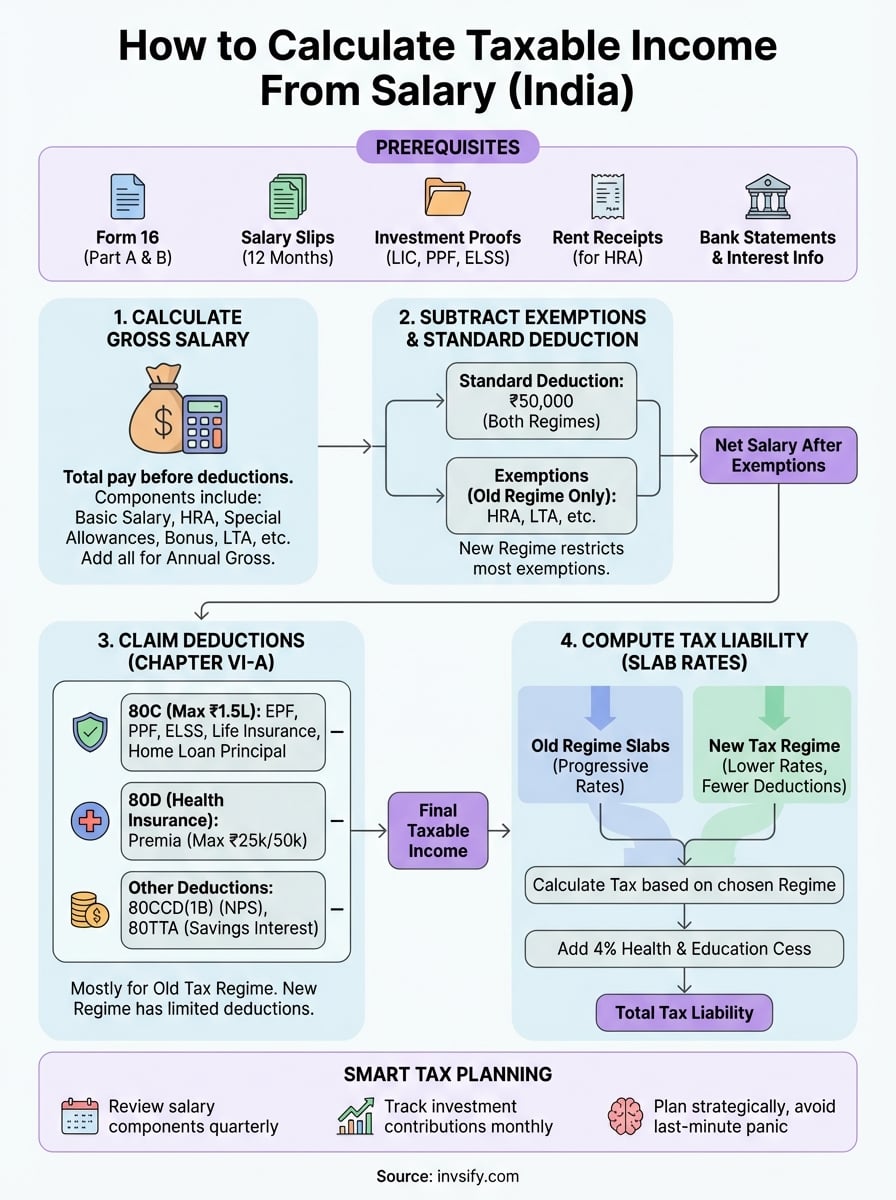

How to Calculate Taxable Income From Salary With Examples

Shlok Sobti

How to Calculate Taxable Income From Salary With Examples

Every month you see a salary slip with numbers that don't match your bank deposit. Tax deducted at source (TDS) chips away at your earnings, but you're not entirely sure if the amount is correct. Understanding how to calculate taxable income from salary helps you verify what you owe, plan better, and avoid surprises during tax filing season.

The good news? Calculating your taxable income follows a clear formula. Start with your gross salary, subtract eligible exemptions like House Rent Allowance (HRA) and the standard deduction, then apply deductions under Section 80C and other provisions. What remains is the amount on which you pay tax based on your chosen regime.

