HDFC Retirement Plan: Compare Options, Returns & Costs 2025

Shlok Sobti

HDFC Retirement Plan: Compare Options, Returns & Costs 2025

HDFC retirement plans are investment products that help you build a corpus for your post-retirement years. These plans combine life insurance protection with systematic savings, allowing you to accumulate wealth during your working years and receive regular income after retirement. HDFC Life offers several retirement and pension schemes with different features, guarantees, and payout structures to match your financial goals and risk appetite.

This guide breaks down everything you need to evaluate HDFC retirement plans in 2025. You'll learn how to compare different plan options, understand the actual returns and guarantees, identify all costs and charges, and make sense of the tax implications. We'll also show you why getting independent advice matters when choosing a retirement plan, and how Invsify's AI-powered platform helps you make smarter decisions without the bias of commission-driven distributors.

Why HDFC retirement plans matter in 2025

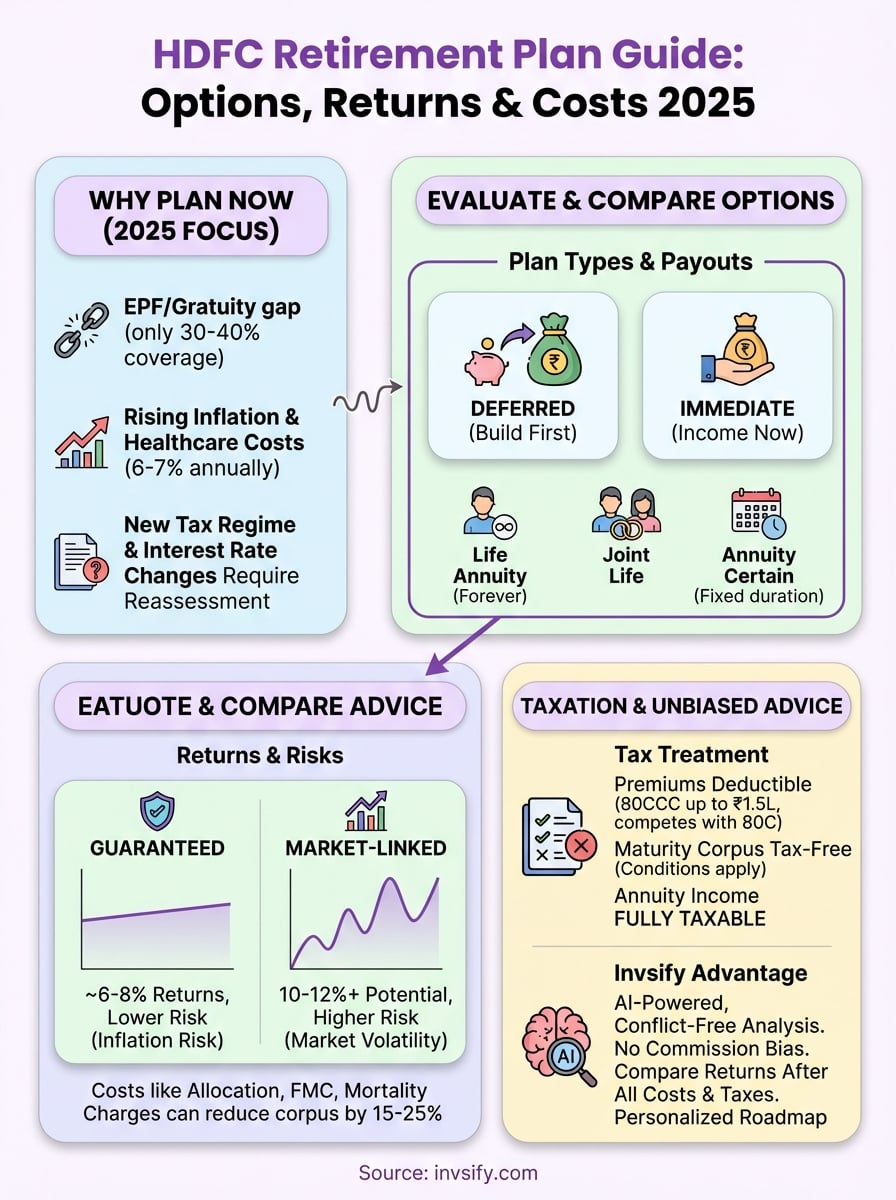

Your retirement corpus needs careful planning because most Indians reach retirement age without adequate savings. The Employee Provident Fund (EPF) and gratuity typically replace only 30-40% of your last drawn salary, leaving a significant income gap. An hdfc retirement plan helps you bridge this gap by creating a dedicated corpus that generates regular income when you stop working. You face rising healthcare costs, longer life expectancy, and inflation that erodes your purchasing power over time, making systematic retirement planning essential rather than optional.

The retirement savings gap in India

Most working professionals underestimate how much they need for retirement. You might assume that ₹50 lakh or ₹1 crore sounds sufficient, but when you account for 25-30 years of post-retirement life, inflation at 6-7% annually, and increasing medical expenses, your actual requirement multiplies. EPF contributions alone rarely create enough corpus to maintain your current lifestyle after retirement. HDFC retirement plans address this gap by allowing you to make regular premium payments during your earning years, which grow through compounding and convert into lifetime income streams through annuity options.

Without dedicated retirement planning, you risk depending on your children or compromising your lifestyle in your golden years.

What makes 2025 different

