Goal Based Investment Planning: Steps, Tools, And Examples

Shlok Sobti

Goal Based Investment Planning: Steps, Tools, And Examples

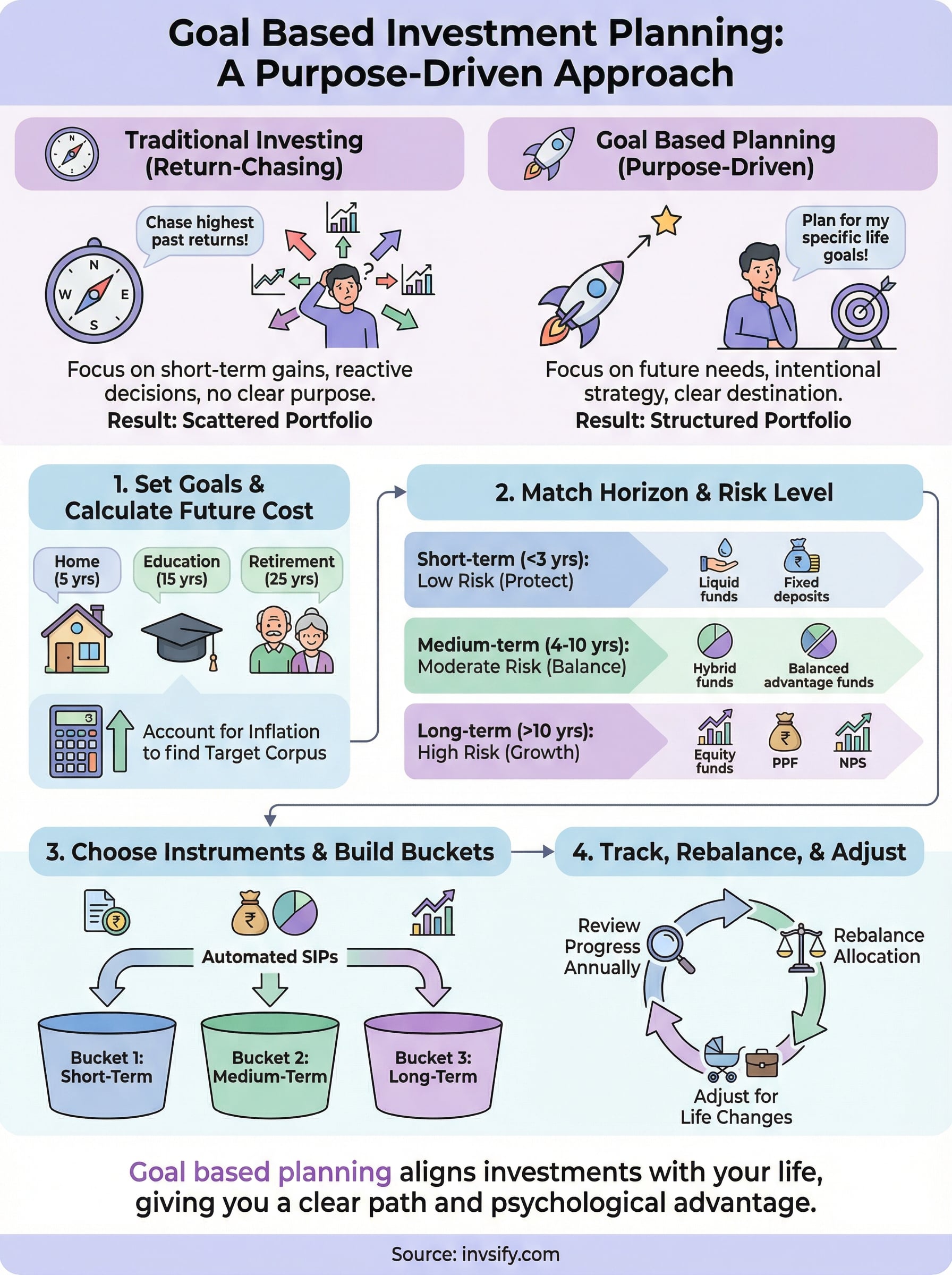

Most people invest without a clear destination. They pick mutual funds because a colleague recommended them, start SIPs because it feels responsible, or chase returns because a YouTube video told them to. The result? A scattered portfolio that doesn't actually move the needle on anything specific. Goal based investment planning flips this approach, it starts with what you want your money to do, then works backward to build a strategy around it.

