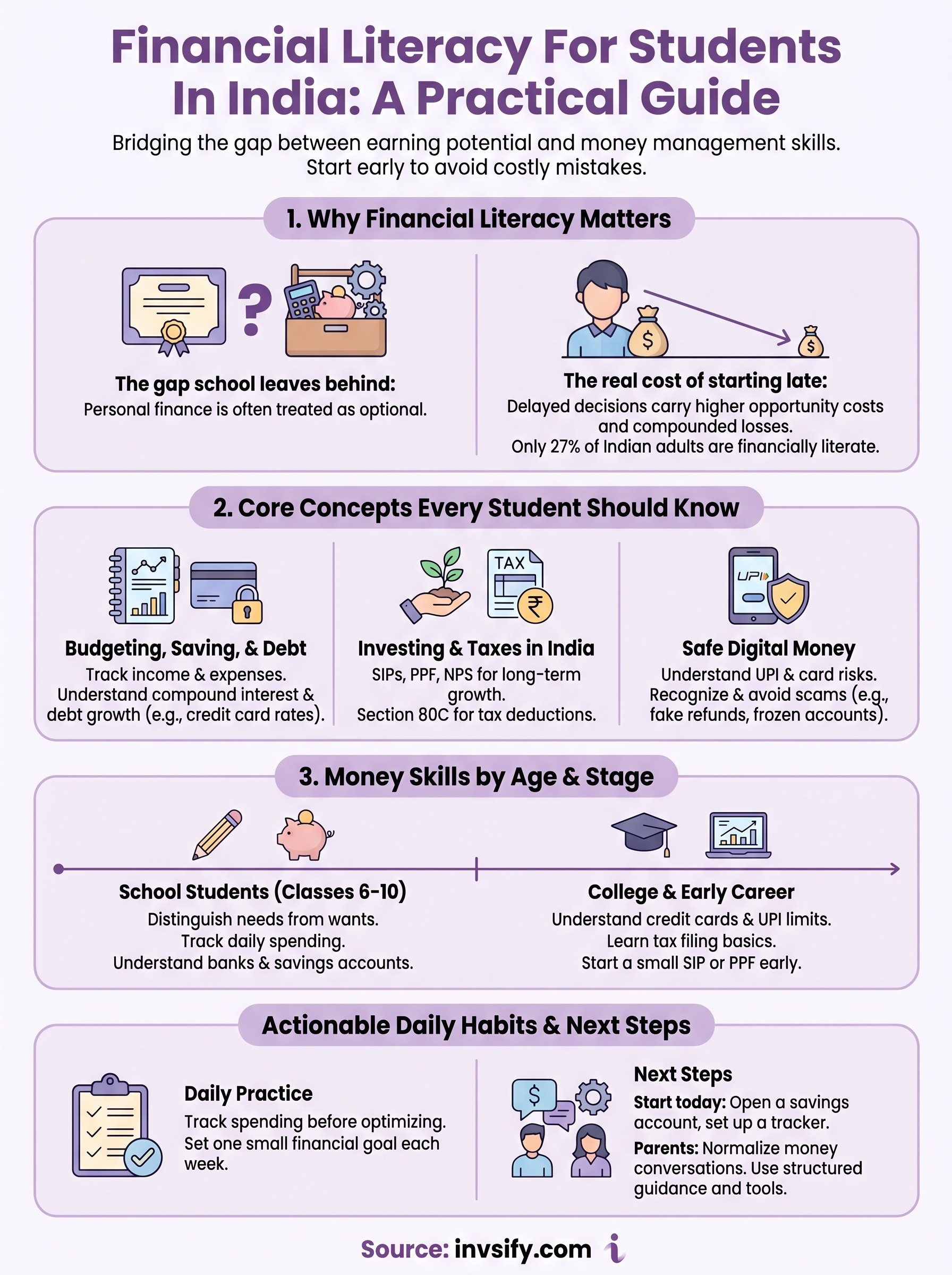

Financial Literacy For Students In India: A Practical Guide

Shlok Sobti

Financial Literacy For Students In India: A Practical Guide

Most students in India finish their degrees without learning how to file taxes, read a mutual fund factsheet, or even build a basic budget. That gap, between earning potential and money management skills, is exactly why financial literacy for students in India matters more than most academic subjects. The earlier you understand how money works, the fewer costly mistakes you make when your first salary hits your bank account.

This guide breaks down what financial literacy actually means in the Indian context, covers the core concepts every student should know, and points you toward practical resources, from government initiatives to digital tools, that make learning accessible. Whether you're in college or just starting your career, you'll find actionable steps you can take right now, not vague advice you've already heard.

At Invsify, we're a SEBI Registered Investment Advisor that uses AI to deliver transparent, conflict-free financial guidance to Indians at every stage of their wealth journey. We built this guide because we believe smart financial decisions start with education, and that education should begin long before your first investment.

Why financial literacy matters for Indian students

India's school system teaches algebra and organic chemistry, but almost nothing about EMIs, credit scores, or income tax slabs. That gap has real consequences. A survey by the National Centre for Financial Education found that only 27% of Indian adults are financially literate, which means the problem starts early and compounds over time. Students who don't learn money basics before their first paycheck often spend years recovering from avoidable debt or missed investment windows.

The gap school leaves behind

The Indian curriculum has improved in many subjects, but personal finance is still treated as optional knowledge rather than a core life skill. You won't find budgeting exercises in a standard Class 12 commerce textbook, and most engineering or arts programs skip money management entirely. This leaves students dependent on advice from parents, friends, or random online forums, sources that can carry outdated assumptions or genuinely wrong information about how the Indian financial system works.