Several factors make 2025 a critical year for retirement planning. The new income tax regime has changed how you evaluate tax-saving instruments, making it important to reassess whether traditional pension plans still offer value. Interest rates on fixed deposits have stabilized around 6-7% annually, which barely beats inflation and provides limited real returns. HDFC has updated its retirement plans with improved annuity rates and flexible payout options that weren't available in older versions. You also have access to better comparison tools and independent advisory platforms that help you evaluate plans without commission bias. The regulatory environment has strengthened with stricter disclosure norms from IRDAI, giving you more transparency about costs, charges, and projected returns. Starting your retirement planning now, even if you're in your 40s or 50s, still gives you meaningful time to build a corpus through systematic contributions.

How to choose the right HDFC retirement plan

Selecting the right hdfc retirement plan requires you to match product features with your specific financial situation, retirement goals, and risk appetite. You cannot rely on generic recommendations from insurance agents who earn higher commissions on certain products. Instead, you need to evaluate how many years you have until retirement, how much corpus you want to build, whether you prefer guaranteed returns or market-linked growth, and what kind of post-retirement income structure suits your lifestyle. The plan you choose at age 35 differs significantly from what makes sense at age 50, because your time horizon, accumulation capacity, and need for certainty all change as you approach retirement age.

Assess your retirement timeline and corpus goal

Your age and years remaining until retirement determine which plan structure works best for you. If you're 30-40 years old, you have 20-30 years to build your corpus, giving you flexibility to choose between guaranteed plans or market-linked options with higher growth potential. Someone starting at age 50 needs a different approach, focusing on guaranteed accumulation and shorter premium payment terms. Calculate your retirement corpus by estimating your monthly expenses after retirement, accounting for 6-7% annual inflation, and multiplying by the number of years you expect to live post-retirement. For example, if you need ₹50,000 monthly in today's terms and retire at 60, you'll need approximately ₹1.2-1.5 crore to generate that income through annuity options, assuming you live until 85.

Your retirement corpus requirement depends not just on your current expenses, but on how inflation will erode purchasing power over 25-30 years of retired life.

