How To Choose Index Funds In India: A Simple Checklist

Shlok Sobti

How To Choose Index Funds In India: A Simple Checklist

Index funds have become one of the most popular investment choices for Indian investors, and for good reason. Low costs, built-in diversification, and zero dependency on a fund manager's stock-picking skills make them hard to ignore. But here's the catch: there are now hundreds of index funds available across AMCs in India, and not all of them are created equal. Knowing how to choose index funds in India comes down to a handful of specific factors that most investors either overlook or don't know about, things like tracking error, expense ratios, and AUM thresholds.

Picking the wrong index fund can quietly eat into your returns over years, even though the fund technically tracks the same benchmark as a better alternative. The difference between a well-run index fund and a mediocre one might look small on paper, say, 0.2% in annual tracking error, but compounded over a decade, that gap can cost you lakhs. This is exactly why a structured checklist matters more than gut feeling or brand loyalty when selecting an index fund.

At Invsify, we help Indian investors cut through this noise with AI-powered, conflict-free investment advisory, registered with SEBI, with no hidden commissions influencing our recommendations. This guide gives you the exact checklist we'd want every investor to use: a clear, step-by-step framework to evaluate and compare index funds so you can invest with confidence. Let's get into it.

What you need before you compare funds

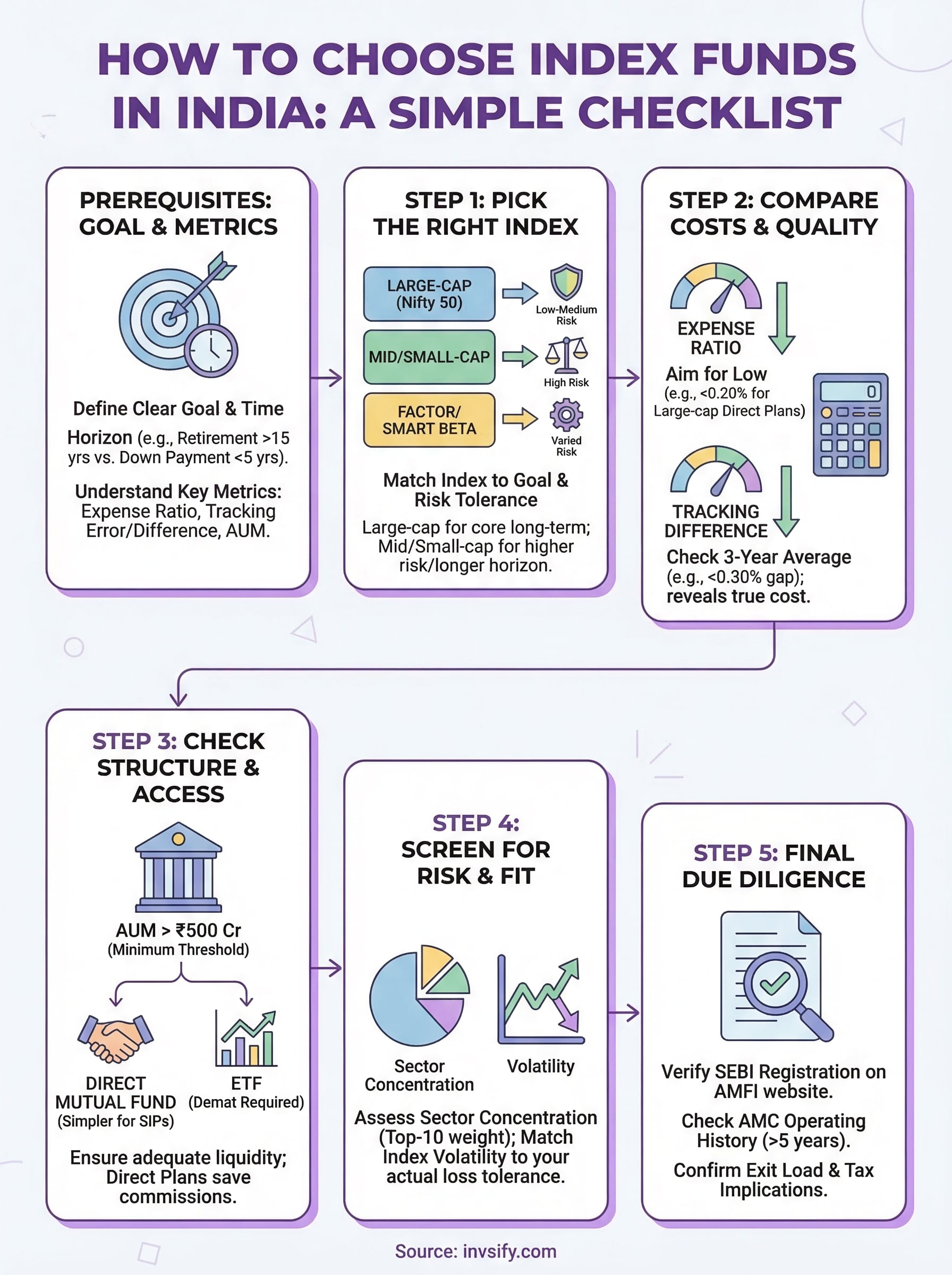

Before you open a fund comparison tool or scan through AMC websites, you need two things sorted: a clear financial goal and a working understanding of the metrics you'll use to evaluate funds. Without these, you'll either pick a fund that doesn't fit your situation or get overwhelmed and default to a brand name you recognize. Neither approach serves your long-term returns well, and the cost of a mismatched fund compounds quietly over years.

Know your goal and time horizon

Your goal shapes every decision in this process. A person saving for retirement in 25 years has almost nothing in common with someone parking money for 3 years before a house down payment, even if both are considering index funds. The goal determines which index to target, which fund category to consider, and how much short-term volatility you can absorb without reacting emotionally and pulling out at the wrong time.

