How To Do Asset Allocation Based On Goals, Risk, And Age

Shlok Sobti

How To Do Asset Allocation Based On Goals, Risk, And Age

Most people start investing by picking individual stocks or mutual funds they've heard about from friends, YouTube, or Reddit threads. But here's the thing, what you invest in matters far less than how to do asset allocation across your entire portfolio. Getting this split right between equity, debt, gold, and cash is the single biggest driver of your long-term investment returns, not stock-picking or market timing.

Asset allocation isn't a one-size-fits-all formula. A 28-year-old software engineer saving for early retirement needs a completely different mix than a 52-year-old planning for their daughter's wedding next year. Your goals, your stomach for risk, and where you are in life all shape how your money should be divided. Skip this step, and you're essentially flying blind with your hard-earned savings.

This guide walks you through the entire process, from understanding each asset class to building an allocation strategy that actually fits your life. We'll cover age-based rules, goal-based frameworks, risk profiling, and when to rebalance. At Invsify, our AI-powered advisory helps investors build and maintain optimized portfolios based on exactly these principles, your goals, risk tolerance, and time horizon. Whether you're doing it yourself or using a SEBI Registered Investment Advisor, knowing how asset allocation works puts you in control of your financial future.

What asset allocation does for you

Asset allocation is the process of deciding what percentage of your money goes into each broad asset category: equity, debt, gold, and cash equivalents. When you understand how to do asset allocation properly, you stop making decisions based on market noise and start making them based on your actual financial picture. This single decision, how your money is divided, explains roughly 90% of the variation in portfolio performance over time, according to widely cited investment research.

It spreads risk across market cycles

No single asset class performs well in every market condition. Equity markets can drop 30-40% in a correction, but debt instruments like government bonds or fixed deposits tend to hold steady or even gain during those same periods. Gold often moves independently of both, giving your portfolio a buffer when stocks and bonds face pressure at the same time.

When one part of your portfolio falls, another part absorbs the blow. That is the fundamental job asset allocation does for you.

Think of it this way: if you held 100% equity in March 2020, your portfolio dropped sharply within weeks. But a portfolio split between 60% equity, 30% debt, and 10% gold would have fallen far less and recovered faster. Diversification across asset classes, not just across individual stocks or funds, is what actually protects your wealth during volatile periods.

It keeps your returns aligned with your goals

Your financial goals have different timelines and different risk requirements. A 3-year goal like a car purchase needs capital safety above everything else, which means more debt and liquid funds in the mix. A 15-year goal like retirement can absorb short-term volatility, which means you can afford more equity exposure over the long run.

Without an allocation framework, most investors end up overweighting one asset class without realizing it. They might hold 12 different mutual funds thinking they're diversified, when in reality all 12 funds track similar market indices and carry the same directional risk. Asset allocation forces you to look at the big picture and ask whether your current mix actually matches your timeline and what you need by when.

The cost of skipping it

Investors who skip proper asset allocation typically face one of two outcomes. The first is taking on more risk than they can handle, which leads to panic-selling during market corrections and locking in real losses. The second is being too conservative, where money sits in savings accounts or low-yield instruments that lose value to inflation over time.

Both outcomes damage your long-term wealth in measurable ways. A portfolio too aggressive for your timeline might force you to sell equities at a loss right when you actually need the money, such as during a planned home purchase or a medical emergency. A portfolio too conservative means your corpus does not grow fast enough to meet your goals, no matter how disciplined you are about saving. Getting the allocation right from the start prevents both of these problems and gives your money a clear, goal-driven direction.

