How to Choose Mutual Funds in India: Categories & Criteria

Shlok Sobti

How to Choose Mutual Funds in India: Categories & Criteria

With over 40 fund houses and more than 1,500 mutual fund schemes available in India, you face an overwhelming number of choices. Each scheme promises attractive returns, but picking the wrong one can cost you years of compounding or expose you to risks you never intended to take. Most investors end up selecting funds based on recent performance or tips from friends, without really understanding what fits their own situation.

The right way to choose starts with getting clear on your goals and how much risk you can handle. Then you match those to specific fund categories and filter using objective criteria. You need to look beyond star ratings and past returns to things like expense ratios, fund manager experience, portfolio composition, and how taxes will affect your gains.

This guide gives you a five step framework for choosing mutual funds that actually align with your financial needs. You'll learn how to evaluate fund categories, dig into performance metrics, compare costs across schemes, and use practical checklists to invest with confidence rather than guesswork.

What you must know about mutual funds in India

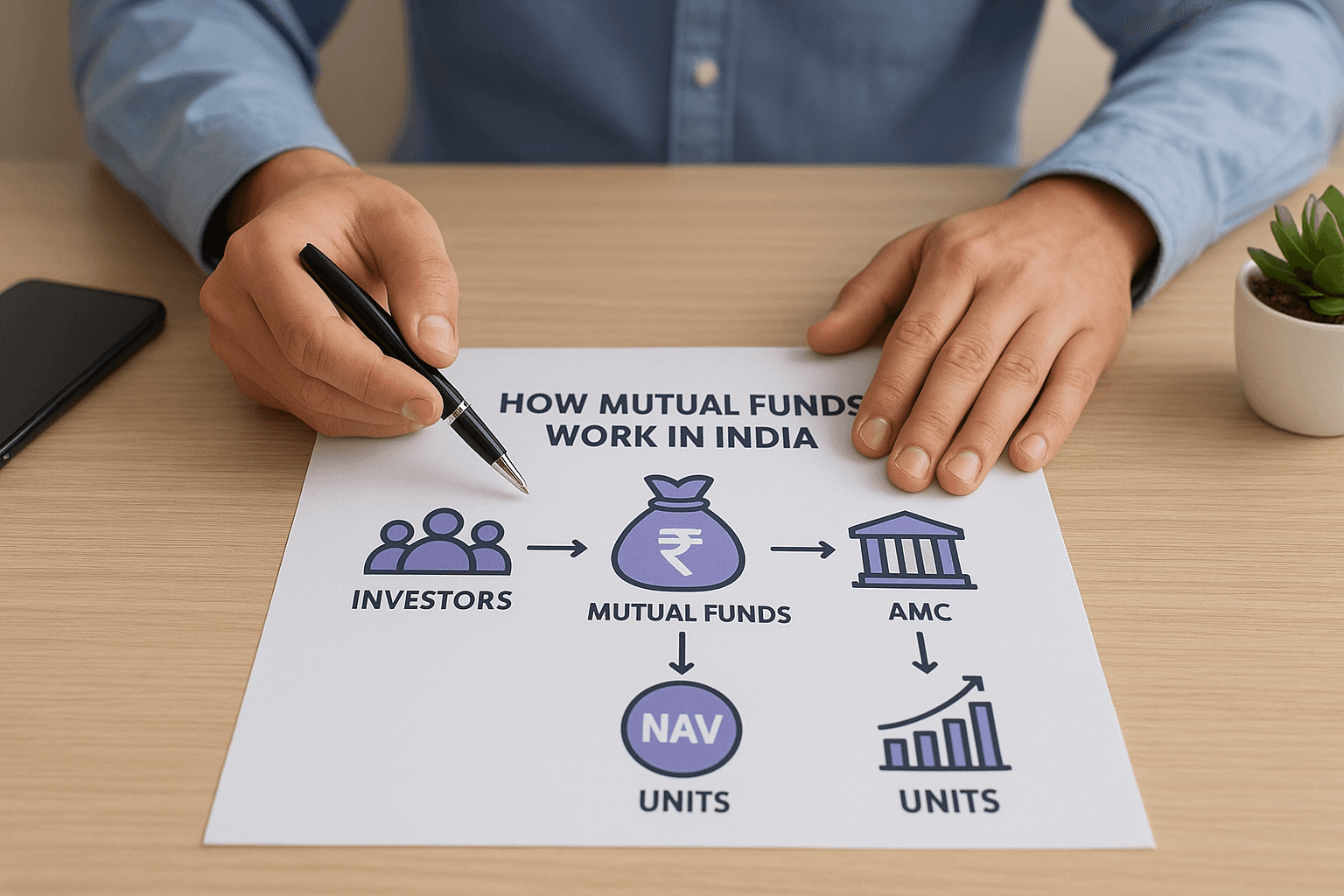

A mutual fund pools money from multiple investors to invest in a diversified basket of stocks, bonds, or other securities. Professional fund managers make all investment decisions on your behalf, and you own units proportional to your investment. When the value of the underlying securities rises or falls, your Net Asset Value (NAV) per unit changes accordingly, reflecting your gains or losses.

How mutual funds work in India

You buy units of a mutual fund scheme at the prevailing NAV. The Asset Management Company (AMC) takes your money along with funds from thousands of other investors and deploys it according to the scheme's stated objective. If you invest Rs. 10,000 in a fund with a NAV of Rs. 50, you receive 200 units. As the fund's portfolio grows, your NAV increases, and you can sell your units back to the fund or on the stock exchange (in case of closed-end funds).