Your investment horizon is one of the most important filters you'll apply before comparing funds. Short horizons under five years reduce the case for equity index funds significantly, while longer horizons make them far more compelling.

Work through this template before you compare any fund:

Question | Your Answer |

|---|---|

What is this investment for? | e.g., retirement, child's education, house down payment |

When will you need this money? | e.g., 5 years, 15 years, 25 years |

How much can you invest monthly? | e.g., ₹5,000 via SIP |

How much loss can you tolerate in a bad year? | e.g., comfortable with -20%, not with -10% |

Filling this in before you compare funds stops you from choosing a fund based on recent performance rather than actual fit. Most investors skip this step and then wonder why their portfolio doesn't match their expectations three years later.

Understand the four key metrics

Most first-time index fund investors know about expense ratio and stop there. To properly understand how to choose index funds in India, you need four specific metrics, not just one. Each one tells you something different about a fund's quality and cost.

Metric | What It Measures | Why It Matters |

|---|---|---|

Expense Ratio | Annual fee charged by the AMC as a percentage of AUM | Directly reduces your return every single year |

Tracking Error | Standard deviation of daily return differences between fund and index | Shows how consistently the fund follows its benchmark |

Tracking Difference | Total gap between fund return and index return over a period | Reveals the actual cost of owning the fund vs holding the index |

AUM | Total money pooled in the fund | Very low AUM funds face liquidity risk and higher per-unit operational costs |

Tracking error and tracking difference are frequently confused, but they measure different things. Tracking error measures consistency, while tracking difference measures total cost. A fund can have low tracking error but still deliver meaningfully lower returns than its benchmark due to cash drag or transaction costs. You need both numbers together to get the full picture, and you'll use them directly in Step 2.

Know where to find the data

You don't need to rely on comparison blogs or advertised fund lists. AMC websites such as those for HDFC Mutual Fund, Nippon India, UTI, SBI, and Mirae Asset all publish monthly factsheets that include expense ratios, portfolio holdings, AUM figures, and benchmark details. The AMFI website at amfiindia.com publishes daily NAV data and scheme-level information for every SEBI-registered mutual fund in India, so it's a reliable starting point for raw numbers.

