How To Create A Financial Plan In India: Step-by-Step

Shlok Sobti

How To Create A Financial Plan In India: Step-by-Step

Most Indians don't have a financial plan. They have a collection of random investments, an LIC policy from a relative, some mutual funds from a bank relationship manager, maybe a few stocks picked from WhatsApp tips. This isn't a plan; it's chaos with extra steps.

Learning how to create a financial plan changes everything. It gives you clarity on where your money goes, what it's doing, and whether you'll actually reach your goals, be it buying a home, funding your child's education, or retiring without depending on anyone.

The good news? You don't need a finance degree or lakhs in savings to start. A solid financial plan is built on simple principles, applied consistently. At Invsify, we help Indians build and execute these plans using AI-powered insights combined with SEBI-registered advisory expertise, no hidden commissions, no conflicts of interest.

This guide walks you through each step of building your own financial plan, from setting clear goals to choosing the right investments. By the end, you'll have a framework you can implement immediately, whether you're just starting out or looking to optimize what you already have.

What a financial plan includes in India

A complete financial plan in India covers seven core areas. Income and expense tracking forms the foundation, showing exactly where your money comes from and where it goes each month. Asset and liability documentation follows, listing everything you own (savings accounts, fixed deposits, mutual funds, property, gold) against everything you owe (home loan, personal loan, credit card debt).

Essential components every Indian needs

Your plan must include a risk management section covering life insurance, health insurance, and critical illness coverage. Most Indians underinsure themselves or buy policies they don't need, both equally dangerous mistakes. Tax planning strategies specific to Section 80C, 80D, and other deductions help you legally minimize your tax outgo while building wealth.

Investment allocation shows how your money gets distributed across equity, debt, gold, and real estate based on your goals and risk tolerance. This isn't about picking stocks; it's about deciding what percentage goes where and why. Emergency fund planning ensures you have three to six months of expenses liquid, so one medical bill or job loss doesn't derail everything.

A financial plan without clear timelines and review mechanisms is just a wish list with calculations attached.

Indian regulations and accounts to factor in

Understanding how to create a financial plan in India means accounting for our specific regulatory environment. Your PAN card, Aadhaar, and bank KYC form the documentation backbone for every investment and insurance product. EPF and NPS contributions need explicit mention because they're often the largest retirement savings most salaried Indians have, yet people rarely track them properly.

Succession planning matters more here because joint family structures and unclear property titles create disputes that drain wealth across generations. You need nominees on every account, a will that's legally valid, and clarity on who gets what. This applies even if you're in your twenties with minimal assets.

Documents and data you'll compile

Gather salary slips, Form 16, and bank statements from the past year to establish your income baseline. Pull investment statements from every mutual fund, stock broker, insurance company, and bank where you hold assets. Collect loan statements showing outstanding principal, interest rate, and tenure for each debt.

Property documents and valuations go into the asset list at current market rates, not what you paid ten years ago. Create a simple spreadsheet listing each account with its current value, expected returns, maturity date if applicable, and purpose. This becomes your single source of truth, updated quarterly at minimum.

