Groww Retirement Calculator: How To Estimate Your Corpus

Shlok Sobti

Groww Retirement Calculator: How To Estimate Your Corpus

Retirement might feel distant when you're in your 20s or 30s, but the numbers don't lie, starting early makes a massive difference in how comfortably you'll live later. The challenge? Figuring out exactly how much you need to save each month to build a corpus that beats inflation and sustains your lifestyle for decades.

That's where the Groww retirement calculator comes in handy. This free online tool helps you estimate your retirement corpus based on your current age, expected retirement age, monthly expenses, and anticipated returns. It takes the guesswork out of planning and gives you a concrete savings target to work toward.

But here's the thing, a calculator gives you numbers, not strategy. At Invsify, we combine AI-powered insights with SEBI-registered advisory expertise to help you actually build toward those numbers with conflict-free, transparent investment recommendations. Whether you're just starting your retirement planning journey or refining an existing strategy, understanding how to use tools like Groww's calculator is the first step.

This guide walks you through how the Groww retirement calculator works, what inputs you need, how to interpret your results, and where its limitations lie. By the end, you'll know exactly how to estimate your retirement corpus, and what to do next with that information.

What the Groww retirement calculator does

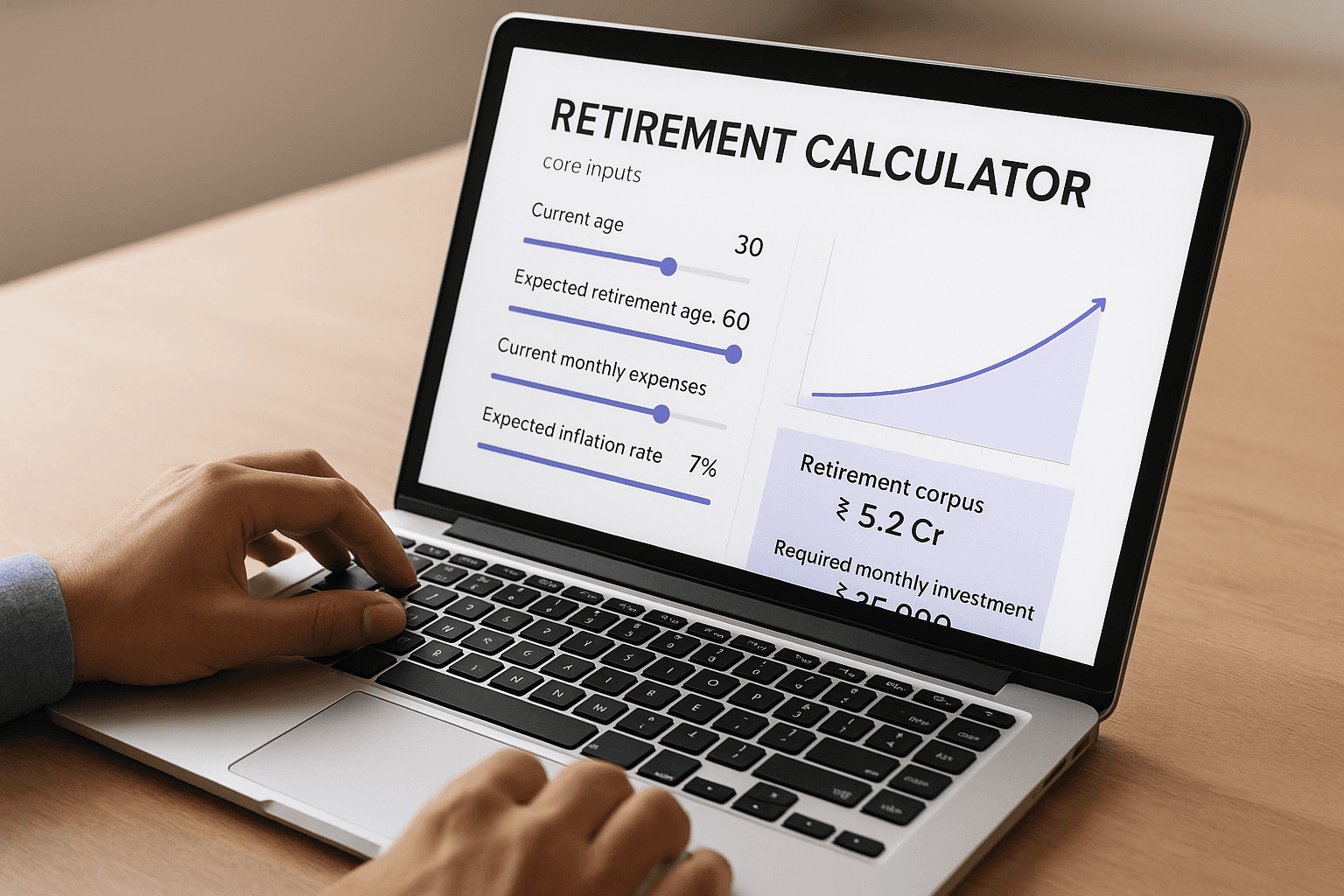

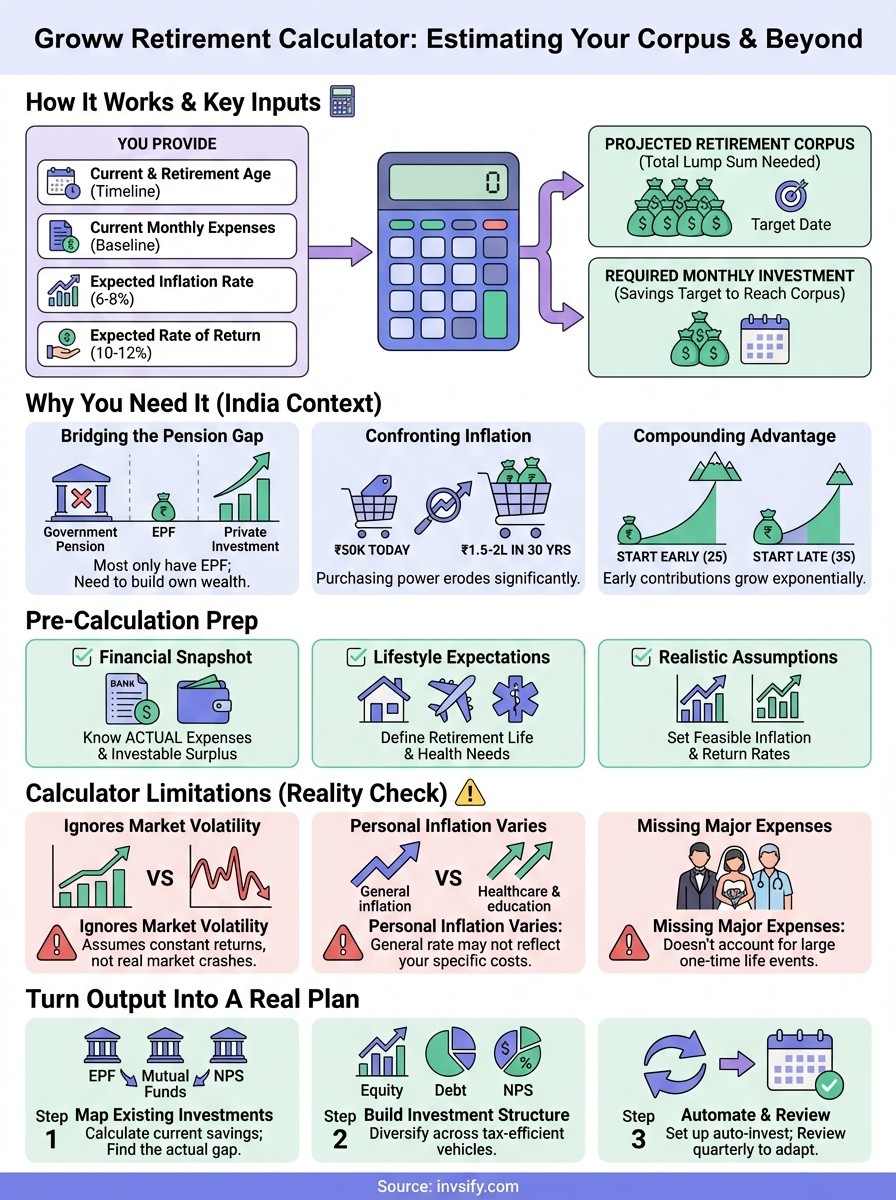

The Groww retirement calculator is a free web-based tool that helps you estimate the lump sum you'll need at retirement and the monthly savings required to reach that target. You plug in basic details like your current age, expected retirement age, current monthly expenses, and anticipated inflation rate. The tool then runs the numbers and shows you a projected corpus along with a suggested monthly investment amount.

Core inputs the calculator asks for

The calculator needs five primary inputs from you to generate meaningful results. First, it asks for your current age and your expected retirement age, which establishes your investment timeline. A 25-year-old planning to retire at 60 has 35 years to build wealth, while a 45-year-old has just 15 years. That difference dramatically affects how aggressively you need to save.

Next, you'll input your current monthly expenses in today's terms. The calculator uses this as a baseline for what you'll need during retirement. If you spend ₹50,000 per month today, the tool assumes you'll need roughly the same purchasing power when you retire, adjusted for inflation over the years.

The third critical input is the expected inflation rate, typically set between 6% and 8% for India. Inflation erodes purchasing power, so ₹50,000 today won't buy the same things in 30 years. The calculator factors this in when projecting your future corpus needs.

