How To Claim HRA Exemption In India: Rules, Proof, ITR Steps

Shlok Sobti

How To Claim HRA Exemption In India: Rules, Proof, ITR Steps

If you're a salaried individual paying rent in India, you're likely leaving money on the table by not fully understanding how to claim HRA exemption. House Rent Allowance is one of the most valuable tax-saving components in your salary structure, yet many employees either skip it entirely or claim it incorrectly, resulting in unnecessary tax outgo.

The good news? Claiming HRA isn't complicated once you know the rules. You need to understand the eligibility criteria under Section 10(13A), gather the right documents, and follow the correct process with your employer or during ITR filing.

At Invsify, we help salaried professionals optimize every rupee of their income through smart, conflict-free financial advice. This guide breaks down everything you need to know about HRA exemption, from calculation methods and required documentation to the exact steps for claiming it. Whether you're renting from a landlord, family member, or paying rent in a metro city, you'll find clear answers here.

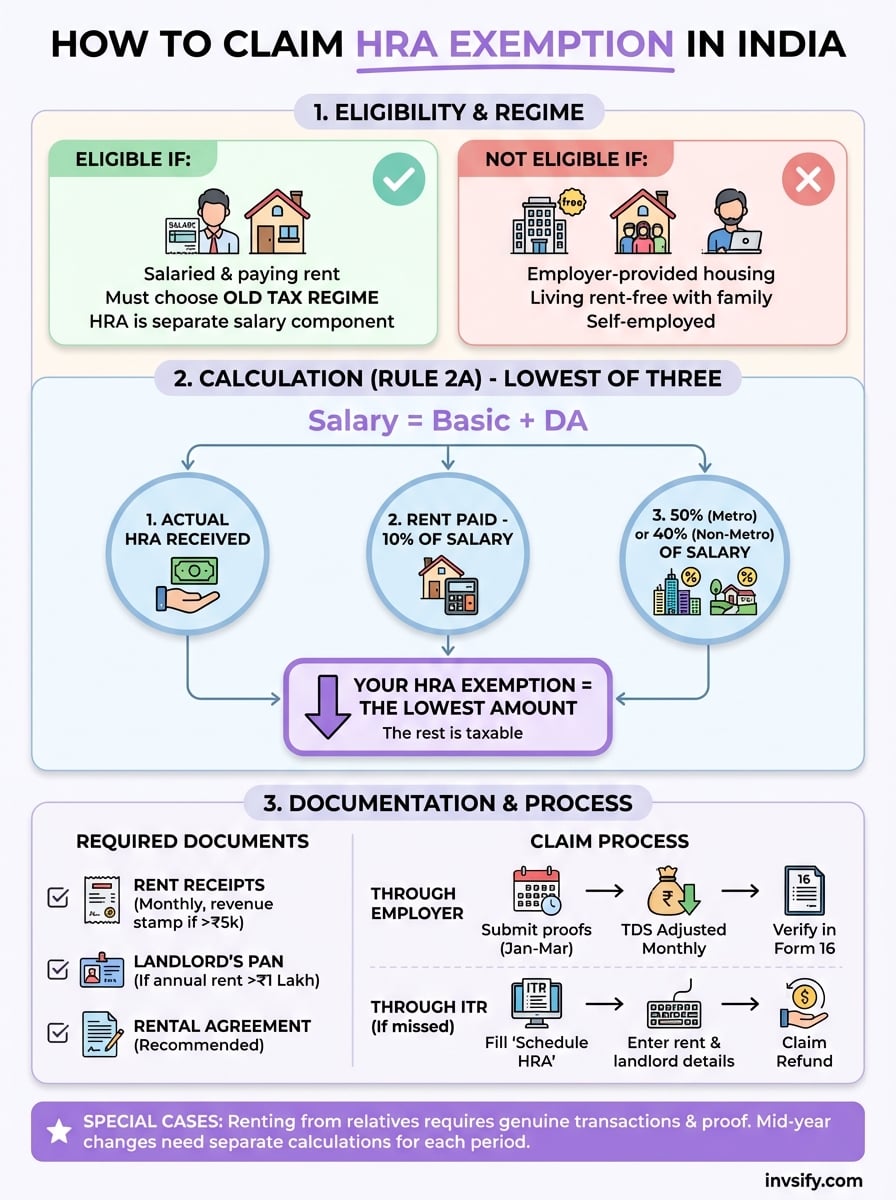

Check if you can claim HRA in the old regime

Before you learn how to claim HRA exemption, you need to confirm that you're eligible under the current tax framework. The most critical point here is your choice of tax regime. HRA exemption is available only if you opt for the old tax regime under Section 10(13A) of the Income Tax Act. If you've switched to the new tax regime introduced in Budget 2020 (and made the default from FY 2023-24), you lose access to this deduction entirely, along with most other exemptions and deductions.

This decision affects thousands of rupees in potential tax savings. You need to evaluate your entire salary structure, including components like LTA, Section 80C investments, and home loan interest, before choosing your regime. For most salaried employees paying rent in metro cities, the old regime remains more beneficial precisely because of HRA exemption availability.

Choosing the wrong tax regime can cost you ₹30,000 to ₹80,000 in annual tax savings, depending on your salary and rent payments.

Understanding the old tax regime requirement

You can claim HRA exemption only when you file your income tax return under the old tax regime. This means you retain access to all traditional deductions like Section 80C (up to ₹1.5 lakh), Section 80D (health insurance), and home loan interest under Section 24(b). The old regime uses tax slabs with rates starting at 5% for income above ₹2.5 lakh, moving up to 30% for income above ₹10 lakh.

