How to Calculate Home Loan EMI in India: Formula & Examples

Shlok Sobti

How to Calculate Home Loan EMI in India: Formula & Examples

You just found your dream home. The price looks right. But before you commit, you need to know if you can afford the monthly payments. Understanding how to calculate home loan EMI matters because your equated monthly installment determines whether your budget stays balanced or gets squeezed thin every month.

The good news? You can calculate your EMI in minutes using an online calculator or a simple formula. Both methods give you accurate results when you know your loan amount, interest rate, and repayment tenure.

This guide walks you through four practical steps to calculate your home loan EMI. You'll learn what EMI means, how to gather your loan details, how to use both online calculators and the manual formula, and how to test different scenarios to plan your budget smartly.

What is home loan EMI in India

EMI stands for Equated Monthly Installment. This is the fixed amount you pay your lender every month until you repay your home loan completely. Your EMI covers both the principal (the original loan amount) and the interest charged by the bank or housing finance company.

How EMI payments work

Banks divide your total loan repayment into equal monthly chunks spread across your chosen tenure. Each EMI payment consists of two parts: an interest component and a principal component. During the early years of your loan, most of your EMI goes toward paying interest. As years pass, more of your payment starts reducing the principal amount you borrowed.

Your lender calculates this split automatically using a method called the reducing balance method. When you understand how to calculate home loan emi, you gain control over your financial planning and can make informed decisions about loan tenure and prepayment strategies.

Key components that determine your EMI

Three factors control your monthly payment amount. The principal is the total loan amount you borrow from the lender. The interest rate is the percentage your lender charges annually on the outstanding loan balance. The tenure is the number of months or years you take to repay the entire loan.

Higher loan amounts and interest rates increase your EMI, while longer tenures reduce your monthly payment but increase your total interest cost.

Most Indian banks offer home loan tenures ranging from 5 years to 30 years. Your EMI amount stays constant throughout the loan period unless you switch from a floating rate to a fixed rate or vice versa. Floating rates change based on market conditions, which means your bank can revise your EMI when the Reserve Bank of India adjusts policy rates.

Understanding these basics helps you make smarter choices when you compare different loan offers. You can now move forward to gather the specific details you need for your EMI calculation.