This guide walks you through each step with real examples using Indian salary structures. You'll learn how to identify every component of your income, apply the right exemptions, claim available deductions, and compute your final tax liability accurately. By the end, you'll know exactly where your money goes and how to optimize it.

Prerequisites for calculating taxable income

Before you learn how to calculate taxable income from salary, you need specific documents and information at hand. Tax calculation isn't guesswork. You're working with official records that detail every rupee you earned and every deduction you claimed throughout the financial year.

Your employer issues a Form 16 each year, typically by mid-June. This document contains your total income, TDS deducted, and exemptions already applied. Without it, you'll struggle to verify whether your tax withholding matches your actual liability. Keep digital and physical copies accessible because you'll reference multiple sections during calculation.

Documents you need

Gather these documents before you start:

Form 16 from your employer (Parts A and B)

Salary slips for all 12 months of the financial year

Investment proof documents (LIC policies, PPF statements, ELSS confirmations)

Rent receipts if you're claiming HRA exemption

Home loan statements showing principal and interest paid

Medical insurance premium receipts for Section 80D

Bank statements showing interest earned on savings accounts

Having complete documentation prevents errors and ensures you claim every eligible deduction.

Information to gather

You need to know your chosen tax regime upfront. India offers two systems: the old regime with deductions and exemptions, and the new regime with lower tax rates but fewer breaks. Your choice fundamentally changes which exemptions you can claim and how your final tax amount gets calculated.

Check your PAN card details match exactly with your Form 16. Mismatches trigger processing delays when you file returns. Note your Aadhaar number as well, since linking PAN with Aadhaar is mandatory for filing. Write down any previous employer details if you switched jobs mid-year, because you'll need to combine income from all sources to arrive at your total gross salary figure.