Match plan features to your income needs

Different HDFC retirement plans offer different payout structures once you reach retirement age. You can choose between immediate annuity plans that start paying you the moment you invest a lump sum, or deferred annuity plans where you accumulate corpus first and convert it to income later. The annuity options include life annuity (income until death), joint life annuity (income for you and your spouse), annuity certain (guaranteed payouts for a fixed period like 15 or 20 years), and annuity with return of purchase price (your nominee gets back the principal if you die early). Plans with guaranteed additions provide clarity on minimum corpus growth, while market-linked retirement plans expose you to equity and debt funds that can deliver higher returns but come with volatility. Your choice depends on whether you prioritize certainty or growth, and whether you need income only for yourself or want to protect your spouse's financial future too.

Evaluate your risk tolerance

Your comfort with risk influences which type of HDFC retirement plan suits you best. Guaranteed pension plans remove market risk entirely by promising fixed accumulation rates and annuity payouts, but typically deliver 6-8% annual returns that barely outpace inflation. Unit-linked retirement plans invest your premiums in equity and debt funds, offering potential for 10-12% returns over long periods but exposing you to market fluctuations and no guaranteed corpus. You need to assess whether you can stomach short-term volatility in exchange for higher long-term growth. Consider your overall asset allocation across EPF, PPF, mutual funds, and real estate before deciding how much retirement corpus should sit in guaranteed versus market-linked products. If you already have significant equity exposure through direct mutual funds or stocks, adding a guaranteed HDFC retirement plan balances your portfolio. Conversely, if most of your savings sit in fixed deposits and PPF, a market-linked retirement plan might help you achieve better inflation-adjusted returns.

What HDFC retirement plans offer

HDFC Life provides three main categories of retirement products that cater to different stages of your financial journey. You can choose between deferred pension plans that help you accumulate corpus during your working years, immediate annuity plans that convert a lump sum into instant monthly income, and hybrid plans that combine both accumulation and payout phases in one product. Each category serves a distinct purpose depending on whether you're still building your retirement fund or ready to start receiving regular income. The products also differ in their underlying investment approach, offering both traditional guaranteed plans and market-linked unit-linked options that give you control over asset allocation.

Core product categories

The HDFC Life Systematic Retirement Plan lets you build your corpus through regular premium payments over 10-15 years with guaranteed additions to your fund value. This non-linked deferred annuity plan removes market risk entirely, making it suitable if you prefer certainty over higher growth potential. HDFC Life also offers unit-linked retirement plans like Click 2 Retire that invest your premiums across equity, debt, and balanced funds, giving you flexibility to switch between fund options based on market conditions and your risk appetite. These plans typically allow premium payment terms ranging from 5 to 30 years, with the option to take lump sum withdrawals or convert the entire corpus into annuity at maturity. Immediate annuity products work differently because you invest a single premium and start receiving monthly, quarterly, or annual payouts immediately, which helps if you've already accumulated wealth through other sources and simply need to convert it into regular income.

Key features across HDFC retirement plans

Most HDFC retirement plans include life insurance coverage equal to 105% of premiums paid, protecting your family if you die during the accumulation phase. Your nominees receive either the accumulated fund value or the sum assured, whichever is higher, ensuring they don't lose the retirement corpus you were building. The plans offer flexible premium payment options including single pay, regular pay, and limited pay variants, allowing you to structure contributions based on your cash flow situation. You can also make top-up premium payments in deferred plans whenever you receive bonuses or extra income, accelerating your corpus accumulation without committing to higher regular premiums upfront.

The insurance component in HDFC retirement plans protects your family's financial security if you pass away before reaching retirement age.

Annuity payout structures

Once your hdfc retirement plan reaches maturity, you convert the accumulated corpus into annuity by choosing from multiple payout structures. Life annuity provides income until you die but stops after that, leaving nothing for your spouse or children. Joint life annuity continues payments to your surviving spouse after your death, though monthly amounts reduce by 50-100% depending on the option you select. Annuity certain guarantees payouts for a fixed period like 15 or 20 years regardless of whether you survive, with remaining payments going to nominees if you die early. Plans with return of purchase price refund the original investment amount to your nominees upon death while still providing lifetime income. Payout frequency options include monthly, quarterly, half-yearly, or annual modes, and you can choose whether to receive level payments or increasing payments that account for inflation through regular increments.

