How To Calculate Risk Capacity: A Step-By-Step Method

Shlok Sobti

How To Calculate Risk Capacity: A Step-By-Step Method

Your willingness to take investment risks tells one story. Your ability to absorb financial losses tells another, often very different, one. That second story is your risk capacity, and knowing how to calculate risk capacity matters more than most investors realize.

Risk tolerance is about emotions and comfort levels. Risk capacity, however, is purely mathematical. It factors in your income stability, existing assets, time horizon, financial obligations, and liquidity needs. Getting this calculation wrong can lead to portfolios that either expose you to unnecessary danger or leave significant growth on the table.

At Invsify, our AI-powered advisory platform helps Indian investors move beyond gut feelings toward objective, SEBI-compliant wealth strategies built on data-driven risk assessment. This guide walks you through the step-by-step method to calculate your true risk capacity, so your investment decisions align with what you can actually afford to risk, not just what you think you can handle.

What risk capacity is and is not

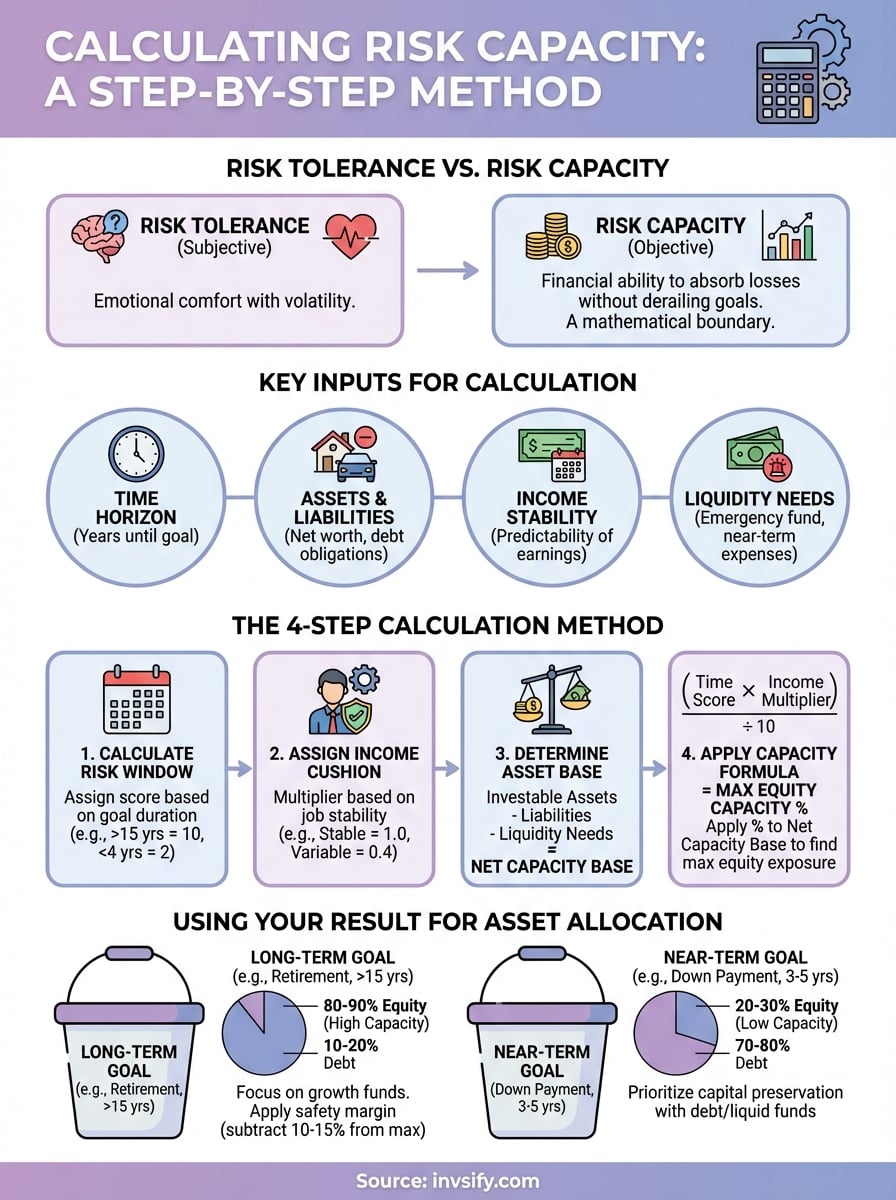

Risk capacity measures the maximum financial loss you can absorb without derailing your long-term goals or immediate needs. It's a mathematical boundary determined by your financial position, not your psychological comfort. Think of it as the ceiling of risk you can afford, calculated by looking at hard numbers like your savings, income stability, time until retirement, and fixed obligations.

The definition of risk capacity

Your risk capacity represents the objective amount of investment risk your financial situation allows. It answers a concrete question: if your portfolio dropped by a certain percentage tomorrow, could you still pay your EMIs, meet your children's education expenses, and retire on schedule? This calculation considers five core inputs: your total investable assets, the time horizon before you need the money, your income sources and stability, your existing financial liabilities, and your liquidity requirements for emergencies.

A 28-year-old software engineer in Bangalore with ₹15 lakh saved, stable employment, no dependents, and 30 years until retirement has high risk capacity. She can weather significant market downturns because time allows recovery, and her obligations are minimal. Contrast this with a 52-year-old small business owner with ₹80 lakh saved but irregular income, college fees due in two years, and retirement in eight years. Despite larger assets, his risk capacity is lower because his timeline is compressed and his cash flow less predictable.

Risk capacity is not about what losses you can stomach emotionally. It's about what losses your financial reality can absorb without forcing you to sell investments at the wrong time or abandon your goals.

What risk capacity is not

