Financial Planning For Beginners India: A Step-By-Step Plan

Shlok Sobti

Financial Planning For Beginners India: A Step-By-Step Plan

Most people in India don't start managing their money because they lack income, they delay it because they don't know where to begin. If you've been searching for financial planning for beginners India, you're already ahead of the curve. The truth is, building wealth isn't about earning more; it's about making smarter decisions with what you already have.

Whether you're a salaried professional putting money into a savings account and calling it a plan, or someone juggling EMIs without a clear strategy, this guide breaks it all down for you. You'll get a step-by-step framework covering budgeting, goal-setting, debt management, emergency funds, and basic investing, all tailored to the Indian financial system, from PPF and ELSS to health insurance and Section 80C.

At Invsify, we work with people exactly at this stage, helping them move from confusion to clarity with AI-powered, conflict-free financial advice as a SEBI Registered Investment Advisor. This guide reflects the same philosophy: give people straightforward, actionable knowledge so they can take control of their money. Let's get into it.

What financial planning means in India

Financial planning is the process of mapping your current money situation to the future you want to build. It's not a one-time spreadsheet exercise or a product your banker sells you. At its core, it means knowing what you earn, what you spend, what you owe, and where your money needs to go to hit specific goals. For anyone starting out with financial planning for beginners India, the first thing to understand is that the Indian financial system has its own tax structures, investment instruments, and regulatory bodies, and any plan worth following has to account for all of them, not just generic advice copied from a global finance blog.

A financial plan built on generic global advice often misses the instruments, tax laws, and inflation realities that define wealth-building in India.

Why the Indian context is different

India's financial landscape presents a unique mix of high inflation, complex tax laws, and homegrown investment options that don't exist in most other countries. The tax system under the Income Tax Act gives you specific deductions like Section 80C (up to ₹1.5 lakh per year), which directly shape how smart investors allocate money into instruments like PPF, ELSS, and NPS. On top of that, inflation in India has historically run higher than in developed economies, which means a savings account paying 3-4% interest is actually losing real purchasing power every year you leave money in it.

Your income structure matters too. Most salaried individuals receive a Cost to Company (CTC) package that includes components like HRA, LTA, and PF contributions, each carrying specific tax implications you can use to your advantage. Understanding these isn't optional; it's foundational. A plan that ignores your HRA exemption or employer PF contribution is leaving real money on the table starting from the very first payslip.