Indian mutual funds come in open-ended and closed-ended structures. Open-ended funds let you buy or redeem units any business day at the current NAV. Closed-ended funds have a fixed maturity period (typically 3 to 5 years) and list on stock exchanges, where you must sell to other investors if you want to exit early.

SEBI regulations and investor protection

The Securities and Exchange Board of India (SEBI) regulates all mutual funds in India. Every AMC must register with SEBI and follow strict disclosure norms about portfolio holdings, expense ratios, and fund manager changes. SEBI mandates that funds publish their complete portfolio every six months and NAV daily, giving you full transparency into where your money sits.

SEBI requires at least two-thirds of trustees to be independent, ensuring that fund houses cannot misuse investor capital.

Investor protection extends to segregated custody of assets. A separate custodian (usually a bank) holds all securities, preventing the AMC from accessing them directly. This three-tier structure of sponsor, trustees, and AMC creates checks and balances that protect your investment from fraud or mismanagement.

Types of schemes and investment approaches

Mutual funds in India offer growth plans and dividend plans. Growth plans reinvest all profits back into the scheme, compounding your returns over time. Dividend plans distribute profits periodically, giving you regular payouts but reducing the capital available for compounding. You also choose between regular plans (with distributor commissions) and direct plans (no intermediary, lower costs), where direct plans typically deliver 0.5% to 1% higher annual returns due to lower expense ratios.

Understanding how to choose mutual funds begins with grasping these structural basics, because the fund's category, cost structure, and regulatory framework all impact your eventual returns and safety.