Whether it's buying a home in five years, funding your child's education in fifteen, or retiring at 50, every financial goal has a timeline, a target amount, and a risk profile attached to it. Matching your investments to these specifics changes everything, from which instruments you choose to how much you need to invest each month. It removes the guesswork and replaces it with structure.

This article breaks down what goal-based investment planning actually means, how it differs from traditional investing, and walks you through a clear step-by-step process to implement it, with real examples, tools, and calculators. At Invsify, as a SEBI Registered Investment Advisor, we use AI-powered insights to help Indian investors plan their wealth around life goals instead of hunches. That perspective shapes everything you'll read here.

Why goal-based planning beats return-chasing

Most investors spend enormous energy tracking which fund gave 18% last year or which stock analyst is bullish on a sector. But return-chasing has a fundamental flaw: it treats investing as a game to win rather than a tool to serve your life. When you focus purely on returns, you make reactive decisions, jump between funds, and end up with a portfolio that looks busy but serves no clear purpose. Goal based investment planning works differently. It anchors every decision to a specific outcome you actually need, which changes how you choose, hold, and rebalance your investments.

The problem with chasing returns

Return-chasing feels rational on the surface. You want your money to grow as fast as possible, so you follow the best-performing funds. But past performance does not reliably predict future results, and most retail investors learn this the hard way. Studies consistently show that investors who switch funds frequently based on recent performance end up with lower actual returns than those who stayed with a consistent strategy. Frequent switching also increases your tax liability through short-term capital gains and creates behavioral traps like panic-selling during market corrections.

The deeper issue is that a high return means nothing without context. A 15% return on a fund you don't need for 20 years is far less urgent than a 6% shortfall on the corpus you need in three years for your child's college admission fees. Without goals, you have no way to measure whether your investing is actually working. You end up optimizing for a number that has no connection to your real life.

Without a destination, any return feels like progress, even when it isn't moving you forward.

How goal-based planning gives you a clear target

When you plan around goals, every investment decision has a reason behind it. You know exactly how much money you need, when you need it, and what rate of return is required to get there. This clarity fundamentally changes how you respond to market volatility. A 10% market correction doesn't send you scrambling when you know your retirement corpus is 25 years away and your equity funds have plenty of time to recover. You stop reacting to short-term noise because your plan already accounts for it.

Planning this way also forces you to prioritize. You might discover that you can't fully fund three goals simultaneously at your current income level. That is not a failure. Knowing the gap early gives you time to adjust, whether that means increasing your monthly SIP, extending your timeline, or scaling down a lower-priority goal. Without this structure, you'd only discover the shortfall when it's far too late to correct course.

The psychological advantage of planning with purpose

Money without meaning is hard to protect. Investors who tie their portfolios to specific goals stay invested longer and make far fewer impulsive decisions. When you know a particular SIP is building toward your child's education or your own early retirement, withdrawing it during a rough quarter feels like abandoning something real. That emotional anchor is a genuine behavioral advantage that has nothing to do with willpower and everything to do with clarity.

Your mindset also shifts when you measure progress differently. Instead of asking "did my portfolio go up this month?", you start asking "am I on track to hit my target in the time I have?" Those are very different questions, and the second one is the only one that actually matters. At Invsify, the Wealth Wellness Score reflects exactly this, not just returns, but how well your current portfolio is positioned to meet each of your actual financial goals on time.