Tracking error data is not always displayed prominently on fund pages, but it appears in detailed factsheets and can also be calculated from historical NAV data if you want to verify it yourself. Before you work through the rest of this checklist, bookmark the AMFI website and pull up the factsheet page for at least one AMC you're considering. Starting with verified, primary source data rather than aggregated third-party summaries keeps your evaluation grounded in facts rather than marketing framing.

Step 1. Pick the right index for your goal

Choosing the right index is the foundation of the entire selection process. Before you can compare expense ratios or tracking errors, you need to know which benchmark your fund should follow in the first place. When people think about how to choose index funds in India, they often jump straight to fund comparison, skipping this step entirely. That mistake means a perfectly managed fund tracking the wrong index will underperform your expectations regardless of its quality.

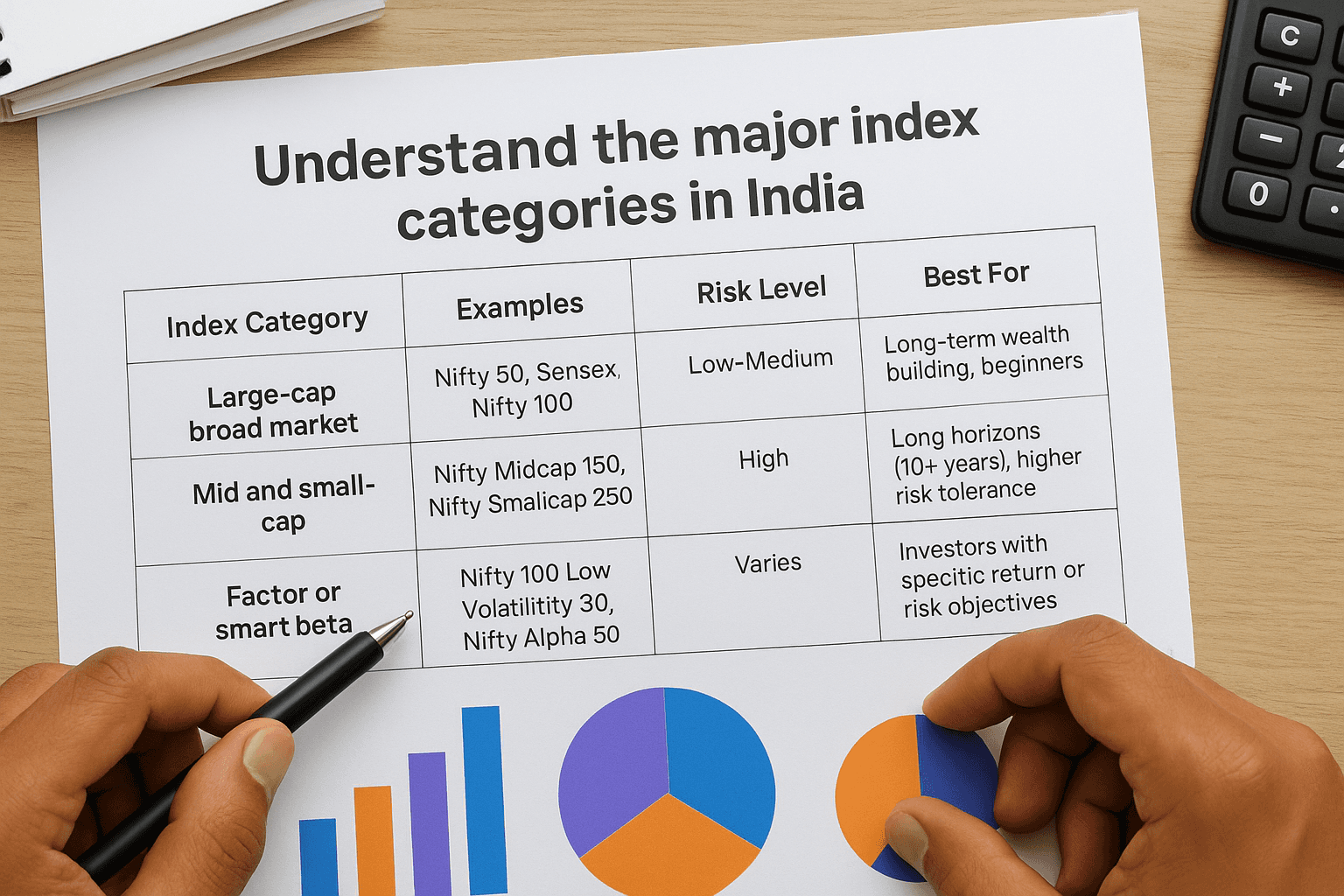

Understand the major index categories in India

Three broad categories of equity indices are available through Indian mutual funds today. Each carries a different risk-return profile and suits a different type of investor.

Index Category | Examples | Risk Level | Best For |

|---|---|---|---|

Large-cap broad market | Nifty 50, Sensex, Nifty 100 | Low-Medium | Long-term wealth building, beginners |

Mid and small-cap | Nifty Midcap 150, Nifty Smallcap 250 | High | Long horizons (10+ years), higher risk tolerance |

Factor or smart beta | Nifty 100 Low Volatility 30, Nifty Alpha 50 | Varies | Investors with specific return or risk objectives |

The Nifty 50 is the most commonly used benchmark for Indian large-cap index funds, covering the top 50 companies by market capitalisation listed on NSE. It is the most liquid, the most widely replicated, and carries the longest trackable history in India. For most first-time index fund investors with a horizon of 7 years or more, a Nifty 50 or Nifty 100 fund is the sensible starting point before exploring other categories.