Risk capacity is not risk tolerance. Tolerance is subjective and emotional. It measures how much volatility keeps you awake at night or triggers panic selling. You might have high tolerance because you don't check your portfolio often or you philosophically believe in long-term growth, but if you need that money in three years for a down payment, your capacity remains low regardless of your comfort with swings.

Risk capacity also differs from required return. Required return tells you how much growth you need to hit a specific goal. If you need 12% annual returns to fund retirement, that's your target, but it says nothing about whether you can afford the volatility typically required to chase that return. You might require high returns but lack the capacity to take the risks those returns demand, creating a planning problem that needs adjustment in goals or timelines.

Many investors confuse risk capacity with current portfolio allocation. Just because you currently hold 80% equities doesn't mean you have the capacity for that level of risk. Your existing allocation might be a historical accident or a product of overconfidence, not a reflection of your true financial ability to handle losses. Learning how to calculate risk capacity properly prevents this mismatch between what you own and what you should own based on your actual financial position.

Risk capacity is also not static. It shifts as your income grows, your liabilities change, your dependents age out, and your time horizons evolve. The capacity you had five years ago may bear little resemblance to your current financial boundary, which is why regular recalculation matters.

Why risk capacity matters for Indian investors

Understanding how to calculate risk capacity prevents the costly mistakes that plague Indian portfolios during market corrections. When the Sensex dropped 23% in early 2020, investors with properly assessed capacity stayed invested and recovered. Those who overestimated their capacity panicked, sold at the bottom, and locked in permanent losses. Your risk capacity acts as a financial safety boundary that keeps you invested through volatility without jeopardizing your essential goals.

The gap between confidence and capacity

Indian investors often display high risk tolerance during bull markets but lack the actual capacity to support it. You might feel comfortable with 90% equity exposure when markets rise, but if you need that money for your daughter's engineering fees in three years, your capacity contradicts your confidence. This mismatch becomes dangerous when corrections hit. SEBI regulations require investment advisors to assess suitability, but most bank relationship managers focus on selling products rather than calculating your true financial ability to absorb losses.

Understanding your capacity prevents the trap of chasing returns your financial situation cannot support, especially in India's volatile equity markets where single-year swings of 30-40% are not uncommon.