Financial literacy for students in India isn't just about learning to save; it's about building the judgment to make smarter decisions across every life stage.

The real cost of starting late

When you begin earning without understanding how compound interest and tax-saving instruments work, you lose money quietly. A 22-year-old who delays investing by just five years can lose several lakhs in potential corpus by retirement, not because they spent recklessly, but simply because nobody told them how SIPs or ELSS funds worked. Students from middle-income families face a sharper version of this problem because every delayed decision carries a higher opportunity cost when your starting capital is limited. The damage from financial ignorance is rarely one dramatic mistake. More often, it's the steady absence of the right move at the right time, and that turns out to be the most expensive pattern of all.

Core concepts every student should know

You don't need an MBA to understand how money works. Financial literacy for students in India starts with a small set of concepts that most adults use daily, and once you grasp them, everything else in personal finance becomes significantly easier to follow.

Budgeting, saving, and debt

A budget is simply a plan for where your money goes before you spend it. You track your income, list fixed costs like fees or rent, and decide what portion goes into savings. Compound interest works in your favor when you save and directly against you when you borrow. Credit cards in India can carry interest rates of 24-36% annually, so understanding how debt grows stops you from treating borrowed money as free money.

The difference between starting a SIP at 22 versus 27 can add several lakhs to your total corpus over a 30-year period.

Investing and taxes in India

The Indian financial system offers several beginner-friendly tools worth knowing before your first paycheck:

Mutual funds and SIPs: Structured ways to grow money consistently over time

PPF and NPS: Government-backed instruments that also carry tax advantages

Section 80C deductions: Allows you to reduce taxable income by up to ₹1.5 lakh each year through eligible instruments

Learning these foundations early gives you a practical edge. You won't need to decode every financial product from scratch when you already understand the building blocks behind them.

Money skills by age and school stage

Financial literacy for students in India doesn't follow one universal starting point. The right concepts to teach a Class 8 student look very different from what a college sophomore needs to learn. Matching money skills to your current life stage makes the learning practical and immediately relevant.

School Students (Classes 6-10)

Students at this stage benefit most from building foundational habits rather than diving into financial products. The core focus should be on understanding where money comes from, tracking small expenses, and recognizing the difference between needs and wants. Even simple exercises like managing a weekly allowance and noting where it goes can build lasting discipline.

Key skills to develop at this stage:

Distinguishing needs from wants

Tracking daily spending in a notebook or simple app

Understanding how banks work and why savings accounts exist

Building the habit of tracking money at 14 is far easier than trying to build it at 24.

College and Early Career Students

Once you start handling tuition fees, part-time income, or internship stipends, the stakes increase. This is the right stage to understand credit cards, UPI limits, tax filing basics, and SIPs. College students who open a PPF account or start a small SIP early give themselves a measurable head start on long-term wealth creation before their first full-time salary arrives.

How students can practice money habits daily

Knowing the theory behind financial literacy for students in India only helps if you actually apply it. Daily practice is what turns abstract knowledge into reliable habits, and most of these habits take less than five minutes to fit into your existing routine.

Track spending before you optimize it

You can't improve what you don't measure. Start by recording every transaction you make, whether it's a canteen meal or a mobile recharge, in a notes app or a pocket diary. After one week, review the list and find where money left without a clear reason. Awareness alone cuts unnecessary spending for most students before any formal budgeting system is even needed.

Use Google Sheets or a free notes app to log daily expenses

Review your spending every Sunday for 10 minutes

Flag impulse purchases and note whether you regret them

The habit of tracking money at 17 is far easier to build than trying to install it at 27.

Set one small financial goal each week

Weekly goals keep you moving without overwhelming you. Pick one specific target, like saving ₹200 from your allowance or reading one article about a financial instrument you don't understand yet.

Small, consistent actions compound over months the same way money does inside an investment account, and completing a small goal each week builds genuine confidence in your ability to manage money over time.

Safe digital money in India: UPI, cards, scams

Digital payments are now a daily reality for most Indian students, but UPI and cards carry risks that nobody explains in school. A solid grounding in financial literacy for students in India includes understanding how these tools work and what fraudsters do to exploit them.

How UPI and debit cards work

UPI lets you transfer money instantly using just a phone number or UPI ID, but your UPI PIN is the single most sensitive piece of information tied to your account. Never share it with anyone, including people claiming to be from your bank. Debit cards draw directly from your savings account balance, so a compromised card drains real money immediately, unlike a credit card where you can dispute charges before payment.

Recognizing and avoiding scams

Scams targeting students in India often follow predictable patterns. Watch for:

Fake "refund" requests asking you to enter your PIN to receive money

Calls from unknown numbers claiming your account is frozen

QR codes that debit your account instead of crediting it

Legitimate banks and payment apps will never ask for your UPI PIN, OTP, or card CVV over a call or message.

Reporting fraud quickly through your bank's helpline or the national cybercrime portal at cybercrime.gov.in limits the damage and improves your chances of recovery.

Next steps for students and parents

Financial literacy for students in India builds over time, not in one afternoon. The most effective approach is to start with one concrete action this week, whether that's opening a savings account, setting up a simple expense tracker, or reading through the basics of Section 80C. Parents play a real role here too: normalizing money conversations at home gives students a foundation that no classroom curriculum currently provides.

For students ready to move beyond the basics, getting structured guidance makes a measurable difference. AI-powered advisory tools can help you understand your financial position, track your investments, and make informed decisions without the hidden fees that come with traditional distributors. If you want transparent, SEBI-registered guidance built around your actual goals rather than generic advice, start your financial journey with Invsify and see how smart, conflict-free advice changes the way you think about your money.