Your employer will ask you to declare your preferred tax regime at the start of each financial year, typically through an investment declaration form. This choice applies to your entire salary income for that year. If you receive HRA in your salary slip and want the exemption, you must explicitly select the old regime during this declaration.

Switching regimes isn't permanent. You can change your choice every financial year when filing your ITR, giving you flexibility to optimize based on your changing financial situation. However, your employer's TDS calculations will follow whichever regime you declared at the year's start.

Basic eligibility criteria for HRA

Your employer must include HRA as a separate component in your salary structure. If your CTC shows only "basic salary" without a breakup, you cannot claim this exemption. Check your salary slip or appointment letter to confirm HRA exists as a distinct allowance.

You must actually pay rent for residential accommodation. This sounds obvious, but the tax department requires genuine rental payments, not just paper transactions. The accommodation can be a flat, house, hostel, or even a rented room, but it must be your residence, not a commercial property.

Living in your own house disqualifies you, even if you're paying an EMI. HRA and home loan interest are separate deductions serving different purposes. You can claim home loan interest under Section 24(b) in the old regime, but not HRA for the same property you own.

When you cannot claim HRA

Several situations make you ineligible for HRA exemption, regardless of your tax regime choice. If you live in accommodation provided by your employer where you pay a nominal license fee, you cannot claim HRA. The tax treatment for employer-provided housing follows different rules under Section 17.

You also lose HRA eligibility when you live rent-free in a property owned by family members without paying actual rent. While renting from parents or relatives is allowed (we'll cover this later), you must make genuine rent payments with proper documentation.

Self-employed professionals and business owners cannot claim HRA at all, as this exemption applies only to salaried individuals receiving HRA from an employer. If you earn freelance income or run a business, you can instead claim actual rent paid as a business expense under different sections, but not as HRA exemption under Section 10(13A).

Finally, if you're living abroad for work and paying foreign rent, you generally cannot claim HRA exemption in India unless your employer specifically includes foreign HRA in your salary structure and the payment qualifies under Indian tax rules. This requires detailed documentation and often professional tax advice.

