How To Calculate Retirement Corpus In India: Step-By-Step

Shlok Sobti

How To Calculate Retirement Corpus In India: Step-By-Step

Most people guess their retirement number. They pick a round figure, ₹5 crore, maybe ₹10 crore, and hope it works out. But hope isn't a financial plan, and a wrong estimate can mean either retiring into anxiety or over-saving at the cost of living well now. If you've ever searched for how to calculate retirement corpus in India, you already know there's no single magic number that applies to everyone.

The actual corpus you need depends on a handful of variables: your current monthly expenses, the age you plan to retire, expected inflation, and the returns your investments can realistically generate. Miss even one of these inputs, and your projection can be off by crores. The good news? The math isn't complicated once you understand the formula, and a step-by-step approach makes it surprisingly straightforward.

This guide walks you through the entire calculation, from identifying your future monthly expenses to arriving at a concrete retirement corpus number. We'll cover the formula, work through a real example with actual numbers, and show you how to use online calculators to verify your math. At Invsify, as a SEBI Registered Investment Advisor, we help salaried professionals in India build clarity around exactly these decisions, using AI-powered, conflict-free advisory that takes the guesswork out of retirement planning. Let's get into the numbers.

What you need before you start

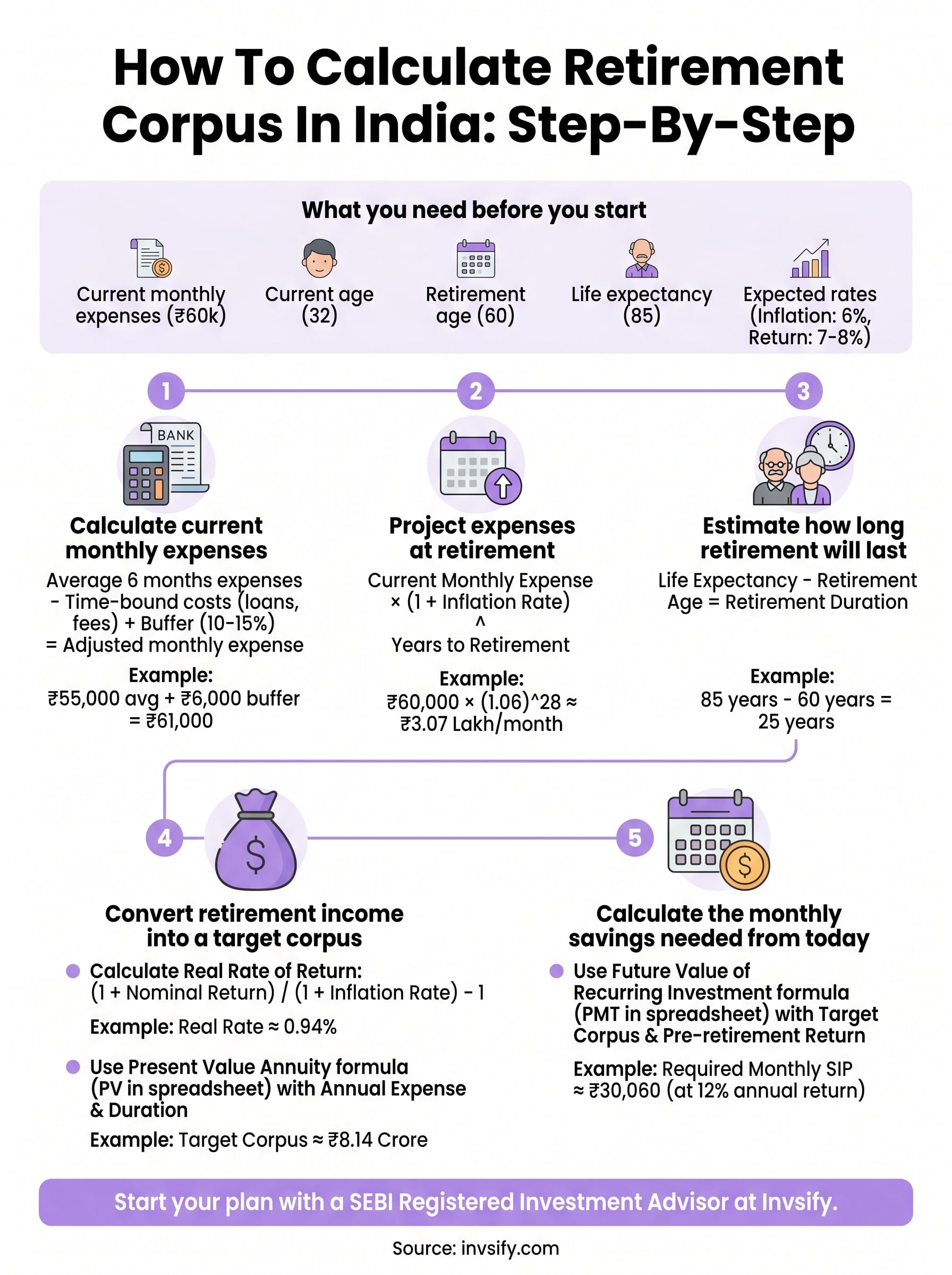

Before you can understand how to calculate retirement corpus in India, you need five specific numbers. Without them, any estimate you produce is just a guess. Gathering these inputs upfront saves you from going back and forth mid-calculation, and it forces you to confront assumptions you may have been avoiding. Spend 20 to 30 minutes pulling together the data below before you open any formula or calculator.

The five inputs that drive the calculation

Every retirement corpus calculation rests on the same five inputs. Getting these numbers right is more important than the formula itself, because a small error in your assumptions compounds over decades into a gap of crores. Here is what you need and where each number feeds into the calculation:

Input | What it is | Example value |

|---|---|---|

Current monthly expenses | What you spend today, excluding EMIs that end before retirement | ₹60,000/month |

Current age | Your age today | 32 years |

Retirement age | The age at which you plan to stop working | 60 years |

Life expectancy | How long you expect your corpus to last | 85 years |

Expected annual inflation | The rate at which your costs will rise over time | 6% per year |

Expected post-retirement return | Annual return your retirement investments will generate | 7-8% per year |

How to estimate your current monthly expenses accurately