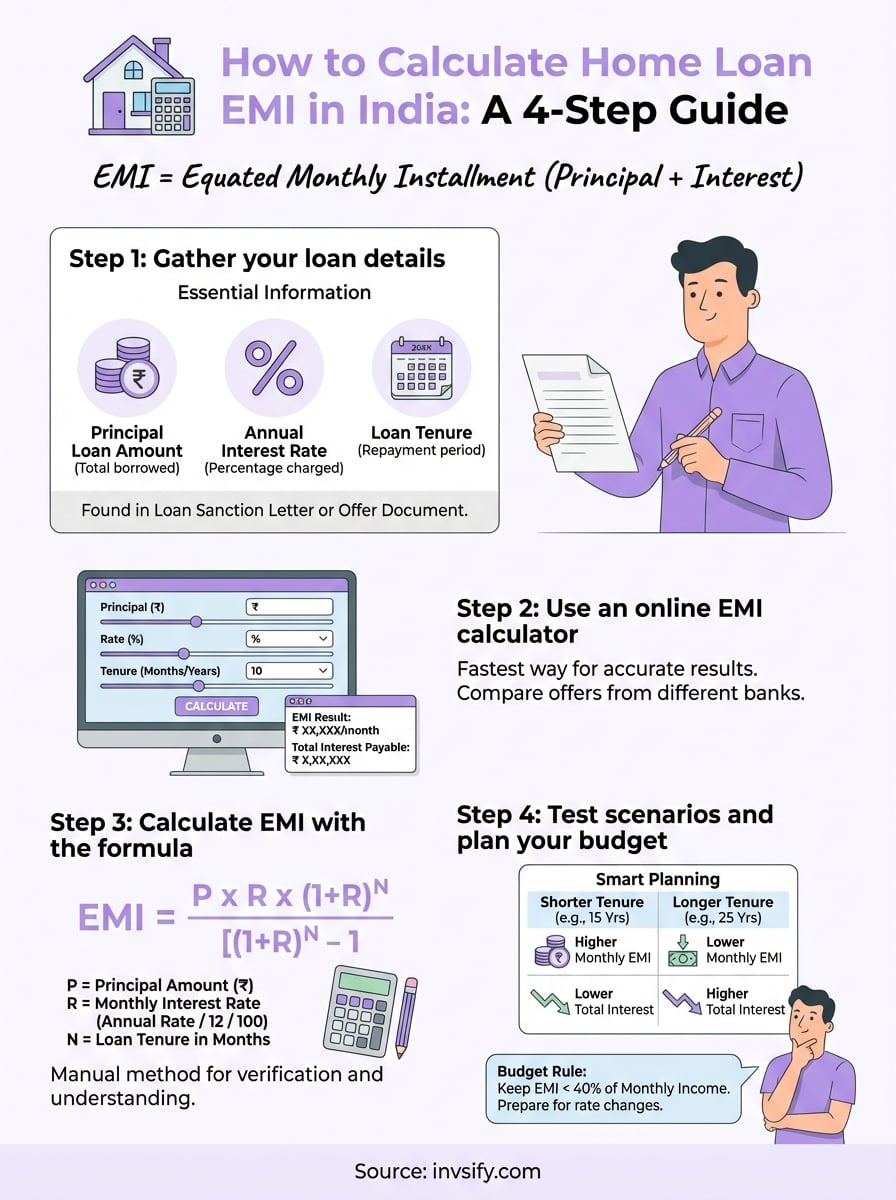

Step 1. Gather your loan details

Before you learn how to calculate home loan emi accurately, you need to collect three specific numbers from your bank or housing finance company. These details form the foundation of your EMI calculation. Missing or incorrect information leads to wrong estimates that can derail your budget planning.

Essential information you need

Your first task involves gathering the principal amount, which is the total loan you plan to borrow. This could be anywhere from ₹5 lakh to ₹2 crore or more, depending on your home price and down payment. Second, you need the annual interest rate your lender offers. Most Indian banks quote home loan rates between 8% and 11% annually, though this varies based on your credit score and the lender's current offers.

The third detail is your loan tenure, measured in months or years. You can choose repayment periods ranging from 60 months (5 years) to 360 months (30 years). Collect these three pieces of information before you proceed with any calculation:

Principal loan amount: Total borrowed sum in rupees

Annual interest rate: Percentage charged by your lender

Loan tenure: Repayment period in months or years

Accurate loan details give you precise EMI estimates that help you compare offers and negotiate better terms with your lender.

Where to find these details

Banks provide these numbers in your loan sanction letter or the initial offer document they send after approving your application. Contact your relationship manager if you're still exploring options and need current rate quotes. Most bank websites also display their prevailing home loan rates in the products section.

Your processing fee statement and loan agreement draft contain the exact principal amount and tenure you agreed upon. Save these documents in a dedicated folder because you'll reference them multiple times during your home buying journey. Keep both digital and physical copies accessible for quick retrieval when you need to recalculate or adjust your loan parameters.