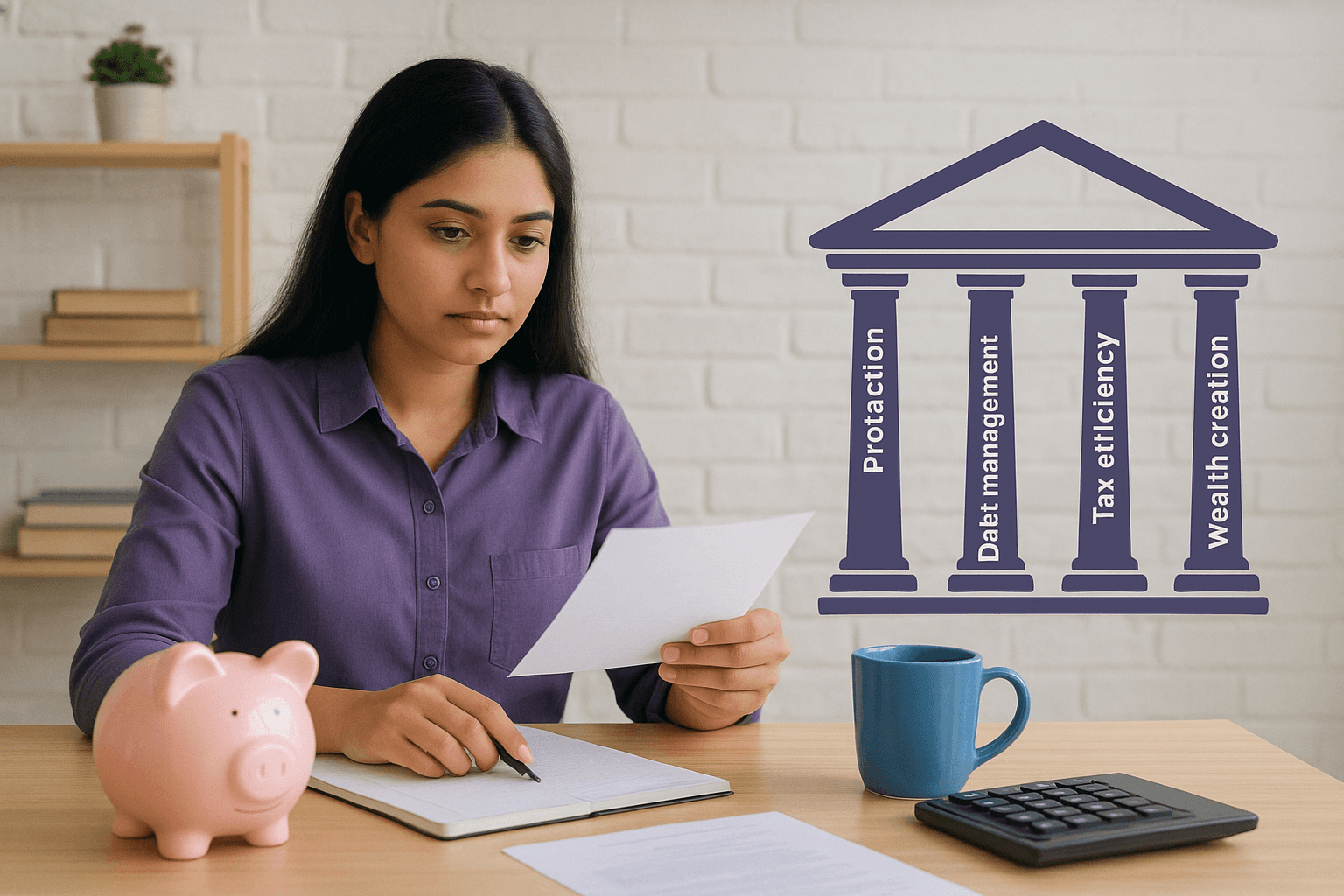

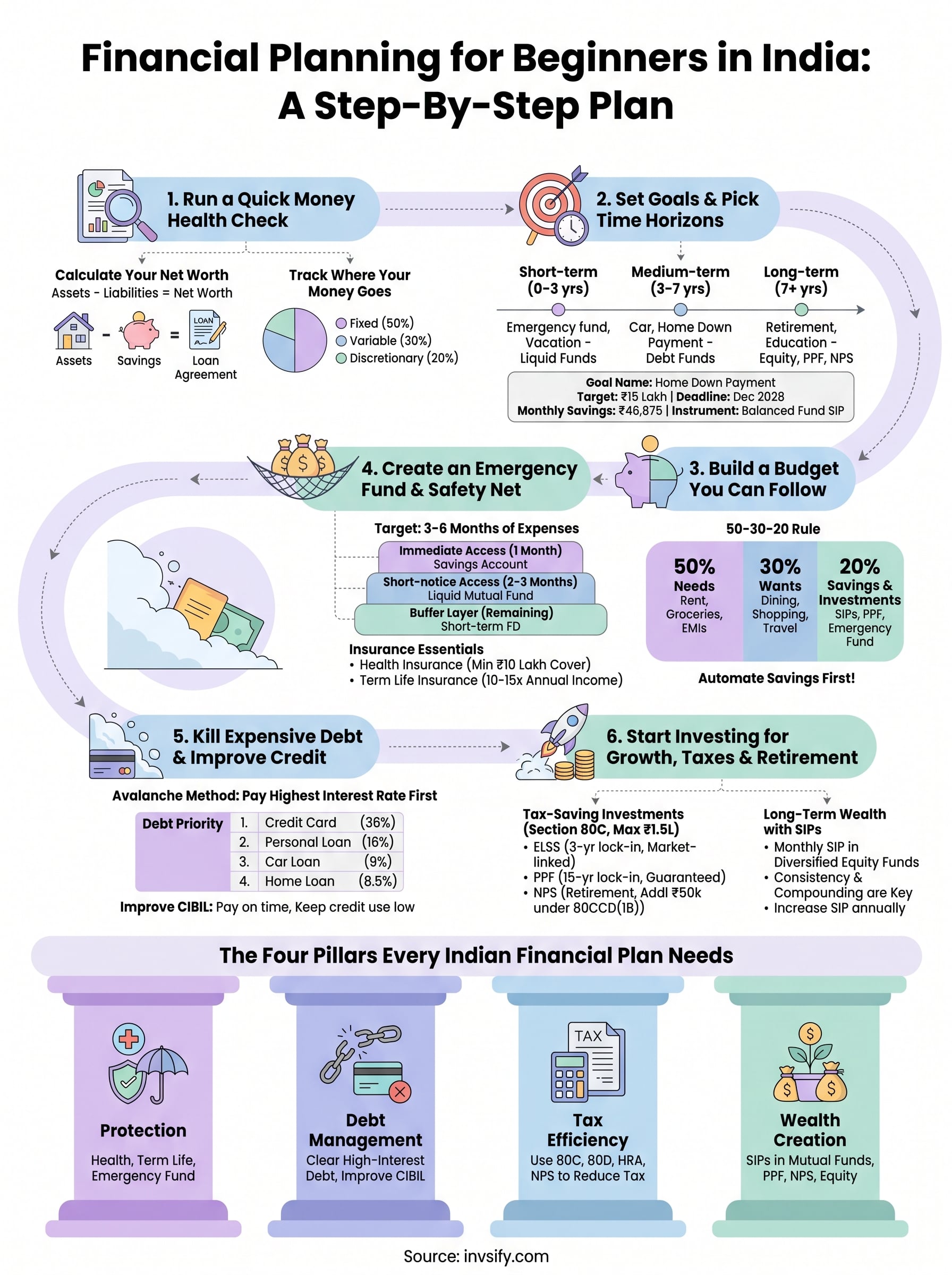

The four pillars every Indian financial plan needs

No financial plan works without a clear foundation. For Indian investors at any income level, these four pillars give you the structure to build on:

Pillar | What it covers |

|---|---|

Protection | Health insurance, term life insurance, emergency fund |

Debt management | Clearing high-interest debt, improving your CIBIL score |

Tax efficiency | Using 80C, 80D, HRA, and NPS to reduce your tax outgo |

Wealth creation | SIPs in mutual funds, PPF, NPS, and direct equity for long-term growth |

Each pillar connects to the others in a specific order. Carrying high-interest debt while trying to invest in equity is like filling a bucket with a hole in it. You need to address protection and debt first before wealth creation makes sense. This sequencing is what separates a real financial plan from a random collection of financial products your relationship manager pushed.

Think of these four pillars as the checklist you return to every time your financial situation changes, whether that's a salary hike, a new dependent, or a home loan decision. Your plan should be a living document you revisit at least once a year, not something you write once and file away. Regular reviews are what keep your money working toward your actual goals rather than just sitting in whatever default account you set up three years ago.

Step 1. Run a quick money health check

Before you build any plan, you need an honest picture of where you stand today. Think of this as your financial baseline: the number you will measure all future progress against. Skipping this step is one of the most common mistakes people make when starting financial planning for beginners India, because they jump straight to investing before understanding what they actually have or owe. Set aside 30 minutes, pull out your bank statements, salary slips, and any loan documents, then work through the two exercises below.

