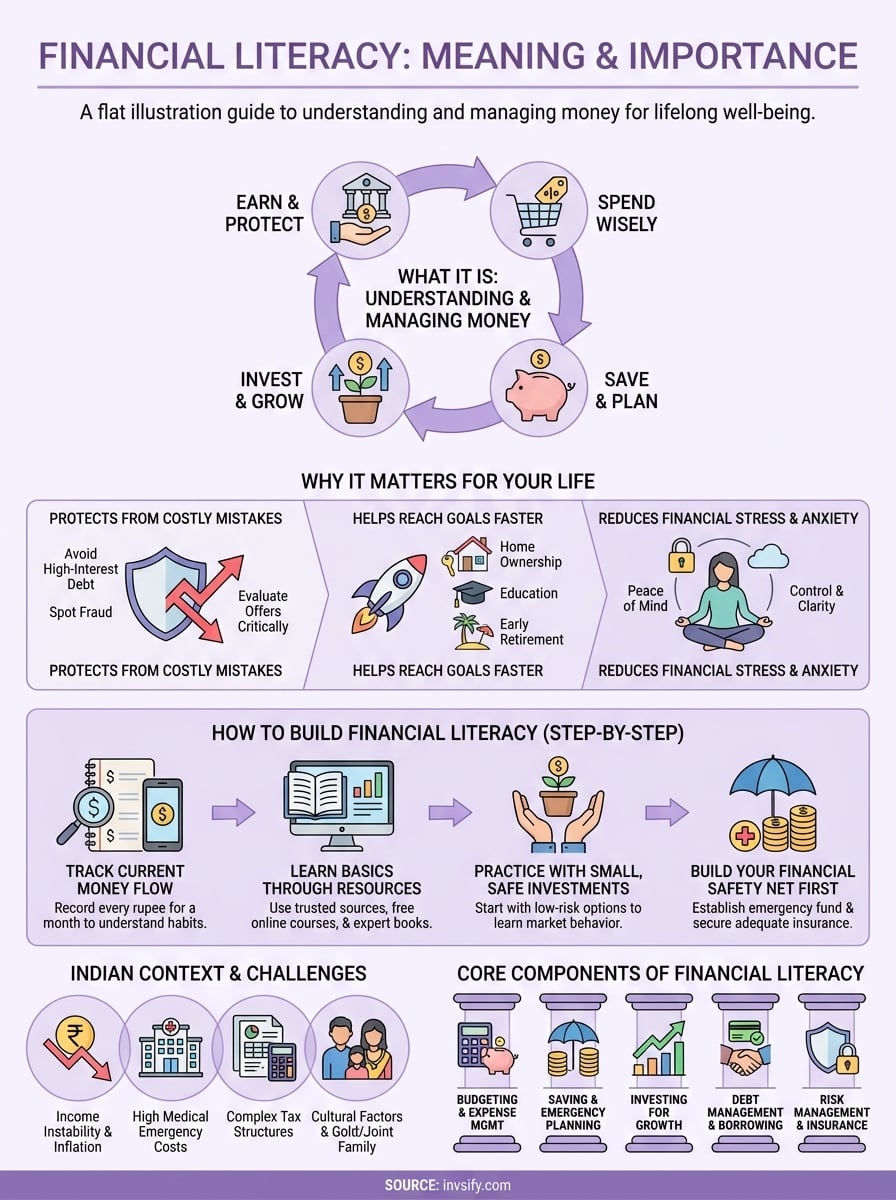

Financial Literacy Meaning: What It Is and Why It Matters

Shlok Sobti

Financial Literacy Meaning: What It Is and Why It Matters

Financial literacy means understanding how money works and knowing how to manage it well. It covers the basics of earning, spending, saving, investing, and protecting your wealth. When you're financially literate, you can make informed decisions about your money instead of feeling confused or overwhelmed. You know how to create a budget, build an emergency fund, choose the right investments, and avoid unnecessary debt. This knowledge helps you move toward your goals with confidence.