Set goals and calculate the future cost

The first real step in goal based investment planning is to move from vague intentions to specific, numbered targets. "I want to retire comfortably" is not a goal. "I need Rs. 5 crore by age 55" is. That specificity is what lets you reverse-engineer a monthly investment amount, choose the right instruments, and measure whether you're actually on track at any point in time. Without a concrete number attached to each goal, every investment decision you make is essentially a guess dressed up as a strategy.

Name each goal and give it a number

Start by listing every financial goal you're working toward, then group them by priority. Essential goals like retirement and your child's education sit at the top, followed by important goals like a home down payment, and then lifestyle goals like international travel or a car upgrade. Once you have your list, assign a rough current cost to each one and write down the year you'll need the money.

Here's a simple starting framework:

Goal | Current Cost Estimate | Timeline |

|---|---|---|

Child's higher education | Rs. 20 lakh | 14 years |

Home purchase (down payment) | Rs. 30 lakh | 6 years |

Retirement corpus | Rs. 2 crore | 25 years |

International vacation | Rs. 5 lakh | 3 years |

This table is not your final plan, it is your starting point. The current cost figure tells you what something costs today, and your next task is to calculate what it will actually cost at the exact time you need it.

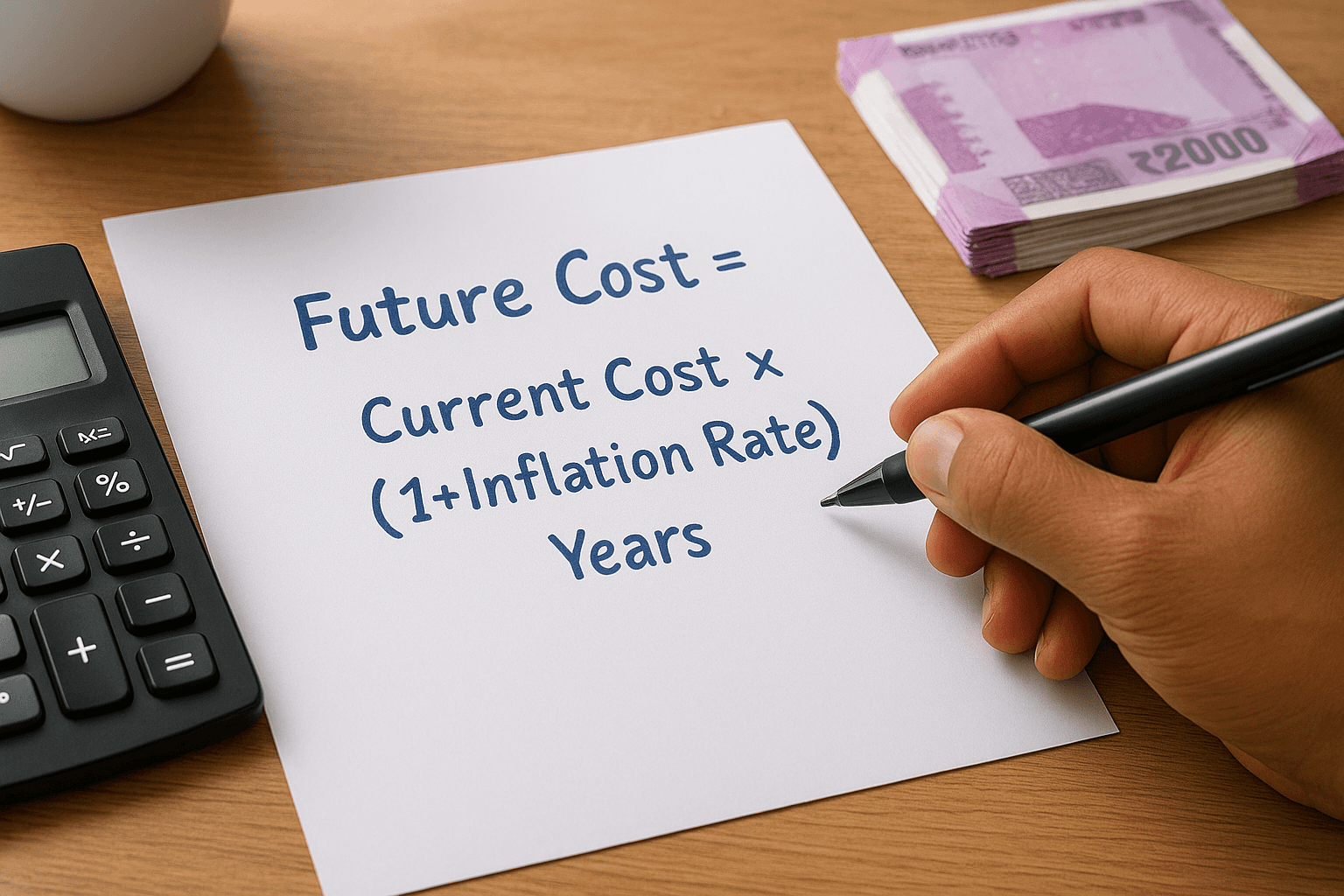

Account for inflation when you calculate the target

Prices do not stay flat over time. A college education that costs Rs. 20 lakh today will cost significantly more in fourteen years. Inflation erodes purchasing power year after year, and if you ignore it when setting your corpus target, you will undershoot and face a shortfall at exactly the moment you cannot afford one.

The formula to calculate the future cost of any goal is straightforward:

Future Value = Current Cost x (1 + Inflation Rate)^Years

For example, Rs. 20 lakh growing at 6% annual inflation over 14 years becomes approximately Rs. 45 lakh. That inflated figure is the number you actually need to target. Once you have it, you can use an SIP calculator to determine how much you need to invest each month, based on a realistic expected return for the appropriate asset class.

The single most common planning mistake is building a strategy around today's prices instead of tomorrow's.

Match each goal to a time horizon and risk level

Once you have a number attached to each goal, the next task is to figure out how much risk you can actually afford to take in pursuit of it. Time horizon is the single biggest factor that determines your risk capacity, not your personality, not your income, and not how calm you feel when markets drop. A goal three years away and a goal twenty-five years away require fundamentally different strategies, even if the target amounts are similar. This matching step is where goal based investment planning separates itself from generic portfolio-building advice.

Your risk level should be set by your deadline, not by how optimistic you feel on any given day.