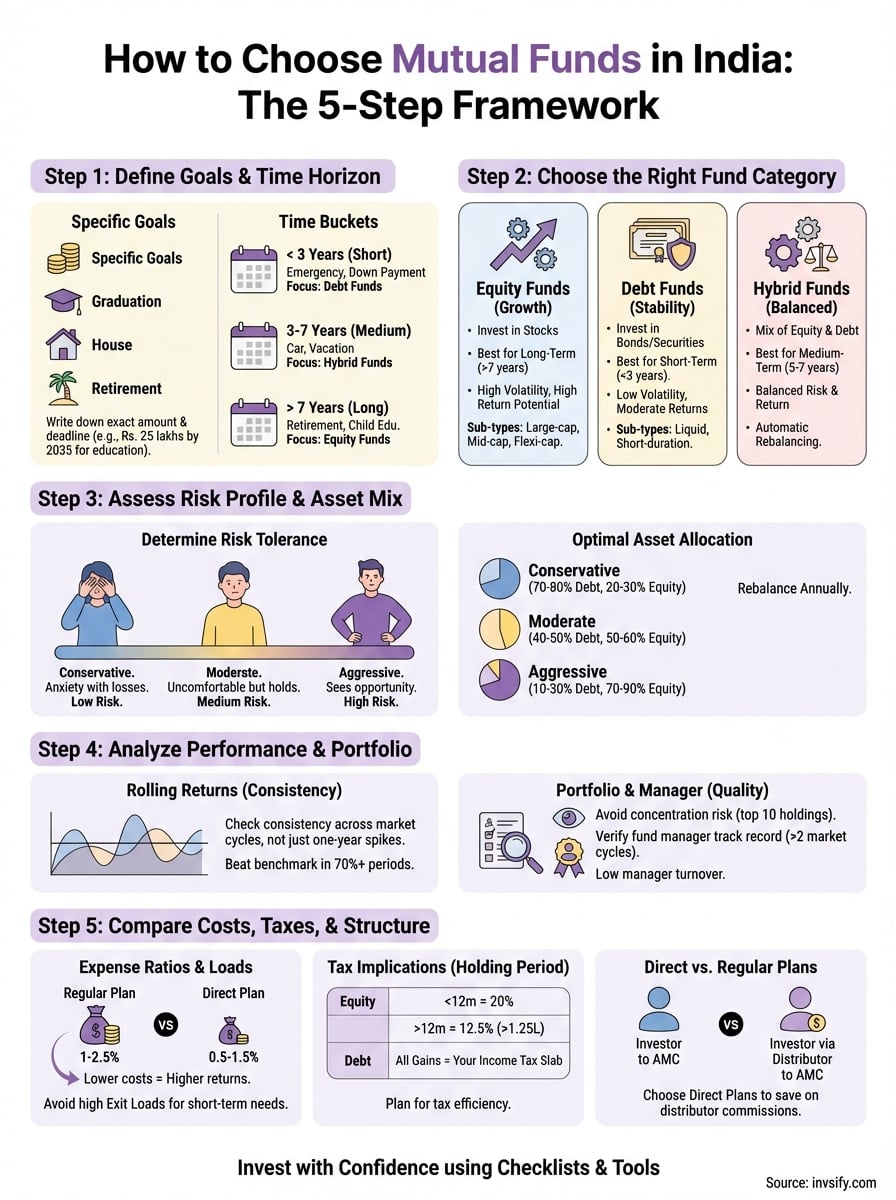

Step 1. Define your goals and time horizon

Your financial goals determine which mutual funds will actually work for you. Without clarity on what you're saving for and when you need the money, you'll end up chasing returns in funds that don't match your situation. A fund that performs brilliantly for retirement savings might be completely wrong for your daughter's college tuition in three years.

Write down specific financial targets

Start by listing each goal with an exact rupee amount and a deadline. Instead of "I want to save for my child's education," write "I need Rs. 25 lakhs by June 2035 for undergraduate fees." This precision lets you calculate how much to invest monthly and what return rate you need to reach that target.

Clear financial targets turn vague wishes into actionable investment plans.