This article breaks down what financial literacy really means and why it matters for your everyday life. You'll discover the core components that make up financial literacy, from budgeting and saving to investing and risk management. We'll explore how these skills apply specifically to the Indian context, where unique challenges and opportunities shape your financial journey. You'll also learn practical steps to build your money skills at any life stage, recognize common mistakes that drain wealth, and understand how modern tools and advisory services can support your growth. By the end, you'll have a clear roadmap for improving your financial knowledge and making smarter decisions with your money.

Why financial literacy matters for your life

Your financial decisions shape your entire life, from the home you live in to the retirement you experience. When you understand financial literacy meaning, you gain the power to control your money instead of letting it control you. Every rupee you earn represents time and effort, and knowing how to manage those rupees determines whether you build wealth or struggle with debt. Financial literacy affects your ability to buy a house, fund your children's education, handle medical emergencies, and retire comfortably. Without it, you risk making expensive mistakes that can take years to recover from.

It protects you from costly mistakes

Poor financial decisions drain your wealth faster than you might realize. When you lack basic money skills, you become vulnerable to high-interest loans, unsuitable investment products, and unnecessary fees that eat into your savings. Credit card debt can spiral out of control when you only make minimum payments, costing you thousands in interest. Many people also fall victim to fraudulent schemes because they cannot recognize red flags or understand the risks involved.

Financial literacy gives you the tools to evaluate offers critically and spot potential problems before they damage your finances. You learn to compare interest rates on loans, understand insurance policy terms, and identify investment scams. This knowledge saves you from paying more than necessary and helps you avoid products that don't match your needs. Your ability to ask the right questions and understand the answers protects your hard-earned money from being wasted.

It helps you reach your goals faster

Every financial goal becomes achievable when you know how to plan and execute effectively. Whether you want to buy your first home, start a business, or retire early, financial literacy provides the roadmap. You learn how to set realistic targets, calculate the amount you need to save, and choose the right investment vehicles to grow your money. Instead of hoping things work out, you create a specific plan with measurable milestones.

Understanding your money gives you the confidence to make decisions that align with your dreams instead of reacting to whatever comes your way.

Smart financial planning accelerates your progress by maximizing returns and minimizing waste. You discover tax-saving strategies that let you keep more of what you earn. You avoid investment products with hidden fees that reduce your gains. Financial literacy turns vague wishes into concrete achievements by showing you exactly what actions to take and when.

It reduces financial stress and anxiety

Money worries keep millions of people awake at night, affecting their health and relationships. When you don't understand your financial situation or feel unable to control it, stress builds daily. You worry about unexpected expenses, retirement security, and whether you're making the right choices. This constant anxiety takes a mental and physical toll that impacts your overall quality of life.

Financial literacy brings peace of mind through clarity and control. You know exactly where your money goes each month, how much you've saved, and what your financial future looks like. This understanding replaces fear with confidence. Even when challenges arise, you feel equipped to handle them because you've built emergency funds and learned problem-solving strategies. Your improved financial health supports better mental health and stronger relationships.

How to build financial literacy step by step

Building financial literacy doesn't happen overnight, but you can develop strong money skills by following a clear path. The journey starts with understanding where you stand today and gradually adding knowledge and habits that strengthen your financial foundation. You don't need to master everything at once or take expensive courses to improve. Small, consistent actions create lasting change in how you handle money. This step-by-step approach helps you develop practical skills while avoiding the overwhelm that stops many people from even starting.

Start with tracking your current money flow

Your first action should be recording every rupee that comes in and goes out for at least one month. This simple practice reveals spending patterns you didn't know existed and shows exactly where your money disappears. Download a basic spreadsheet or use a notebook to write down each transaction, from your morning chai to your monthly rent. You'll discover categories where you spend more than you realized and opportunities to redirect money toward your goals.

This tracking exercise creates awareness that changes behavior automatically. When you see that restaurant meals cost ₹8,000 last month, you'll naturally think twice before ordering delivery again. Understanding your cash flow forms the foundation for every other financial skill because you cannot improve what you don't measure. After tracking for a month, you'll have real data to build your first budget instead of guessing at numbers.