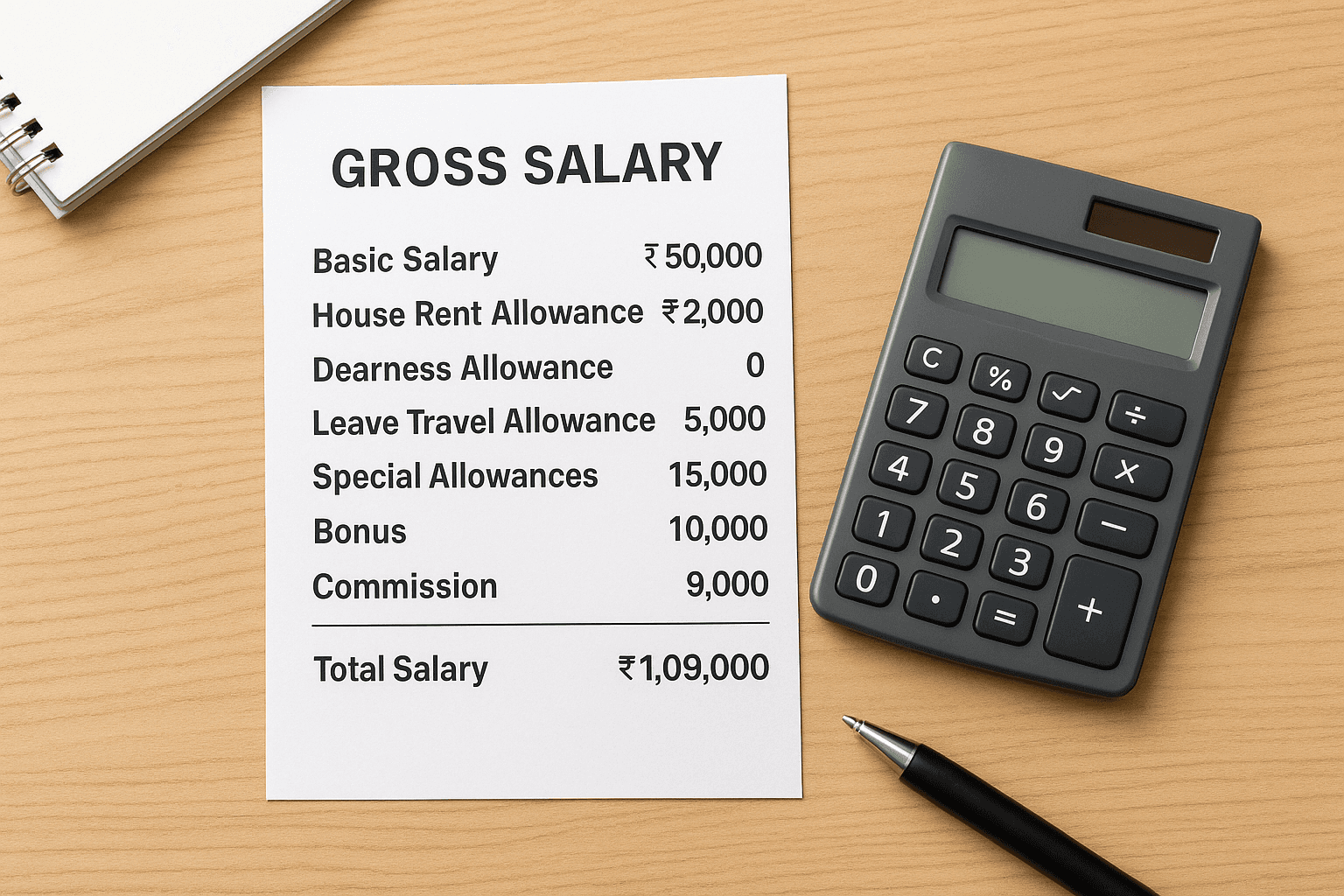

Step 1. Calculate your gross salary

Your gross salary forms the foundation when you learn how to calculate taxable income from salary. This figure represents every rupee your employer pays you before any deductions, exemptions, or taxes get applied. Most people confuse gross salary with take-home pay, but they're completely different numbers.

Components of gross salary

Gross salary includes all monetary and non-monetary benefits you receive from your employer during the financial year. Your salary slip breaks this down into multiple components, each serving a specific purpose in your compensation structure.

Add these elements together to arrive at your total gross salary:

Basic salary: The fixed component forming 40-50% of your total compensation

House Rent Allowance (HRA): Monthly allowance for housing expenses

Dearness Allowance (DA): Cost of living adjustment (common in government jobs)

Leave Travel Allowance (LTA): Reimbursement for travel during leave

Special allowances: Transport allowance, medical allowance, or other fixed payments

Bonus: Annual or performance-based bonuses

Commission: Variable pay based on targets or sales

Employer's contribution to provident fund: The amount your company deposits into your PF account

Your Form 16 Part B shows the complete breakup of all salary components under different heads.

Calculate the total

Take your April 2025 salary slip. Suppose your basic salary is ₹50,000, HRA is ₹20,000, special allowance is ₹15,000, and LTA is ₹5,000. Your monthly gross equals ₹90,000. Multiply by 12 months to get your annual gross salary of ₹10,80,000. Add any bonus received during the year to this figure for your final gross salary amount.

Step 2. Subtract exemptions and standard deduction

After calculating your gross salary in Step 1, you move to subtracting allowable exemptions and the standard deduction. This step reduces your taxable base significantly, but only if you understand which components qualify. The old tax regime permits numerous exemptions, while the new regime restricts most of them except the standard deduction.

Standard deduction

Every salaried individual gets a standard deduction of ₹50,000 per year under both tax regimes. You don't need to submit any proof or receipts to claim this amount. Your employer automatically applies this deduction when calculating TDS throughout the year, reducing your taxable income before tax gets withheld from your monthly salary.

If your annual gross salary is ₹10,80,000, subtract ₹50,000 immediately. Your income after standard deduction becomes ₹10,30,000. This flat deduction replaces the older transport and medical reimbursement exemptions that existed before 2018.

Common salary exemptions

Under the old tax regime, you can claim exemptions on specific allowances. House Rent Allowance qualifies for exemption based on the least of three amounts: actual HRA received, rent paid minus 10% of basic salary, or 50% of basic salary for metro cities (40% for non-metros). Leave Travel Allowance exempts actual travel costs for two journeys in a block of four years.

Calculate your HRA exemption with this example: If your basic salary is ₹50,000 monthly, HRA received is ₹20,000, and actual rent paid is ₹18,000, compare these three figures. Actual HRA is ₹20,000, rent minus 10% of basic equals ₹13,000 (₹18,000 - ₹5,000), and 50% of basic is ₹25,000. The exemption equals ₹13,000 monthly or ₹1,56,000 annually.