Finally, you'll enter your expected rate of return on investments. Most calculators default to around 10-12% annually, reflecting historical equity market returns. This assumption directly impacts how much you need to invest monthly, higher expected returns mean lower monthly contributions.

What it calculates for you

Once you feed in those inputs, the calculator generates two key outputs. The first is your retirement corpus, the total amount you'll need saved by retirement day. This number accounts for inflation-adjusted monthly expenses multiplied by the years you expect to live post-retirement, usually around 25-30 years.

The second output is your required monthly investment, the amount you need to set aside each month to reach that corpus. The calculator assumes you'll invest this amount consistently, earning your expected rate of return compounded annually. If you're 30 and need ₹5 crores at 60, the tool might suggest investing ₹25,000 per month at 12% returns.

The calculator gives you a snapshot based on assumptions, not a guaranteed outcome, so you'll need to revisit these numbers regularly as your life circumstances change.

Some versions of the Groww retirement calculator also show you a year-by-year breakdown of how your corpus will grow. This projection helps you visualize the power of compounding and understand how early contributions have more time to multiply compared to later ones.

The interface and user experience

The calculator itself is straightforward, you'll find it on Groww's website under their financial tools section. The interface uses slider controls for most inputs, letting you adjust values and see results update in real time. This interactive design helps you experiment with different scenarios quickly.

You don't need to create an account or log in to use the tool, it's completely accessible to anyone visiting the site. That makes it convenient for quick calculations, but it also means you can't save multiple scenarios or track how your projections change over time unless you manually record them elsewhere.

The results display in a clean, visual format with charts showing projected growth over your investment timeline. You'll see how your monthly contributions accumulate, how returns compound, and what your final corpus looks like compared to what you'll need. The visual representation makes abstract numbers more tangible and easier to grasp at a glance.

Why retirement calculators matter in India

Most Indians don't have a government-backed pension waiting for them at retirement. You're largely on your own when it comes to building wealth for your later years, and that reality makes planning tools like the Groww retirement calculator absolutely necessary. Without a structured approach to estimating your needs, you risk underestimating how much you'll actually need or overshooting to the point where you sacrifice too much today.

The pension crisis you're facing

India's social security system leaves massive gaps for private sector employees. While government workers enjoy defined benefit pensions, most salaried professionals only have the Employees' Provident Fund (EPF) as a mandatory retirement benefit. EPF contributions, 12% of your basic salary plus dearness allowance, often fall short of building a sufficient corpus for 25-30 years of post-retirement life.

Your EPF accumulation depends heavily on how long you work and your salary progression, but it rarely covers more than a fraction of your total retirement needs. A retirement calculator helps you see this gap clearly. When you input your current EPF balance and projected contributions, the tool shows exactly how much additional investment you need through other vehicles like mutual funds, NPS, or PPF to reach your target corpus.

Without quantifying this shortfall early, you'll likely wake up at 50 realizing you're a decade behind on savings.

