds restrictive until you realize it actually gives you permission to spend on things you value while cutting waste from areas that don't matter. Your first budget won't be perfect, and that's expected. The goal is creating a living document that evolves with your income and priorities rather than following some generic 50-30-20 template that doesn't match Indian realities. You need visibility into where money goes currently before you can redirect it toward goals that actually improve your life.

Most budgeting advice fails because it starts with ideal percentages instead of your actual behavior. Financial literacy for beginners teaches you to work with your natural spending patterns first, then gradually optimize rather than forcing yourself into categories that create guilt and abandonment. Think of your budget as a GPS that shows your current location before plotting the best route forward.

Track every rupee for one month first

You cannot budget accurately without knowing your baseline spending patterns. Download your bank statements, credit card bills, and UPI transaction history for the past month. Create a simple spreadsheet with columns for date, description, amount, and category. Go through every transaction and categorize it honestly: groceries, rent, utilities, transportation, entertainment, dining out, shopping, subscriptions, and miscellaneous.

This exercise reveals uncomfortable truths about unconscious spending habits most people prefer to ignore. You might discover that food delivery apps consume more than your grocery budget, or that subscription services you forgot about drain thousands annually. The awareness alone often triggers immediate behavior changes before you even set formal limits.

Divide spending into fixed, variable, and goal categories

Your budget needs three distinct sections that handle different types of money flow. Fixed expenses include rent, loan EMIs, insurance premiums, and subscriptions you can't easily change month-to-month. These typically claim 40-50% of your income and require long-term decisions to reduce. Variable expenses cover groceries, utilities, transportation, and discretionary spending where you have month-to-month control.

Goal-based allocations form the third category, covering emergency fund contributions, investment SIPs, and savings for specific purchases. Many budgets fail by treating savings as whatever remains after spending, which usually means nothing remains. Reverse this by allocating toward goals immediately after receiving income, then budgeting the remainder for expenses.

Your budget succeeds when it prevents regret purchases while funding the life experiences and security you actually want.

Adjust limits based on reality, not ideals

Start with spending limits that reflect your tracked actuals, even if they seem excessive initially. Trying to slash your food budget by 50% overnight creates deprivation that leads to binge spending and budget abandonment. Instead, reduce gradually by 10% monthly in areas where tracking revealed waste. Maybe you cut one food delivery per week or pause a subscription you rarely use.

Review your budget every month and adjust categories based on what actually happened versus what you planned. Life changes constantly, bringing unexpected medical costs, vehicle repairs, or family obligations that rigid budgets can't accommodate. Building flexibility through a miscellaneous buffer and treating your budget as guidance rather than law makes the whole system sustainable long-term.

How to set up banking and cash flow

Your banking setup determines whether money management feels chaotic or controlled. Most Indians open a savings account because their employer requires it, then let everything pile into that single account without structure. This creates confusion when trying to separate daily spending money from emergency funds or investment capital. Setting up a deliberate banking architecture and cash flow system forms the backbone of financial literacy for beginners, giving you clarity about what money serves which purpose at any given time.

You need visibility into money movement from the moment your salary hits your account until you spend or invest it. Poor cash flow management causes people with good incomes to feel perpetually broke because they can't see where funds went or what remains available for discretionary spending. The right setup prevents this by creating clear boundaries between different money buckets.

Choosing the right bank accounts

Start with a primary savings account that receives your salary and handles all automated payments for fixed expenses like rent, loan EMIs, and insurance premiums. Choose a bank with a good mobile app interface, widespread ATM network, and no hidden charges for basic transactions. Zero-balance accounts from digital banks work well if you maintain minimal balances, while traditional banks suit those who prefer branch access for complex transactions.

Add a secondary savings account or digital wallet for discretionary spending on entertainment, dining, and shopping. Transfer your budgeted amount for variable expenses here monthly, making it impossible to accidentally spend money earmarked for bills or investments. This psychological separation works better than willpower alone because you see real limits rather than your total balance.

Organizing money flow systematically

Create a specific sequence for handling incoming salary. First, automate transfers to your investment accounts and emergency fund on salary day itself, removing that money from sight before spending temptations arise. Second, pay all fixed expenses through standing instructions or autopay. Third, move your discretionary budget to the spending account. Whatever remains becomes your buffer for irregular expenses like vehicle maintenance or medical costs.

Your cash flow system succeeds when you never wonder whether you can afford something because each rupee already has an assigned job.

This framework prevents the common problem of reaching month-end with no money for SIPs because you spent freely early in the month. You make savings automatic rather than dependent on leftover funds that rarely materialize.

Automating payments and transfers

Set up standing instructions for every predictable monthly outflow including mutual fund SIPs, insurance premiums, utility bills, and loan EMIs. Most banks allow you to schedule transfers between your own accounts too, making the salary-day allocation process completely hands-off. Automation removes decision fatigue and ensures you never miss important payments that affect your credit score or investment discipline.