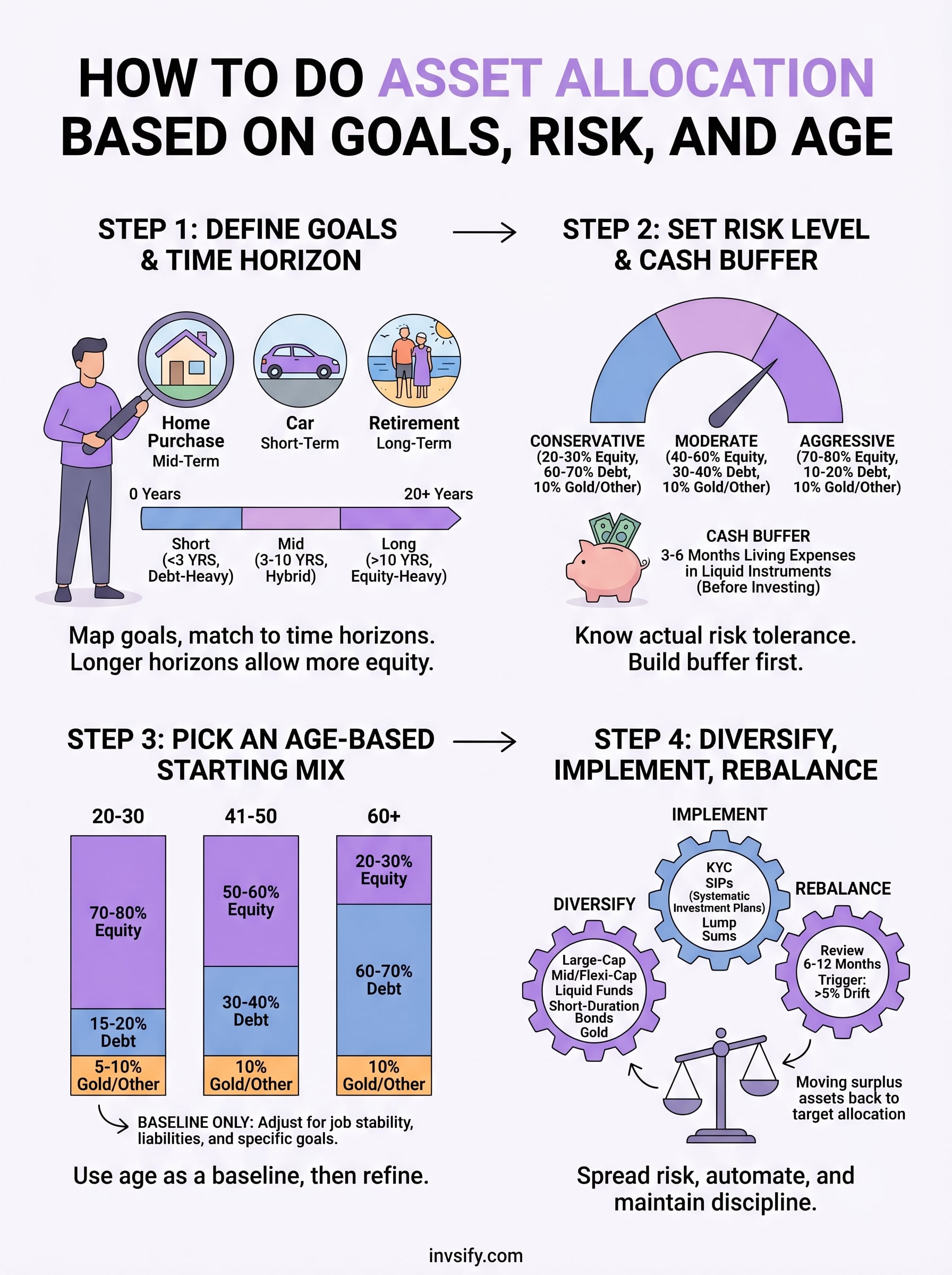

Step 1. Define goals and time horizon

Before you touch any investment product, you need to know exactly what you are investing for and when you will need the money. This step is the foundation of the entire process. When you understand how to do asset allocation properly, the first thing you do is build a clear picture of your goals, because every allocation decision flows from this list.

