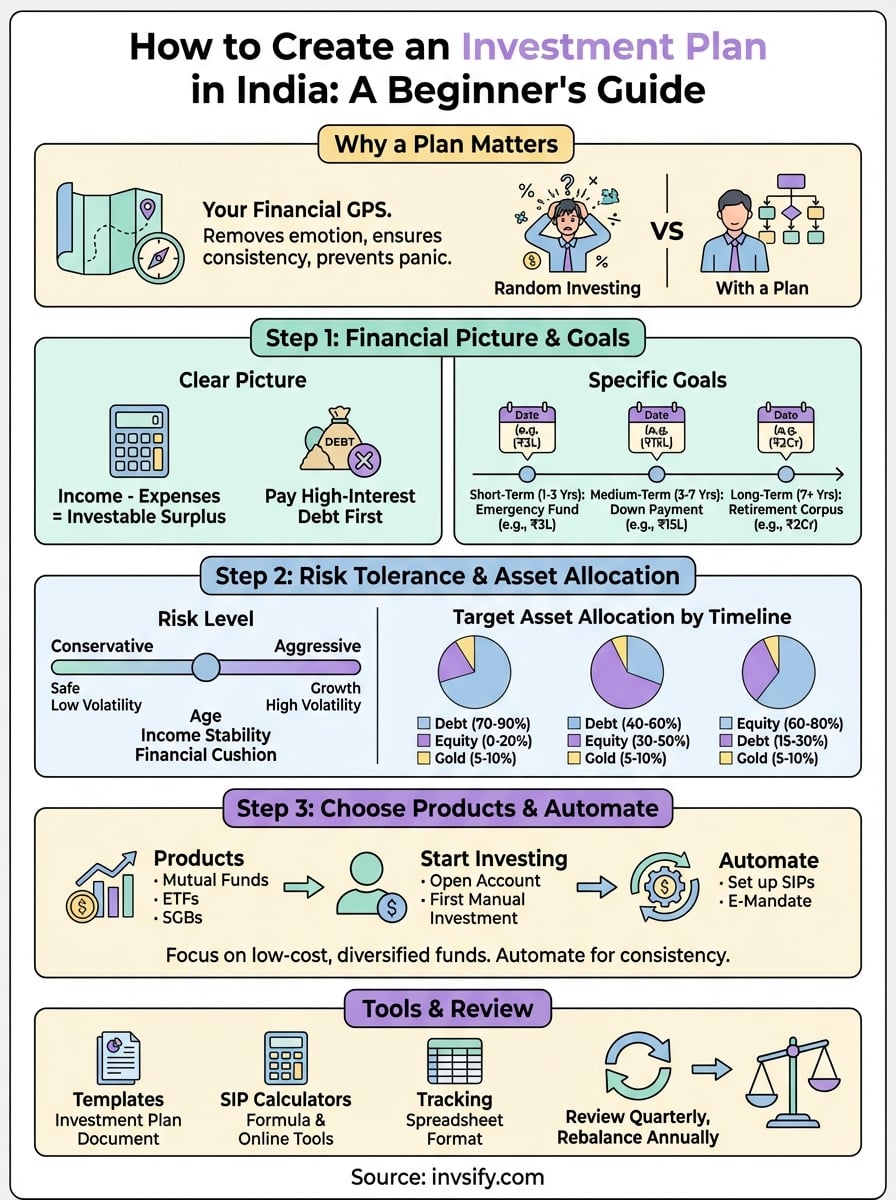

How to Create an Investment Plan in India: Beginner's Guide

Shlok Sobti

How to Create an Investment Plan in India: Beginner's Guide

You know you should invest. Your salary sits in a savings account earning 3%, while inflation eats away at your purchasing power. You see colleagues talking about mutual funds and stocks, but you're not sure where to start. Too many options. Too much jargon. And honestly, you're worried about making expensive mistakes with your hard earned money.

The good news is you don't need a finance degree or a six figure salary to start investing properly. You need an investment plan. Think of it as your financial GPS. It tells you exactly how much to invest, where to put your money, and how to adjust as your life changes. Once you have this plan in place, investing becomes straightforward instead of stressful.