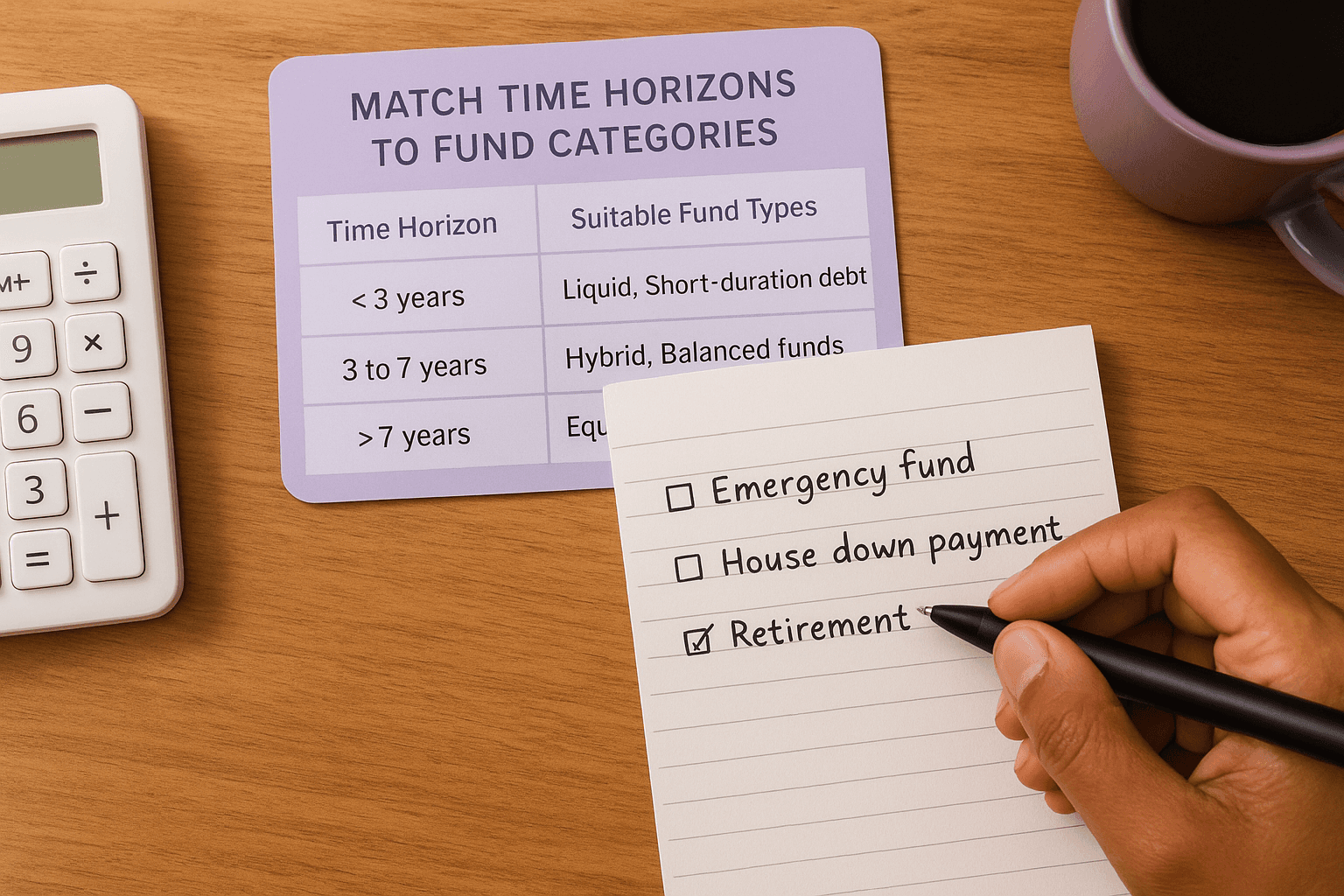

Create separate buckets for short-term goals (less than 3 years), medium-term goals (3 to 7 years), and long-term goals (beyond 7 years). Your emergency fund or a house down payment in two years belongs in short-term, while retirement or a child's higher education sits in long-term. Each bucket will need different fund categories with appropriate risk profiles.

Match time horizons to fund categories

The length of time you can stay invested determines how much equity exposure you can handle. Equity funds fluctuate sharply in the short run but historically deliver higher returns over 7+ years. If you need money within two years, you cannot afford a market crash eating into your principal right before withdrawal.

Use this framework when deciding how to choose mutual funds based on your timeline:

Time Horizon | Suitable Fund Types | Typical Equity Allocation |

|---|---|---|

< 3 years | Liquid, Short-duration debt | 0% to 20% |

3 to 7 years | Hybrid, Balanced funds | 30% to 60% |

> 7 years | Equity, Flexi-cap funds | 70% to 100% |

Match each of your written goals to one of these time buckets before you start comparing individual schemes.

Step 2. Choose the right fund category

Once you know your goals and timelines, you need to map them to the correct fund categories. Indian mutual funds fall into three broad types: equity, debt, and hybrid. Each category serves different purposes and comes with its own risk-return profile. Choosing the wrong category for your goal means either taking unnecessary risk or missing out on growth you could have captured.

Equity funds for growth-oriented goals

Equity funds invest primarily in stocks of companies and aim for capital appreciation over the long term. You should consider these funds only for goals that are at least seven years away, because they experience significant volatility in shorter periods. Market corrections can pull your portfolio down by 20% or more in a single year, but history shows that equity funds have delivered 12% to 15% annual returns over ten-year periods.