Choosing the new tax regime forfeits most exemptions except the standard deduction, so compare both regimes before deciding.

Subtract total exemptions and standard deduction from your gross salary. Using the earlier example of ₹10,80,000 gross, subtract ₹50,000 (standard) and ₹1,56,000 (HRA). Your income now stands at ₹8,74,000 before claiming any deductions.

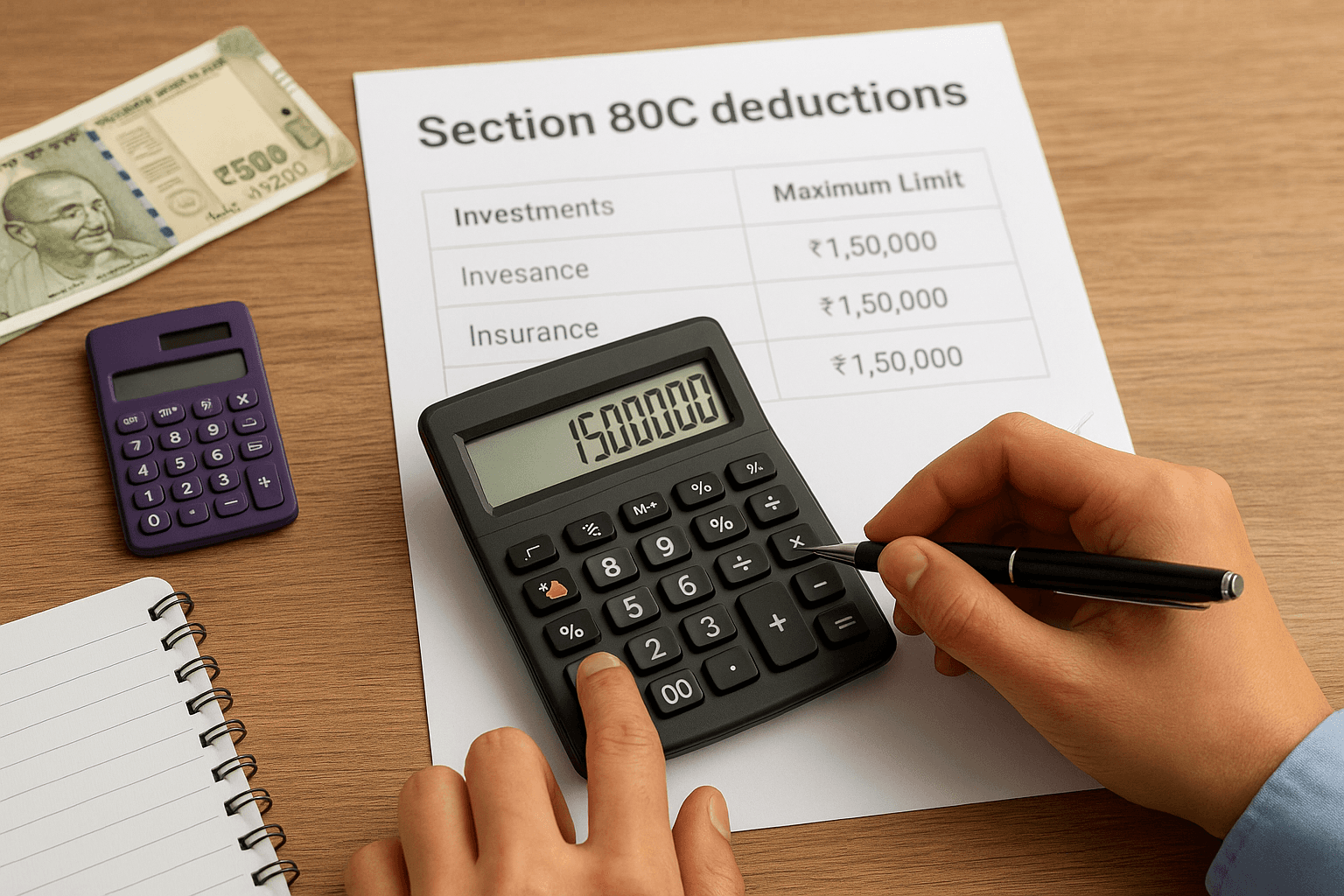

Step 3. Claim deductions under Chapter VI-A

After subtracting exemptions in Step 2, you claim deductions under Chapter VI-A to further reduce your taxable income. These deductions apply only if you choose the old tax regime, and each section has specific limits and qualifying investments. Unlike exemptions that depend on your salary structure, deductions reward your financial decisions like saving, insuring, or donating.