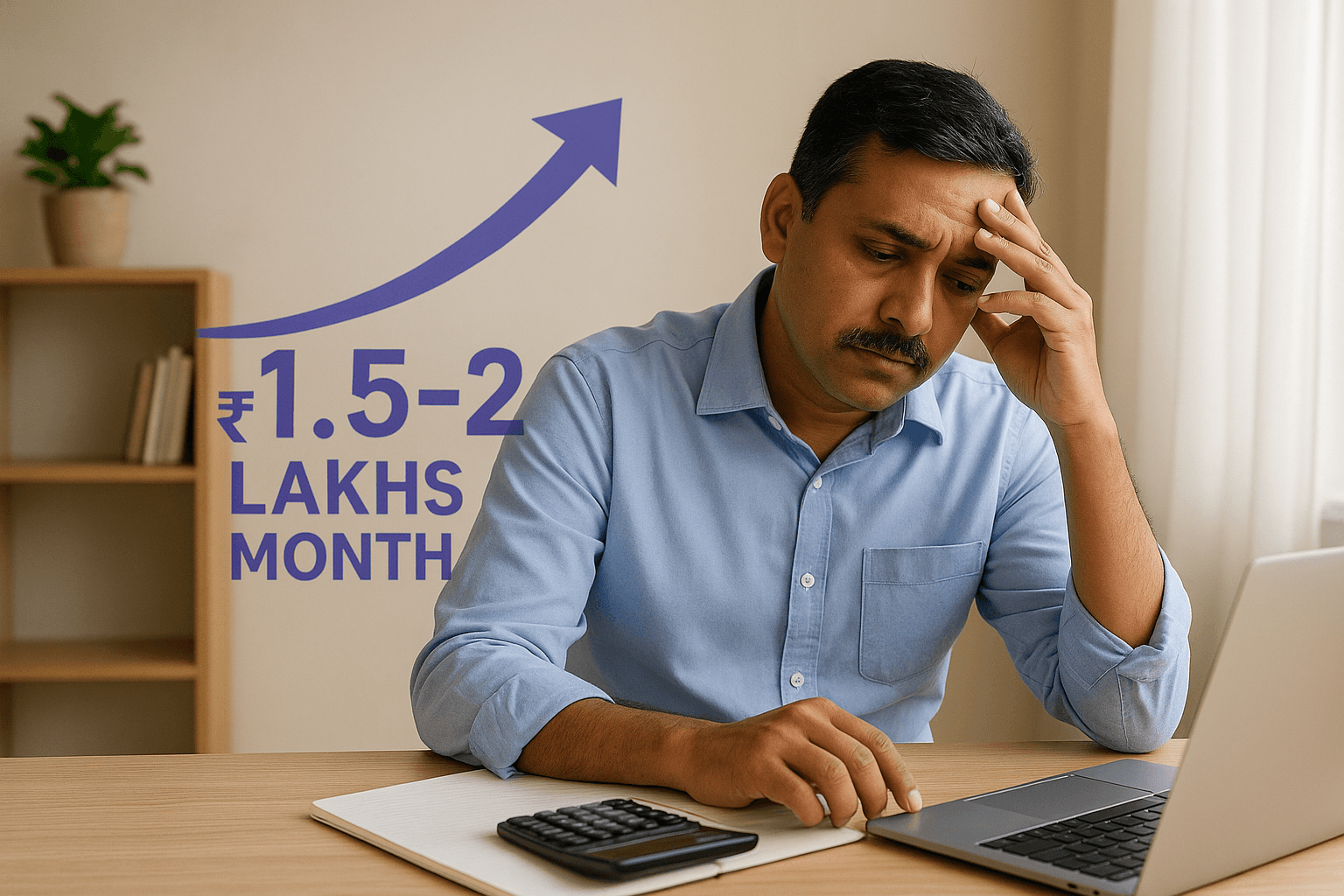

Inflation hits harder over decades

India's inflation rate has historically hovered between 6% and 8% annually, meaning prices roughly double every 10-12 years. That ₹50,000 monthly expense you have today will cost closer to ₹1.5-2 lakhs per month in 30 years. Your brain struggles to intuitively grasp this compounding effect, which is exactly why calculators exist.

The Groww retirement calculator forces you to confront inflation's impact on your purchasing power. It projects your future expenses in nominal terms, making abstract concepts concrete. When you see that you'll need ₹8 crores to maintain a modest lifestyle, the urgency of starting today becomes impossible to ignore.

The compounding advantage of early planning

Starting your retirement savings at 25 versus 35 doesn't just give you 10 extra years, it gives you exponentially more wealth due to compounding. A calculator demonstrates this visually by showing how early contributions grow into disproportionately large portions of your final corpus. That first ₹10,000 you invest at 25 has 35 years to compound, potentially growing 40-50 times by retirement at 12% returns.

Retirement calculators quantify the cost of delay in exact rupee terms. When you adjust the starting age slider, you'll see your required monthly investment spike dramatically with each year you wait. This concrete feedback often provides the motivation needed to start investing immediately rather than putting it off until you're "more settled" or "earning more."

What you need before you start

Jumping into the Groww retirement calculator without preparation leads to garbage in, garbage out results. You need specific financial information and realistic assumptions ready before you start inputting numbers. Spending 15 minutes gathering this data upfront gives you far more accurate projections than guessing your way through the calculator's fields.

Your current financial snapshot

You'll need your actual monthly expenses broken down clearly. Pull up your bank statements from the last three months and calculate your average spending across categories like rent, groceries, utilities, transportation, and discretionary expenses. Don't just estimate based on what you think you spend, actual transaction data reveals spending patterns you might miss.

Calculate your current investable surplus by subtracting monthly expenses from your take-home salary. This number tells you how much you can realistically commit to retirement savings without straining your budget. If you're already investing through EPF, NPS, or mutual funds, note these amounts separately so you can factor them into your total retirement contribution.

Your existing investments and their current values matter because the calculator needs to account for what you've already built, not just future contributions.

Retirement lifestyle expectations

Think through what your post-retirement life actually looks like in practical terms. Will you live in your current city or move somewhere with lower living costs? Do you plan to downsize your home? Will your kids be financially independent by then, or will you still support them? These decisions directly impact your monthly expense projections.

Consider your health and longevity expectations based on family history. If your parents lived into their 90s, you'll need your corpus to stretch further than someone planning for 70-75 years. Factor in potential medical expenses that typically increase with age, even with insurance coverage.

Basic assumption decisions

You need to pick an inflation rate that reflects reality. While the calculator might suggest 6%, India's actual inflation for lifestyle expenses often runs higher, especially for healthcare and education if you'll support grandchildren. Conservative planning uses 7-8% to avoid underestimating future costs.