Your monthly expense figure is the foundation of the entire calculation. If you underestimate it, every number that follows will be too small. Pull three to six months of bank and credit card statements and add up what you actually spend on rent or home loan EMIs that will continue past retirement, utilities, groceries, transport, healthcare, leisure, and subscriptions. Do not include EMIs for loans you'll pay off before you retire, since those obligations end before your retirement phase begins.

The most common mistake in retirement planning is underestimating current expenses by 20 to 30%, which translates into a corpus shortfall of crores by the time you actually stop working.

Once you have a monthly total, add a 10 to 15% buffer for irregular expenses you may have missed, such as annual insurance premiums, travel, or home maintenance. For example, if your tallied expenses come to ₹55,000, use ₹61,000 to ₹63,000 as your base figure. This buffer keeps your estimate realistic without overcorrecting to an unworkable number.

Key assumptions to lock in before you calculate

Two assumptions will shape your results more than any other: inflation rate and post-retirement return on investment. For India, a 6% annual inflation rate is a reasonable working assumption for general living costs, though healthcare inflation historically runs higher at 8 to 10%. For post-retirement return, most conservative plans use 7 to 8% annually, assuming a balanced mix of debt and equity instruments.

Write these down before you begin the steps:

Inflation rate: 6% per year (use 8% if your expenses are heavily healthcare-related)

Post-retirement return: 7% per year (conservative) or 8% per year (moderate)

Retirement duration: your life expectancy minus your planned retirement age

With these inputs ready, you can move through each calculation step without stopping to search for missing numbers.

Step 1. Calculate your current monthly expenses

The first step in understanding how to calculate retirement corpus in India is knowing exactly what you spend today. Pull up your last six months of bank and credit card statements and calculate an average monthly total across all categories. Do not estimate from memory - actual statement data will likely reveal spending 15 to 25% higher than what most people recall, and that gap matters enormously when it compounds over decades.

List every spending category

Go through your statements and sort every transaction into one of the categories below. Running this exercise across six months rather than just one gives you a more accurate average, since it smooths out months with unusual expenses like a family trip or a medical procedure.

Expense Category | Monthly Amount (₹) |

|---|---|

Rent or home loan EMI (if continuing past retirement) | |

Utilities (electricity, water, gas, internet) | |

Groceries and household supplies | |

Transport (fuel, metro, cabs) | |

Healthcare and medicines | |

Leisure and dining out | |

Insurance premiums (monthly equivalent) | |

Education (if applicable) | |

Subscriptions and memberships | |

Miscellaneous | |

Total |

Fill in your own figures in the right column. Once you have a total, add 10 to 15% to account for irregular spending you may have missed across those six months.