Calculate your HRA exemption using Rule 2A

Once you confirm your eligibility, you need to calculate the actual tax-exempt amount using Rule 2A of the Income Tax Rules. This calculation determines how much of your HRA you can exclude from taxable income. The rule uses a three-way comparison method where you must identify the lowest amount among three different calculations, and that becomes your exemption. Understanding this formula is critical because it directly impacts your tax liability, and many employees either overclaim or underclaim due to incorrect calculations.

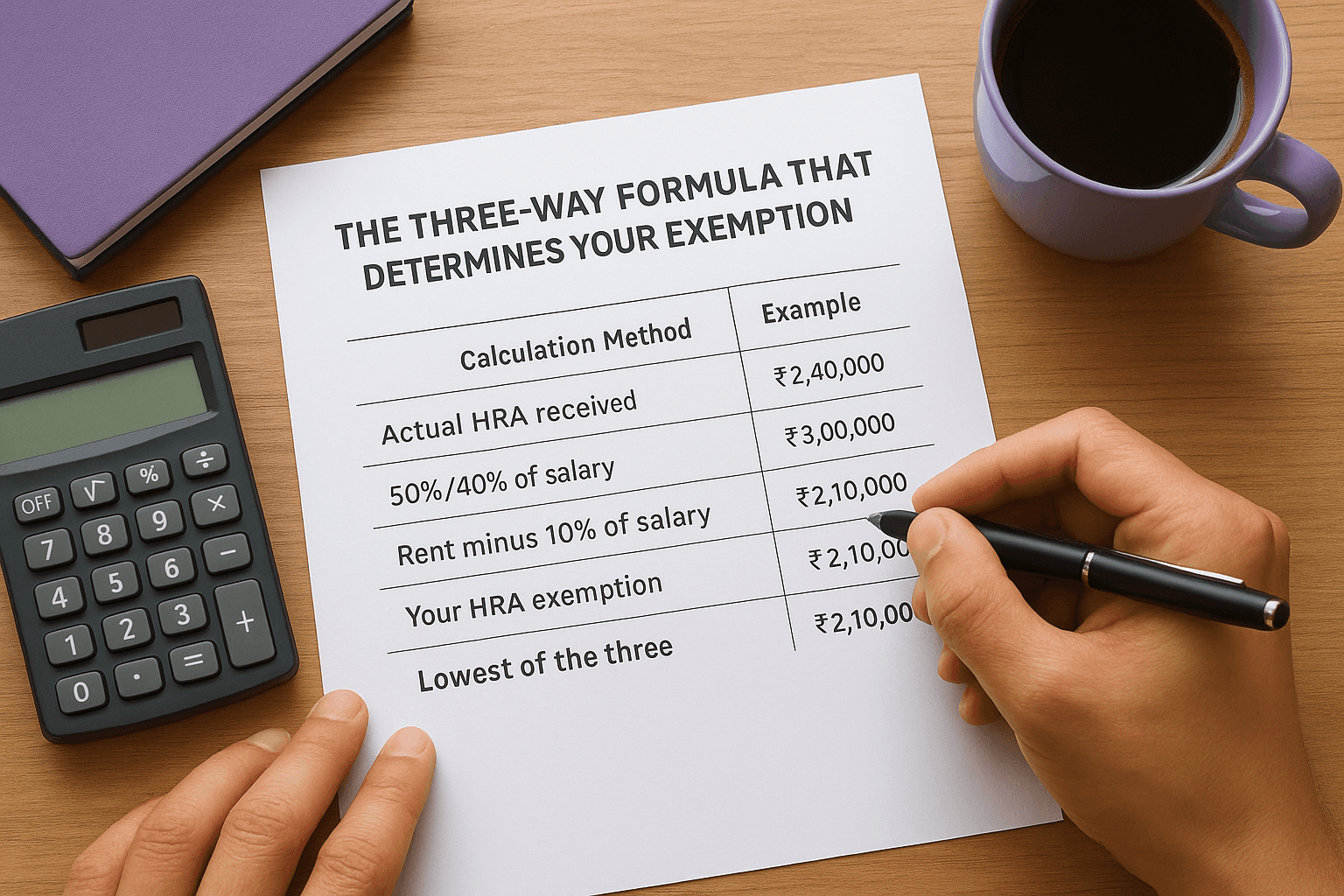

The three-way formula that determines your exemption

Rule 2A requires you to calculate three separate amounts and then pick the smallest one. The first amount is the actual HRA you received from your employer throughout the year. Check your Form 16 or salary slips to find this total. The second amount depends on your city classification: 50% of your salary if you live in a metro city, or 40% of your salary if you live in a non-metro city. The third amount is your actual annual rent paid minus 10% of your salary.

"Salary" for HRA calculation includes your basic salary plus dearness allowance (DA), but excludes all other allowances and perquisites. Don't use your gross salary or CTC for this calculation. If your employer pays you a fixed DA, add it to basic salary. If DA varies with inflation and isn't fixed, include only the fixed portion.

The three-way formula ensures that neither your rent payments nor your HRA component alone determines your exemption, making the calculation fairer but more complex.

Here's how the comparison works in practice:

Component | Calculation Method | Example (Metro) |

|---|---|---|

Actual HRA received | Sum from salary slips | ₹2,40,000 |

50%/40% of salary | 50% × (Basic + DA) | ₹3,00,000 |

Rent minus 10% of salary | Annual rent - (10% × Salary) | ₹2,10,000 |

Your HRA exemption | Lowest of the three | ₹2,10,000 |

Step-by-step calculation with real numbers