This guide breaks down how to create your own investment plan from scratch. We'll cover how to set clear financial goals, figure out your risk tolerance, choose the right mix of investments, pick actual products, and track everything over time. By the end, you'll have a practical framework you can use to start building wealth on your own terms.

What an investment plan is and why it matters

An investment plan is your written roadmap for building wealth. It documents your financial goals, how much you'll invest each month, which types of assets you'll buy, and when you'll review your portfolio. This isn't a vague wish list. It's a concrete document that answers specific questions: Where is your money going? Why are you investing in particular products? What returns do you need to hit your goals?

Why a plan beats random investing

Without a plan, you make emotional decisions. You buy stocks when they're expensive because everyone's talking about them. You panic-sell during market drops. You chase last year's top performers. A proper plan removes emotion from the equation. It keeps you investing consistently, regardless of market noise.

The data backs this up. Studies show that investors who follow a systematic plan outperform those who make ad-hoc decisions. Your plan also forces you to think about risk before you lose money, not after. You decide upfront how much volatility you can stomach, then build a portfolio that matches. This prevents the classic mistake of investing aggressively in bull markets, panicking during a crash, and locking in losses by selling at the worst possible time.

A plan turns investing from a stressful guessing game into a repeatable system you can follow in any market condition.

When you learn how to create investment plan properly, you build in accountability. You set specific targets (like ₹50 lakhs in 10 years for your child's education) and track whether you're on pace. If you fall short, you adjust your monthly contributions or timeline early, while you still have options. Without this framework, you discover problems too late to fix them.

Step 1. Get your financial picture and goals clear

Before you invest a single rupee, you need to understand where you stand today and where you want to go. This sounds basic, but most people skip this step and jump straight into buying products. That's like booking flight tickets before deciding your destination. You need two things clear: your current financial situation and your specific financial goals.

Calculate your monthly investable surplus

Start by tracking your monthly income and expenses for at least two months. Write down every source of income (salary, freelance work, rental income). Then list all your monthly expenses, including rent, groceries, utilities, EMIs, insurance premiums, and discretionary spending. The difference between income and expenses is your surplus. This number tells you how much you can invest each month without stretching yourself.

Next, check your existing assets and liabilities. List what you own (savings account balance, fixed deposits, PPF, existing mutual funds, gold, real estate) and what you owe (home loans, car loans, personal loans, credit card debt). If you're carrying high-interest debt like credit card balances at 36% per year, paying that off comes before investing. You can't earn investment returns that beat 36% consistently.

Write down specific goals with rupee amounts and dates

Vague goals like "save for retirement" or "buy a house" don't help when you learn how to create investment plan that actually works. You need specific targets with numbers and deadlines. Break your goals into three categories:

Short-term (1 to 3 years): Emergency fund of ₹3 lakhs, vacation budget of ₹1.5 lakhs, new laptop for ₹80,000.

Medium-term (3 to 7 years): Down payment of ₹15 lakhs for a house, car purchase of ₹8 lakhs, wedding fund of ₹10 lakhs.

Long-term (7+ years): Retirement corpus of ₹2 crores in 25 years, child's education fund of ₹50 lakhs in 15 years.

For each goal, write the exact amount you need and the exact date you need it. Then adjust for inflation. If your child's engineering degree costs ₹20 lakhs today and you need it in 15 years, assume 7% education inflation. The real target becomes roughly ₹55 lakhs. This forces you to invest enough from the start instead of scrambling later.

Clear goals with specific numbers transform investing from a vague intention into a measurable process you can actually track and achieve.

Once you have your surplus amount and goal list documented, you know how much you can invest monthly and what returns you need to hit each target. This foundation makes every subsequent decision easier.

Step 2. Decide your risk level and asset mix

Now that you know your goals and surplus, you need to figure out how much risk you can handle and how to split your money across different assets. This step determines which products you'll buy and what returns you can realistically expect. Get this wrong and you'll either take too much risk and panic during market crashes, or play it too safe and fall short of your goals.