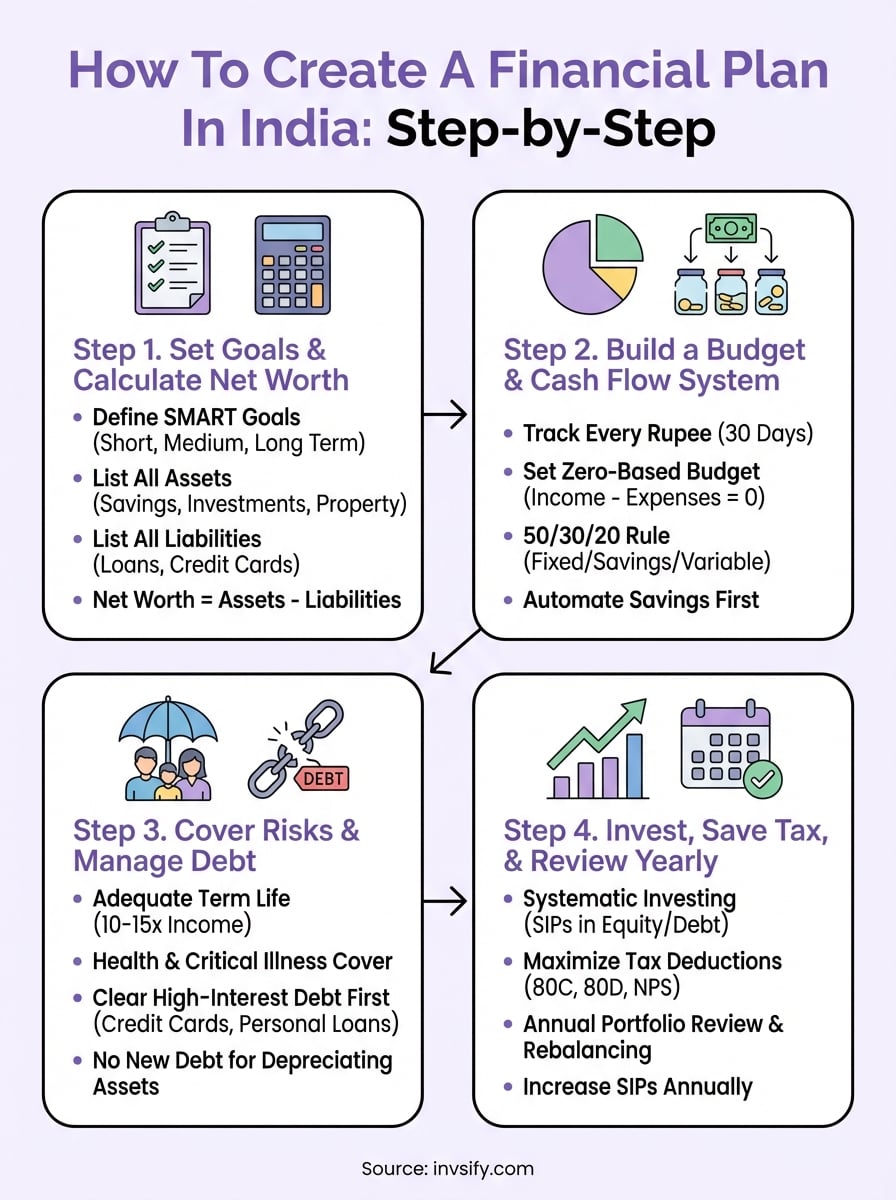

Step 1. Set goals and calculate net worth

Start by writing down three to five specific financial goals with exact numbers and deadlines. Don't write "buy a house someday" or "retire comfortably." Write "₹40 lakh down payment for 3BHK in Pune by December 2028" or "₹2 crore retirement corpus by age 58." Vague goals produce vague results, and the first step in learning how to create a financial plan is getting brutally specific about what you want your money to accomplish.

Define your short and long term goals

Your short term goals span zero to three years and include emergency fund creation, vacation planning, vehicle purchase, or clearing high interest debt. Medium term goals run three to seven years, typically covering children's higher education, property down payment, or starting a business. Long term goals stretch beyond seven years and usually center on retirement, children's marriage, or achieving financial independence.

Assign a priority level to each goal because you can't fund everything simultaneously. Mark goals as essential (retirement, children's education, health insurance), important (home purchase, vehicle upgrade), or nice to have (international vacation, luxury purchases). Write the current cost, inflate it at 6% annually to estimate future cost, then reverse calculate how much you need to save monthly assuming reasonable returns.

Goals without numbers and dates are just expensive dreams that drain your salary every month without building anything real.