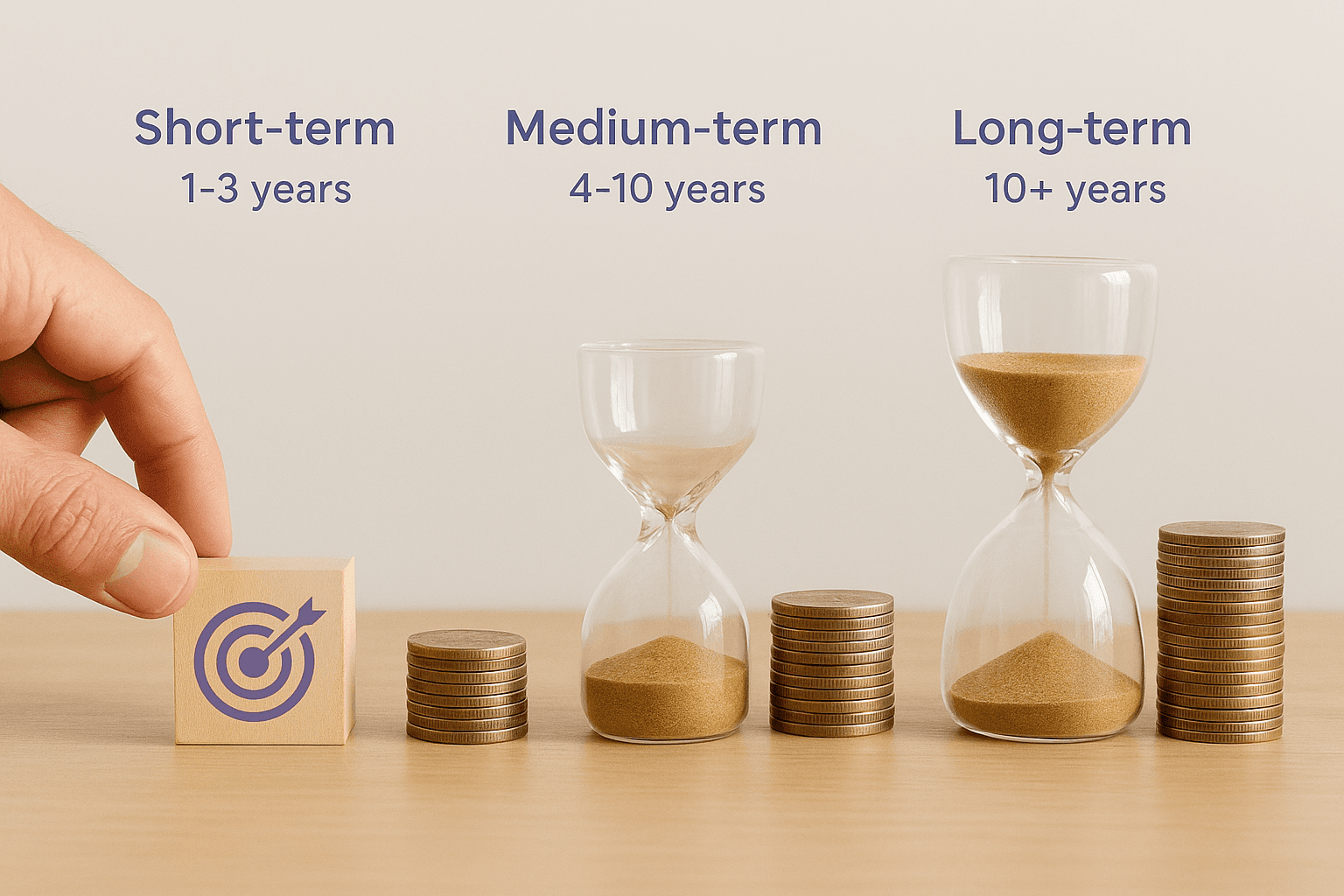

Short-term goals: protect what you'll need soon

Short-term goals are anything you need funded within one to three years. Because the timeline is tight, you cannot afford significant drawdowns, even temporary ones. A 30% market correction that recovers in three years is manageable for a retirement fund. For a home down payment you need in eighteen months, that same correction could derail your entire plan.

For these goals, capital preservation matters more than growth. Liquid mutual funds, short-duration debt funds, and high-yield savings instruments are appropriate here. The expected return will be modest, typically in the 5% to 7% range, but that is acceptable because the goal of this bucket is not to grow aggressively. It is to make sure the money is there when you need it, in full.

Medium-term goals: balance growth with stability

Medium-term goals sit in the four to ten year window. This timeline gives you enough room to absorb some volatility, but not enough to fully recover from a prolonged downturn in a purely equity-heavy portfolio. A balanced or hybrid approach works best here, mixing equity mutual funds with debt instruments in a ratio that reflects both the timeline and the amount still needed.

Balanced advantage funds and hybrid funds are practical choices for this bucket because they dynamically adjust their equity-to-debt ratio based on market valuations. As your goal moves closer to its deadline, you should gradually shift the allocation away from equity, a process called lifecycle rebalancing. Start with 60% equity if you have eight years to go, and reduce that exposure progressively as you approach year four.

