Financial Risk Assessment Meaning: Definition, Types, Steps

Shlok Sobti

Financial Risk Assessment Meaning: Definition, Types, Steps

Financial risk assessment is a process that identifies potential threats to your money and investments. It helps you understand what could go wrong with your finances and how likely those events are to happen. Think of it as a health checkup for your wallet. You examine different areas where you might lose money or face financial trouble. The goal is straightforward. Spot problems before they hurt you. Most people skip this step and regret it later.

This article breaks down what financial risk assessment means and why you need it as a salaried professional in India. You'll learn the main types of financial risks that affect your investments and savings. We'll walk through the specific steps to assess your own financial risks. You'll also discover practical tools and real examples you can use starting today. By the end, you'll know how to protect your wealth and make smarter investment decisions with confidence.

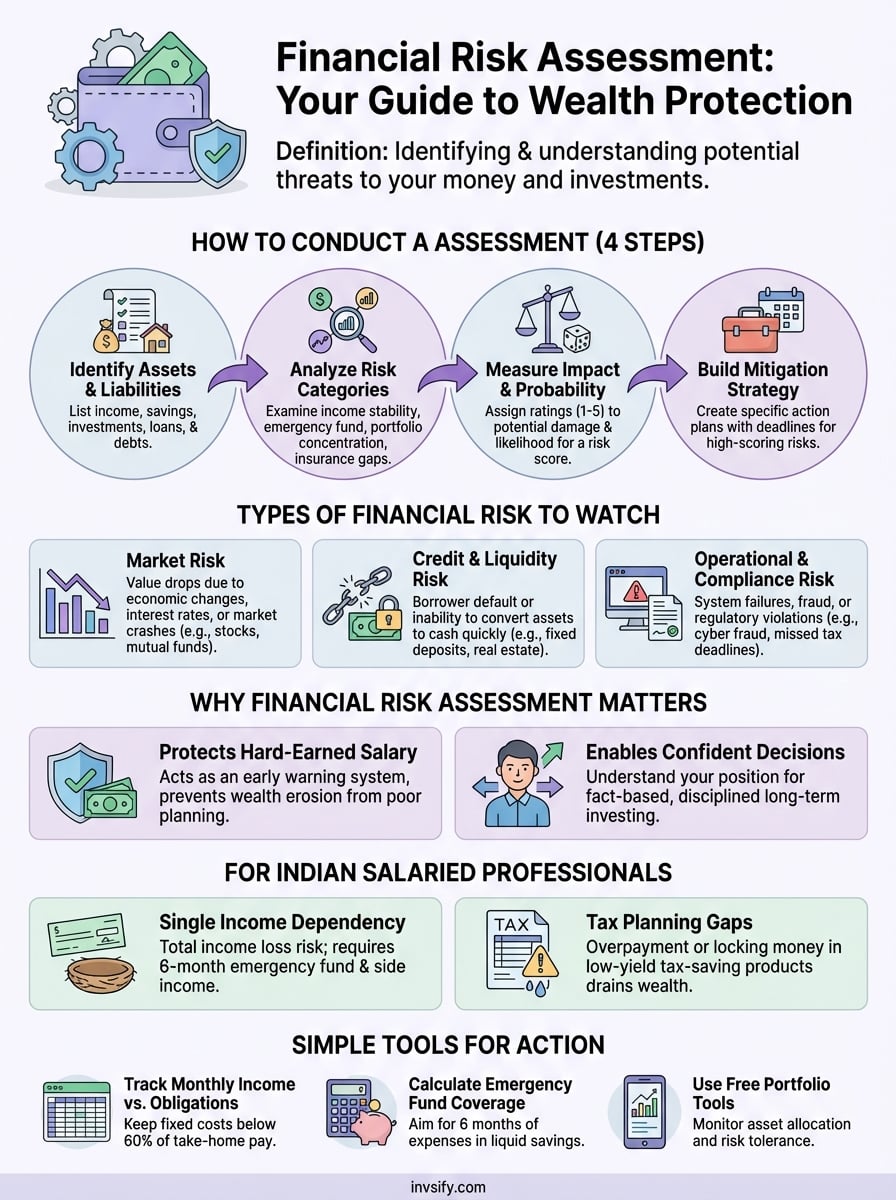

Why financial risk assessment matters

Your financial future depends on understanding where your money might fail you. Without proper risk assessment, you make investment choices based on gut feeling or advice from friends. This approach puts your savings at risk and leaves you vulnerable to market swings, job loss, or unexpected expenses. Most salaried Indians discover their financial weaknesses only after a crisis hits. By then, recovering becomes much harder and more expensive. The financial risk assessment meaning becomes clear when you realize it acts as your early warning system for money problems.