Assume your basic salary is ₹50,000 per month (₹6,00,000 annually), you receive ₹20,000 monthly HRA (₹2,40,000 annually), and you pay ₹15,000 monthly rent (₹1,80,000 annually) in Mumbai. Calculate the first amount: your actual HRA received is ₹2,40,000. For the second amount in a metro city: 50% of ₹6,00,000 equals ₹3,00,000. The third calculation requires you to subtract 10% of salary from annual rent: ₹1,80,000 minus (10% of ₹6,00,000) equals ₹1,80,000 minus ₹60,000, giving you ₹1,20,000.

Compare all three amounts: ₹2,40,000, ₹3,00,000, and ₹1,20,000. Your HRA exemption is ₹1,20,000, the lowest amount. You'll add the remaining ₹1,20,000 (₹2,40,000 minus ₹1,20,000) to your taxable income when you learn how to claim HRA exemption through your employer.

Metro vs non-metro classification matters

The Income Tax Act defines eight metro cities for HRA purposes: Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Hyderabad, Ahmedabad, and Pune. If you live in any of these cities, you use the 50% calculation. Every other city, town, or village in India qualifies as non-metro, where you apply the 40% rate instead.

Your classification depends on where you actually reside and pay rent, not where your office is located or where your employer is registered. If you work remotely from Jaipur while your office is in Delhi, you use the 40% non-metro rate because Jaipur is your residence.

Gather rent proof, landlord PAN, and forms

Documentation forms the backbone of your HRA exemption claim, whether you submit it to your employer or file it during ITR. You cannot claim this benefit without proper paperwork that proves you actually paid rent to someone else for your accommodation. The Income Tax Department requires specific documents to verify your claim, and missing even one piece can lead to rejection or scrutiny during assessment. Start collecting these documents at the beginning of the financial year to avoid last-minute scrambling when your employer asks for declarations.