Separate costs that end before retirement

Not every expense you carry today will follow you into retirement. Loan EMIs on a car or home that you'll fully repay before you stop working should be removed from your base figure, since those obligations won't exist by the time you retire. School fees for children who will finish their education well before your retirement date also come out of the number.

Removing time-bound expenses before you build your projection prevents years of unnecessary over-saving, which frees up cash flow for goals you actually want to pursue right now.

What remains after stripping out those costs is your adjusted monthly expense figure. Write this number down clearly, because you carry it directly into Step 2 to project what the same lifestyle will cost you at retirement age, after years of inflation.

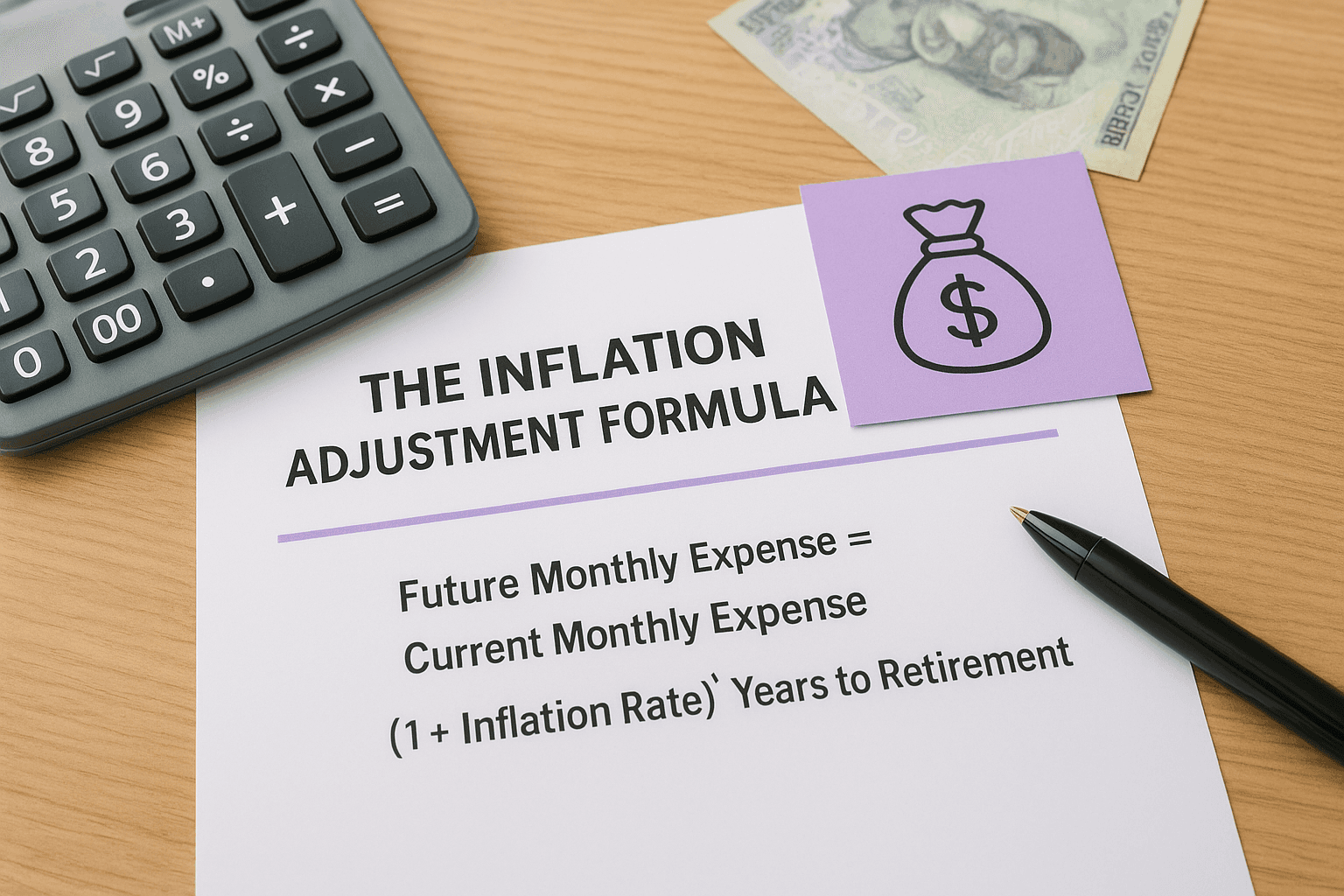

Step 2. Project expenses at retirement using inflation

Your current monthly expenses reflect today's prices. By the time you retire, inflation will have significantly increased the cost of the same lifestyle. This step converts your present-day spending into what it will actually cost at retirement, which is the critical bridge between Step 1 and your final corpus number. Skipping this step, or plugging in a rough guess, is how most people end up with a corpus that looks large but runs out far too soon.

The inflation adjustment formula

The formula used in every serious retirement calculation, and central to understanding how to calculate retirement corpus in India, is straightforward:

Future Monthly Expense = Current Monthly Expense × (1 + Inflation Rate) ^ Years to Retirement

Here is what each variable means:

Current monthly expense: the adjusted figure you calculated in Step 1

Inflation rate: expressed as a decimal (6% becomes 0.06)

Years to retirement: your planned retirement age minus your current age

A 6% annual inflation rate doubles your costs roughly every 12 years, which means ₹60,000 in monthly expenses today becomes approximately ₹2.4 lakh per month after 24 years.

Working through a concrete example

Take your Step 1 figure and apply the formula directly. If your adjusted monthly expense is ₹60,000 today, you are 32 years old, and you plan to retire at 60, you have 28 years until retirement.

Calculation:

Future Monthly Expense = ₹60,000 × (1.06)^28

(1.06)^28 = approximately 5.11

Future Monthly Expense = ₹60,000 × 5.11 = ₹3,06,600 per month

That figure means you will need roughly ₹3.07 lakh per month at retirement just to maintain the lifestyle you live today. To run this calculation for your own numbers, open a spreadsheet and enter =B1*(1.06^B2), where B1 holds your current monthly expense and B2 holds your years to retirement. Swap 0.06 for 0.08 if your expenses skew heavily toward healthcare, since medical inflation in India has historically run 2 to 4 percentage points higher than general inflation.