It protects your hard-earned salary

You work too hard to watch your income disappear because of poor planning. Risk assessment shows you exactly where your financial vulnerabilities exist. Maybe you have too much money in one stock. Perhaps your emergency fund won't last three months. Or you might discover that your insurance coverage leaves gaps that could wipe out your family's security. Understanding these risks lets you fix problems before they hurt you. Your salary gives you a chance to build wealth, but only if you protect it systematically.

Regular financial risk assessment turns reactive damage control into proactive wealth protection.

It helps you make confident decisions

Making investment choices becomes easier when you know your risk tolerance and exposure. You stop second-guessing every market movement because you understand your position. Should you invest in that new mutual fund? Your risk assessment gives you the answer based on facts, not fear. This clarity helps you sleep better at night. You also avoid the common mistake of pulling out of investments at the wrong time. Smart investors use risk assessment to stay disciplined and focused on long-term goals despite short-term market noise.

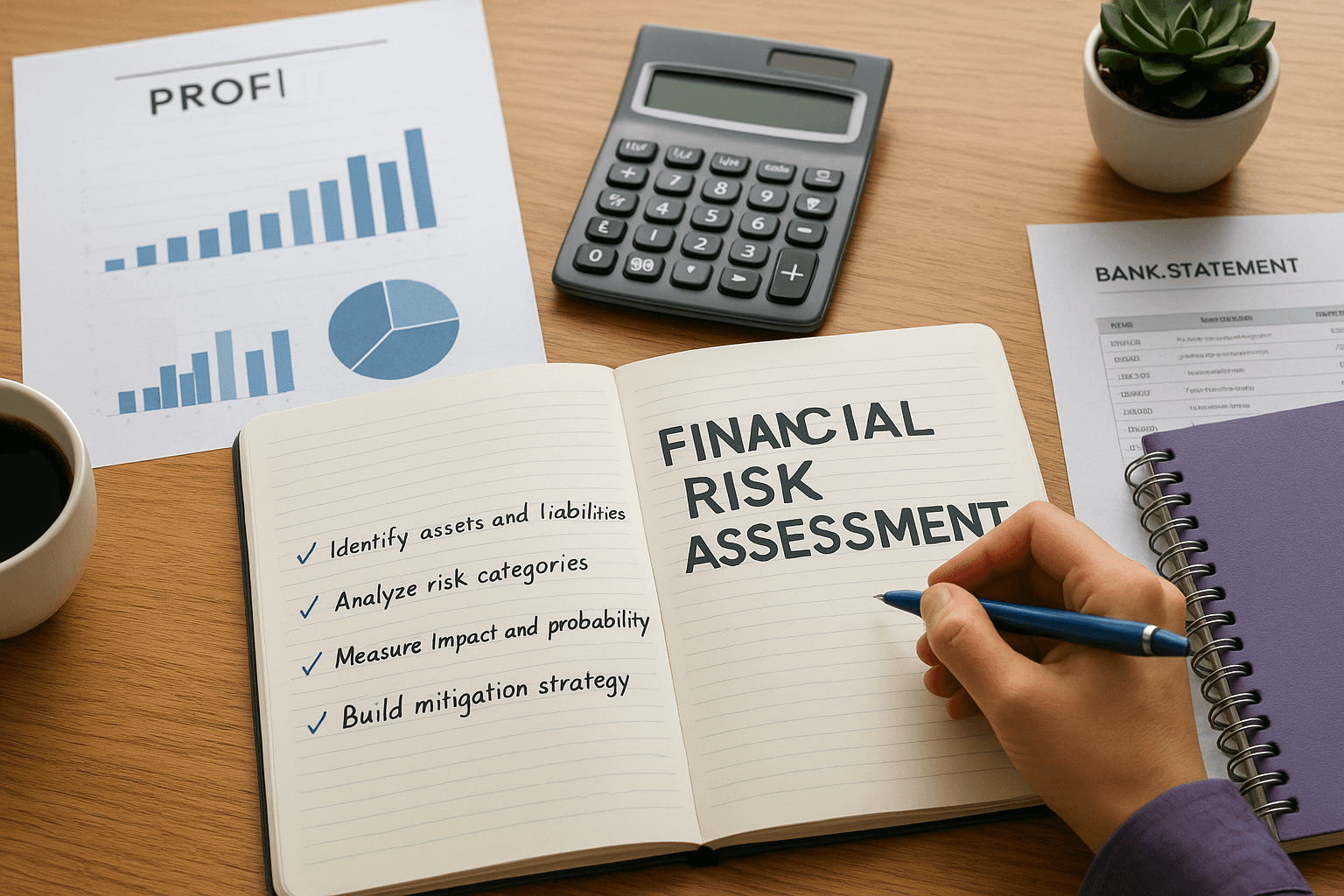

How to conduct a financial risk assessment

Conducting a financial risk assessment requires a structured approach that examines your complete financial picture. You need to look at everything from your monthly income to your long-term investments. The financial risk assessment meaning becomes practical when you apply specific steps to your own situation. Most people feel overwhelmed at first, but breaking the process into clear stages makes it manageable. Start by setting aside two hours when you can focus without interruptions. Gather your bank statements, investment documents, insurance policies, and loan papers before you begin.

Identify all your financial assets and liabilities

List every source of income you receive each month. Include your salary, rental income, bonuses, and any side hustle earnings. Write down the exact amounts and note which ones are guaranteed versus variable. Next, document all your assets such as savings accounts, fixed deposits, mutual funds, stocks, real estate, and EPF balance. Be thorough because missing items creates blind spots in your assessment. Then list every liability including home loans, personal loans, credit card debt, and money you owe to family or friends. Calculate your net worth by subtracting total liabilities from total assets. This snapshot shows you where you stand financially right now.

Analyze each risk category systematically

Work through different risk types one by one to understand your vulnerability levels. Check your income stability first by asking what happens if you lose your job tomorrow. Look at your emergency fund and determine if it covers six months of expenses. Examine your investment portfolio for concentration risk by calculating what percentage sits in single stocks or sectors. Review your insurance coverage to spot gaps that could bankrupt you during medical emergencies or accidents. Assess your debt burden by comparing monthly EMI payments against your take-home salary. Calculate if you can handle a 25% income drop without defaulting on obligations.