Calculate your net worth

Your net worth is the single most useful number in any financial health check. It tells you exactly where you stand: total assets minus total liabilities. Calculating it takes less time than you think, and the result gives you a clear starting point for every financial decision you make going forward.

Here's a simple template you can fill in right now:

Category | Item | Value (₹) |

|---|---|---|

Assets | Savings account balance | |

Fixed deposits and RDs | ||

PPF / EPF balance | ||

Mutual funds / stocks | ||

Property (current market value) | ||

Gold (physical + digital) | ||

Liabilities | Home loan outstanding | |

Personal loan outstanding | ||

Credit card outstanding | ||

Education loan |

Net Worth = Total Assets - Total Liabilities

A negative result isn't a failure. It's information, and knowing it tells you exactly which problem to address first.

Your net worth is a starting point, not a verdict. Every financial decision you make from here should move this number in the right direction.

Track where your money actually goes

Most people significantly underestimate their monthly expenses because they only track large payments and forget smaller recurring ones. Download your last three months of bank statements and categorize every transaction into three buckets: fixed expenses (rent, EMIs, insurance premiums), variable essentials (groceries, fuel, utilities), and discretionary spending (dining out, streaming subscriptions, weekend plans).

Once you have those three months averaged, you'll have your actual monthly burn rate, not a rough guess. This number feeds directly into your budget in Step 3 and shows you precisely how much you have available to save and invest each month without feeling the pinch.

Step 2. Set goals and pick time horizons

Without clearly defined goals, every financial decision becomes arbitrary. You save some money here, spend more there, with no real direction guiding any of it. This is where financial planning for beginners India often breaks down early: people know they want to "save more," but they haven't attached a specific rupee amount or a deadline to that intention. A goal without a number and a timeline is just a preference dressed up as a plan.

A goal without a rupee amount and a deadline is not a financial goal; it is simply a preference.

Sort your goals by time horizon

Not all goals operate on the same timeline, and the investment instruments you use to reach them depend almost entirely on when you need the money. Mixing short-term and long-term goals is how people end up locking money into an illiquid instrument and then breaking it early at a penalty or a loss.

Time Horizon | Duration | Example Goals | Suitable Instruments |

|---|---|---|---|

Short-term | 0-3 years | Emergency fund, vacation, gadget | Liquid funds, high-yield savings, short-term FDs |

Medium-term | 3-7 years | Car, wedding, home down payment | Debt mutual funds, balanced advantage funds, RDs |

Long-term | 7+ years | Retirement, child's education, property | ELSS, PPF, NPS, equity mutual funds via SIP |

Match each goal to the right instrument for its timeline, and you avoid two common mistakes: taking too much risk for a short-term need, or staying too conservative with money you won't touch for 20 years.

Write goals that force a number and a deadline

Vague goals produce vague action. Instead of writing "save for a house," write it in a format that forces specificity and accountability. Use this template for each goal you identify:

Goal name: Home down payment

Target amount: ₹15,00,000

Deadline: December 2028

Months remaining: 32

Monthly savings needed: ₹46,875

Instrument: Balanced advantage fund via SIP

Work backwards from your target amount to the monthly contribution required, and you'll know immediately whether each goal is realistic with your current income or needs to be adjusted before you commit to it.