Step 3. Estimate how long retirement will last

This number, retirement duration, determines how many years your corpus needs to fund. When you're working through how to calculate retirement corpus in India, retirement duration is the multiplier that separates an adequate plan from one that runs out while you're still alive. A difference of five years in your life expectancy estimate can change your required corpus by ₹50 lakh to over ₹1 crore, depending on the size of your monthly drawdown.

Why retirement duration changes everything

Retirement duration is simply your expected life expectancy minus your planned retirement age. If you plan to retire at 60 and expect to live until 85, your corpus must sustain you for 25 years. The longer that window, the more money you need upfront, because your corpus must generate returns and cover inflation simultaneously, year after year, without running out. Most people underestimate this number because they anchor to their parents' generation, where life expectancy was meaningfully shorter.

Underestimating retirement duration by just five years is one of the most common and costly errors in retirement planning, and it leaves you financially exposed at the age when you can least recover from it.

How to set a realistic life expectancy figure

Start with 85 years as your default assumption if you have no significant health conditions. If you have a family history of longevity or you are in good health, push that to 90 years. India's average life expectancy is rising steadily, and healthcare improvements mean the current generation of retirees will likely live longer than any before them.

Use this reference table to find your retirement duration quickly:

Retirement Age | Life Expectancy | Retirement Duration |

|---|---|---|

55 years | 85 years | 30 years |

60 years | 85 years | 25 years |

60 years | 90 years | 30 years |

65 years | 85 years | 20 years |

65 years | 90 years | 25 years |

Pick the row that matches your situation and carry that retirement duration figure into Step 4, where you combine it with your projected monthly expense to calculate your total corpus target.

Step 4. Convert retirement income into a target corpus

You now have two critical numbers: your projected monthly expense at retirement from Step 2, and your retirement duration from Step 3. This step combines them into a single corpus figure, the total amount your portfolio must hold on the day you retire. This is the core of understanding how to calculate retirement corpus in India, and it uses the Present Value of Annuity formula to account for both the returns your corpus will earn and the inflation that will keep eroding its purchasing power.