A systematic risk analysis reveals hidden vulnerabilities that random financial reviews always miss.

Measure the impact and probability

Assign ratings to each risk you identified based on potential damage and likelihood. Use a simple scale from 1 to 5 where 5 means catastrophic impact or very high probability. A job loss might rate 4 for impact and 2 for probability. Inadequate health insurance could score 5 for impact and 3 for probability. Multiply these numbers to get a risk priority score for each item. This calculation helps you focus on the biggest threats first. Your goal is not to eliminate every risk, but to manage the ones that could seriously harm your financial security.

Build your risk mitigation strategy

Take the highest scoring risks from your assessment and create specific action steps to reduce them. If emergency funds scored high, set up automatic transfers to build that cushion within six months. When investment concentration appears risky, plan to diversify across asset classes over the next quarter. For insurance gaps, research policies and get quotes within two weeks. Schedule these actions in your calendar with deadlines. Review your complete risk assessment every six months because your financial situation keeps changing. Update your strategy as you achieve milestones or face new circumstances.

Types of financial risk to watch

Understanding the financial risk assessment meaning requires knowing the specific categories of risks that threaten your wealth. Each type of risk operates differently and demands unique mitigation strategies. You face multiple risk categories simultaneously, and ignoring any single type leaves dangerous gaps in your financial defense. Indian salaried professionals encounter all these risks through their investments, loans, and daily financial activities. The key is recognizing which risks apply to your situation and monitoring them regularly. Some risks hit you suddenly while others erode your wealth slowly over months or years.

Market risk affects your investments daily

Market risk describes the possibility of losing money when investment values drop because of economic changes, interest rate movements, or stock market crashes. Your mutual fund portfolio faces this risk every single day the markets open. When the Nifty or Sensex falls 10%, your equity investments lose value immediately. Currency fluctuations create market risk too, especially if you hold international investments or foreign stocks. Interest rate changes by the Reserve Bank of India impact your bond funds and fixed-income securities directly. You cannot eliminate market risk completely, but diversification across asset classes reduces the damage. Real estate investments face market risk when property values decline in your locality or across cities.

Market risk punishes concentrated portfolios during downturns but rewards those who diversify intelligently across sectors and asset classes.