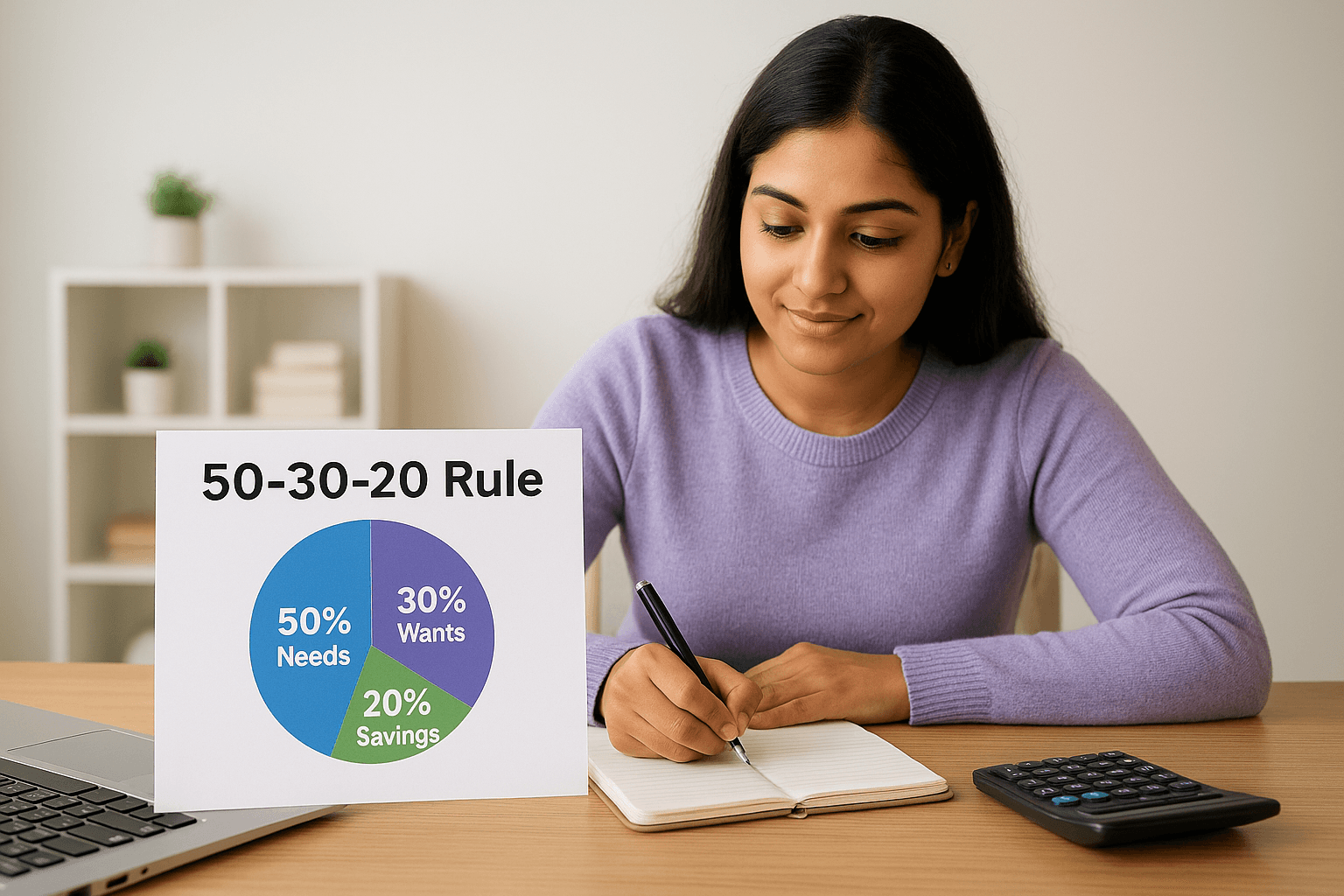

Step 3. Build a budget you can follow

Knowing your money health check number and your goals means nothing if you spend more than you plan every month. A budget isn't a restriction on your lifestyle; it's a system that makes sure your money goes toward what you actually want before it disappears on things you barely remember buying. For anyone working through financial planning for beginners India, the key is to [pick a budgeting structure](https://uat.invsify.com/blog/how-to-create-a-financial-plan) simple enough to stick to, not a 40-row spreadsheet that you abandon after two weeks.

The best budget is not the most detailed one; it's the one you actually review and follow each month.