The formula you need

The standard approach adjusts your nominal investment return for inflation to get a real rate of return, then uses that rate to calculate how large a lump sum you need on Day 1 of retirement to sustain your expenses for the entire duration.

Step-by-step formula:

Real Rate of Return = [(1 + Nominal Return) / (1 + Inflation Rate)] - 1

Annual Retirement Expense = Monthly Expense at Retirement × 12

Corpus = Annual Expense × [1 - (1 + Real Rate)^(-N)] / Real Rate

Where N = number of years in retirement.

Working through the example

Continuing from the earlier example: ₹3,06,600/month at retirement, retiring at 60, expecting to live until 85, so N = 25 years. Nominal post-retirement return is 7%, inflation is 6%.

Real Rate = (1.07 / 1.06) - 1 = 0.0094 (approximately 0.94% per year)

Annual Retirement Expense = ₹3,06,600 × 12 = ₹36,79,200

Corpus = ₹36,79,200 × [1 - (1.0094)^(-25)] / 0.0094

(1.0094)^25 ≈ 1.263, so [1 - (1/1.263)] / 0.0094 = [0.208] / 0.0094 ≈ 22.13

Corpus = ₹36,79,200 × 22.13 ≈ ₹8.14 crore

A small change in your assumed post-retirement return, even half a percentage point, shifts your required corpus by 30 to 50 lakh, which makes locking in a conservative return assumption far safer than being optimistic.

To run this in a spreadsheet, enter this formula directly:

Replace real_rate with 0.0094, N with 25, and annual_expense with your calculated annual figure. The PV function in Google Sheets and Excel handles the annuity math automatically and produces your target corpus as a positive number.

Step 5. Calculate the monthly savings needed from today

You now have your target corpus from Step 4. The final calculation answers a practical question: how much do you need to invest every month, starting today, to reach that number by retirement? This step turns understanding how to calculate retirement corpus in India into a concrete monthly action you can set up through a SIP this week.

The SIP formula

The standard formula for calculating monthly savings uses the Future Value of a recurring investment. This is the same math behind every SIP calculator in India, and running it yourself gives you a number you can actually trust.

Monthly SIP = Corpus × r / [(1 + r)^n - 1]

Where:

Corpus = your target retirement corpus (from Step 4)

r = monthly rate of return (annual pre-retirement return divided by 12)

n = total number of months until retirement

Working through the numbers

Continuing the example: the target corpus is ₹8.14 crore, current age is 32, retirement age is 60, giving 28 years or 336 months. Assume a 12% annual pre-retirement return from a diversified equity mutual fund portfolio, which gives a monthly rate of 0.01.

Monthly SIP = ₹8,14,00,000 × 0.01 / [(1.01)^336 - 1]

(1.01)^336 is approximately 28.08, so the denominator becomes 27.08.

Monthly SIP = ₹81,400 / 27.08 ≈ ₹30,060 per month

To run this directly in a spreadsheet, use the PMT function:

Replace monthly_rate with 0.01, n with 336, and corpus with your Step 4 figure. The PMT function returns your required monthly investment as a positive number with no manual computation needed.

Starting your SIP five years earlier at 27 instead of 32 cuts your required monthly contribution by nearly 40%, because compounding handles a larger share of the heavy lifting.

Adjust your assumed annual return based on your actual investment allocation. A 100% equity portfolio in India historically delivers 12 to 14% over long horizons, while a 60:40 equity-debt split is more conservative at 9 to 10%. Use the return that matches your risk tolerance, not the one that makes the monthly number look smaller.

Final checklist

You now have every piece you need to calculate your retirement corpus from scratch. Run through this list before you finalize your plan:

Current monthly expenses confirmed from actual bank statements, not from memory

Time-bound EMIs removed from your base expense figure

Inflation-adjusted monthly expense calculated using (1 + 0.06)^years to retirement

Retirement duration set to at least 25 years, or longer if your health warrants it

Real rate of return calculated by adjusting nominal return for inflation

Target corpus derived using the PV annuity formula or the PMT function in a spreadsheet

Monthly SIP amount confirmed using the PMT formula at a realistic pre-retirement return

Understanding how to calculate retirement corpus in India gives you a number you can actually act on. If you want a personalized plan reviewed by a SEBI Registered Investment Advisor, start your retirement planning with Invsify today.