Credit and liquidity risks threaten cash flow

Credit risk appears when borrowers fail to repay money they owe you or when your investment counterparties default. Fixed deposits with weak banks carry credit risk if those institutions fail. Corporate bonds expose you to credit risk because companies might default on interest payments or principal repayment. Your personal lending to friends or family involves significant credit risk that most people underestimate badly. Liquidity risk strikes when you cannot convert your assets into cash quickly without heavy losses. Real estate holds the highest liquidity risk among common investments because selling property takes months. Some mutual funds with lock-in periods trap your money when you need it urgently. Emergency expenses become crises when all your money sits in illiquid investments you cannot access.

Operational and compliance risks lurk in the background

Operational risk emerges from failures in your financial processes, systems, or service providers. Banking errors, fraudulent transactions, or investment platform crashes create operational losses. Identity theft and cyber fraud represent growing operational risks for digital investors. Your financial advisor making unauthorized transactions falls under operational risk too. Compliance risk happens when you violate financial regulations or tax laws unintentionally. Missing tax filing deadlines, underreporting income, or misusing tax-saving instruments creates compliance problems. Penalties and legal issues from non-compliance drain your wealth and create stress. Poor record keeping increases both operational and compliance risks because you cannot track transactions or prove your financial activities during audits.

Simple examples and tools you can use

Applying the financial risk assessment meaning to your life becomes easier when you see real examples and use simple tools. You don't need expensive software or financial degrees to protect your wealth. Start with basic spreadsheets and free calculators that show exactly where your money sits vulnerable. Most people complicate risk assessment unnecessarily, but effective protection comes from consistent tracking rather than complex formulas. These examples show you how ordinary salaried professionals assess their risks and make improvements within weeks.