Start with the 50-30-20 rule

The 50-30-20 rule gives you a percentage-based split that works across most income levels and requires minimal tracking effort. You divide your take-home salary (not CTC) into three buckets and assign every rupee before the month begins.

Bucket | Percentage | What goes here |

|---|---|---|

Needs | 50% | Rent, groceries, utilities, EMIs, insurance premiums |

Wants | 30% | Dining out, streaming, travel, shopping |

Savings and investments | 20% | SIPs, PPF contributions, emergency fund top-ups |

For example, if your take-home salary is ₹60,000 per month, your target split would be ₹30,000 for needs, ₹18,000 for wants, and ₹12,000 for savings. Write these three numbers down before the first of every month and treat your savings bucket as a non-negotiable bill, not whatever is left over after spending.

Adjust the split for your actual numbers

The 50-30-20 rule is a starting point, not a law. If you live in Mumbai or Bengaluru, rent and commute costs alone may push your needs bucket above 50%, and that's fine as long as you consciously trim from wants rather than savings. Shift the wants bucket down to 20% and keep savings at 20% even if it feels tight at first.

Automating your savings is the single most effective way to make your budget stick. Set up an auto-debit or a SIP instruction to trigger on your salary credit date so the money moves before you have any chance to spend it.

Step 4. Create an emergency fund and safety net

An emergency fund is the foundation every other financial goal sits on. Without it, one medical bill, one job loss, or one major repair can force you to break an investment, take a high-interest personal loan, or max out a credit card. For anyone working through financial planning for beginners India, this step is non-negotiable. You build the emergency fund before you optimize taxes, before you chase market returns, and before you consider any other financial goal beyond basic insurance.

Your emergency fund is not an investment; it is a firewall that keeps every other part of your financial plan intact.

How much to save and where to keep it

Most financial advisors recommend three to six months of your total monthly expenses as the target for an emergency fund. Use the monthly burn rate you calculated in Step 1 as your baseline. If your expenses run ₹40,000 per month, your target range is ₹1,20,000 to ₹2,40,000, sitting somewhere accessible without a long lock-in period.

Here is where to keep different portions of that fund:

Portion | Amount | Where to park it |

|---|---|---|

Immediate access | 1 month of expenses | High-yield savings account or salary account |

Short-notice access | 2-3 months of expenses | Liquid mutual fund with instant redemption |

Buffer layer | Remaining amount | Short-term FD (sweepstake or 3-month tenure) |

Build the fund in stages. Start with one month of expenses, then add to it each month until you reach your target. Treat your monthly emergency fund contribution as a fixed line item in your budget, not an optional top-up.

Cover yourself with the right insurance

No emergency fund fully protects you against a serious illness or an income loss that stretches beyond six months. Term life insurance and health insurance are the two policies every working Indian should own before investing a single rupee in the market.

For health insurance, buy a minimum of ₹10 lakh individual cover and consider a super top-up plan to extend it further at a low premium. For term insurance, your sum assured should be at least 10 to 15 times your annual income, bought as a pure term plan with no investment component mixed in.