Protection during income disruptions

Indian employment patterns make risk capacity calculation essential. If you work in sectors prone to cyclical downturns like real estate, automotive, or IT services, your income stability differs vastly from a government employee or doctor. Job losses often coincide with market downturns, forcing premature withdrawals at the worst time. Calculating capacity helps you build the right liquidity buffer and adjust your equity allocation based on income predictability, not just current salary figures.

Preventing goal abandonment

Most Indian households juggle multiple financial goals simultaneously: children's education, parents' healthcare, property purchase, and retirement. Without proper capacity assessment, you risk underfunding critical goals by taking excessive risk on money needed within five years, or conversely, parking long-term retirement funds in fixed deposits that barely beat inflation. Your calculated capacity tells you exactly which goal buckets can handle equity exposure and which cannot, creating a goal-specific risk framework rather than a one-size-fits-all portfolio.

Inputs you need before you calculate it

Before you learn how to calculate risk capacity, you need to gather specific financial data points that paint an accurate picture of your situation. These inputs are not estimates or rough guesses. You need precise numbers pulled from bank statements, investment account summaries, loan documents, and income records. The accuracy of your capacity calculation depends entirely on the quality of these inputs, so allocate an hour to compile them before starting any formula.

Your time horizon for each goal

You need the exact number of years until you need the money for each financial goal. If your daughter's engineering admission is in 2030, your time horizon is four years, not "a few years" or "soon." Break down your total investable assets by goal and assign each bucket a specific timeframe. Retirement funds might have a 20-year horizon, while your planned property purchase has three years. This input directly determines how much volatility your portfolio can absorb, because longer horizons allow recovery from market downturns.

Your current assets and liabilities

List every investable asset you own: equity mutual funds, stocks, PPF balance, EPF corpus, fixed deposits, bonds, and liquid funds. Exclude your primary residence unless you plan to monetize it. Then compile all liabilities: home loans, car loans, personal loans, and credit card debt. You need the outstanding principal, not the original loan amount, and the monthly EMI obligation. Your net worth (assets minus liabilities) forms the foundation of your capacity calculation, showing how much cushion exists between what you own and what you owe.

Your income stability and sources

Document your monthly take-home salary, any rental income, business profits, or investment dividends. More importantly, assess the stability of each income source. Salaried employees in stable sectors have predictable income, while freelancers or business owners face variability. If your income fluctuates seasonally or depends on commissions, you need to factor in worst-case scenarios rather than peak earnings. This input prevents overestimating your ability to weather market drops when income itself might be under pressure.

Your risk capacity cannot exceed what your income stability and time horizon can support, regardless of your current asset size.

Your non-negotiable liquidity needs

Calculate the minimum cash you need accessible within three months for emergencies, planned expenses, and financial obligations. This includes six months of living expenses, upcoming tax payments, insurance premiums, and any planned purchases. You cannot invest money earmarked for immediate liquidity in volatile assets, so this figure reduces your investable base before you even start calculating capacity.

How to calculate risk capacity step by step

Now that you have your inputs assembled, you can calculate your actual risk capacity using a methodical approach. This calculation combines time horizon, income stability, and net assets into a single metric that tells you the maximum portfolio volatility you can handle. The method below follows principles used by SEBI-registered investment advisors but simplifies the math so you can apply it yourself.

Step one: calculate your risk window

Take your time horizon in years for each goal and assign a capacity score based on duration. Goals beyond 15 years get a score of 10. Goals between 10-15 years score 8. Goals in the 7-10 year range score 6. Goals 4-7 years away score 4. Anything under 4 years scores 2. You need separate scores for separate goal buckets because each has different capacity limits. Your retirement fund at 25 years gets a 10, while your property fund at 3 years gets a 2.

Step two: assess your income cushion

Evaluate your income stability and assign a multiplier. Salaried employees in stable sectors (government, healthcare, education) get a 1.0 multiplier. Private sector employees in established companies get 0.8. Business owners or commission-based earners get 0.6. Freelancers or those in cyclical industries get 0.4. This multiplier reflects the probability your income continues during market downturns when you most need it.