Within equity funds, you'll find multiple subcategories based on company size and investment style:

Equity Fund Type | Focus Area | Best For |

|---|---|---|

Large-cap | Top 100 companies | Steady growth, lower volatility |

Mid-cap | 101st to 250th largest companies | Higher growth potential, moderate risk |

Small-cap | Companies beyond 251st rank | Maximum growth, highest volatility |

Flexi-cap | Mix across all market caps | Balanced equity exposure |

Sectoral/Thematic | Specific industries (pharma, IT, banking) | Tactical bets, higher risk |

Pick large-cap or flexi-cap funds for your first equity investment. Avoid sectoral funds unless you have deep knowledge of that industry and can monitor performance actively.

Debt funds for stability and liquidity

Debt funds invest in fixed-income securities like government bonds, corporate debentures, and money market instruments. These funds suit goals under three years or portions of your portfolio where you cannot afford volatility. Returns typically range from 6% to 9% annually, depending on interest rate movements and credit quality of holdings.

Understanding how to choose mutual funds in the debt category requires looking at maturity profiles. Liquid funds hold securities that mature within 91 days and work well for your emergency fund. Short-duration funds (1 to 3 year maturity) fit goals like a vacation or car down payment in two years. Corporate bond funds offer slightly higher returns but carry credit risk if companies default on payments.

Debt funds are not risk-free; interest rate changes can cause temporary losses in longer-duration funds.

Check the credit rating of the fund's portfolio before investing. Stick to funds holding mostly AAA-rated and government securities if you need predictable returns.

Hybrid funds for balanced exposure

Hybrid funds combine equity and debt in a single scheme, giving you diversification without managing multiple funds yourself. Aggressive hybrid funds keep 65% to 80% in equity and work for moderate-term goals (5 to 7 years). Conservative hybrid funds hold only 10% to 25% equity, suitable when you want slightly better returns than pure debt but cannot handle full equity swings.

These funds automatically rebalance between asset classes, which saves you the effort of adjusting allocations as market conditions change.

Step 3. Assess your risk profile and asset mix

Your risk tolerance dictates how much volatility you can stomach without panicking and selling at the wrong time. Even if your goal sits ten years away, you might lose sleep watching your portfolio drop 30% in a market crash. Understanding how to choose mutual funds requires honest self-assessment of your emotional capacity to handle losses, not just your theoretical ability to stay invested long term.

Determine your risk tolerance

Start by asking yourself how you would react if your Rs. 10 lakh investment suddenly became Rs. 7 lakhs in six months. Conservative investors feel severe anxiety and might exit immediately, locking in losses. Moderate investors feel uncomfortable but can hold through corrections if they believe in the long-term plan. Aggressive investors see the drop as a buying opportunity and stay calm or even invest more.

Your age, income stability, existing savings, and financial dependents all shape your risk capacity. A 30-year-old professional with steady income and no dependents can take more risk than a 55-year-old approaching retirement with limited savings. Consider both your psychological comfort with losses and your actual financial situation.

Risk tolerance isn't just about what losses you can afford financially but what keeps you awake at night emotionally.

Take SEBI-approved risk profiling questionnaires that most fund houses offer during onboarding. These tools rate you as conservative, moderate, or aggressive based on your answers about investment experience, reaction to losses, and financial situation.

Calculate your optimal asset allocation

Once you know your risk profile, translate it into specific percentage allocations between equity and debt. This asset mix becomes your blueprint for selecting funds across categories. A conservative investor might hold 20% equity and 80% debt, while an aggressive investor with a long horizon could go 90% equity and 10% debt.

Use this framework to set your starting allocation:

Risk Profile | Equity Allocation | Debt Allocation | Suitable For |

|---|---|---|---|

Conservative | 20% to 30% | 70% to 80% | Nearing goals, low risk appetite |

Moderate | 50% to 60% | 40% to 50% | Medium-term goals, balanced approach |

Aggressive | 70% to 90% | 10% to 30% | Long horizon, high risk capacity |

Apply different allocations to different goals based on their timelines. Your retirement fund twenty years away can sit at 80% equity, while your house down payment in five years needs 40% equity maximum. Review and rebalance your asset mix annually as you age or as goals approach, gradually shifting from equity to debt to protect accumulated gains.