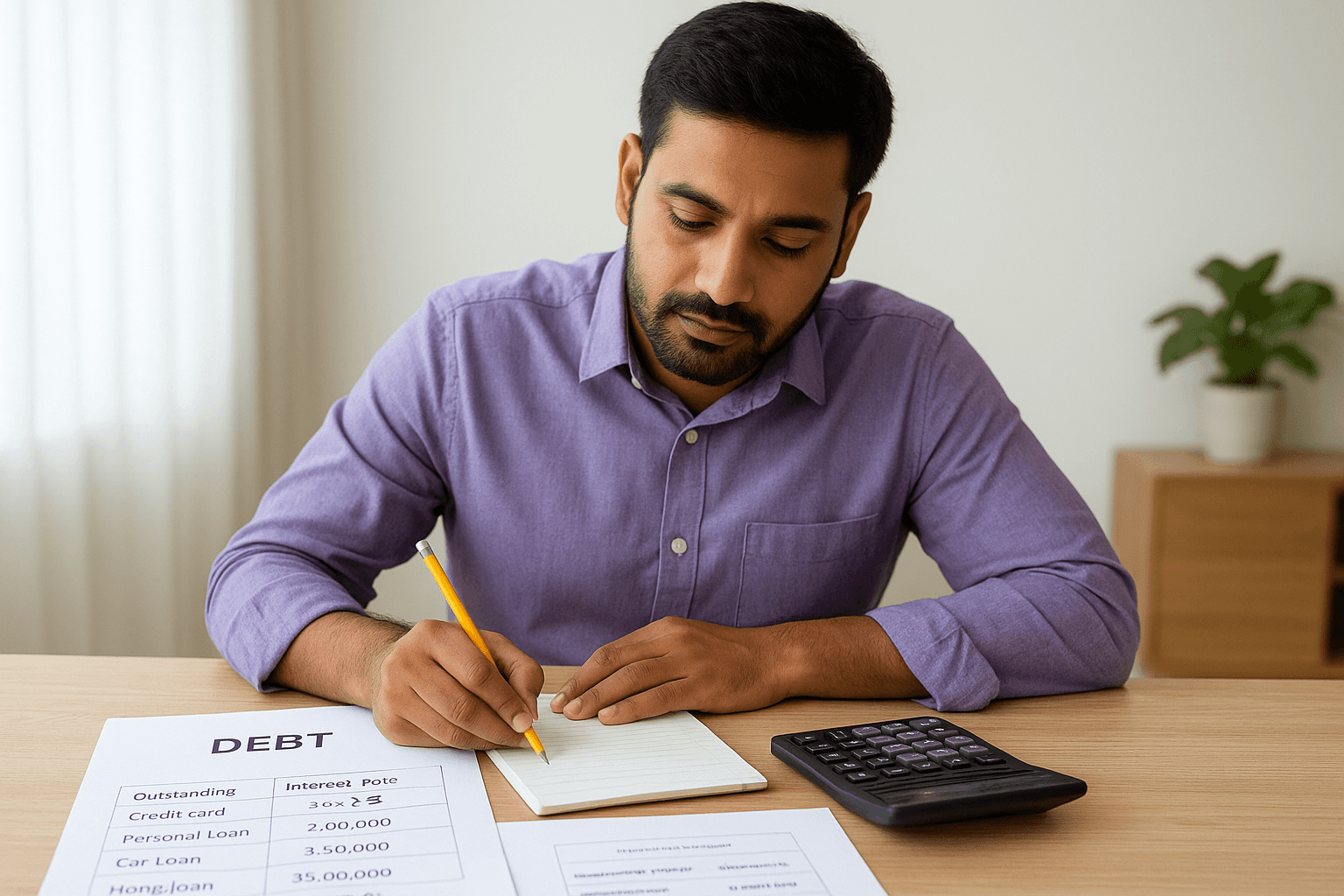

Step 5. Kill expensive debt and improve credit

Carrying expensive debt while trying to build wealth is one of the most common traps in financial planning for beginners India. A personal loan at 15% interest or a credit card balance at 36% annually wipes out any gains you might earn from a mutual fund or a fixed deposit. Before you put serious money into any investment, you need to eliminate high-cost debt systematically, not randomly, using a method that saves you the most in interest charges.

Paying off a 36% credit card balance is the equivalent of earning a guaranteed 36% return on that money; no investment in India comes close to that.

Use the avalanche method to clear debt faster

The avalanche method directs every extra rupee toward the debt with the highest interest rate first, while you pay the minimums on everything else. Once the most expensive debt is cleared, you roll that freed-up payment into the next highest-rate debt. This approach minimizes the total interest you pay across all your loans.