Learn the basics through reliable resources

You need to educate yourself using trusted sources that explain concepts clearly without selling you products. Start with fundamental topics like compound interest, asset allocation, tax planning, and emergency funds. The Reserve Bank of India's financial education resources provide accurate information specific to Indian financial products and regulations. Free online courses from reputable institutions teach you at your own pace without pressure.

Building knowledge through quality education prevents costly mistakes and helps you recognize when someone gives you bad advice.

Books written by respected financial experts offer deeper insights than random blog posts or social media tips. Look for authors who explain financial literacy meaning through real examples and avoid those promising quick riches. Your goal is understanding principles that apply regardless of market conditions, not chasing the latest investment fad. Quality education gives you the confidence to ask advisors tough questions and verify their recommendations.

Practice with small, safe investments

Once you understand basic concepts, start applying them with small amounts you can afford to lose while learning. Open a recurring deposit or invest ₹500 monthly in a low-cost index fund to experience how markets behave. This hands-on practice teaches lessons no book can, like how your emotions respond to portfolio fluctuations. You'll learn to distinguish between temporary volatility and genuine problems.

Starting small protects your wealth while you develop judgment about which investments match your goals and risk tolerance. Track these initial investments carefully and review them quarterly to see what works. Real experience builds intuition that helps you make better decisions as your portfolio grows larger.

Build your financial safety net first

Before chasing returns, establish an emergency fund covering three to six months of expenses. This fund gives you financial security to handle job loss, medical emergencies, or urgent home repairs without taking debt. Keep this money in a liquid account where you can access it quickly, like a savings account or liquid mutual fund. Your emergency fund protects all your other financial progress from derailing when unexpected costs arise.

After securing your emergency fund, focus on adequate insurance coverage for health, life, and disability. These protections prevent financial disasters that wipe out years of savings in one accident or illness. Building this foundation first means your investments can focus purely on growth instead of needing to be liquidated for emergencies.

What financial literacy means in the Indian context

Financial literacy meaning takes on unique dimensions in India, where diverse financial systems, cultural practices, and economic realities shape how you manage money. Your financial journey differs significantly from someone in developed nations because you navigate challenges like high inflation, complex tax structures, and a rapidly evolving digital payment ecosystem. Understanding financial literacy in India means knowing how to balance traditional values like family obligations and gold purchases with modern investment vehicles. You also need to grasp the role of government schemes, the importance of formal banking systems, and how to protect yourself from unregulated investment schemes that proliferate in Indian markets.

India-specific financial challenges you face

You encounter obstacles that make financial planning more complex than in many other countries. Income instability affects millions, whether you're in the gig economy, run a small business, or work in sectors without guaranteed monthly salaries. This unpredictability makes it harder to commit to systematic investment plans or secure loans on favorable terms. Healthcare costs represent another major concern since medical emergencies can drain entire life savings in days, and insurance penetration remains relatively low across the country.

Your tax obligations also require special attention because the Indian tax system includes multiple categories, deductions, and filing requirements that confuse many taxpayers. You need to understand concepts like Form 16, advance tax payments, and various exemptions to optimize your tax burden legally. Many Indians also support extended family members financially, which creates obligations that Western financial planning models never account for.

Cultural factors that shape your money choices

Indian society influences your financial decisions in ways that pure economics cannot explain. Joint family systems often mean you contribute to shared expenses or support elderly parents, affecting how much you can save independently. Gold holds cultural and emotional value beyond its investment returns, so you might allocate more to jewelry than financial advisors typically recommend. These traditions reflect valid priorities even if they don't maximize returns.

Understanding these cultural contexts helps you make financial choices that honor your values while still building wealth effectively.

Property ownership carries immense social significance in India, pushing many people to buy homes earlier than financially optimal. You feel pressure to purchase real estate even when renting would free up capital for higher-return investments.