Section 80C deductions

Section 80C offers the largest deduction opportunity at ₹1,50,000 per year. Your investments in Employee Provident Fund (EPF), Public Provident Fund (PPF), Equity Linked Savings Schemes (ELSS), life insurance premiums, National Savings Certificate (NSC), and home loan principal repayment all qualify under this single limit. You combine all these investments, but the total deduction caps at ₹1,50,000.

Calculate your 80C deduction using actual investments. If you contributed ₹1,00,000 to EPF throughout the year, paid ₹30,000 in life insurance premiums, and invested ₹50,000 in ELSS, your total is ₹1,80,000. You claim only ₹1,50,000 as the deduction since that's the maximum limit.

Other key deductions

Beyond 80C, you claim additional deductions that don't share the same limit. Section 80D allows ₹25,000 for health insurance premiums (₹50,000 if you're a senior citizen), while Section 80CCD(1B) permits an extra ₹50,000 for National Pension System contributions. Section 80TTA exempts ₹10,000 of savings account interest.

Section | Purpose | Maximum Limit |

|---|---|---|

80C | Investments, insurance, loan principal | ₹1,50,000 |

80CCD(1B) | NPS contributions | ₹50,000 |

80D | Health insurance premiums | ₹25,000/₹50,000 |

80TTA | Savings account interest | ₹10,000 |

Keep all investment proofs and receipts organized because your employer needs them to adjust TDS, and you'll need them when filing returns.

Step 4. Compute tax liability using slab rates

You've subtracted exemptions and claimed deductions from your gross salary. Now you apply tax slab rates to the remaining amount, which is your final taxable income. This step transforms your income figure into the actual tax you owe to the government. The calculation differs based on whether you chose the old or new tax regime, since each uses different slab structures.

Tax slab rates for 2025-26

The old tax regime uses these progressive slabs for individuals below 60 years:

Income Range | Tax Rate |

|---|---|

Up to ₹2,50,000 | Nil |

₹2,50,001 to ₹5,00,000 | 5% |

₹5,00,001 to ₹10,00,000 | 20% |

Above ₹10,00,000 | 30% |

The new tax regime offers lower rates but restricts deductions. Under the new system, income up to ₹3,00,000 attracts no tax, followed by 5% up to ₹7,00,000, 10% up to ₹10,00,000, 15% up to ₹12,00,000, 20% up to ₹15,00,000, and 30% beyond that.

Calculate tax step by step

Take your taxable income after all deductions. If you started with ₹8,74,000 and claimed ₹1,50,000 under 80C plus ₹25,000 under 80D, your final taxable income equals ₹6,99,000. Apply the old regime slabs: zero tax on first ₹2,50,000, then 5% on the next ₹2,50,000 (₹12,500), and 20% on the remaining ₹1,99,000 (₹39,800). Your total tax equals ₹52,300 before adding cess of 4%, bringing your final liability to ₹54,392.

Round off your final tax amount to the nearest rupee when filing returns to match government requirements.

Smart tax planning

Understanding how to calculate taxable income from salary gives you control over your finances instead of blindly trusting your employer's TDS calculations. You can now verify every deduction, spot errors before they compound, and plan your investments strategically throughout the year rather than scrambling in March to save tax. This knowledge transforms you from a passive taxpayer into an informed decision-maker.

Regular tax planning beats last-minute panic. Review your salary components each quarter, track your investment contributions monthly, and adjust your Section 80C allocations based on your actual spending patterns. This proactive approach maximizes your take-home income while staying fully compliant with tax laws.

Professional guidance makes tax optimization simpler. Sign up with Invsify to access AI-powered tax planning insights, personalized recommendations based on your salary structure, and expert advice that identifies opportunities you might miss calculating manually. Smart investors plan their taxes continuously, not just during filing season.