Here is how to apply it to a typical debt stack:

Debt | Outstanding (₹) | Interest Rate | Minimum Payment (₹) | Priority |

|---|---|---|---|---|

Credit card | 80,000 | 36% p.a. | 2,400 | 1 |

Personal loan | 2,00,000 | 16% p.a. | 5,500 | 2 |

Car loan | 3,50,000 | 9% p.a. | 7,200 | 3 |

Home loan | 35,00,000 | 8.5% p.a. | 28,000 | 4 |

Pay minimums on the car and home loans, then direct all surplus cash at the credit card balance until it reaches zero. Then move that payment to the personal loan.

Protect and improve your CIBIL score

Your CIBIL score determines whether a lender approves your home loan, at what interest rate, and on what terms. A score above 750 gives you access to better rates; a score below 650 can cost you several percentage points more across a 20-year loan tenure, which translates to lakhs in additional interest paid.

Three actions have the biggest impact on your score: paying every EMI and credit card bill on or before the due date, keeping your credit card utilization below 30% of your total credit limit, and avoiding multiple loan applications within a short window since each hard inquiry pulls your score down slightly.

Step 6. Start investing for growth, taxes, and retirement

Once you have your emergency fund in place and your expensive debt cleared, investing becomes the most powerful tool in your financial planning for beginners India journey. The goal at this stage isn't to pick the hottest stock or chase the highest short-term return. It's to build a portfolio that grows your wealth, cuts your tax bill, and funds your retirement, all working in parallel from the moment you start.

The longer you stay invested, the more compounding works in your favor; starting five years earlier can mean the difference of several lakhs in your final corpus.

Start with tax-saving investments under Section 80C

Your first investment priority should be filling your Section 80C limit of ₹1.5 lakh per year, because every rupee you invest here reduces your taxable income directly. Your EPF contribution already counts toward this limit, so check your payslip first before adding more instruments. Allocate the remaining room across instruments based on your liquidity needs and risk tolerance:

Instrument | Lock-in Period | Expected Return | Best for |

|---|---|---|---|

ELSS mutual funds | 3 years (shortest among 80C) | 10-14% (market-linked) | Growth-oriented investors |

PPF | 15 years | 7.1% (government-set) | Conservative, guaranteed growth |

NPS (Tier 1) | Until retirement | 8-12% (market-linked) | Additional ₹50,000 deduction under 80CCD(1B) |

For most salaried investors, a combination of ELSS for growth and PPF for stability covers both the tax benefit and the long-term compounding objective without taking unnecessary risk.

Build long-term wealth with SIPs

Beyond Section 80C, Systematic Investment Plans (SIPs) in diversified equity mutual funds are the most accessible way to build serious long-term wealth. You don't need a large lump sum to start. A monthly SIP of even ₹2,000 to ₹5,000 in a large-cap or flexi-cap fund, maintained consistently over 10 to 15 years, builds a corpus that outpaces fixed deposits and savings accounts by a significant margin.

Set up your SIP to auto-debit on your salary credit date, pick a fund with a consistent 5-year and 10-year track record, and increase your SIP amount by at least 10% every year as your salary grows. This one habit, sustained over time, does more for your retirement than any single investment decision you will ever make.

Next steps

You now have a complete framework for financial planning for beginners India: from running your money health check and defining goals to clearing debt, building an emergency buffer, and growing wealth through SIPs and tax-efficient instruments. The steps work in sequence, so resist the urge to skip ahead. Each layer supports the next, and skipping one creates gaps that compound into bigger problems over time.

Start this week with one concrete action. Calculate your net worth using the template in Step 1, identify your single most expensive debt, and set up an auto-transfer to a liquid fund for your emergency savings. Small actions taken consistently do more than a perfect plan that never gets executed.

If you want personalized guidance rather than a self-managed approach, get started with Invsify and let AI-powered, conflict-free advice from a SEBI Registered Investment Advisor help you build and track a plan built around your actual numbers.