How Indian regulations protect and guide you

You benefit from specific regulatory frameworks designed for Indian investors. SEBI registration helps you identify legitimate investment advisors versus commission-driven distributors who may not act in your best interest. Knowing that your bank deposits enjoy insurance up to ₹5 lakh through DICGC protects you from bank failures. These regulations create safety nets that reduce risk when you make informed choices about where to invest your money.

Core components of financial literacy

Understanding financial literacy meaning requires grasping the five fundamental pillars that support your entire financial life. These components work together to help you make smart money decisions, build wealth over time, and protect yourself from financial setbacks. You need to develop competence in each area because weakness in one component undermines your overall financial health. Mastering these building blocks gives you the confidence to navigate complex financial situations and seize opportunities when they appear.

Budgeting and expense management

Your budget acts as the foundation for all other financial activities because it shows exactly where your money goes each month. You create a realistic plan that allocates income across necessities like rent and groceries, savings goals, and discretionary spending on entertainment or dining out. This practice reveals spending leaks where money disappears without adding value to your life, allowing you to redirect those funds toward more meaningful goals.

Effective budgeting means tracking expenses regularly and adjusting allocations when your income or priorities change. You learn to distinguish between needs and wants, making conscious choices about trade-offs instead of wondering why your account runs empty before month end. Smart expense management also includes negotiating bills, comparing prices before major purchases, and finding ways to reduce recurring costs without sacrificing quality of life.

Saving and emergency planning

Building savings protects you from falling into debt when unexpected costs arise and provides capital for pursuing opportunities. You start by establishing an emergency fund covering three to six months of essential expenses, keeping this money accessible in liquid accounts. This safety net gives you breathing room to handle job loss, medical emergencies, or urgent home repairs without disrupting your long-term investment plans.

Beyond emergencies, systematic saving helps you accumulate funds for specific goals like wedding expenses, property down payments, or foreign travel. You develop the discipline to pay yourself first by setting aside money immediately when salary arrives rather than saving whatever remains at month end.

Investing for growth

Investing transforms your money from static savings into growing wealth that outpaces inflation and builds financial independence. You learn how different asset classes like equity, debt, gold, and real estate each serve specific purposes in your portfolio. Understanding risk and return helps you match investments to your goals, timeline, and comfort level with market fluctuations.

Smart investing involves starting early to harness compound returns, diversifying across assets to reduce risk, and maintaining discipline during market volatility. You discover tax-efficient investment vehicles like ELSS funds or PPF that reduce your tax burden while growing wealth. Regular portfolio reviews ensure your investments stay aligned with changing life circumstances and financial goals.

Debt management and borrowing

Knowing how to use debt strategically accelerates your financial progress while avoiding traps that drain wealth for years. You understand the difference between productive debt like education or home loans that build assets versus destructive debt from credit cards or personal loans for consumption. Smart borrowing means comparing interest rates, understanding repayment terms, and calculating the total cost before committing to any loan.

Managing debt effectively means borrowing only what you can comfortably repay while maintaining your savings and investment contributions.

Debt management includes strategies for paying down existing loans faster through prepayments or balance transfers to lower-rate options. You protect your credit score by making timely payments and keeping credit utilization low, ensuring access to favorable borrowing terms when genuinely needed.

Risk management and insurance

Insurance protects your financial plan from devastating setbacks that could wipe out years of savings in one event. You identify risks your family faces and purchase adequate coverage for health, life, disability, and property damage. Understanding policy terms helps you avoid over-insurance that wastes money or under-insurance that leaves dangerous gaps in protection.

Effective risk management extends beyond insurance to include diversifying income sources, maintaining emergency funds, and avoiding concentrated bets on single investments. You regularly review coverage as your responsibilities grow with marriage, children, or business ownership to ensure protection keeps pace with your needs.

How financial literacy changes across life stages

Your financial priorities and challenges evolve significantly as you move through different life phases, requiring you to adapt your money skills accordingly. What worked perfectly in your twenties becomes inadequate when you start a family or approach retirement. Understanding financial literacy meaning includes recognizing how your financial needs shift over time and adjusting your strategies to match each stage. The investment mix that builds wealth in your thirties differs dramatically from the protective strategies you need in your sixties. Your ability to adapt your financial approach ensures continuous progress toward security and independence regardless of your current age.