Step three: determine your asset base

Subtract your total liabilities from your total investable assets to get your net investable base. Then subtract your emergency fund and any liquidity needs for the next 12 months. What remains is your true capacity base for risk-taking. If you have ₹50 lakh in assets, ₹10 lakh in loans, and need ₹8 lakh for liquidity, your capacity base is ₹32 lakh, not ₹50 lakh.

Step four: apply the capacity formula

Multiply your goal's time score by your income multiplier, then divide by 10 to get a percentage capacity. A stable salaried employee with a 15-year goal calculates: (10 × 1.0) ÷ 10 = 100% equity capacity. A freelancer with a 5-year goal calculates: (4 × 0.4) ÷ 10 = 16% equity capacity. Apply this percentage to your capacity base for that goal to determine maximum equity exposure.

Your calculated capacity sets the ceiling for equity allocation, not the target. You can always invest more conservatively than your capacity allows, but exceeding it invites financial danger.

How to use your result to set asset mix

Your calculated risk capacity gives you a maximum equity percentage, but translating that number into an actual portfolio requires additional steps. The capacity figure sets the upper boundary of risk you can take, not necessarily the target allocation you should implement. You need to convert this mathematical result into a practical asset mix that balances growth potential with your calculated safety limits.

Translate capacity into equity allocation

If your capacity calculation shows 70% equity tolerance for a particular goal bucket, that means you can allocate up to 70% of that bucket into equity mutual funds or stocks, with the remaining 30% in debt instruments. Start by identifying which equity funds match your goal timeline. Goals beyond 10 years can use pure equity funds like large-cap or multi-cap schemes. Goals in the 5-10 year range benefit from balanced advantage funds that automatically adjust equity exposure based on market valuations.

Your debt allocation should fill the gap between your equity percentage and 100%. If you calculated 60% equity capacity, the remaining 40% goes into debt mutual funds for goals beyond three years, or fixed deposits and liquid funds for nearer goals. Avoid the trap of thinking 100% capacity means you must take 100% equity exposure. Markets reward caution as much as they punish excess risk.

Your asset mix should sit comfortably below your calculated capacity ceiling, giving you room to handle market volatility without breaching your financial boundaries.

Apply goal-specific allocations

Each financial goal you identified when learning how to calculate risk capacity needs its own asset allocation based on its individual capacity score. Your retirement fund with 25 years and 100% capacity can sit in pure equity, while your property fund with 3 years and 20% capacity needs mostly debt instruments. Create separate portfolios or mentally segment your existing investments by goal, then apply the appropriate equity-debt mix to each bucket based on its calculated capacity.

Build in safety margins

Subtract 10-15 percentage points from your calculated maximum capacity to create a practical allocation target. If your capacity calculation shows 80% equity tolerance, implement 65-70% instead. This buffer protects you from calculation errors, unexpected expenses, and the reality that markets often behave worse than historical patterns suggest. You preserve growth potential while avoiding the financial stress that comes from operating at your absolute risk limit.

Next steps

You now understand how to calculate risk capacity using concrete financial inputs instead of relying on gut feelings or generic questionnaires. Your calculation reveals the mathematical boundary between safe investing and financial danger, giving you a defensible framework for every portfolio decision you make going forward. This capacity number changes as your income evolves, your liabilities shift, and your goals approach, so recalculate annually or whenever major life events occur.

Start implementing your capacity-based asset allocation this month. Review your existing mutual funds and rebalance any goal buckets that exceed their calculated equity limits. Create separate investment accounts for different goals if your current setup mixes retirement funds with near-term expenses, making it impossible to apply the right allocation to each bucket.

Invsify's AI-powered platform automates this entire capacity assessment process, combining your financial data with SEBI-compliant advisory standards to deliver personalized portfolio recommendations without hidden distributor fees. Get started with Invsify to move beyond generic advice toward a risk framework built specifically for your financial reality.