Match the index to your actual goal

Your goal from the earlier planning step now becomes your filter here. If you are building a retirement corpus over 20 or more years, a combination of Nifty 50 and Nifty Next 50 gives you broad large-cap exposure with some growth bias built in. Targeting higher long-term growth while accepting higher short-term drawdowns opens the door to a Nifty Midcap 150 fund as part of your allocation, but only after your core large-cap position is established.

Adding a midcap index fund to a 3-year goal introduces volatility you don't need and cannot afford to absorb in that timeframe.

Use this matching guide before shortlisting any fund:

Under 5 years: Avoid pure equity index funds; consider debt index funds tracking Nifty G-Sec or SDL indices instead

5 to 10 years: Nifty 50 or Nifty 100 as your core holding

10 to 20 years: Nifty 50 as core, with Nifty Next 50 or Nifty Midcap 150 as a satellite position

20 or more years: A broader allocation including midcap and smallcap indices is reasonable given the long recovery runway

Step 2. Compare costs and tracking quality

Once you've identified the right index for your goal, cost comparison is where most of the practical work happens. Two funds tracking the exact same benchmark can produce meaningfully different outcomes for you over 10 or 15 years, purely because of expense ratio differences and tracking quality gaps. This step walks you through exactly what to compare and how to interpret the numbers.

Evaluate the expense ratio first

The expense ratio is the annual fee an AMC charges to manage the fund, expressed as a percentage of your invested amount. Even a difference of 0.10% to 0.20% between two Nifty 50 funds may seem trivial, but on a ₹10 lakh corpus held for 15 years, that gap compounds into a difference of tens of thousands of rupees. Always check the direct plan expense ratio, not the regular plan, since regular plans route through distributors and carry higher costs that reduce your net returns.