Early career years (20s to early 30s)

Your focus during this stage centers on building solid financial foundations while maximizing growth opportunities. You establish good money habits like tracking expenses, creating budgets, and automating savings before lifestyle inflation erodes your earning power. Time remains your greatest asset because even small investments made now benefit from decades of compounding returns. Starting a systematic investment plan in equity mutual funds lets you ride out market volatility while accumulating substantial wealth over time.

This phase also requires protecting yourself with adequate health insurance and term life insurance if you have dependents. You learn to balance loan repayments for education or vehicles with building emergency funds and retirement savings. Career development investments like skill upgrades or certifications deliver high returns by increasing your earning potential for decades ahead.

Family building phase (mid-30s to 40s)

Your financial responsibilities multiply during these years as you support children, manage home loans, and care for aging parents. Education planning becomes critical because school and college costs rise faster than general inflation, requiring dedicated investments in child-specific plans. You need higher insurance coverage to protect your family's lifestyle if something happens to you, making adequate term insurance and comprehensive health coverage essential.

Balancing current family needs with future retirement savings defines your financial success during these demanding middle years.

This stage tests your discipline because immediate demands often tempt you to reduce long-term savings. You must maintain retirement contributions even while paying school fees and EMIs because lost years cannot be recovered later. Reviewing and rebalancing your portfolio annually ensures your investments match your changing risk tolerance and approaching goals.

Pre-retirement and retirement years (50s onwards)

Your strategy shifts from aggressive growth to wealth preservation and income generation as retirement approaches. You gradually move money from equity to debt instruments that provide stability and regular income without excessive market risk. Planning systematic withdrawal strategies helps you determine how much you can safely spend monthly without depleting savings prematurely. Healthcare becomes your largest concern, requiring comprehensive insurance coverage and dedicated funds for medical expenses that increase with age.

Estate planning gains importance as you consider how to transfer wealth efficiently to heirs while minimizing tax burdens. You focus on simplifying your financial life by consolidating accounts, updating nominees, and ensuring family members understand your financial arrangements.

Everyday money decisions that show financial literacy

Financial literacy shows up not just in major investment choices but in the small money decisions you make every single day. These routine choices reveal whether you truly understand financial literacy meaning and apply it practically. Your daily actions around spending, saving, and managing transactions demonstrate your real competence with money far more clearly than theoretical knowledge ever could. Smart everyday decisions compound over time to create significant wealth differences between people with similar incomes. The way you handle your morning coffee purchase, monthly subscriptions, and bill payments shows whether financial principles guide your behavior or whether you operate on autopilot.

Choosing the right payment method

You demonstrate financial wisdom when you select payment methods strategically based on each situation rather than using one option mindlessly. Paying with a credit card for purchases you can afford immediately lets you earn rewards points while maintaining a strong credit score through full monthly payments. Switching to UPI or debit cards for impulse purchases helps you avoid debt on items that don't justify borrowing costs.

Understanding transaction fees guides your choices at ATMs, where you withdraw from network machines to avoid unnecessary charges that drain ₹20 each time. You recognize when cash payments secure better discounts than card transactions, saving you money on everything from vegetables to vehicle servicing. These small payment decisions reflect your grasp of costs and benefits in each transaction.

Comparing before you buy

Financially literate people research major purchases carefully instead of buying impulsively or blindly trusting a single vendor. You check multiple sellers before purchasing electronics, appliances, or furniture to find the best combination of price, warranty, and service. Online comparison helps you identify inflated prices and negotiate better deals even in physical stores.

Smart shoppers understand that spending an hour researching a ₹15,000 purchase can save thousands while building better financial judgment for future decisions.

This habit extends to financial products where you compare interest rates on loans, insurance premiums across insurers, and mutual fund expense ratios before committing your money. Your willingness to invest time in comparison shopping demonstrates the patience and discipline that builds wealth over decades.