Risk tolerance isn't about what sounds good in theory. It's about how you'll actually react when your portfolio drops 20% in three months. If that drop would make you lose sleep and sell everything, you can't handle aggressive investments. Your risk level depends on three factors: your age (younger investors can take more risk because they have time to recover), your income stability (steady salary job versus variable freelance income), and your financial cushion (emergency fund and other assets beyond investments).

Assess your risk tolerance honestly

Answer these questions to understand your true risk capacity. Can you afford to see your portfolio value drop 30% without needing to withdraw money? If you're investing for a goal 15 years away, the answer should be yes. If you need the money in three years, any big drop could derail your plans. Would a 25% portfolio decline make you sell in panic? Be honest. If market volatility keeps you awake at night, you need a more conservative approach even if calculators say you can handle higher risk.

Your time horizon matters most. Money you need within three years belongs in safe options like debt funds or fixed deposits, regardless of your age. Goals beyond seven years can handle equity exposure because short-term volatility smooths out over time. For retirement funds 20 years away, you can invest aggressively in your 30s and gradually reduce equity as you approach retirement.

Match your investment risk to your emotional capacity and goal timeline, not to what sounds impressive or what others are doing.

Create your target asset allocation

Asset allocation means deciding what percentage of your money goes into different asset classes: equity (stocks and equity mutual funds), debt (fixed deposits, debt funds, bonds), gold, and cash. When you learn how to create investment plan that balances growth and safety, this split becomes your portfolio blueprint.

Here's a simple framework based on your primary goal timeline:

Goal Timeline | Equity % | Debt % | Gold % |

|---|---|---|---|

0-3 years | 0-20% | 70-90% | 5-10% |

3-7 years | 30-50% | 40-60% | 5-10% |

7+ years | 60-80% | 15-30% | 5-10% |

These ranges give you flexibility. If you're risk-averse, pick the lower end of equity allocation. If you're comfortable with volatility and have strong income stability, go higher. Equity drives long-term growth but swings violently short-term. Debt provides stability but barely beats inflation. Gold acts as insurance against extreme events and typically moves differently from stocks and bonds.

Once you set your target allocation, write it down. This becomes your rebalancing guide. If equity markets surge and your 70% equity allocation becomes 85%, you sell some equity and buy debt to return to 70%. This forces you to sell high and buy low systematically instead of chasing performance.

Step 3. Choose products, start investing, and automate

You've mapped your goals and decided your asset split. Now comes the practical part: choosing actual investment products, opening the necessary accounts, and setting up automation so you invest consistently without thinking about it every month. This is where your plan moves from paper to reality. The goal here is to pick simple, low-cost products that match your allocation, start with whatever amount you have ready, and build systems that keep your investment plan running on autopilot.

Pick specific products that match your allocation

Start with mutual funds for most of your portfolio. They're regulated, liquid, and require no specialized knowledge. For your equity portion, pick one or two diversified equity funds. Look for large-cap or flexi-cap funds with expense ratios below 1% and consistent 10-year track records. Avoid sector funds or thematic funds until you understand how they work. For debt allocation, choose liquid funds for money you need within a year and short-duration debt funds for the 1 to 3 year bucket.

Gold exposure comes easiest through gold ETFs or sovereign gold bonds (SGBs). SGBs pay 2.5% annual interest and offer capital gains tax exemption if you hold until maturity. Gold ETFs trade like stocks and give you instant liquidity. Pick one method and stick with it. For your emergency fund (typically 6 months of expenses), keep it in a combination of savings account and liquid mutual funds. You need this money accessible within 24 hours, so avoid fixed deposits with penalties on early withdrawal.

Here's a sample product selection for ₹10,000 monthly investment with 70% equity, 20% debt, 10% gold allocation:

Asset Class | Product Type | Monthly Amount |

|---|---|---|

Equity | Flexi-cap fund (₹5,000) + Index fund (₹2,000) | ₹7,000 |

Debt | Short-duration debt fund | ₹2,000 |

Gold | Gold ETF or SGB | ₹1,000 |

Don't obsess over finding the "perfect" fund. Good is better than perfect when you're learning how to create investment plan that actually gets implemented. You can always adjust later. Focus on starting with low-cost, diversified options from established fund houses like HDFC, ICICI Prudential, SBI, or Axis.