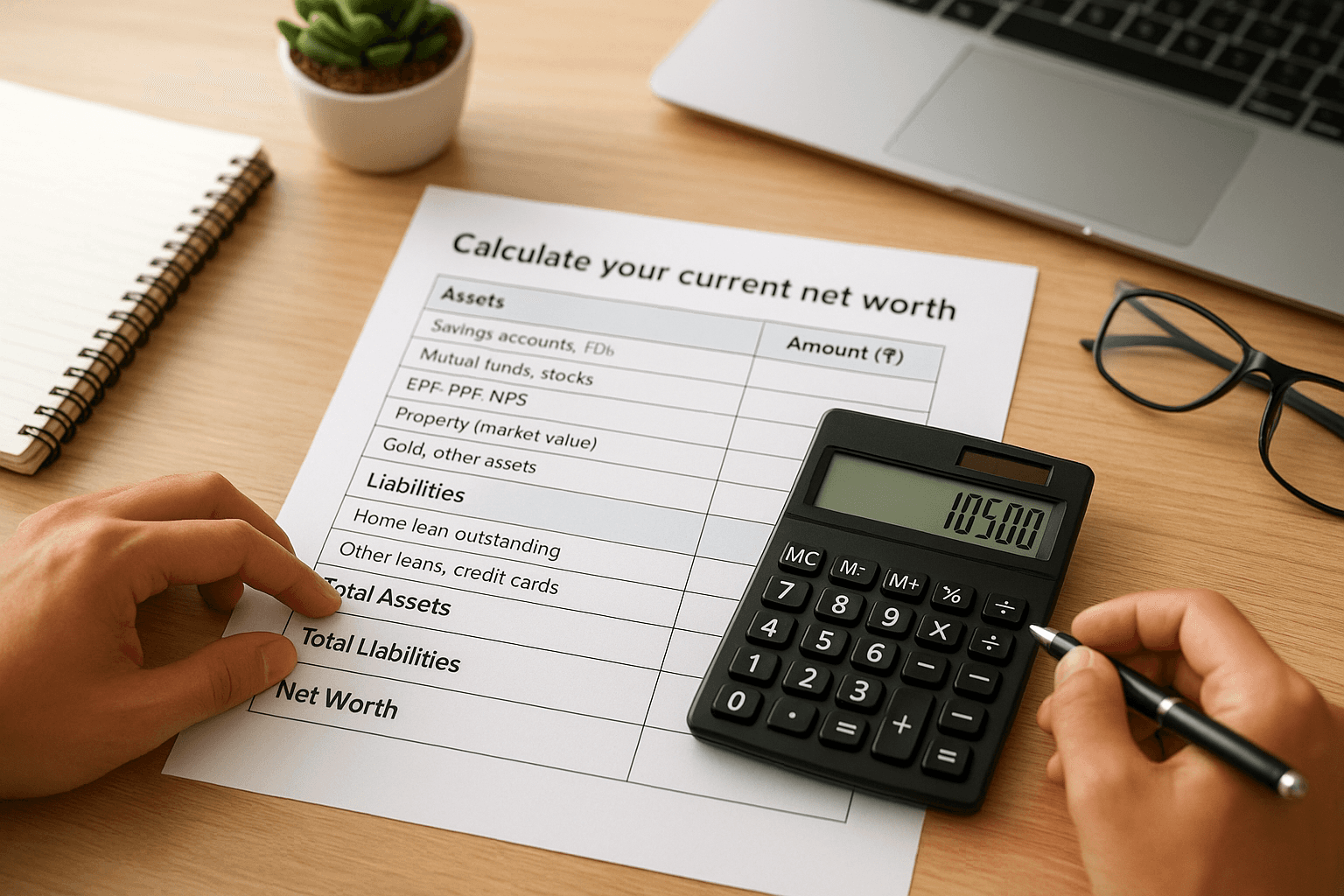

Calculate your current net worth

List every asset with its current market value, not what you paid for it. Include bank balances, fixed deposits, mutual fund current values, stock portfolio, EPF balance, PPF, NPS, property valuations, gold holdings, and insurance cash values. Add these to get your total assets. Then list every liability with outstanding principal, home loan balance, car loan, personal loans, credit card debt, and money borrowed from family or friends.

Your net worth equals total assets minus total liabilities. Use this simple template:

Category | Details | Amount (₹) |

|---|---|---|

Assets | Savings accounts, FDs | |

Mutual funds, stocks | ||

EPF, PPF, NPS | ||

Property (market value) | ||

Gold, other assets | ||

Total Assets | ||

Liabilities | Home loan outstanding | |

Other loans, credit cards | ||

Total Liabilities | ||

Net Worth | Assets minus Liabilities |

Track this number quarterly. Your financial plan succeeds when net worth increases consistently after accounting for your savings and investment returns.

Step 2. Build a budget and cash flow system

Building a budget that actually works requires tracking where every rupee goes for at least thirty days. Download your bank statements, credit card statements, and payment app transaction histories from the past month. Categorize each expense into groups like rent, groceries, utilities, transport, dining out, entertainment, EMIs, insurance premiums, and miscellaneous. This exercise reveals your actual spending patterns, not what you think you spend.

Track every rupee for one month

Use a simple spreadsheet or banking app that auto-categorizes transactions. Manual tracking works better initially because you become conscious of each purchase when you write it down. Mark expenses as fixed (rent, EMIs, insurance), variable but necessary (groceries, utilities, fuel), or discretionary (subscriptions, dining out, shopping). Calculate what percentage of your income goes to each category.

Understanding how to create a financial plan becomes impossible when you don't know where your money disappears every month.

Set up a zero-based budget

Allocate every rupee of your monthly income to a specific category before the month begins. Your income minus all allocated expenses should equal zero. This doesn't mean spending everything; it means giving every rupee a job, whether that job is paying bills, investing, or sitting in your emergency fund. Review this budget weekly for the first month, adjusting categories as reality hits your assumptions.

Here's a basic allocation framework for salaried Indians:

Category | Percentage | Example (₹75,000 salary) |

|---|---|---|

Fixed expenses | 40-50% | ₹30,000-37,500 |

Savings & investments | 20-30% | ₹15,000-22,500 |

Variable expenses | 15-25% | ₹11,250-18,750 |

Discretionary | 5-10% | ₹3,750-7,500 |

Automate your savings first

Set up automatic transfers on salary day moving money to investment accounts, recurring deposits, or SIPs before you see it in your main account. Treat savings like a non-negotiable EMI payment. Keep your spending account lean with just enough to cover budgeted expenses plus a small buffer, forcing you to live on what remains after saving, not save what remains after living.