Comparing returns risk and guarantees

Understanding the actual returns, risks, and guarantees behind HDFC retirement plans helps you set realistic expectations and avoid disappointment at maturity. Insurance companies show illustrated returns in their brochures that assume 4% and 8% growth rates, but these projections don't reflect guaranteed amounts you'll actually receive. You need to distinguish between what the plan promises with certainty versus what depends on market performance or the insurer's discretionary bonuses. The return profile of your hdfc retirement plan directly impacts how much monthly income you receive after retirement, making this comparison essential before you commit to premium payments for the next 10-30 years.

Guaranteed versus market-linked returns

Traditional guaranteed pension plans from HDFC Life specify exact accumulation rates and guaranteed additions to your corpus each year. These products deliver 6-7.5% annual returns by investing your premiums in government securities, high-grade corporate bonds, and other fixed-income instruments that carry minimal credit risk. You know precisely how much corpus you'll build by the end of your premium payment term, removing all uncertainty about fund value at maturity. The annuity rates at vesting also get locked based on prevailing rates when you start the plan or when you convert to annuity, depending on plan structure.

Market-linked unit-linked retirement plans expose your money to equity and debt fund performance, which fluctuates based on stock market movements and interest rate cycles. These plans allocate your premiums across different fund options ranging from pure equity funds to balanced funds and debt funds, with you controlling the asset mix. Historical data shows equity funds can deliver 10-14% returns over 15-20 year periods, but you face years where your fund value drops by 20-30% during market corrections. Younger investors starting retirement planning in their 30s benefit more from unit-linked plans because they have time to recover from market downturns, while those closer to retirement in their 50s need guaranteed plans to protect accumulated corpus from sudden market crashes.

Guaranteed plans trade higher growth potential for certainty, while market-linked plans offer better inflation-beating returns at the cost of volatility you must tolerate.

Understanding historical performance data

HDFC Life publishes fund performance reports for its unit-linked retirement plans showing actual returns delivered over 1-year, 3-year, 5-year, and 10-year periods across different fund options. You should examine these returns against relevant benchmarks like Nifty 50 for equity funds or CRISIL Composite Bond Index for debt funds to assess whether the fund manager adds value or underperforms the market. Past performance doesn't guarantee future returns, but consistent outperformance or underperformance relative to benchmarks reveals fund management quality. Many unit-linked plans show impressive long-term returns of 12-14% annually, but these include periods when markets delivered exceptional growth that might not repeat in the next 10-20 years.

Guaranteed plans rely on declared bonus rates rather than fund performance, with HDFC Life announcing terminal bonuses and guaranteed additions based on its investment experience. You need to check historical bonus declaration patterns over the past 5-10 years to understand how conservative or generous the insurer has been. Companies facing financial stress or poor investment performance cut bonus rates, directly reducing your final corpus despite having paid premiums for years.

Risk factors you cannot ignore

Several risks affect your hdfc retirement plan returns regardless of product type. Inflation risk erodes the purchasing power of fixed annuity payments, meaning the ₹50,000 monthly income you receive at age 60 buys far less by the time you reach 75. Guaranteed plans particularly suffer from this because annuity payments remain constant while your expenses increase 6-7% annually. Reinvestment risk impacts immediate annuity plans when interest rates fall after you purchase the annuity, locking you into lower payouts than prevailing rates a few years later.

Longevity risk works in your favor with life annuity options because you continue receiving income even if you live beyond 90, but it works against you if you die soon after retirement because your corpus doesn't benefit your nominees. Unit-linked plans carry market timing risk if your retirement date coincides with a market crash, forcing you to convert a depleted fund value into annuity. You can partially mitigate this by systematically shifting from equity to debt funds starting 5 years before your target retirement age, protecting accumulated gains from last-minute volatility.