Open accounts and make your first investments

You need a mutual fund investment account and a demat account (for ETFs). You can open both through online platforms that offer direct mutual funds (no commission charges). The KYC process takes 2 to 3 days. You'll need your PAN card, Aadhaar, bank account details, and a cancelled cheque. Complete your risk profiling during account opening. This creates an audit trail showing you understood the risks before investing.

Make your first investment manually to understand the process. Log in, search for your chosen fund, enter the amount, and complete the payment. Most platforms accept UPI, net banking, or NEFT. Your units get allotted within 1 to 3 business days depending on the fund type. Check your portfolio dashboard after a week to see your holdings. This initial hands-on experience removes the mystery from investing.

Set up automatic monthly transfers

Once you've made your first investment, set up SIPs (Systematic Investment Plans) for all your chosen funds. SIPs automatically deduct a fixed amount from your bank account on a specific date each month and invest it in your selected funds. Log into your investment platform, select each fund, choose the SIP option, enter your monthly amount, and pick a date (ideally 2 to 3 days after your salary credit).

Register an e-mandate with your bank during SIP setup. This one-time authorization allows the fund house to debit your account automatically every month. You'll receive an email confirmation for each SIP. Once active, these SIPs run indefinitely until you pause or cancel them. Review your SIPs quarterly to ensure they're executing properly and to increase amounts when your income grows.

Automation removes the monthly decision fatigue of whether to invest and eliminates the risk of skipping months when markets look scary or you feel busy.

Helpful tools, examples, and templates

You don't need expensive software or complicated spreadsheets to manage your investments. Simple templates and basic calculations give you everything required to track progress and stay on course. The tools below help you document your plan, calculate monthly contributions, and monitor your portfolio without getting lost in unnecessary complexity. Copy these formats, adjust them to your situation, and use them as your investment dashboard.

Sample investment plan template

This template documents everything you need when figuring out how to create investment plan that you'll actually follow. Copy this format into a document and fill in your specific details:

Calculate how much to invest monthly

Once you know your goal amount and timeline, use this formula to calculate your required monthly SIP. Assume 12% annual returns for equity-heavy portfolios and 7% for conservative ones. The formula accounts for compounding:

Monthly SIP = [Goal Amount × Interest Rate] ÷ [((1 + Interest Rate)^Months) - 1]

Example calculation: You need ₹50 lakhs in 15 years for your child's education. Assuming 12% annual returns (1% monthly rate):

Goal: ₹50,00,000

Months: 180

Monthly Interest Rate: 0.01

Required Monthly SIP: ₹50,00,000 × 0.01 ÷ [((1.01)^180) - 1] = ₹8,600 approximately

Your investment platform's SIP calculator does this math automatically. Verify your calculations using these calculators before committing to any investment amount.

Simple tracking spreadsheet format

Track your portfolio monthly using this table structure. Update values on the first of each month and compare against your target allocation:

Asset Class | Target % | Current Value | Current % | Action Needed |

|---|---|---|---|---|

Equity Funds | 70% | ₹2,45,000 | 73% | Rebalance if >75% |

Debt Funds | 20% | ₹65,000 | 19% | Within range |

Gold ETF | 10% | ₹28,000 | 8% | Add ₹7,000 |

Total | 100% | ₹3,38,000 | 100% | - |

Add rows for each specific fund you own. Review this monthly but rebalance only when any asset class moves more than 5% away from its target allocation. This prevents unnecessary transaction costs while keeping your plan on track.

Use these templates as starting points, not rigid rules. Adjust them as your financial situation evolves and you gain investing experience.

A quick wrap up

You now understand how to create investment plan that matches your goals and risk tolerance. Start with your financial snapshot and clear goals, then pick your asset allocation based on timelines. Choose simple, low-cost products and set up automatic monthly investments. Review quarterly and rebalance yearly.

The hardest part is taking the first step. You don't need perfect knowledge or large amounts to begin. Start with whatever monthly surplus you have today. If you want AI-powered guidance to build and track your personalized investment plan, sign up with Invsify for conflict-free advice.