Decide on a realistic expected return based on your risk appetite and investment approach. Equity-heavy portfolios historically deliver 10-12% long-term returns, but you need to stick with this allocation for decades. If you'll shift to safer assets as retirement approaches, use a blended rate like 9-10% that accounts for this gradual rebalancing.

Your target retirement age matters more than you think. Retiring at 58 versus 60 costs you two years of compounding and adds two years to your withdrawal phase. Be honest about whether you'll actually work until 60, especially if your industry favors younger employees.

How to use the Groww retirement calculator

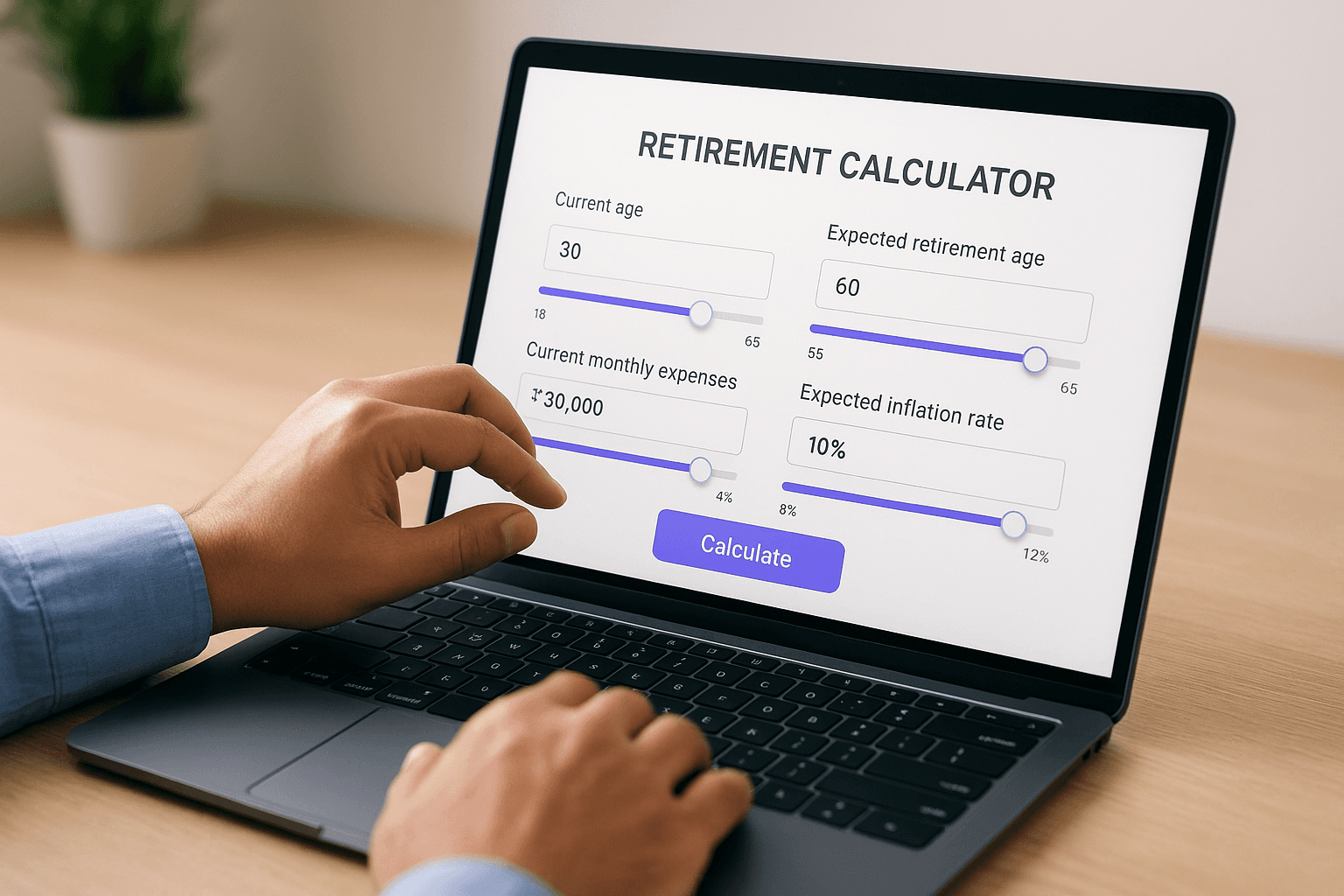

You'll find the Groww retirement calculator on their website under the calculators or tools section, no login required. The interface loads instantly and presents a simple form with labeled input fields and slider controls. Most people complete the calculation in under two minutes, but rushing through without thinking about each input leads to meaningless results that won't help your actual planning.