Rent receipts and what they must contain

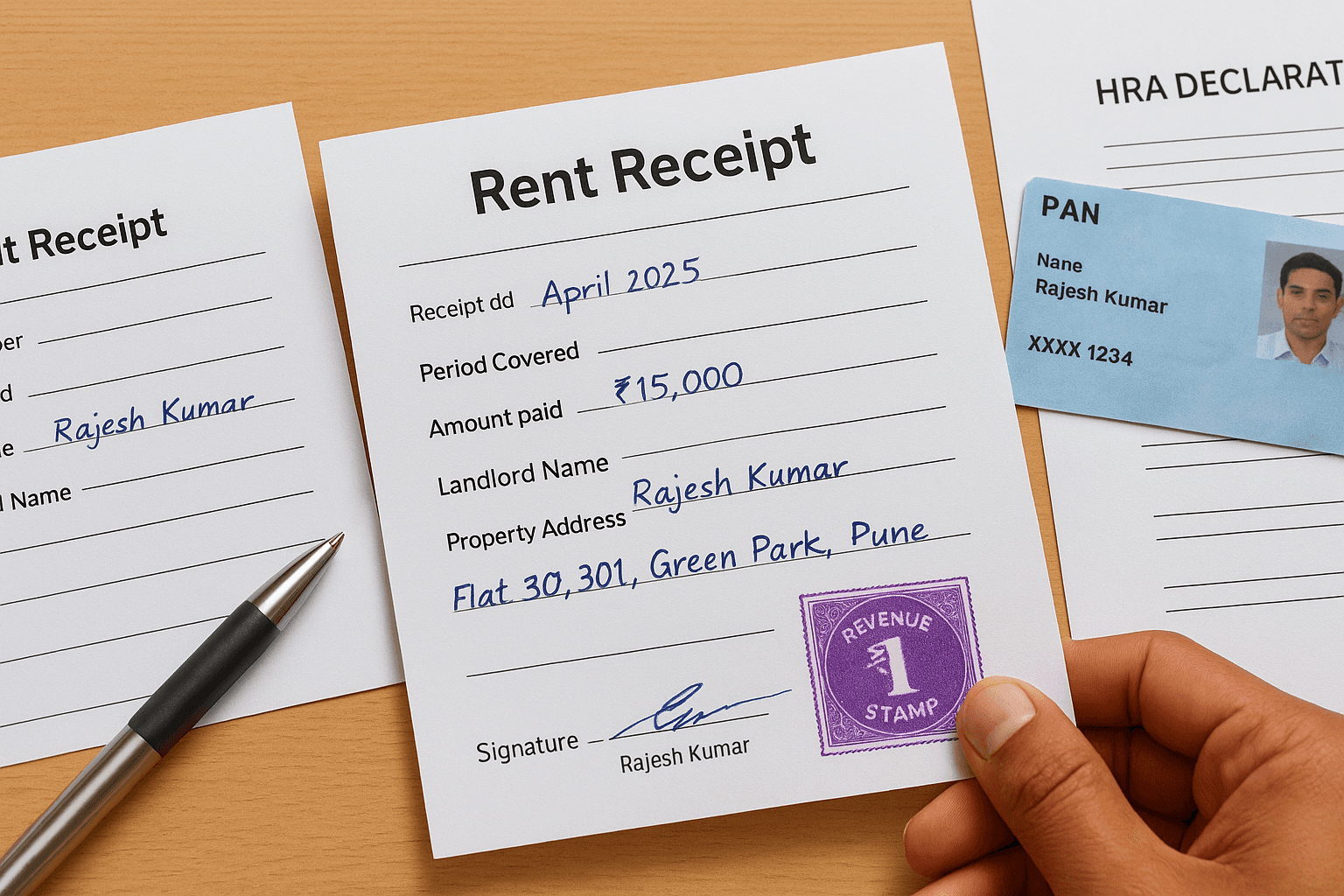

You need monthly rent receipts from your landlord for every month you paid rent during the financial year. Each receipt must include specific mandatory details: the rental period covered, the amount paid, your landlord's full name and complete address, a revenue stamp if the monthly rent exceeds ₹5,000, and your landlord's signature across the stamp. Generic or incomplete receipts will not satisfy tax authorities.