Costs charges and hidden fees to watch

Every hdfc retirement plan deducts multiple charges from your premiums and accumulated corpus that directly reduce your final returns. These costs compound over 20-30 years, potentially eating away 15-25% of your total fund value by the time you reach retirement. Insurance companies bury these charges in policy documents spanning 40-50 pages, making it difficult for you to calculate the actual impact on your corpus. You need to understand each cost component before signing up because even a 1-2% annual charge difference translates into lakhs of rupees less in your retirement fund after decades of compounding.

Premium allocation charges and policy administration fees

Premium allocation charges take a cut from every premium payment you make, with first-year charges ranging from 15-40% of your premium depending on the plan and payment mode. HDFC retirement plans typically deduct 2-7% from your second year onwards, though these percentages vary based on premium payment term and whether you choose regular pay or limited pay options. Shorter payment terms usually attract higher allocation charges because the insurer needs to recover distribution costs faster. Policy administration charges add another ₹500-1,500 monthly to cover administrative expenses, and this amount increases by 3-5% annually to account for inflation. Single premium plans avoid ongoing allocation charges but still deduct a percentage upfront, sometimes as high as 4-6% of your lump sum investment.

Premium allocation charges in the first year can consume almost half your premium payment in some retirement plans, severely limiting the amount actually invested for your future.

Fund management charges in unit-linked plans

Unit-linked retirement plans levy fund management charges (FMC) ranging from 1.35-1.5% annually on your fund value across equity, debt, and balanced fund options. The insurer deducts this charge daily by canceling units from your portfolio, making it invisible unless you carefully track your unit balance and NAV movements. A 1.5% annual FMC on a corpus of ₹50 lakh means you lose ₹75,000 every year, which itself could have grown through compounding over the remaining years until retirement. Guaranteed pension plans avoid FMC entirely because they don't invest in segregated fund options, instead pooling all premiums into the insurer's participating fund that declares bonuses based on overall investment performance.

Mortality charges and other deductions

Mortality charges pay for the life insurance coverage embedded in your retirement plan, with amounts increasing as you age because death risk rises with advancing years. HDFC deducts these charges monthly from your fund value in unit-linked plans, typically starting at ₹200-500 per lakh of cover for someone in their 30s and rising to ₹2,000-3,000 per lakh by the time you reach 50. Switching charges apply when you move money between different fund options in unit-linked plans, though most insurers allow 4-12 free switches annually before charging ₹100-250 per subsequent switch. Surrender charges penalize you for exiting the plan early, with charges as high as 6-8% of fund value in the first year, gradually reducing to zero after 5-7 years. Partial withdrawal charges range from ₹250-500 per transaction and limit how often you can access your accumulated corpus before maturity.

Tax treatment of HDFC retirement plans

Tax treatment across different stages of your hdfc retirement plan determines how much you actually save and receive after accounting for government deductions. You benefit from upfront tax deductions when paying premiums, but face tax liability when you convert your corpus to annuity or withdraw accumulated funds. The tax implications vary significantly between traditional guaranteed plans and unit-linked retirement products, and recent changes to the Income Tax Act have altered the calculation for many investors. Understanding these tax rules helps you maximize post-tax returns and avoid unpleasant surprises when you finally access your retirement corpus after decades of premium payments.

Tax benefits during accumulation phase

Premiums you pay toward HDFC retirement plans qualify for tax deduction under Section 80CCC up to ₹1.5 lakh annually, which falls within the overall Section 80C limit combining EPF, PPF, life insurance, and other eligible investments. You cannot claim deductions exceeding this combined ceiling, meaning your retirement plan premiums compete with other tax-saving instruments for the same benefit. The deduction applies only when you actually pay the premium, so yearly premium payments give you annual tax benefits while single premium plans provide the deduction only once. Your marginal tax rate determines actual savings, with someone in the 30% bracket saving ₹45,000 in taxes for every ₹1.5 lakh invested, while those in lower brackets save proportionally less.