Step-by-step walkthrough

Start by entering your current age in the first field. The calculator accepts any age from 18 to 65, though starting before 30 gives you the most useful projections. Next, input your expected retirement age, typically between 55 and 65 for most Indian professionals. This gap between your current age and retirement age determines your investment timeline and dramatically affects your required monthly contributions.

Move to the current monthly expenses field and enter what you actually spend today, not what you think you should spend. Include everything from rent and EMIs to groceries and entertainment, a realistic baseline matters more than an aspirational one. The calculator uses this figure as your retirement lifestyle benchmark, assuming you'll want similar purchasing power when you stop working.

Input your expected inflation rate next, usually pre-filled at 6-7% but adjustable based on your assumptions. Follow this with your expected rate of return on investments, where you'll see defaults around 10-12% reflecting equity-heavy portfolios. Adjust this number based on whether you'll actually maintain aggressive allocations or shift to debt instruments as retirement approaches.

The calculator updates results in real-time as you adjust sliders, so you can immediately see how each assumption changes your required corpus and monthly investment.

Testing different scenarios

Run multiple calculations by varying your retirement age by 2-3 years to see the impact of working longer. A 60 versus 58 retirement can reduce your monthly investment needs by 15-20% while giving your existing corpus more time to compound. Similarly, adjust your expected returns up and down by 2% to understand how market performance assumptions affect your planning.

Experiment with different expense levels that reflect lifestyle changes. Calculate one scenario with current expenses, another with 80% of current expenses assuming downsizing, and a third with 120% accounting for increased medical costs. These variations show you a range of outcomes rather than betting everything on a single projection.

Common mistakes to avoid

Don't ignore your existing investments when planning additional contributions. If you already have ₹10 lakhs in EPF and mutual funds, factor this starting capital into your calculations separately since the Groww retirement calculator focuses on future monthly investments. You'll need to manually account for what you've already built when determining your total gap.

Avoid using overly optimistic return assumptions just to make the required monthly investment look manageable. A 15% expected return might make today's contribution comfortable, but actual markets rarely deliver that consistently over 30 years. Conservative assumptions protect you from falling short when reality doesn't match projections.

How the calculator estimates your retirement corpus

The Groww retirement calculator runs three sequential calculations behind the scenes to generate your results. First, it projects your future monthly expenses by compounding your current expenses at your chosen inflation rate. Then it multiplies this inflated expense figure by the number of months you'll live post-retirement to determine your total corpus requirement. Finally, it works backward using compound interest formulas to calculate the monthly investment needed to reach that corpus by your retirement date.

The future value formula for expenses

Your current monthly expense of ₹50,000 won't remain ₹50,000 in 30 years. The calculator applies the future value formula to inflate this amount: FV = PV × (1 + r)^n, where PV is your present expense, r is the annual inflation rate, and n is the number of years until retirement. If you're 30 and retiring at 60 with 7% inflation, your ₹50,000 becomes approximately ₹3.8 lakhs per month.

This inflated monthly expense becomes the foundation for all subsequent calculations. The tool assumes you'll maintain this purchasing power equivalent throughout retirement, meaning if you live 25 years post-retirement, you'll need 300 months' worth of expenses in today's terms, adjusted for inflation.

The calculator doesn't account for changing expense patterns like reduced spending in later retirement years or increased medical costs, it uses a flat inflated expense throughout.

The corpus calculation for post-retirement years

Once the calculator knows your inflated monthly expense, it multiplies this by your expected lifespan in retirement. Most calculators assume 25-30 years of post-retirement life, though some let you adjust this. If your inflated monthly expense is ₹3.8 lakhs and you'll live 25 years after retiring, you need approximately ₹11.4 crores as your target retirement corpus.

The calculation gets slightly more sophisticated when accounting for returns during retirement. Some versions assume your corpus will continue earning returns while you withdraw, extending how long it lasts. The basic formula treats your corpus as a depleting asset that needs to cover every single month until your projected end date.

The monthly investment calculation

The final step reverses the compounding formula to determine your required monthly investment. The calculator uses the future value of an annuity formula: FV = P × [((1 + r)^n - 1) / r], where P is your monthly payment, r is the monthly rate of return, and n is the total number of months. It solves for P given your target FV (retirement corpus).

Your investment timeline dramatically affects this calculation. If you need ₹11.4 crores in 30 years at 12% annual returns, the calculator determines you must invest approximately ₹25,000-30,000 monthly. Delay that start by 10 years, and your monthly requirement jumps to ₹75,000-80,000 because you've lost significant compounding time. The formula assumes consistent monthly contributions with returns compounded annually, which is why the Groww retirement calculator emphasizes starting early.

How to interpret the results and make tradeoffs

The Groww retirement calculator gives you two critical numbers, your total retirement corpus and your required monthly investment. These figures represent mathematical outcomes based on your inputs, not instructions carved in stone. Your job now is to evaluate whether these numbers fit your actual life, and if they don't, you need to understand which variables you can realistically adjust to create a workable plan.