Your receipts must show consecutive numbering and maintain a clear payment trail. If you pay through bank transfer or check, keep copies of all bank statements showing these transactions. Digital payment screenshots from UPI apps work as supporting evidence but don't replace physical receipts. Download a standard rent receipt format that includes all required fields:

Required Field | Example |

|---|---|

Receipt number | 001/2025-26 |

Period covered | April 2025 |

Amount paid | ₹15,000 |

Landlord name | Rajesh Kumar |

Property address | Flat 301, Green Park, Pune |

Revenue stamp | ₹1 stamp if rent > ₹5,000 |

Signature | Across the stamp |

Missing revenue stamps on rent receipts exceeding ₹5,000 monthly can invalidate your entire HRA claim during tax scrutiny.

When you need your landlord's PAN card

You must submit your landlord's PAN card copy if your total annual rent exceeds ₹1,00,000, which equals roughly ₹8,334 monthly. This threshold applies to the entire financial year, not individual months. Calculate your annual rent carefully because if you pay ₹8,500 monthly, your total reaches ₹1,02,000, triggering the PAN requirement.

If your landlord doesn't have a PAN card, you need a declaration from them stating they don't possess one, along with their name, address, and any other identification. Foreign landlords require different documentation that includes their Tax Identification Number from their home country.

Forms your employer needs from you

Most employers require you to fill an HRA declaration form before they process your exemption and adjust TDS. This form typically asks for your rental address, landlord details, monthly rent amount, and the period for which you paid rent. Submit this declaration along with all rent receipts and the landlord's PAN copy (if applicable) to your HR or accounts department.

Your employer might also ask for a tenancy agreement or rent agreement as additional proof. While not mandatory under tax law, many companies want this document to verify the authenticity of your rental arrangement. Keep signed copies of your rental agreement accessible throughout the year when you figure out how to claim HRA exemption through your payroll.

Claim HRA through your employer and Form 16

Your employer plays the primary role in processing your HRA exemption and adjusting your monthly Tax Deducted at Source (TDS). This process happens during the financial year itself, reducing your tax burden month by month instead of waiting until ITR filing. You submit your documentation to your employer, they calculate the exemption amount using Rule 2A, and then they deduct lower TDS from your salary after accounting for this benefit. This advance adjustment means you take home more money every month rather than waiting for a refund after filing your return.

Submit declarations at the right time

Most companies require you to submit your HRA declaration form along with all supporting documents during their annual investment declaration cycle, typically between January and March for the ongoing financial year. Your employer sets specific deadlines for these submissions, often around mid-February or early March. Missing this deadline means your employer will deduct TDS at full rates without considering your HRA exemption, forcing you to claim the entire benefit later when you learn how to claim HRA exemption through your income tax return.

Submit your complete documentation package to your HR or payroll department: the filled declaration form, all monthly rent receipts for the year, your landlord's PAN card copy (if annual rent exceeds ₹1,00,000), and your rental agreement. Your employer's tax team reviews these documents, verifies the calculations, and processes the exemption. They then adjust your TDS from the next payroll cycle onwards, though some employers make retroactive adjustments and refund excess TDS deducted in earlier months of the same financial year.

Your employer cannot process HRA exemption retroactively for previous financial years, making timely declaration submissions critical for maximizing monthly take-home pay.

Verify your Form 16 after year-end

Your employer issues Form 16 after June 15th following the financial year's end. This certificate shows your total salary income, all deductions claimed (including HRA exemption), and the final TDS deducted. Download Form 16 from your employer's portal and check Part B, which breaks down salary components. Look for the "Less: Allowances to the extent exempt under section 10" section where your HRA exemption appears as a separate line item.

Cross-verify three critical numbers: the HRA amount received (should match your total annual HRA from salary slips), the HRA exemption amount claimed (should match your Rule 2A calculation), and the taxable HRA (the difference between received and exempt amounts). Any mismatch between your calculation and Form 16 requires immediate clarification with your employer before filing your ITR, as Form 16 forms the basis of your income tax return.

Track monthly TDS adjustments

Check your monthly salary slip after your employer processes your HRA declaration. You'll notice a reduction in TDS deducted compared to previous months before the declaration. Your payslip should show the HRA component separately and indicate the exempt portion either in the deductions section or through lower taxable income calculation.