For large-cap index funds like Nifty 50 trackers, you should expect expense ratios between 0.05% and 0.20%. Any fund charging above 0.25% for a plain large-cap index fund warrants scrutiny. Use this as your benchmark when shortlisting:

Index Category | Acceptable Expense Ratio Range |

|---|---|

Nifty 50 / Sensex | 0.05% to 0.20% |

Nifty Next 50 / Nifty 100 | 0.15% to 0.30% |

Midcap / Smallcap index | 0.20% to 0.40% |

Factor / Smart Beta | 0.25% to 0.50% |

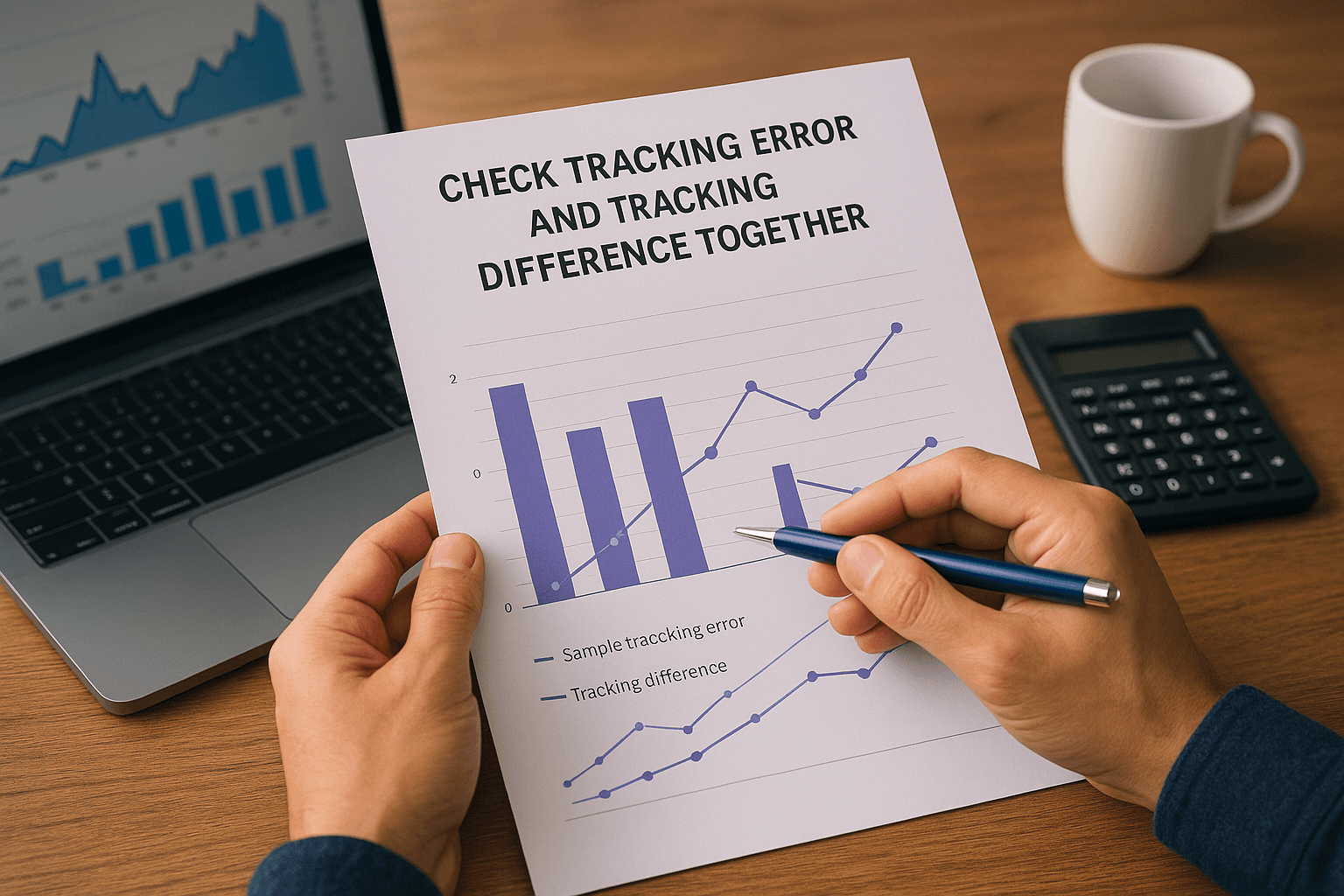

Check tracking error and tracking difference together

Tracking error alone does not tell the full story of how to choose index funds in India. A low tracking error only means the fund is consistent in following its benchmark, not that it is close to the benchmark's actual returns. Tracking difference is the number that reveals the true performance gap, showing you how much the fund underperformed or overperformed the index over a full year, while tracking error only measures the consistency of that deviation.