Long-term goals: let equity work over time

Long-term goals with timelines of ten years or more are where equity should do most of the work. Over long periods, equity as an asset class consistently outperforms inflation and debt instruments, and the volatility that feels dangerous in the short term becomes irrelevant when you have decades for compounding to work. Retirement planning is the clearest example of a goal that belongs almost entirely in equity for the first fifteen to twenty years.

Diversified equity funds, index funds tracking the Nifty 50 or Nifty 500, and small-cap allocations for higher-risk appetite all make sense here. The key discipline for long-term buckets is to avoid touching them during market downturns. Staying invested through corrections is not passive, it is the active, intentional choice that makes long-term wealth building work.

Choose the right investment options in India

Once you've matched each goal to a timeline and risk level, you need to select the actual instruments that will carry each goal forward. India's investment landscape has expanded significantly, and salaried investors today have access to a wide range of regulated options, from index funds to government-backed schemes. The key is not to pick the ones with the best recent returns but to pick the ones that fit the risk profile and timeline you've already established for each goal.

Equity instruments for growth-oriented goals

For long-term goals, equity mutual funds are the workhorse of most well-structured plans in India. Diversified large-cap and flexi-cap funds give you broad market exposure with lower concentration risk than picking individual stocks. Index funds tracking benchmarks like the Nifty 50 or Nifty 500 offer low-cost, passive exposure to India's market growth and are an excellent core holding for any goal ten or more years away. For investors with higher risk tolerance and very long timelines, adding a mid-cap or small-cap fund can boost long-term compounding.

Equity is not inherently risky for long-term goals. It becomes risky only when you treat a long-term instrument as a short-term one.

Direct equity investing through individual stocks requires significant research and active monitoring, which makes it unsuitable for most salaried individuals using goal based investment planning as a structured framework. Sticking to mutual funds keeps the approach manageable and well-diversified without demanding constant attention from you.

Debt and hybrid instruments for shorter timelines

Debt mutual funds, PPF, and fixed deposits serve different functions depending on your goal's timeline and the level of liquidity you need. For goals under three years, liquid funds and short-duration debt funds let you earn returns above a savings account while keeping your capital accessible and relatively stable. For medium-term goals, hybrid funds that blend equity and debt provide built-in rebalancing and reduce single-asset-class concentration.

PPF deserves special mention for long-term, tax-efficient savings. The 15-year lock-in period aligns naturally with retirement or education planning, and the EEE tax status, exempt at contribution, growth, and withdrawal, makes it one of the most efficient instruments available to Indian investors. NPS is another strong option for retirement, offering both equity and debt allocation with additional tax benefits under Section 80CCD(1B). Neither requires active management from you, which keeps long-term execution simple and consistent.

Build your plan using SIPs, buckets, and automation

Knowing what to invest in is only half the job. The other half is building a system that runs consistently, even when markets are volatile, your income changes, or life gets busy. This is where the structure of goal based investment planning becomes practical: you organize your investments into distinct buckets, set up systematic investment plans (SIPs) for each one, and automate contributions so the plan executes with minimal manual effort from you every month.