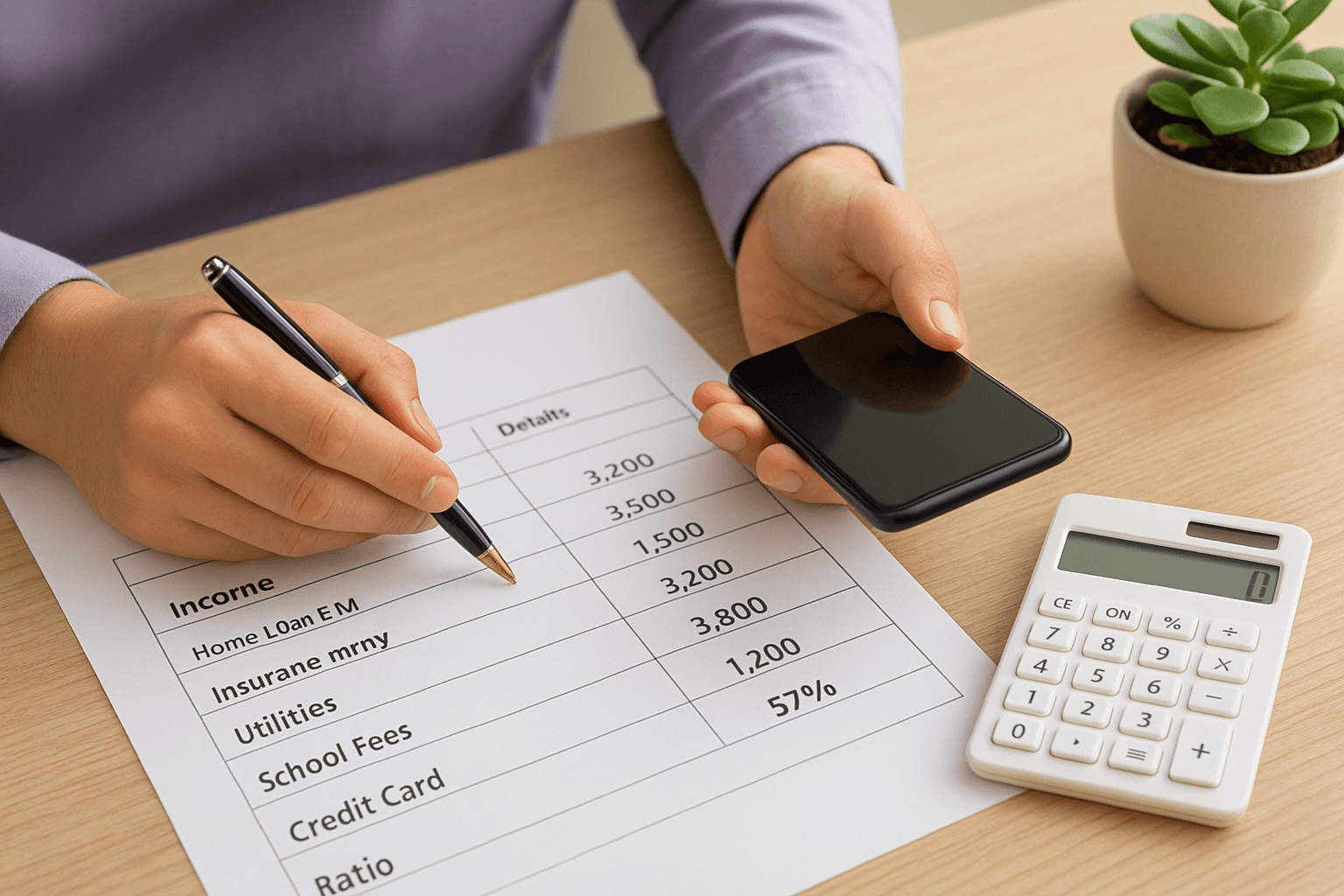

Track monthly income versus fixed obligations

Create a simple spreadsheet listing your salary and every mandatory payment you make. Include your home loan EMI, insurance premiums, utility bills, school fees, and credit card minimum payments. Add up these fixed costs and divide by your monthly take-home pay. If this ratio exceeds 60%, you face serious cash flow risk. One salary delay or unexpected expense pushes you into debt. Reduce this ratio by prepaying high-interest loans or cutting discretionary subscriptions. Update this sheet every month to catch problems early.

Simple monthly tracking reveals cash flow vulnerabilities that annual reviews always miss.

Calculate your emergency fund coverage

Take your average monthly expenses and multiply by six to get your target emergency fund. Now check your actual savings account balance and liquid mutual funds. Divide your current savings by your monthly expenses to see how many months you can survive without income. Most Indians score below three months, which creates dangerous exposure. Build this fund systematically by saving 20% of each salary increment until you hit six months of coverage.

Use free portfolio tracking tools

Many investment platforms offer free portfolio analysis features that calculate your asset allocation automatically. Google Sheets provides templates for tracking investments across multiple accounts in one place. Log into your mutual fund, EPF, and stock accounts monthly to update your portfolio value. Check if your equity exposure matches your age-based risk tolerance. These free tools prevent you from discovering concentration risk only after markets crash.

Financial risk assessment for Indian salaried people

Indian salaried professionals face unique financial risks that differ from other countries and employment types. Your provident fund contributions, tax-saving investments, and family obligations create specific vulnerabilities that generic risk assessments miss. Most salaried Indians depend entirely on one monthly paycheck while supporting parents, children, and extended family members. This situation demands a customized risk framework that accounts for Indian market conditions, regulatory requirements, and cultural financial expectations. The financial risk assessment meaning takes on practical importance when you apply it to your actual salary structure, EPF balance, and tax obligations under Indian laws.

Single income dependency multiplies every risk

Relying on one salary makes you extremely vulnerable when that income stream stops or reduces. Unlike business owners with multiple revenue sources, you face total income loss if your employer terminates you or your company shuts down. Your emergency fund becomes critical because job searches in India take three to six months on average. Calculate your family's monthly burn rate including EMIs, school fees, medical expenses, and household costs. Build liquid savings equal to at least six months of this burn rate before making aggressive investments. Consider developing side income through consulting or freelancing to reduce single-source dependency.

Tax planning gaps drain wealth silently

Poor tax planning creates unnecessary losses that compound over years. Many salaried Indians overpay taxes by not optimizing deductions under Section 80C, 80D, and HRA exemptions properly. Others invest in tax-saving instruments without checking returns, locking money into low-yield products for years. Review your Form 16 and ITR every year to spot missed deductions. Compare the actual returns from your tax-saving investments against inflation and opportunity costs.

Single income dependency and tax inefficiency together create the biggest wealth destruction for Indian salaried professionals.

Key takeaways

Understanding the financial risk assessment meaning gives you power to protect your wealth systematically. You learned that risk assessment identifies threats before they damage your finances and helps you make confident investment decisions. The process involves identifying assets and liabilities, analyzing risk categories, measuring impact probability, and building mitigation strategies. Indian salaried professionals face specific challenges including single income dependency and tax planning gaps that require focused attention.

Start your assessment today by tracking monthly obligations versus income and calculating emergency fund coverage. Review each risk type affecting your investments and savings. Regular assessment every six months keeps you protected as your financial situation evolves. Get personalized AI-powered financial guidance that helps you identify risks specific to your salary structure and investment portfolio. Take control of your financial future by acting on the steps outlined in this article within the next week.