A fund with a tracking error of 0.05% but a tracking difference of 0.40% is consistently delivering returns well below its benchmark. That 0.40% gap is your real annual cost of ownership.

Look for funds where tracking difference stays below 0.30% for large-cap indices over a three-year period. Pull the fund's annual factsheet from the AMC website, compare the fund's CAGR against the benchmark CAGR for the same period, and calculate the gap yourself. Any fund where tracking difference consistently exceeds tracking error by a wide margin is likely dealing with cash drag or operational inefficiencies that will keep working against your returns year after year.

Step 3. Check the fund structure and access

Cost and tracking quality matter, but a fund you can't easily access or one with structural weaknesses will create real friction and financial risk. This step covers fund size, plan type, and investment route, three structural factors that determine whether a fund actually works in practice for your situation when learning how to choose index funds in India.

Check AUM and liquidity thresholds

AUM, or assets under management, is not just a prestige metric. A fund with very low AUM faces real operational problems: higher per-unit transaction costs during rebalancing, difficulty maintaining exact index weights, and a genuine risk of the AMC shutting down or merging the scheme if it stays commercially unviable. For equity index funds, a minimum AUM of ₹500 crore is a reasonable threshold before you consider a fund worth adding to your shortlist.

Funds with AUM below ₹100 crore are particularly vulnerable to being wound up or merged into a larger scheme, which can trigger unexpected capital gains tax events for you as an investor.

Use this quick AUM filter when shortlisting funds:

Fund Category | Minimum AUM to Consider |

|---|---|

Nifty 50 / Sensex trackers | ₹1,000 crore or more |

Nifty Next 50 / Nifty 100 | ₹500 crore or more |

Midcap / Smallcap index | ₹500 crore or more |

Factor / Smart Beta | ₹300 crore or more |

Choose the right plan and access route

Direct plans always cost less than regular plans because they cut out the distributor commission entirely. When you invest through an AMC's own website or a platform offering direct plans, you get a lower expense ratio on the same underlying fund. The difference looks small on paper, but on a ₹5,000 monthly SIP held for 15 years, even 0.5% saved annually compounds into a significantly larger final corpus.

You also need to decide between a mutual fund index scheme and an ETF tracking the same index. Both can work, but they operate differently. Mutual fund index schemes let you invest via SIP without a demat account, while ETFs require a demat account and trade like stocks on an exchange with brokerage costs on every purchase. For most salaried investors running a monthly SIP, a direct plan mutual fund index scheme offers simpler, more automated access with no per-transaction brokerage eating into your returns.

Step 4. Screen for risk and diversification fit

Buying an index fund does not automatically mean you are well-diversified. The index itself may be heavily concentrated in a few sectors or companies, which can expose your portfolio to risks that don't show up until markets turn against those sectors. This step shows you how to choose index funds in India by evaluating whether the fund's underlying index actually adds diversification to your portfolio or just duplicates what you already hold.

Measure concentration risk in the underlying index

Every index has a top-10 holdings weight you can check in the factsheet. For the Nifty 50, the top 10 stocks often account for over 60% of the index weight, meaning your returns will be heavily tied to a handful of large financial and IT companies. That is not inherently bad, but you need to understand it before you commit. If your existing portfolio already has high exposure to banking stocks, adding a Nifty Bank index fund compounds your concentration problem rather than spreading it.

Two index funds can track completely different-sounding benchmarks yet hold nearly identical top-10 stocks, making your portfolio look diversified when it is not.