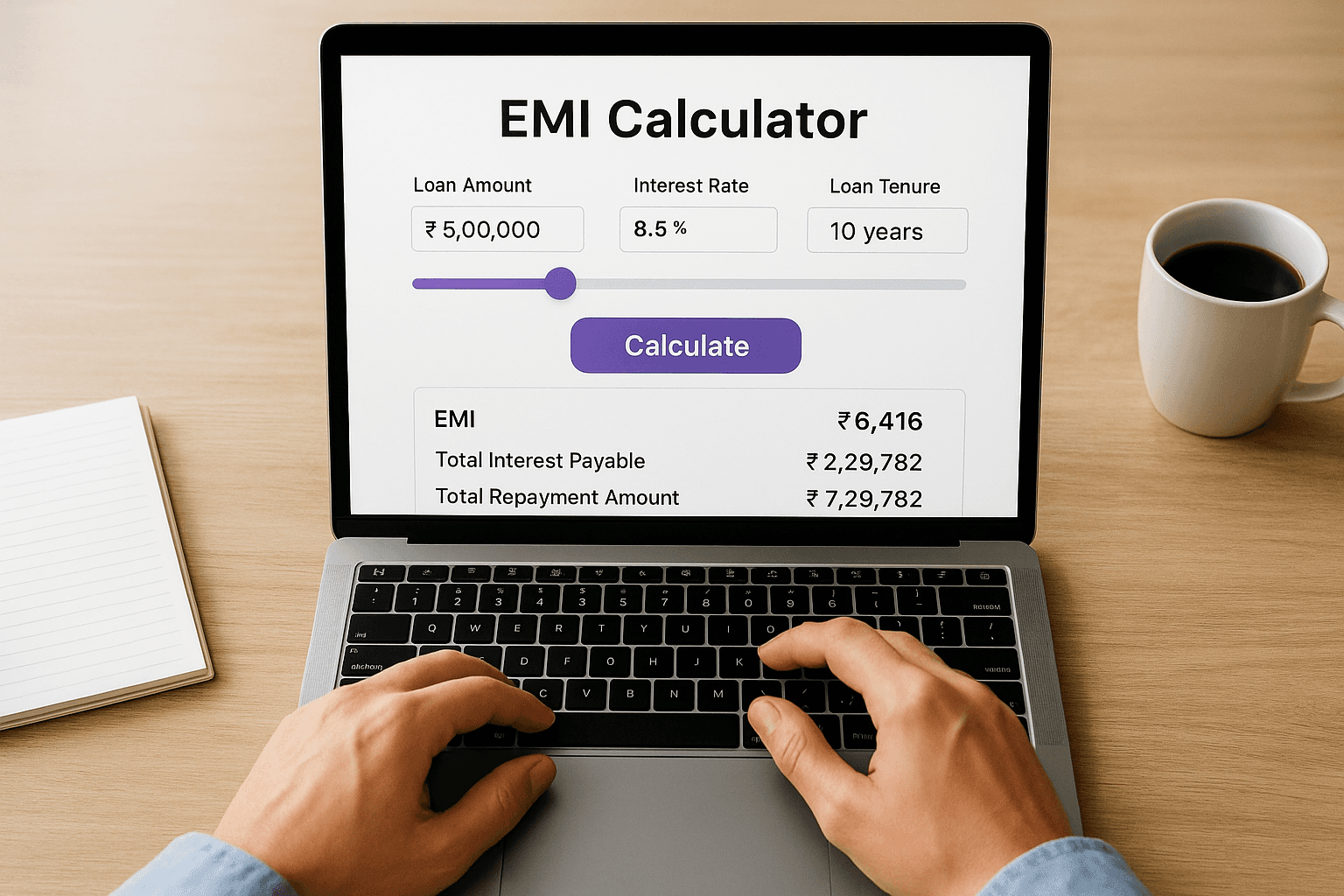

Step 2. Use an online EMI calculator

Online calculators offer the fastest way to learn how to calculate home loan emi without manual math. Most Indian banks and housing finance companies provide free EMI calculators on their websites. These tools deliver instant results once you enter your loan details. You simply adjust three sliders or input boxes, and the calculator displays your monthly payment amount along with a breakdown of interest versus principal.

Steps to calculate using online tools

Visit your preferred lender's website and locate their EMI calculator in the loans or tools section. Enter your principal amount (the loan sum you plan to borrow) in the first field. Most calculators accept amounts ranging from ₹1 lakh to ₹10 crore or higher. Next, input your annual interest rate as a percentage. Banks typically display their current rates near the calculator, so you can reference them directly.

Set your loan tenure using either a dropdown menu or a slider that lets you pick months or years. Click the calculate button, and the tool generates your EMI instantly. Many calculators also show an amortization schedule that breaks down each month's payment into principal and interest components. This schedule helps you understand exactly how much interest you pay over the loan lifetime.

Using multiple calculators from different banks lets you compare offers side by side and choose the most affordable option for your budget.

Understanding your calculation results

The calculator displays your monthly EMI amount prominently at the top of the results section. Below this, you'll see your total interest payable across the entire tenure and the combined total repayment amount (principal plus interest). These three numbers give you a complete picture of your loan cost.

Step 3. Calculate EMI with the formula

Learning how to calculate home loan emi manually gives you complete control over your loan planning without depending on online tools. The EMI formula uses basic mathematics that you can apply using a simple calculator or spreadsheet. This method helps you verify calculator results and understand exactly how banks arrive at your monthly payment amount.