Step 3. Cover risks and manage debt

Risk protection and debt elimination form the defensive layer of your financial plan. Most Indians skip insurance or buy inadequate coverage because agents push expensive products with poor terms. Meanwhile, high-interest debt compounds against you faster than any investment can grow your wealth. Fixing both problems immediately protects everything you've built and frees up cash flow for investing.

Get adequate insurance coverage

Buy term life insurance worth 10 to 15 times your annual income if dependents rely on your salary. A 35-year-old non-smoker pays roughly ₹12,000 to ₹15,000 annually for ₹1 crore coverage, far cheaper than mixing insurance with investment through ULIPs or endowment policies. Purchase family health insurance with ₹10 lakh minimum coverage, increasing to ₹20 lakh if you're in metro cities where hospitalization costs drain savings overnight.

Add critical illness cover worth ₹50 lakh as a separate rider or standalone policy because cancer or heart disease treatment creates expenses health insurance won't fully cover. Skip policies that "return your premium" after 20 years, they cost double for negligible returns. Understanding how to create a financial plan means separating protection from investment completely, buying pure term cover and investing the difference yourself.

Insurance isn't an investment; it's the firewall that prevents one medical emergency or death from destroying decades of financial discipline.

Clear high-interest debt strategically

List every debt with its interest rate, outstanding amount, and monthly EMI. Prioritize credit card debt (18% to 42% interest) and personal loans (12% to 20% interest) over home loans (8% to 9% interest). Allocate extra money beyond minimum payments to the highest interest debt first, a strategy that saves lakhs in interest charges over time.

Debt Type | Interest Rate | Action Priority |

|---|---|---|

Credit cards | 18-42% | Pay off immediately |

Personal loans | 12-20% | Accelerate repayment |

Car loans | 9-12% | Regular EMI, prepay if possible |

Home loans | 8-9% | Maintain, invest surplus elsewhere |

Avoid taking new debt for depreciating assets like vehicles or vacations. Negotiate interest rate reductions on existing loans by showing clean repayment history or threatening to transfer the loan to competitors offering better rates.

Step 4. Invest, save tax, and review yearly

Your financial plan converts from theory to wealth when you invest consistently and optimize taxes without waiting for perfect market conditions or complete knowledge. The final step ties everything together through systematic investing, maximizing deductions legally available to Indians, and conducting annual reviews that keep your plan aligned with changing goals and circumstances.

Start systematic investing across asset classes

Begin monthly SIPs in diversified equity mutual funds for goals beyond five years, allocating 60% to 80% of your investment bucket to equity when you're under 40. Place debt mutual funds or fixed deposits for goals three to five years away, providing stability while beating savings account returns. Keep emergency funds in liquid funds or savings accounts where you can access money within 24 hours without penalties.

Maintain this basic allocation framework adjusted for your age:

Age Group | Equity | Debt | Gold/Others |

|---|---|---|---|

20-35 | 70-80% | 15-25% | 5% |

36-45 | 60-70% | 25-35% | 5% |

46-55 | 40-50% | 45-55% | 5% |

56+ | 20-30% | 65-75% | 5% |

Increase SIP amounts annually by at least 10% as your salary grows, automating this increment to match appraisals or bonuses.

Learning how to create a financial plan becomes meaningless if you never execute the investment and tax strategies that actually build wealth over decades.

Maximize tax deductions under current laws

Exhaust your Section 80C limit of ₹1.5 lakh through EPF contributions, ELSS mutual funds, PPF deposits, or life insurance premiums, choosing options that also serve your investment goals rather than just saving tax. Claim ₹25,000 under Section 80D for health insurance premiums, increasing to ₹50,000 if covering parents above 60. Use NPS contributions under Section 80CCD(1B) for an additional ₹50,000 deduction beyond 80C, particularly effective for those in 30% tax brackets.

Conduct annual review every December

Block three hours in late December to review every aspect of your financial plan. Compare actual savings against budgeted amounts, check if investments delivered expected returns, verify insurance coverage remains adequate as income grows, and adjust SIP amounts for the coming year. Rebalance your portfolio when equity allocation drifts 5% above or below target, selling winners and buying underperformers to maintain discipline.

Next steps to keep your plan on track

You've learned how to create a financial plan that covers every aspect of Indian personal finance. The difference between successful and failed plans isn't knowledge, it's consistent execution and periodic course correction. Set calendar reminders for quarterly net worth calculations, annual insurance reviews, and monthly budget checks.

Update your goals every six months as life circumstances change, salary increases, or priorities shift. Increase SIP amounts by at least 10% annually, rebalance portfolios when allocations drift 5% from targets, and review tax saving opportunities each December before the financial year ends.

Consider working with a SEBI-registered advisor who uses AI-powered insights to optimize your plan continuously. Invsify provides conflict-free financial advice with transparent fee structures, eliminating hidden commissions that traditional distributors charge. Get your personalized wealth wellness score and start building a plan that actually delivers on your goals.