Pull the sector breakdown table from any factsheet you are evaluating and check these two things:

Check | What to Look For |

|---|---|

Top-10 holdings weight | Below 55% is reasonable; above 65% signals high concentration |

Sector weight vs your existing portfolio | No single sector should dominate more than 35% of your total equity exposure |

Match volatility to your risk tolerance

Different indices carry different standard deviation profiles, which is a measure of how much the fund's returns swing in a given year. Nifty 50 funds have historically shown annualized standard deviations around 15% to 18%, while midcap and smallcap index funds can run well above 20%. A fund that looks attractive on return charts may require you to sit through a 30% to 40% drawdown in a bad year without selling. Most investors overestimate their ability to hold through that kind of loss.

Your planning template from Step 1 already captured how much annual loss you can tolerate without reacting. Use that number as a hard filter now. If you answered that a loss of more than 15% in any single year would push you to withdraw, eliminate any midcap or smallcap index funds from your shortlist immediately, regardless of their long-term return history. Match the volatility profile of the index to your actual behavior, not to the behavior you hope you will have under pressure.

Step 5. Do a quick final due diligence

You have now filtered by index fit, cost, structure, and risk. Before you commit any money, one final verification layer protects you from funds that look good on paper but carry hidden problems. This step takes 30 minutes at most, and it covers the three checks that most investors skip entirely because they feel like formality rather than necessity. They are not formality. They are the difference between choosing a fund you can hold confidently for 15 years and one that surprises you later.

Verify the AMC and scheme registration

Every mutual fund scheme available to Indian investors must be registered with SEBI, and you can confirm this directly. Visit the AMFI website at amfiindia.com, search for the scheme by name, and confirm it appears with an active status. Check the AMC's operating history as well. An AMC that has been running index funds for at least five years has demonstrated it can manage rebalancing events, corporate actions, and index reconstitutions without generating excessive tracking difference. Newer AMCs are not automatically disqualified, but a shorter track record means you have less evidence to evaluate.

Confirming SEBI registration takes two minutes and gives you a verified baseline that no amount of marketing material can substitute.

Run a final comparison checklist before you invest

When you understand how to choose index funds in India, the final step is bringing all your research into one structured comparison. Pull together every fund that has survived your earlier filters and score them against each other using this checklist before making a final decision:

Check | What to Confirm |

|---|---|

Expense ratio (direct plan) | Below your category threshold from Step 2 |

Tracking difference (3-year) | Below 0.30% for large-cap indices |

AUM | Above your category minimum from Step 3 |

Index match | Correct benchmark for your goal and timeline |

SEBI / AMFI registration | Active status confirmed on amfiindia.com |

AMC operating history | At least 5 years managing index schemes |

Sector concentration | No single sector above 35% of index weight |

Check exit load and tax implications before committing

Exit load is a redemption charge some AMCs apply if you sell within a set period, typically within 7 to 15 business days for most equity index funds. Confirm the exit load policy in the scheme information document before investing. Also confirm whether the fund is equity-oriented or debt-oriented since that determines your tax treatment. Equity index funds held over 12 months attract long-term capital gains tax at 12.5% above ₹1.25 lakh in a financial year, a detail worth factoring into your net return calculation before you finalize your choice.

Your index fund shortlist

You now have a complete, repeatable framework for how to choose index funds in India without relying on brand recognition or recent return charts. Work through each step in order: confirm your goal and timeline, pick the right benchmark, filter on expense ratio and tracking difference, verify fund structure and AUM, screen for concentration risk, and run the final due diligence checklist before committing a single rupee. Every filter you apply narrows your list to funds that actually fit your situation, rather than funds that simply look good on a comparison website.

If you want a second layer of confidence before you invest, AI-powered, conflict-free advisory from a SEBI Registered Investment Advisor can validate your shortlist against your complete financial picture. No distributor commissions, no hidden incentives pushing you toward a particular fund. Get personalized index fund guidance from Invsify and invest knowing your choice was built on verified data, not guesswork.