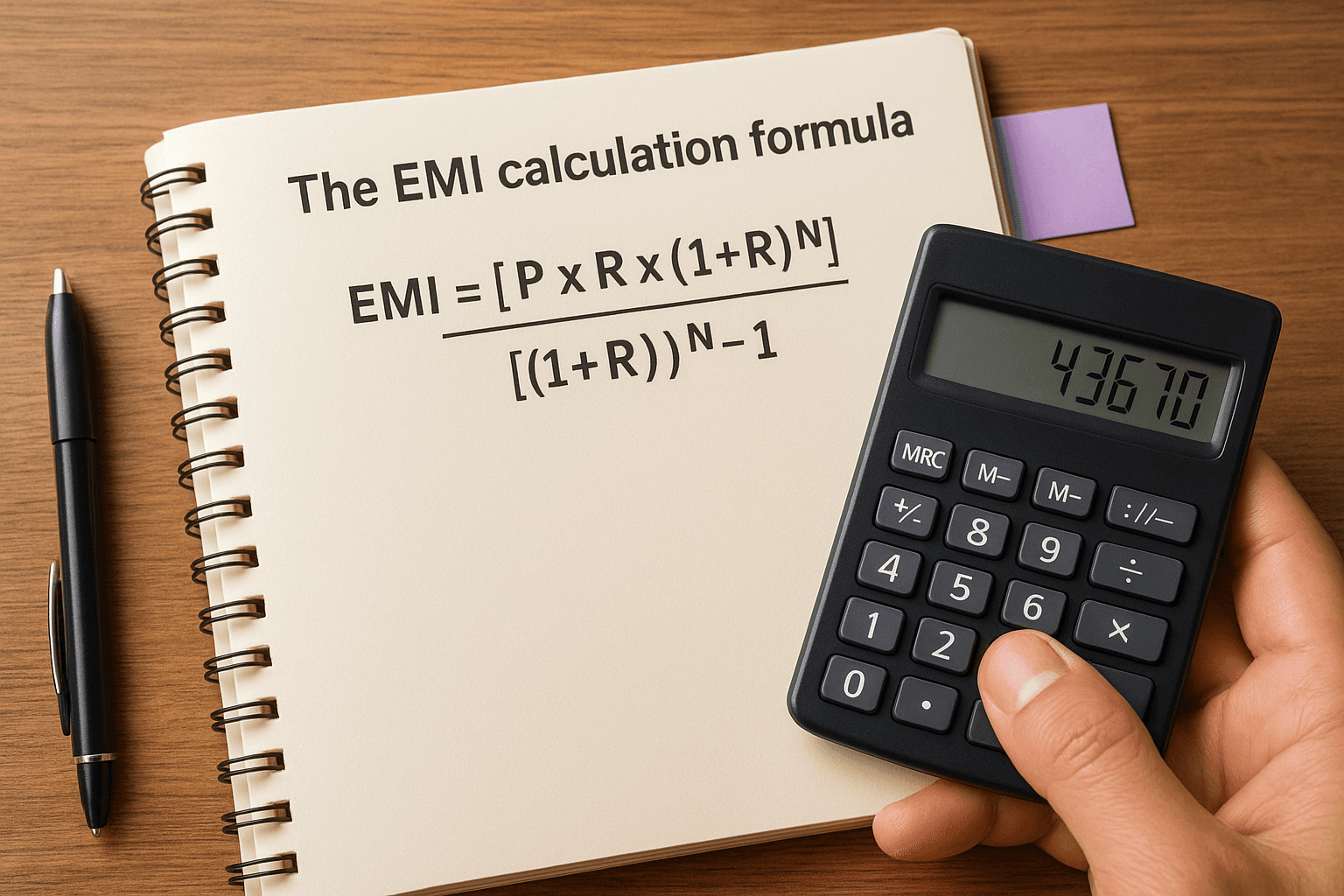

The EMI calculation formula

Banks across India use a standard mathematical formula to calculate your EMI. This formula accounts for your loan amount, interest rate, and repayment tenure in a single calculation. The formula looks like this:

This formula divides your loan repayment into equal monthly installments that remain constant throughout your tenure. Your first EMI and your last EMI will be the same amount, though the split between principal and interest changes each month.

Breaking down the formula components

Each letter in the formula represents a specific value from your loan details. P stands for the principal, which is your total loan amount in rupees. R represents the monthly interest rate, which you calculate by dividing your annual rate by 12 months and then by 100 to convert from percentage to decimal. N indicates the tenure in months, so a 20-year loan equals 240 months.