Step 4. Analyze fund performance and portfolio

Past performance does not guarantee future returns, but it reveals how a fund manager navigates different market conditions. You need to dig deeper than the headline returns displayed on fund fact sheets. Raw numbers can mislead if you only compare annual returns without understanding the underlying portfolio quality, consistency across cycles, or the risks taken to achieve those gains.

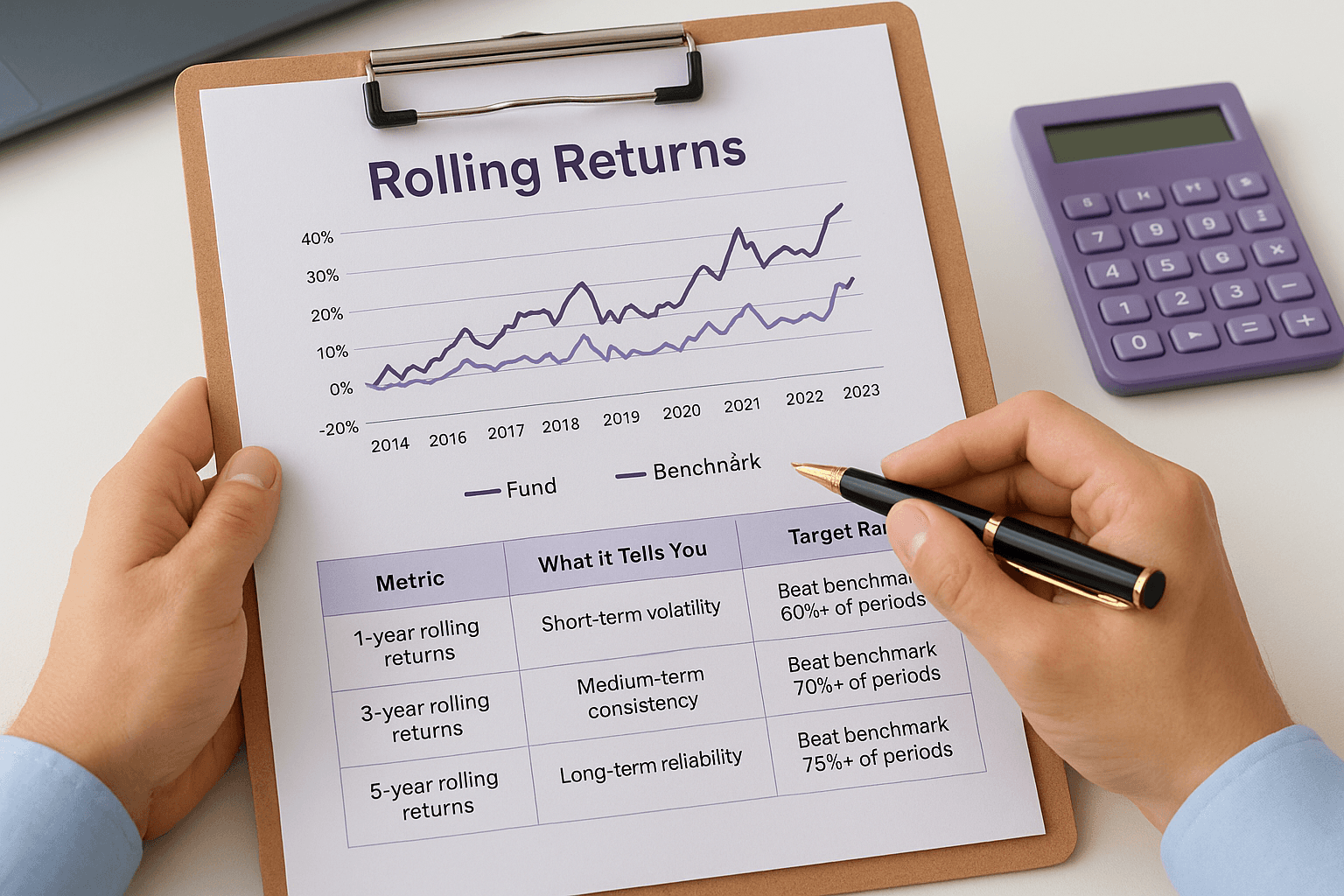

Check rolling returns across market cycles

Rolling returns show you how a fund performed over multiple overlapping periods instead of just one fixed timeframe. A fund might show 15% returns over the last five years, but rolling returns reveal whether it delivered consistently or had one exceptional year that inflated the average. Calculate returns for every possible five-year period within the last ten years to spot patterns.