Reading your corpus and monthly investment numbers

Your projected corpus might look shockingly large, ₹8 crores or ₹12 crores when you see it for the first time. This number accounts for decades of inflation eating away at purchasing power, so what looks excessive today will barely cover modest living expenses in 30 years. Don't panic at the size, focus instead on whether the monthly investment amount fits your current budget.

If the calculator tells you to invest ₹40,000 monthly but you only have ₹15,000 available after expenses, you're staring at a planning gap. This gap doesn't mean retirement is impossible, it means you need to adjust your assumptions or make lifestyle changes today. The number serves as a wake-up call, not a death sentence for your retirement dreams.

When your required investment exceeds your current capacity by more than 50%, you'll need to modify multiple variables simultaneously rather than hoping a single change fixes everything.

Adjusting variables to find your balance

Start by pushing your retirement age forward by 2-3 years in the calculator. Working until 62 instead of 60 dramatically reduces your required monthly investment while giving existing savings more time to compound. This represents one of the easiest tradeoffs since most people underestimate how long they'll actually work.

Next, test more conservative expense projections by reducing your current monthly spending estimate by 20-30%. You'll likely downsize housing, eliminate commuting costs, and reduce discretionary spending in retirement. These aren't deprivation tactics, they're realistic adjustments that reflect how retired life differs from working years when you're supporting children and maintaining career appearances.

Making realistic tradeoffs that work

You can't fake your way to a comfortable retirement, so prioritize tradeoffs you'll actually implement over wishful thinking. If you genuinely plan to relocate from Mumbai to Pune post-retirement, model this as a 40% expense reduction. If you're just daydreaming about moving someday, keep your current city's costs in the calculation.

Accept that you might need to increase monthly investments gradually rather than hitting the target amount immediately. Starting with ₹10,000 monthly and increasing by ₹2,000 annually as your salary grows beats waiting until you can afford the full ₹25,000. The calculator shows the ideal endpoint, but you build toward it through consistent incremental progress rather than perfect execution from day one.

Quick reality checks for common retirement questions

You'll face the same questions everyone else asks when planning retirement, and the answers depend entirely on your specific numbers. The groww retirement calculator gives you customized projections, but certain patterns emerge across thousands of users that help you gut-check whether your expectations align with reality. These quick assessments save you from common planning mistakes that derail retirement goals years before you notice the damage.

Can I really retire by 50?

Early retirement by 50 requires aggressive savings rates that most people can't sustain without significant income. You'll need to invest 40-50% of your take-home salary consistently for 20-25 years to build a corpus that lasts 35-40 years. The math works if you're disciplined, but factor in marriage, children's education, and property purchases that typically consume disposable income during your peak earning years.

Your expense assumptions matter even more for early retirement because inflation compounds over longer periods. What costs ₹50,000 monthly today becomes ₹8-10 lakhs monthly by the time you're 85, assuming 7% inflation. Most people underestimate how much corpus they need to maintain purchasing power across four decades of retirement.

Retiring early sounds appealing until you realize you're asking your savings to support you for more years than you worked to build them.

Will ₹1 crore be enough?

A ₹1 crore corpus sounds substantial, but it typically covers only 8-10 years of retirement expenses at current middle-class lifestyle levels. At ₹50,000 monthly expenses, you'll burn through ₹6 lakhs annually, which means your corpus depletes in 16-17 years without accounting for inflation. Add 6-7% annual inflation, and that timeline shrinks to barely a decade.

You need ₹3-5 crores minimum for a comfortable 25-year retirement if you're retiring today with moderate expenses. This number scales up dramatically if you're planning to retire 20-30 years from now because inflation will have multiplied your monthly expense requirements several times over.

Should I wait until my salary increases?

Waiting costs you more than the extra income gains you. Every year you delay investing means losing compounding time that you can never recover, regardless of how much you invest later. Starting with ₹10,000 monthly at 30 beats starting with ₹30,000 monthly at 40 because early contributions compound across more years.

Your salary will likely increase, but so will your lifestyle expenses and obligations. The financial freedom you imagine having at a higher salary rarely materializes because bigger homes, better cars, and children's education consume the incremental income. Start investing whatever you can afford today rather than betting on future discipline you statistically won't maintain.

Where the calculator can mislead you

The Groww retirement calculator operates on simplified assumptions that don't reflect real life's complexity. While the tool provides useful baseline estimates, it treats your financial future as a smooth, predictable path when actual retirement planning involves market crashes, health emergencies, and family obligations that calculators can't anticipate. Understanding these limitations prevents you from either overestimating your readiness or panicking unnecessarily when reality diverges from projections.