Reviewing and negotiating bills

You practice financial literacy when you scrutinize monthly bills instead of paying them blindly. Checking mobile plans regularly helps you identify unused features or cheaper alternatives that reduce expenses without sacrificing service quality. Examining credit card statements catches unauthorized charges or subscription renewals you forgot to cancel, protecting your money from leaking away unnoticed.

Negotiating with service providers shows you understand your value as a customer and refuse to overpay. You call internet providers to request better rates or threaten to switch, often securing discounts that loyal customers who never ask continue missing. These small acts of financial self-advocacy accumulate meaningful savings.

Mistakes people make when they lack financial literacy

People without solid money skills fall into predictable traps that drain their wealth and delay their financial goals for years. These mistakes stem from not understanding financial literacy meaning and failing to apply basic principles to everyday decisions. You see these errors repeatedly across income levels because they reflect gaps in knowledge rather than lack of money. Recognizing common mistakes helps you avoid them and course-correct quickly if you've already made them. The financial damage from these missteps compounds over time, making early awareness and prevention crucial for your long-term wealth building.

Taking high-interest debt without understanding costs

You make one of the most expensive mistakes when you borrow money without calculating the true repayment amount. Credit cards charging 36-42% annual interest turn a ₹50,000 purchase into ₹75,000 or more when you make only minimum payments. Personal loans marketed as quick solutions often carry processing fees and interest rates that double your actual borrowing cost compared to what advertisements highlight.

Many people also fall into the trap of taking multiple small loans from different lenders without realizing how the combined EMIs exceed their repayment capacity. Payday loans and instant credit apps promise convenience but charge interest rates that would be illegal in many countries. Your lack of understanding about compound interest and effective annual rates costs you thousands in unnecessary payments that could have built wealth instead.

Skipping insurance until it's too late

Delaying insurance purchases represents a dangerous gamble that destroys families financially when medical emergencies or deaths occur. You assume nothing bad will happen to you, so you avoid health insurance premiums to save a few thousand rupees monthly. This decision backfires catastrophically when a single hospitalization costs ₹5-10 lakh, wiping out all your savings and forcing you into debt.

Waiting until you face health issues to buy insurance means either paying prohibitively high premiums or facing coverage rejections that leave you permanently unprotected.

Term life insurance becomes more expensive as you age, and waiting costs you significantly in cumulative premiums over your working life. Young people especially neglect insurance, not understanding that their insurability and low premiums represent advantages they lose forever by delaying.

Following investment advice from unqualified sources

You damage your financial future when you take investment tips from relatives, colleagues, or social media personalities without verifying their expertise or intentions. Unregistered advisors often push products that earn them commissions rather than matching your goals and risk tolerance. Friends share hot stock tips based on rumors or past performance, leading you to invest in overpriced assets right before crashes.

Television anchors and YouTube influencers create urgency around investments without disclosing conflicts of interest or explaining risks honestly. Your tendency to trust familiar faces over qualified professionals costs you returns and exposes you to fraudulent schemes that SEBI regularly warns against.

Simple tools to improve your money skills

You don't need expensive software or complicated systems to strengthen your financial knowledge and habits. Simple, accessible tools help you track progress, understand concepts, and make better decisions without overwhelming you with features you'll never use. Modern technology puts powerful financial management capabilities in your pocket through smartphone apps and free online resources. These tools transform abstract financial concepts into concrete numbers and visual progress that keeps you motivated. Starting with basic tools builds confidence before you graduate to more sophisticated platforms as your needs grow.

Digital apps that track your spending automatically

Mobile apps connect to your bank accounts and credit cards to categorize every transaction without manual data entry. You see exactly where your money goes each month through visual breakdowns that highlight problem areas like excessive dining out or subscription services you forgot existed. Popular apps like Walnut, ET Money, or your bank's own application provide this functionality free, eliminating the excuse that tracking feels too tedious or time-consuming.

These apps send spending alerts when you exceed budget limits in specific categories, helping you course-correct immediately instead of discovering problems when the month ends. Push notifications about bill due dates prevent late payment charges that damage your credit score and waste money.