Look for funds that beat their benchmark index in at least 70% of rolling periods. This consistency matters more than topping the charts in a single bull market. Compare returns during both rising and falling markets to see how the fund protects capital when conditions turn negative.

Metric to Check | What It Tells You | Target Range |

|---|---|---|

1-year rolling returns | Short-term volatility | Beat benchmark 60%+ of periods |

3-year rolling returns | Medium-term consistency | Beat benchmark 70%+ of periods |

5-year rolling returns | Long-term reliability | Beat benchmark 75%+ of periods |

Understanding how to choose mutual funds requires looking beyond promotional material showing only the best time periods.

Examine portfolio holdings and concentration

Download the fund's latest portfolio disclosure from the AMC website or SEBI's mutual fund portal. Check the top ten holdings to understand where the fund manager places the biggest bets. If three stocks account for 30% of the portfolio, you face concentration risk that could hurt badly if those companies underperform.

Verify that equity funds actually hold stocks matching their stated category. Some mid-cap funds drift into small-caps chasing higher returns, exposing you to risks you never signed up for. Count the total number of stocks in the portfolio; anything below 30 stocks in a diversified equity fund suggests poor diversification.

A well-diversified equity fund typically holds 50 to 80 stocks across multiple sectors, preventing any single company's failure from derailing your returns.

Compare sector allocation against the benchmark index. Overweight positions in cyclical sectors like real estate or metals indicate aggressive bets that could amplify losses during downturns.

Evaluate fund manager track record

The fund manager's experience directly impacts your returns. Check how long the current manager has run this specific fund, not just their total industry experience. A manager with ten years of experience but only six months on your fund means the historical performance you reviewed came from someone else's decisions.

Look for managers who have delivered consistent performance across at least two market cycles (one bull and one bear market). This proves they can adapt strategies as conditions change rather than riding luck during a single uptrend. Frequent manager changes signal instability and make past performance irrelevant for predicting future results.

Verify the manager's educational background and professional certifications like CFA or MBA. While degrees do not guarantee performance, they indicate serious commitment to investment management as a career rather than a temporary assignment.

Step 5. Compare costs, taxes and fund structure

Fees and taxes directly eat into your returns, compounding negatively over time just as your gains compound positively. A seemingly small 0.5% difference in annual expenses translates to lakhs of rupees lost over a 20-year investment horizon. When learning how to choose mutual funds, you must calculate the true cost of ownership across expense ratios, exit loads, and tax liability to understand what you actually keep after all deductions.

Decode expense ratios and loads

The expense ratio represents the annual fee charged as a percentage of your investment for fund management, administration, and distribution costs. Equity funds in India typically charge 1% to 2.5% for regular plans and 0.5% to 1.5% for direct plans. Debt funds charge lower ratios, usually between 0.5% to 1.5%. You pay this fee regardless of whether the fund makes or loses money, so lower expenses give you better odds of outperforming over time.

Calculate the actual rupee impact of expenses using this formula: If you invest Rs. 10 lakhs at 12% annual returns for 20 years, a fund with 1% expense ratio grows to Rs. 80.6 lakhs, while a fund with 2% expenses grows to only Rs. 67.3 lakhs. That Rs. 13.3 lakh difference comes purely from higher fees, not performance.

Check if the fund charges an exit load for redeeming units within a specified period. Most equity funds impose a 1% exit load if you withdraw within one year, penalizing short-term trading. Debt funds may charge exit loads for withdrawals within three to six months. These loads protect long-term investors from frequent redemptions that force managers to sell holdings prematurely.