Review your automated transactions quarterly to cancel subscriptions you stopped using and adjust SIP amounts when income increases. The goal is making your banking system work in the background while you focus on earning more and spending wisely within the boundaries you've established.

How to use credit and handle debt safely

Credit cards and loans amplify your purchasing power but destroy your wealth when misused. Most Indians treat credit cards as extra income rather than borrowed money requiring full repayment, leading to debt spirals that take years to escape. Understanding how credit actually works, what behaviors damage your financial health, and how to extract benefits without falling into traps forms a critical part of financial literacy for beginners. The difference between someone who uses credit strategically and someone drowning in high-interest debt often comes down to knowing a few fundamental rules.

Your relationship with credit determines whether you build wealth through leverage or spend decades paying interest that funds someone else's retirement. You need clear frameworks for when borrowing makes sense, how to prioritize repayment, and what credit behaviors protect versus damage your long-term financial standing.

Understanding credit cards and their traps

Credit cards offer convenience, reward points, and purchase protection, but come with interest rates between 36-42% annually if you carry balances forward. You should treat your credit card as a delayed payment method rather than a loan facility. Charge only what you can pay completely when the bill arrives, avoiding the minimum payment trap that keeps you in debt indefinitely while interest compounds.

The minimum payment option exists to profit the bank, not help you. Paying only 5% monthly on a ₹50,000 balance takes over 10 years to clear while you pay ₹70,000+ in interest alone. Instead, configure autopay for the full statement amount so you never accidentally carry balances. Use credit cards strategically for their benefits like cashback or reward points on planned purchases, not as permission to buy things you cannot afford immediately.

Managing existing debt strategically

List all your current debts with their interest rates, outstanding amounts, and minimum payments. Personal loans typically charge 10-18%, credit cards 36-42%, and education loans 8-12%. You cannot treat all debt equally when rates vary this dramatically. Focus on eliminating the highest-interest obligations first while maintaining minimum payments on others, a method that saves you the most money over time.

Your debt repayment strategy succeeds when you attack high-interest balances aggressively while protecting your credit score through timely minimum payments everywhere else.

Avoid taking new debt to pay existing debt unless you're consolidating high-interest obligations into significantly lower rates. Balance transfer offers on credit cards sometimes provide 0% interest for 6-12 months, giving you breathing room to pay down principal faster, but only work if you commit to clearing the balance before promotional rates expire.

Building healthy credit behavior

Your credit score between 300-900 determines your ability to access loans at favorable rates for major purchases like homes or vehicles. Payment history contributes 30% of your score, making on-time payments non-negotiable. Set reminders or automate payments to never miss due dates, as even one 30-day delay drops your score significantly and stays on your record for years.

Maintain credit utilization below 30% of your total limit across all cards. If your combined credit limit is ₹2 lakhs, keep outstanding balances under ₹60,000 at any time. High utilization signals financial stress to lenders even if you pay on time. Request limit increases periodically or add new cards to expand available credit, making the same spending appear as lower utilization percentage.

How to save for goals and emergencies

Saving without clear targets leads to weak commitment and frequent dipping into your accumulated funds for random purchases. You need a structured approach that separates money meant for emergencies from funds earmarked for specific goals like a vehicle, home down payment, or wedding. The difference between people who achieve their financial objectives and those who perpetually struggle comes down to treating savings as mandatory allocations rather than whatever remains after spending. Financial literacy for beginners emphasizes this distinction because it prevents the common pattern of saving diligently for months, then draining everything when an unplanned expense appears.

Your savings strategy requires multiple buckets working simultaneously toward different purposes. Emergency funds protect against immediate crises, short-term goal savings fund purchases within one to three years, and long-term goal savings prepare you for objectives further out. Mixing these together creates confusion about what you can actually afford to spend and what needs protection.

Building your emergency fund first

You need three to six months of essential expenses set aside in highly liquid accounts before focusing heavily on other goals. Calculate your absolute minimum monthly costs including rent, utilities, groceries, loan EMIs, and insurance premiums, then multiply by the number of months you want covered. This fund exists solely for genuine emergencies like job loss, medical crises, or major home repairs, not for sales or vacation opportunities.

Park your emergency money in savings accounts or liquid funds where you can access it within 24-48 hours without penalties or market risk. High-interest savings accounts from digital banks currently offer 6-7% returns, while liquid funds provide slightly better returns with minimal volatility. Never invest emergency funds in equity or lock them in fixed deposits with premature withdrawal penalties.

Your emergency fund succeeds when it prevents you from selling investments at losses or taking high-interest loans during unexpected crises.