The caret symbol (^) means "raised to the power of," so (1+R)^N tells you to multiply (1+R) by itself N times. Your calculator or spreadsheet handles this exponential calculation automatically when you enter the formula correctly.

Step-by-step calculation example

Suppose you borrow ₹50 lakh for your home purchase at an 8.5% annual interest rate for 20 years. Start by converting these values into the formula format. Your principal P equals ₹50,00,000. Calculate your monthly interest rate R by dividing 8.5 by 12 and then by 100, which gives you 0.00708333. Your tenure N equals 240 months (20 years x 12 months).

Manual calculation confirms your EMI and helps you catch errors in online calculators or lender quotes.

Now substitute these values into the formula:

Calculate (1+0.00708333)^240 first, which equals 5.2945. Multiply your principal by the monthly rate: 5000000 x 0.00708333 = 35416.65. Then multiply this by 5.2945: 35416.65 x 5.2945 = 187539.74. For the denominator, subtract 1 from 5.2945 to get 4.2945. Finally, divide 187539.74 by 4.2945 to arrive at your EMI of ₹43,670 (rounded to the nearest rupee).

You can verify this calculation using a spreadsheet tool like Google Sheets or Excel with the PMT function: =PMT(0.00708333, 240, -5000000). The negative principal indicates money flowing out from your perspective. This function automatically returns the same EMI amount without requiring manual formula entry.

Your total repayment over 20 years equals ₹43,670 x 240 months = ₹1,04,80,800. Subtract your principal of ₹50,00,000 to find your total interest cost of ₹54,80,800. This detailed breakdown shows you pay more in interest than your original loan amount over a 20-year tenure.

Step 4. Test scenarios and plan your budget

Once you know how to calculate home loan emi, you should test different scenarios before committing to any loan offer. Your initial EMI calculation gives you a starting point, but testing various combinations of loan amount, interest rate, and tenure helps you find the most comfortable repayment structure for your monthly budget. Running multiple calculations takes just a few minutes and can save you from financial stress later.