Understand tax implications on different fund types

Tax treatment varies sharply between equity and debt funds based on your holding period. Equity funds (those with 65%+ equity allocation) qualify for long-term capital gains tax of 12.5% on profits exceeding Rs. 1.25 lakhs per year if you hold for more than 12 months. Short-term gains (holding under 12 months) face 20% tax regardless of profit amount.

Tax efficiency matters as much as gross returns because you only spend what remains after the government takes its share.

Debt funds now face taxation at your income tax slab rate for both short-term and long-term gains, after Budget 2023 removed indexation benefits. This makes debt funds less attractive for investors in higher tax brackets who might prefer fixed deposits or tax-free bonds instead.

Fund Type | Short-Term (< 12 months) | Long-Term (> 12 months) |

|---|---|---|

Equity funds | 20% flat | 12.5% on gains above Rs. 1.25L |

Debt funds | Your slab rate | Your slab rate |

Hybrid (equity-oriented) | 20% flat | 12.5% on gains above Rs. 1.25L |

Pick direct plans over regular plans

Direct plans remove the distributor commission that regular plans pay to brokers and financial advisors, typically saving you 0.5% to 1% annually in expense ratio. You invest directly through the AMC website or platforms that offer direct mutual funds. Both plan types hold identical portfolios managed by the same fund manager, so the only difference lies in costs.

Your Rs. 5 lakh invested at 12% returns over 15 years grows to Rs. 27.4 lakhs in a regular plan (2% expense ratio) but reaches Rs. 30.6 lakhs in a direct plan (1% expense ratio). That Rs. 3.2 lakh extra requires zero additional effort beyond selecting the direct option during purchase.

Additional tools and checklists for investors

You can streamline your fund selection process by using structured checklists and comparison tools that eliminate guesswork. These frameworks force you to evaluate every important parameter before committing money, preventing emotional decisions driven by marketing hype or recent performance spikes. Understanding how to choose mutual funds becomes easier when you follow repeatable processes that catch red flags early.

Use fund comparison worksheets

Create a simple spreadsheet template to compare up to five funds side by side across key metrics. List each criterion in rows and fund names in columns, making differences immediately visible. This visual comparison helps you spot which funds truly meet your requirements versus those that look good in only one or two areas.

Your comparison worksheet should include these evaluation points:

3-year and 5-year rolling returns vs benchmark

Expense ratio (direct plan)

Fund manager tenure on this specific scheme

Portfolio turnover ratio (lower indicates buy-and-hold strategy)

Standard deviation (measures volatility)

Sharpe ratio (risk-adjusted returns)

AUM size (avoid funds below Rs. 100 crores)

Exit load terms and minimum investment amount

Score each fund from 1 to 5 on every parameter, then calculate a total score to identify clear winners objectively.

Download portfolio review templates

Set up a quarterly review checklist that tracks whether your funds still align with your original goals and risk profile. Markets shift, fund managers change, and your life circumstances evolve, requiring periodic adjustments to stay on track. Schedule these reviews every three months in your calendar as non-negotiable appointments.

Regular portfolio reviews prevent drift from your investment plan and catch underperforming funds before they erode significant wealth.

Your review template should ask these questions: Has any fund underperformed its benchmark for three consecutive quarters? Did any fund manager change in the last quarter? Has your goal timeline shortened by a year, requiring asset allocation adjustment? Are any funds now exceeding 25% of your total portfolio due to outperformance? Document answers and action items each quarter to maintain discipline.

Moving forward with confidence

You now have a complete framework for evaluating mutual funds across categories, costs, and performance metrics. The five steps covered here remove guesswork from your investment decisions and help you build a portfolio aligned with your actual financial needs rather than market hype. Start by writing down your specific goals with exact amounts and deadlines, then systematically work through fund selection using the comparison worksheets and review checklists provided.

Knowing how to choose mutual funds puts you ahead of most retail investors who chase recent winners or follow tips without proper analysis. Your next action matters more than perfect knowledge. Begin with one fund that matches your largest financial goal and time horizon, then add others gradually as you gain confidence. If you want personalized recommendations based on your unique risk profile and goals, create your free Invsify account to access AI-powered insights that guide your fund selection process without hidden fees or commissions eating into your returns.