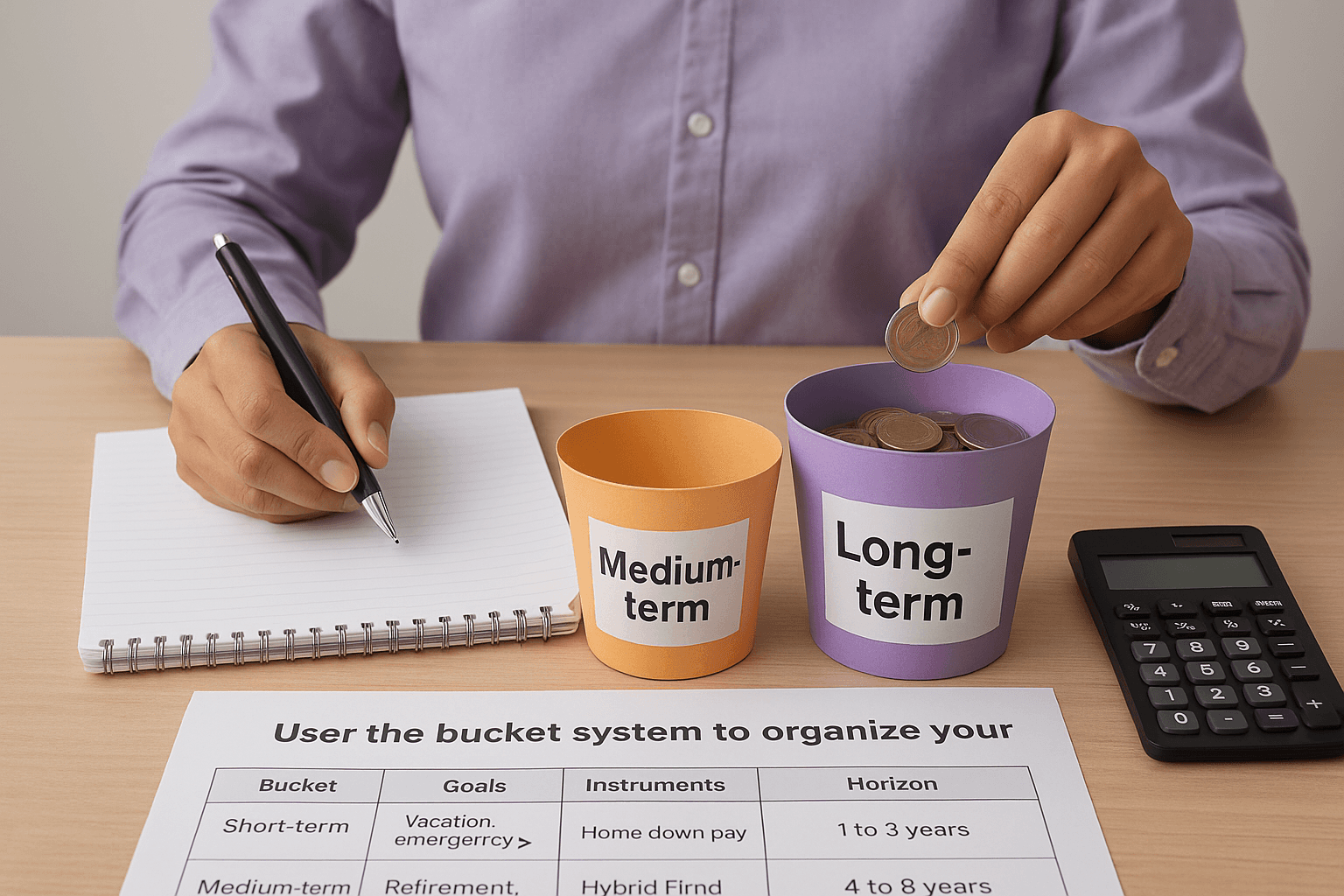

Use the bucket system to organize your goals

The bucket approach means each goal gets its own dedicated pool of investments, separate from every other goal. Your child's education fund does not mix with your retirement corpus, and your short-term vacation fund stays completely separate from your home down payment bucket. This separation gives you a clear picture of where you stand on each goal independently, so a shortfall in one bucket doesn't obscure progress in another.

Here's how a simple three-bucket structure might look for a salaried investor:

Bucket | Goals | Instruments | Horizon |

|---|---|---|---|

Short-term | Vacation, emergency buffer top-up | Liquid funds, short-duration debt | 1 to 3 years |

Medium-term | Home down payment | Hybrid funds, balanced advantage funds | 4 to 8 years |

Long-term | Retirement, child's education | Equity mutual funds, PPF, NPS | 10+ years |

Mixing goals into a single undifferentiated portfolio is one of the fastest ways to lose track of whether any specific goal is actually on track.