Maintain a simple tracking sheet throughout the year:

Month | Gross Salary | HRA Received | TDS Deducted | Notes |

|---|---|---|---|---|

April | ₹80,000 | ₹20,000 | ₹8,500 | Before declaration |

May | ₹80,000 | ₹20,000 | ₹6,200 | After HRA adjustment |

This tracking helps you catch processing errors early and ensures your employer correctly applies the exemption every month.

Claim HRA in your ITR and handle tricky cases

You need to claim HRA exemption in your Income Tax Return when your employer hasn't adjusted it in your TDS, or when you missed submitting declarations during the year. This situation arises frequently when you start renting mid-year, switch employers, or your company's payroll system doesn't process exemptions. Filing your ITR gives you a second opportunity to claim this benefit and reduce your tax liability, though it means waiting longer for your refund instead of getting monthly TDS relief.

Fill Schedule HRA in your ITR form

Navigate to Schedule HRA in your ITR-1 or ITR-2 form when you file online. This schedule appears under the "Salary" section after you enter your Form 16 details. You need to input specific information: your total HRA received, the name and address of your landlord, your landlord's PAN (if annual rent exceeds ₹1,00,000), and the total rent you actually paid during the year.

The portal automatically calculates your exempt amount using Rule 2A once you fill these fields. Enter your annual basic salary plus dearness allowance in the designated field, specify whether you lived in a metro or non-metro city, and input your rent payments. The system compares all three formula components and shows your final HRA exemption. Verify this calculated amount matches your manual calculation before submitting your return.

Filing HRA exemption through ITR requires the same documentation rigor as employer declarations, so keep all rent receipts and landlord details ready when you learn how to claim HRA exemption this way.

Renting from parents or relatives

You can legally claim HRA when renting from your parents, siblings, or other relatives, but you must follow strict documentation rules. Your parents cannot claim your property as self-occupied for their income tax purposes if they're charging you rent. They must declare your rent as income from house property in their ITR and pay tax on it after deducting standard deduction and applicable expenses.

Create a proper rental agreement with your parent or relative, just as you would with any landlord. Pay rent through bank transfers or checks to maintain a clear audit trail, never in cash. Collect monthly rent receipts with revenue stamps, and ensure your parent provides their PAN card copy. Tax authorities scrutinize these arrangements closely, so genuine transactions with proper documentation are essential.

Handle mid-year changes and multiple cities

Calculate your HRA exemption separately for each period if you moved cities during the year. Apply the 50% rate for months you lived in metro cities and the 40% rate for non-metro months. If you paid ₹20,000 monthly rent in Bangalore for eight months, then ₹12,000 in Jaipur for four months, you calculate two separate exemptions and add them.

Split your annual salary proportionally across these periods if you changed jobs mid-year. Your new employer's Form 16 only covers the period you worked there, so you need to combine both Form 16s when filing your ITR. Calculate HRA exemption separately for each employment period, using the respective employer's HRA and salary components.

Final checklist before you file

You now understand how to claim HRA exemption from choosing the right tax regime to submitting documents and filing your ITR. Before you finalize your claim, verify five critical items: confirm your employer included the correct HRA exemption amount in Form 16, ensure you have all monthly rent receipts with proper revenue stamps and signatures, check that your landlord's PAN copy is ready if your annual rent crossed ₹1,00,000, validate your Rule 2A calculation matches the exemption shown in your payslips, and keep copies of your rental agreement accessible for potential scrutiny.

Double-check your ITR form's Schedule HRA section shows accurate rent amounts and landlord details before submitting. Review your refund calculation to confirm the exemption reduced your tax liability as expected. Keep all documentation safely stored for at least six years in case the Income Tax Department requests verification during assessment.

Smart tax planning goes beyond just HRA. Get personalized wealth optimization advice from Invsify's AI-powered platform to maximize every deduction and build long-term financial security.