Static return assumptions ignore market volatility

The calculator asks for your expected annual return, say 12%, and applies this rate consistently across every year until retirement. Real markets don't work this way. You'll experience years where your portfolio drops 20-30% during crashes followed by years of 25% gains, and this sequence matters more than average returns suggest.

A portfolio earning 12%, then losing 20%, then gaining 15% doesn't produce the same outcome as steady 12% annual returns, even though the arithmetic average looks similar. This sequence of returns risk hits hardest when you're nearing retirement and have accumulated substantial capital. The groww retirement calculator can't model these fluctuations, so your actual corpus might fall significantly short if you retire during a market downturn.

Your retirement success depends not just on average returns but on when those returns occur, and calculators assume perfect timing that never happens.

The inflation rate trap

Most users input the general inflation rate they've heard quoted, around 6-7%, but your personal inflation rate will likely run higher. Healthcare costs in India inflate at 10-15% annually, and if you'll support grandchildren's education, those expenses compound even faster. The calculator treats inflation as a single uniform number across all expense categories.

Geographic inflation matters too. Retiring in a metro city versus a tier-2 town creates vastly different expense trajectories that a single inflation input can't capture. Your housing, medical, and lifestyle costs will inflate at different rates, but the calculator lumps everything together and applies one blanket percentage.

Missing life events and expenses

The calculator completely ignores one-time expenses that puncture your retirement corpus. You might need to support adult children through job loss, help with weddings, or fund medical treatments not covered by insurance. These irregular but significant expenses can consume ₹10-20 lakhs in a single year, yet the calculator assumes smooth monthly withdrawals.

Estate planning, tax implications, and legacy goals don't factor into the calculation either. You'll face capital gains taxes on mutual fund redemptions, potential wealth taxes, and decisions about leaving assets for heirs. The calculator treats your corpus as if you'll spend every rupee by your last day, when most people want to leave something behind or face forced liquidations that trigger tax liabilities.

How to turn the output into a real plan

The groww retirement calculator gives you numbers, but numbers don't save themselves. You need to translate that required monthly investment figure into actual transfers from your salary account into specific investment vehicles every month. Most people bookmark the results, feel motivated for three days, then do nothing because they haven't built a concrete implementation system that survives daily life's distractions.

Map your existing investments first

Before starting new contributions, audit every rupee you've already invested toward retirement. Pull together your EPF statements, mutual fund holdings, NPS accounts, and any PPF or other fixed deposits earmarked for later life. Calculate the current value and project what these will grow to by retirement using your assumed rate of return.

Subtract this projected value from your total corpus requirement to determine your actual gap. If the calculator says you need ₹8 crores and your existing investments will grow to ₹3 crores, you're really solving for the remaining ₹5 crores. This reframed target typically reduces your required monthly contribution by 30-40%, making the goal feel more achievable and preventing you from over-investing unnecessarily.

Your existing savings have already done significant work toward your goal, so factor them in rather than treating your retirement plan as starting from zero.

Build your investment structure across vehicles

Divide your required monthly investment across different tax-efficient instruments based on your risk appetite and liquidity needs. Allocate 60-70% to equity mutual funds through SIPs for growth, 20-30% to NPS for tax benefits under Section 80CCD(1B), and the remainder to safer debt instruments as you approach retirement.

Choose specific funds rather than leaving this abstract. If you need to invest ₹25,000 monthly, set up SIPs of ₹15,000 in two equity index funds, ₹6,000 in NPS, and ₹4,000 in a balanced advantage fund. Document these specific allocations with fund names, amounts, and dates so you can set them up immediately rather than researching options later when motivation fades.

Automate and track quarterly

Set up automatic transfers on your salary date for every investment vehicle you've chosen. Link your salary account to your mutual fund platform, NPS account, and any other instruments so money moves without requiring your monthly attention. Automation removes the decision fatigue that kills consistent investing over decades.

Schedule quarterly reviews where you compare your actual corpus growth against projections. Check if your returns match assumptions, whether you've maintained contribution discipline, and if life changes require updating your plan. These 30-minute quarterly sessions keep you on track without creating the burden of constant monitoring that leads to emotional decisions during market volatility.

A simple way to move forward

The groww retirement calculator gives you a starting point, but numbers on a screen don't build wealth by themselves. You need to commit to consistent action today rather than waiting for the perfect moment or salary level that never arrives. Start with whatever amount fits your current budget, even if it's half of what the calculator recommends, because building the habit matters more than hitting ideal numbers immediately.

Your retirement planning doesn't exist in isolation from your overall financial health. You'll benefit from ongoing guidance that adapts to market changes, life events, and evolving goals rather than relying on a single calculation you made years ago. At Invsify, our AI-powered platform combines SEBI-registered advisory with transparent, conflict-free recommendations that help you actually execute on retirement goals. Create your free account to get personalized insights that go beyond what any calculator can provide, and start building a retirement strategy that works for your specific situation.