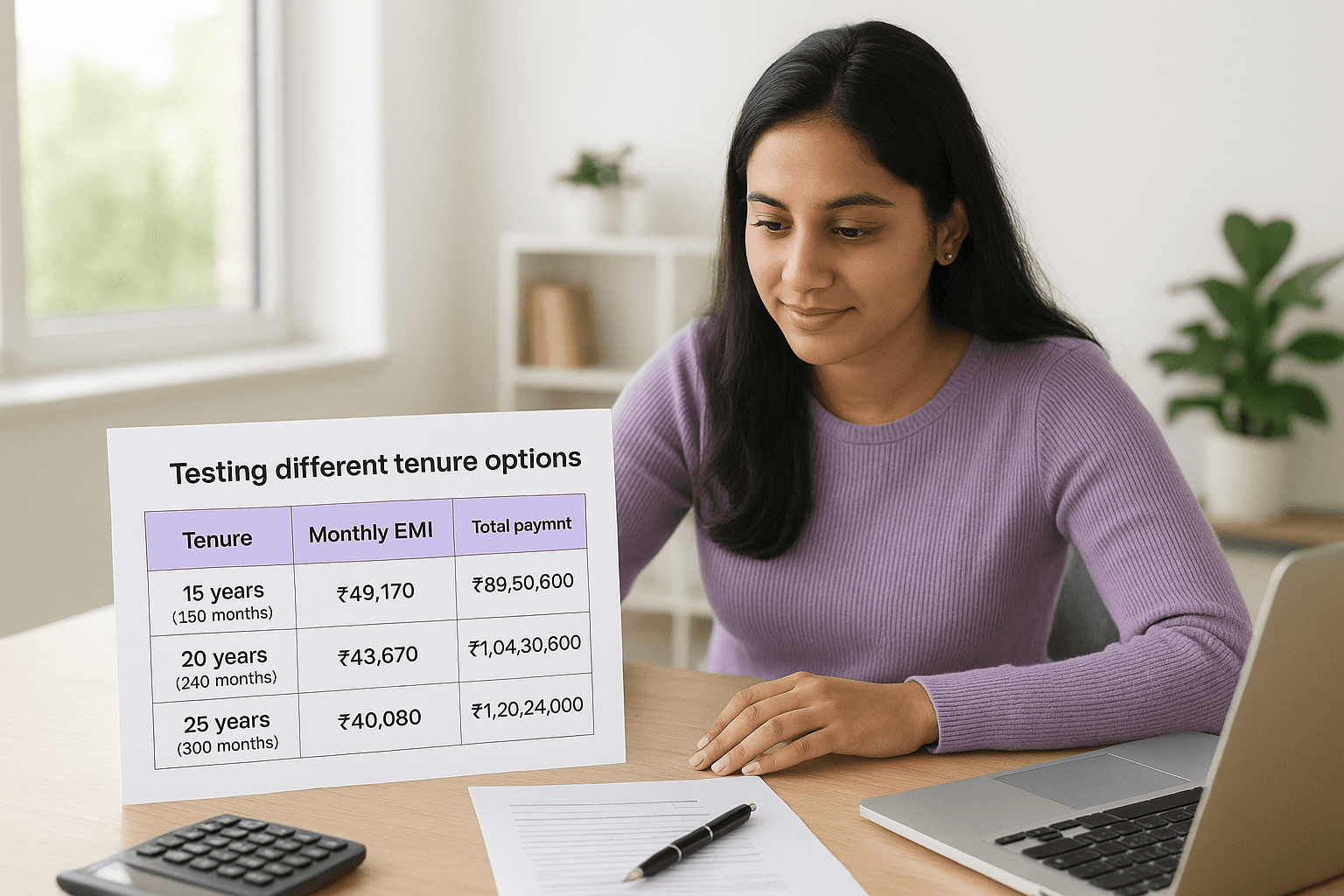

Testing different tenure options

Compare how your EMI changes when you adjust your loan tenure while keeping the principal and interest rate constant. Shorter tenures mean higher monthly payments but lower total interest costs. Longer tenures reduce your EMI but increase the total amount you pay over the loan lifetime. Test at least three tenure options to see the trade-offs clearly.

Here's a comparison using a ₹50 lakh loan at 8.5% annual interest:

Tenure | Monthly EMI | Total Interest | Total Repayment |

|---|---|---|---|

15 years (180 months) | ₹49,170 | ₹38,50,600 | ₹88,50,600 |

20 years (240 months) | ₹43,670 | ₹54,80,800 | ₹1,04,80,800 |

25 years (300 months) | ₹40,080 | ₹70,24,000 | ₹1,20,24,000 |

Choosing a 15-year tenure over 25 years saves you ₹31,73,400 in interest, though your monthly payment increases by ₹9,090.

Adjusting your loan amount based on EMI

Work backward from your affordable monthly payment to determine the maximum loan amount you can manage. Financial experts recommend keeping your EMI below 40% of your monthly income to maintain healthy finances. Calculate your comfortable EMI limit by multiplying your monthly take-home salary by 0.40.

Suppose your monthly income equals ₹1,20,000 and you want to stay within the 40% threshold. Your maximum affordable EMI becomes ₹48,000. Use this figure with different interest rates and tenures to find your ideal loan amount. Test scenarios where you adjust the principal downward until your EMI falls within your budget comfort zone.

Planning for rate changes

Banks offer both fixed and floating interest rates for home loans. Fixed rates remain constant throughout your tenure, while floating rates change based on market conditions and Reserve Bank of India policy decisions. Most Indian borrowers choose floating rates because they typically start lower than fixed rates, but you must prepare for potential increases.

Add a safety buffer of 1% to 2% above your current floating rate when you calculate scenarios. This buffer helps you prepare for rate hikes that could increase your EMI unexpectedly. Calculate your EMI at 8.5%, 9.5%, and 10.5% to understand how much your monthly payment could rise during economic changes.

Build your monthly budget by allocating funds for your EMI, property taxes, maintenance charges, and an emergency fund covering at least six months of EMI payments. This comprehensive planning ensures you can handle your home loan comfortably even during income disruptions or rate increases. Testing multiple scenarios before you apply gives you confidence that your chosen loan structure fits your long-term financial goals.

Plan your EMI with confidence

You now know how to calculate home loan emi using both online calculators and the manual formula. These calculation methods help you compare different loan offers, adjust your repayment tenure based on your monthly budget, and prepare for potential interest rate changes before you commit to any lender.

Your home loan decision affects your finances for the next two or three decades, so invest time testing multiple scenarios and selecting loan terms that fit your budget comfortably without stretching your monthly cash flow. Get personalized financial guidance to build a complete wealth plan that balances your home loan alongside your other investment goals.