Setting specific financial goals

Write down exactly what you're saving toward, the target amount needed, and your timeline for each goal. Vague intentions like "save more money" fail because you have no way to measure progress or adjust contributions. Specific targets like "₹3 lakhs for vehicle down payment in 18 months" or "₹50,000 for laptop in 8 months" create clarity and motivation.

Divide each goal amount by the months available to determine your required monthly contribution. A ₹3 lakh goal over 18 months needs approximately ₹16,700 monthly contributions assuming minimal returns. Compare this requirement against your income and existing commitments to verify whether the timeline remains realistic or needs adjustment.

Choosing the right savings instruments

Match your savings instrument to your goal timeline and liquidity needs. Recurring deposits work well for goals under two years because they enforce monthly discipline and provide guaranteed returns around 6-7%. Debt mutual funds suit three to five year goals by offering tax-efficient returns potentially exceeding fixed deposits without equity market volatility.

Keep short-term goal money in liquid funds or ultra short-term debt funds where you maintain flexibility to withdraw when opportunities arise. Goals beyond five years can incorporate equity exposure through balanced funds, but anything needed within three years belongs in stable, predictable instruments regardless of how attractive equity returns appear.

How to start investing with confidence

Investing intimidates beginners because the financial industry profits from complexity, surrounding basic concepts with technical terms that make you feel underqualified. You don't need to predict market movements or analyze company balance sheets to start building wealth through investments. What you need is understanding risk tolerance, time horizons, and disciplined consistency rather than perfect timing or sophisticated strategies. The anxiety around investing often disappears once you realize that successful investors focus on time in the market rather than timing the market, holding investments through volatility instead of reacting to every price movement.

Your first investments should reflect your learning phase where understanding how markets behave matters more than maximizing returns immediately. Starting small allows you to experience market fluctuations without risking money you cannot afford to lose, building confidence through actual participation rather than endless research that delays action. Financial literacy for beginners emphasizes this practical learning approach because reading about investing differs dramatically from watching your own money grow or temporarily decline.

Understanding your investment timeline

You must match investment choices to when you actually need the money back. Goals under three years belong in debt instruments like short-term debt funds or fixed deposits because equity markets fluctuate too much over brief periods. Your emergency fund never goes into equity investments regardless of how attractive returns appear, since you might need access exactly when markets have dropped 20-30%.

Equity investments through mutual funds or direct stocks suit goals beyond five years because longer timeframes let you ride out market cycles and benefit from compounding growth. The seven to ten year horizon allows enough time for temporary losses to recover and for equity's superior long-term returns to materialize. Anything between three to five years typically works best with balanced funds that mix debt and equity, providing moderate growth with less volatility than pure equity exposure.

Starting with simple, low-cost instruments

Begin your investing journey with index funds or diversified equity mutual funds that spread risk across multiple companies instead of betting on individual stocks. Index funds tracking the Nifty 50 or Sensex provide instant diversification at minimal expense ratios, typically 0.1-0.5% annually compared to 1-2% for actively managed funds. Lower costs directly improve your returns because every rupee paid in fees reduces your final corpus.

Systematic Investment Plans (SIPs) automate monthly investments, removing the temptation to time markets or skip contributions when headlines sound scary. Starting with ₹1,000-5,000 monthly builds the investing habit without straining your budget, with flexibility to increase amounts as income grows.

Your confidence in investing grows through consistent participation over years, not from finding the perfect entry point or hottest fund.

Learning to ignore market noise

Markets will drop 10-15% multiple times during your investing lifetime, triggering panic among inexperienced investors who sell at losses. You need mental preparation for volatility before it happens, understanding that temporary declines create opportunities to buy more units cheaply rather than reasons to exit. Daily market movements mean nothing for goals decades away, yet people obsessively check portfolio values and make emotional decisions.

Limit yourself to quarterly reviews of your investments instead of daily tracking. Assess whether your asset allocation still matches your goals and timeline, rebalancing if needed, but resist the urge to abandon solid investment plans because markets had a bad month or headlines predict crashes.

Your next step

Financial literacy for beginners isn't about memorizing terms or becoming an expert overnight. You've learned the core building blocks: budgeting your income, managing cash flow, using credit responsibly, saving strategically, and starting investments with confidence. The difference between reading this guide and actually improving your financial life comes down to taking the first concrete action this week rather than waiting for the perfect moment.

Start with one area where you feel most uncertain or where problems currently exist. Maybe that means tracking expenses for 30 days, opening a separate savings account for your emergency fund, or setting up your first monthly SIP of ₹1,000. Small consistent actions compound into major financial transformation over months and years, while perfect plans that never start produce zero results.

If you want AI-powered guidance tailored to your specific situation without hidden fees or commission-driven advice, explore how Invsify helps beginners build wealth systematically. Your financial future depends on decisions you make today, not someday.