Calculators that show your financial progress

Online calculators help you understand financial literacy meaning by showing the real impact of your decisions in rupees and years. Compound interest calculators demonstrate how starting investments today versus five years later affects your final wealth dramatically. EMI calculators reveal the true cost of loans by showing total interest payments alongside principal amounts, helping you evaluate whether borrowing makes sense.

Retirement calculators translate vague future worries into specific monthly savings targets you can act on immediately.

SIP calculators show how regular small investments grow into substantial amounts through market returns over decades. Goal planning tools help you determine exactly how much to save monthly for specific objectives like home down payments or children's education.

Learning platforms that teach at your pace

Free educational resources from institutions like the National Institute of Securities Markets or RBI's financial education portal teach fundamental concepts through structured courses you complete on your schedule. YouTube channels run by qualified financial planners explain complex topics using real examples that make sense for Indian investors.

Podcast apps let you learn during commutes by listening to episodes about budgeting, tax planning, or investment strategies. These audio resources turn otherwise wasted time into education that compounds your knowledge steadily without requiring dedicated study hours.

How smart advisory supports your financial literacy

Building financial knowledge on your own takes years of learning from mistakes and piecing together information from scattered sources. Professional advisory services accelerate this process by giving you expert guidance that prevents costly errors while teaching you sound financial principles. Modern AI-powered advisory combines technology with human expertise to make quality financial advice accessible and affordable for everyone, not just wealthy investors. You gain structured education tailored to your specific situation rather than wading through generic content that may not apply to your circumstances.

Professional guidance removes confusion

You avoid wasting time on trial and error when qualified advisors explain concepts in clear terms and show you how to apply them. SEBI-registered investment advisors operate under fiduciary standards that require them to act in your best interest rather than earning commissions by selling unsuitable products. This conflict-free advice helps you understand financial literacy meaning through personalized recommendations that consider your income, goals, risk tolerance, and life stage.

Professional advisors also spot blind spots in your financial plan that you might overlook completely. They identify gaps in insurance coverage, tax inefficiencies, or portfolio imbalances that quietly drain wealth. Your conversations with advisors build knowledge systematically as they explain the reasoning behind each recommendation.

Technology makes expertise accessible 24/7

AI-powered advisory platforms provide instant answers to your financial questions without waiting for business hours or scheduling appointments. You interact with intelligent chatbots that analyze your portfolio, suggest optimizations, and explain complex concepts in simple language whenever questions arise. This constant availability means you learn continuously through real-time feedback rather than annual reviews that happen too late to prevent mistakes.

Technology democratizes financial expertise by making professional-grade tools and insights available to everyone regardless of their account size or location.

Automated tracking shows your wealth wellness score and highlights specific areas needing attention, turning vague financial anxiety into concrete action items. You receive personalized insights based on your actual financial data rather than generic advice that may not suit your situation.

Personalized recommendations match your reality

Generic financial content cannot account for your unique circumstances, goals, or constraints. Smart advisory services analyze your complete financial picture including income patterns, existing investments, debts, and family obligations to provide customized guidance. You receive recommendations that balance your immediate needs with long-term wealth building in ways that reflect your actual priorities and comfort level.

This personalization extends to ongoing adjustments as your life changes through marriage, children, career shifts, or approaching retirement. Your financial plan evolves with you rather than following a static template that becomes outdated quickly.

Keep growing your money skills

Financial literacy represents a journey rather than a destination that you complete and forget. Your understanding of financial literacy meaning deepens as you gain experience, face new challenges, and apply concepts to real situations throughout your life. Each year brings different financial decisions that test and expand your knowledge, from buying your first property to managing portfolio rebalancing during market volatility. Continuous learning keeps you ahead of changing regulations, new investment products, and evolving tax rules that affect your wealth building strategies.

Start implementing what you've learned today by tracking expenses, building emergency savings, and evaluating your current investments critically. Professional guidance accelerates your progress by providing personalized insights matched to your specific goals and risk tolerance. Discover how Invsify's AI-powered advisory helps you make smarter financial decisions while building the knowledge you need for long-term wealth success and financial independence.