Set up a dedicated SIP for each bucket

Once your buckets are defined, assign a specific SIP amount to each one based on the monthly investment figure your inflation-adjusted corpus calculation produced. Each SIP should draw from your salary account on a fixed date, ideally within two to three days of your pay credit. Running separate SIPs rather than one lump SIP into a general fund keeps your tracking clean and prevents you from accidentally drawing down a long-term investment when a short-term need arises.

Review the SIP amount for each goal at least once a year. As your income grows, increasing your SIP by even 10% annually compounds your corpus significantly over long timelines, often closing gaps before they become problems.

Automate to remove friction and bias

Manual investing introduces two problems: you might forget, or you might talk yourself out of it during a bad market month. Automation removes both. Most fund platforms and banks in India allow you to set standing instructions that move money into specific fund folios on a scheduled date without any action from you.

Treat your SIPs as non-negotiable fixed expenses, the same way you treat rent or an EMI. When investing becomes automatic, it stops competing with discretionary spending decisions, and your plan stays on track regardless of how you feel about the market on any given day.

Track progress, rebalance, and handle life changes

Building your plan is the start, not the finish. Goal based investment planning only works if you review it regularly, because markets move, your income shifts, and life circumstances rarely stay static. A plan you set up two years ago and never revisited is not a plan. It is a starting point that has quietly drifted off course.

Review your goal progress at least once a year

Set a fixed annual review date, your birthday, the start of the financial year, whichever date you will actually keep. On that date, check how much each bucket has grown against the trajectory it needs to reach your inflation-adjusted target on time. Most fund platforms in India show your current corpus value; compare that figure against where you should be by now based on the SIP calculator math you did when you set each goal.

If a bucket is ahead of schedule, you may reduce its SIP slightly and redirect that amount toward a lagging goal. If a bucket is behind, identify the cause, whether it is underperformance, missed contributions, or an original assumption that no longer holds, and adjust before the gap becomes unrecoverable.

The annual review is the single most important habit that separates investors who hit their goals from those who miss them by a margin they never saw coming.

Rebalance when your allocation drifts

Markets shift your asset allocation over time without you doing anything. A portfolio that started at 70% equity and 30% debt may sit at 85% equity after a strong bull run, taking on more risk than your goal's timeline actually warrants. Rebalancing means selling a portion of the over-weighted asset class and moving it into the under-weighted one to restore your original target allocation.

Rebalance annually or whenever any asset class drifts more than 10 percentage points from its target. In India, factor in the tax implications of redeeming units, since short-term capital gains on equity held under a year attract higher rates than long-term gains. Timing your rebalance thoughtfully reduces the tax drag on your returns.

Adjust when life changes your goals

A promotion, a new child, a medical expense, or a shift in your retirement timeline can make your original plan obsolete overnight. When a major life event happens, revisit your goal list and update both the target corpus and the timeline for every affected goal. Some goals will rise in priority, others may drop entirely.

Treat your plan as a living document that reflects your current reality, not a contract you signed once and must honor at any cost. Updating it when life changes is not a failure. It is exactly what responsible, structured investing looks like over the long run.

Next steps to get your plan in motion

Goal based investment planning is not a one-time exercise you complete and shelve. It is an ongoing system that connects every rupee you invest to something specific and meaningful in your life. You now have the full framework: setting inflation-adjusted targets, matching goals to the right risk level, choosing instruments that fit each timeline, building separate buckets with automated SIPs, and reviewing your progress every year.

The next practical step is to sit down with your actual numbers. List your goals, assign a current cost and a deadline to each one, and run the inflation-adjusted calculation to find out what you truly need to accumulate. That number will likely surprise you, and that surprise is exactly why starting early and staying structured matters more than chasing returns.

If you want a data-backed starting point built around your real goals, get started with Invsify and let AI-powered advisory do the heavy lifting for you.