Section 80CCC deductions reduce your taxable income during working years, but remember this benefit competes with other Section 80C investments within the ₹1.5 lakh annual limit.

Tax on maturity and annuity income

The accumulated corpus at maturity remains tax-free under Section 10(10D) if the annual premium stays below ₹2.5 lakh and the plan meets specific conditions around sum assured to premium ratio. Annuity income you receive after converting your corpus attracts full taxation as income from other sources, added to your total income and taxed at applicable slab rates. Someone receiving ₹50,000 monthly annuity pays tax on ₹6 lakh annually based on their total income including pension, rental income, and interest from other sources. Commutation of up to one-third of the annuity purchase price qualifies for tax exemption under Section 10(10A), though HDFC retirement plans may restrict how much corpus you can commute based on annuity option selected.

Unit-linked retirement plans face different tax treatment because fund switches during accumulation don't trigger capital gains tax. Partial withdrawals from these plans get taxed based on whether the plan qualifies as equity-oriented or debt-oriented, with equity funds attracting long-term capital gains tax at 10% above ₹1 lakh annually and debt funds taxed at slab rates if withdrawn before three years.

New tax regime considerations

The new income tax regime introduced lower tax rates but removed most deductions including Section 80C benefits, fundamentally changing how you evaluate retirement plan tax efficiency. Someone opting for the new regime sacrifices the ₹45,000 annual tax saving from retirement plan premiums but pays lower overall tax on their salary. You need to calculate whether the cumulative tax savings over 20-30 years of premium payments under the old regime outweigh the consistently lower tax liability under the new regime. Many investors now prefer direct mutual fund SIPs with post-tax money because they offer better returns and liquidity compared to tax-saving retirement plans that lock your money until age 58-60.

How Invsify helps you plan for retirement

Choosing an hdfc retirement plan without independent advice leaves you vulnerable to commission-driven recommendations from distributors who earn 15-40% of your first-year premium. Invsify eliminates this conflict by providing AI-powered financial advisory services as a SEBI Registered Investment Advisor, ensuring every recommendation prioritizes your financial goals over product commissions. Our platform analyzes your current financial situation, retirement timeline, and risk appetite to suggest whether HDFC retirement plans suit your needs or if alternative investments deliver better post-tax returns.

Unbiased plan comparison and cost analysis

You receive objective plan comparisons through our conversational RM AI that explains complex insurance terms in simple language, available 24/7 in multiple Indian languages. The platform calculates actual returns after deducting all charges and taxes, showing you precisely how much corpus you'll build with different premium amounts and payment terms. Our hidden fee calculator reveals exactly how much you save by avoiding traditional distributor commissions, often amounting to lakhs of rupees over a 20-30 year investment horizon.

Invsify's conflict-free advice ensures you select retirement products based on financial merit, not on which plan pays the highest commission to the advisor.

Personalized retirement roadmap

Your Wealth Wellness Score identifies gaps in your current retirement planning and suggests specific actions to bridge them. You get personalized weekly insights tracking your progress toward retirement goals, with AI-powered recommendations adjusting as your income grows or life circumstances change.

Bringing your retirement plan together

Evaluating an hdfc retirement plan requires you to look beyond marketing brochures and agent recommendations. You need to calculate actual post-tax returns after accounting for all charges, compare these returns against direct mutual fund investments, and determine whether the insurance component justifies lower growth potential. The annuity structure you choose affects how much monthly income you receive and whether your spouse gets financial protection after your death. Tax implications differ significantly between old and new tax regimes, influencing whether premium deductions provide meaningful savings or simply lock your money into inflexible products.

Invsify removes the guesswork by delivering conflict-free retirement advice backed by AI analysis and SEBI-registered expertise. You get transparent cost comparisons, personalized corpus projections, and unbiased recommendations that align with your financial goals rather than product commissions. Start your retirement planning journey with Invsify today to build a retirement strategy that actually works for your specific situation, timeline, and risk appetite.