Map out your financial goals

Write down every financial goal you have, short, medium, and long-term. Be specific. "Retirement" is not a goal, but "build a corpus of Rs. 3 crore by age 55" is. Vague goals produce vague allocations, which means your money ends up parked in the wrong instruments for the wrong duration.

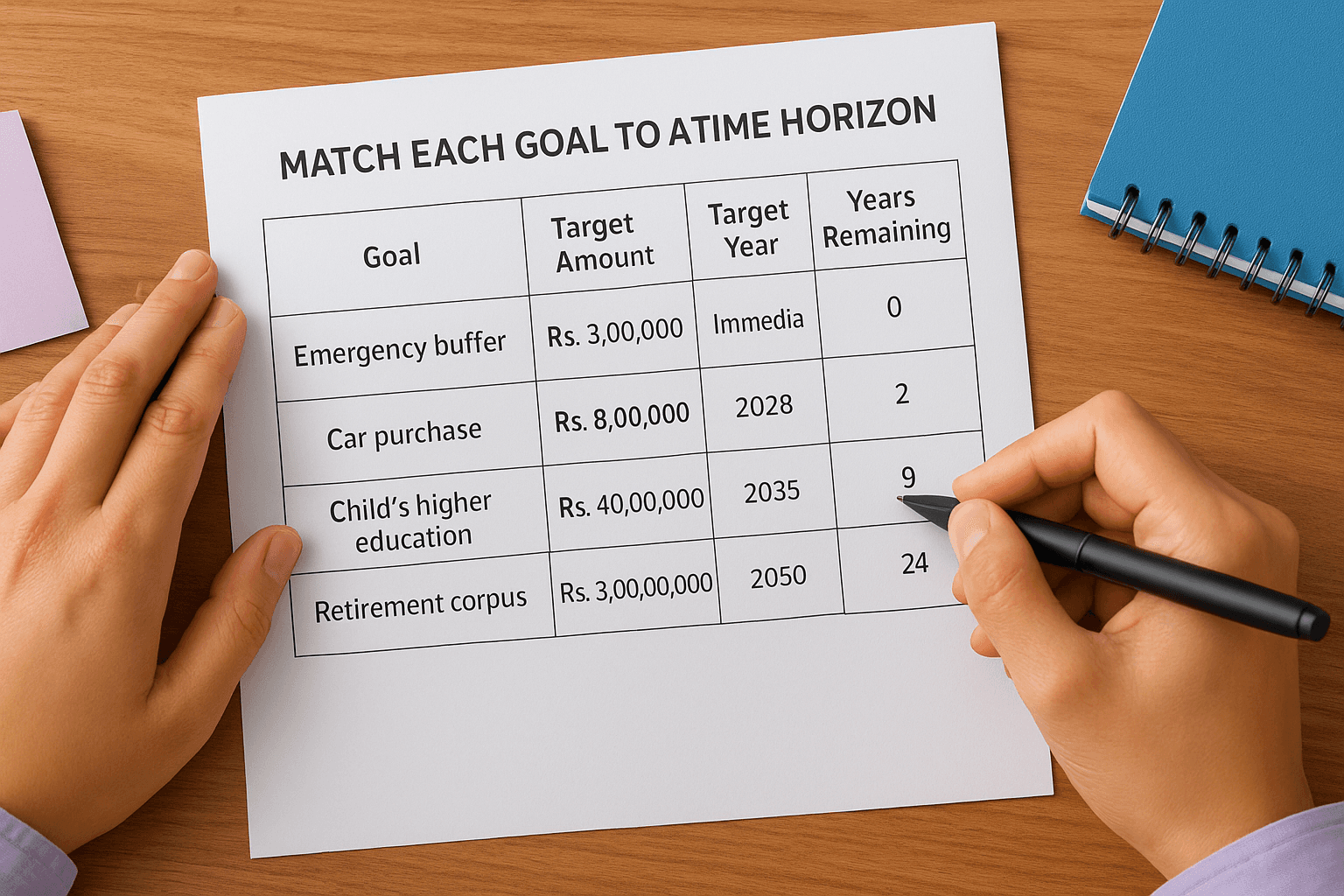

Here is a simple template to start with:

Goal | Target Amount | Target Year | Years Remaining |

|---|---|---|---|

Emergency buffer | Rs. 3,00,000 | Immediate | 0 |

Car purchase | Rs. 8,00,000 | 2028 | 2 |

Child's higher education | Rs. 40,00,000 | 2035 | 9 |

Retirement corpus | Rs. 3,00,00,000 | 2050 | 24 |

Fill this in with your own numbers. Once you can see all your goals on one page, patterns become visible, and you can start assigning each goal its own investment bucket.

Match each goal to a time horizon

Time horizon is the single most important input in your allocation decision. A short-term goal under 3 years cannot afford equity's volatility, so it needs debt-heavy instruments like liquid funds, short-term FDs, or ultra-short bond funds. A long-term goal beyond 10 years can ride out multiple market cycles, so equity should anchor that portion of your portfolio.

The longer your time horizon, the more equity your portfolio can carry, because time itself reduces the real risk of market swings.

Goals between 3 and 7 years sit in the middle. Here, a hybrid approach mixing equity and debt in a 40:60 or 50:50 ratio gives you some growth while keeping downside risk manageable. Knowing your time horizon for each goal removes the guesswork from your allocation entirely.

Step 2. Set your risk level and cash buffer

Once your goals and timelines are clear, the next input you need is your actual risk tolerance. This is not about how much risk you think you should take; it is about how much volatility your behavior can handle without triggering panic decisions. Knowing your real risk level is a core part of understanding how to do asset allocation correctly, because an allocation that pushes you to sell during a market drop defeats its own purpose before it even has a chance to work.

Know your actual risk tolerance

Most investors overestimate their risk appetite during a bull run and discover the hard truth the moment portfolios turn red. A practical way to calibrate this honestly is to ask yourself: if your portfolio dropped 25% in six months, what would you actually do? If your honest answer is "sell everything and move to FD," you are a conservative investor regardless of what you told yourself during the planning phase.

Your true risk tolerance shows up during a downturn, not a rally, so design your portfolio for your worst-case reaction, not your best-case intentions.

Use this as a starting framework before you settle on your mix:

Risk Profile | Equity | Debt | Gold/Other |

|---|---|---|---|

Conservative | 20-30% | 60-70% | 10% |

Moderate | 40-60% | 30-40% | 10% |

Aggressive | 70-80% | 10-20% | 10% |

Your income stability shapes your risk profile just as much as your personality does. A salaried professional with a secure job, low liabilities, and no dependents can afford a more aggressive equity mix than someone with irregular freelance income, even if both investors are the same age with the same goals.

Build your cash buffer first

Before you invest a single rupee into equity or debt instruments, set aside 3 to 6 months of living expenses in a liquid instrument such as a savings account or a liquid mutual fund. This emergency buffer sits completely outside your investment portfolio. Its only job is to cover you when an unplanned expense hits, so you never need to touch your investments at the wrong moment.

Skipping this step breaks your allocation strategy from the inside. Without a cash buffer in place, you are forced to redeem investments under pressure, often when markets are already down and your emotional state is already stretched, which locks in real losses and undoes months of disciplined investing in a single transaction.

Step 3. Pick an age-based starting mix

Age gives you a practical starting point when you're figuring out how to do asset allocation before you've done any deeper analysis. The most widely used rule is the "100 minus your age" formula, which tells you roughly what percentage of your portfolio should sit in equity. At 30, that means 70% equity. At 50, it means 50% equity. It is a blunt instrument, but it gives you a defensible baseline to work from before you refine it using your goals and risk profile from the earlier steps.

Use age as your baseline, then adjust

The standard rule works because time and equity risk move in opposite directions. Younger investors have more time to recover from market corrections, which makes a higher equity allocation appropriate. As you get older and your investment horizon shortens, you need more capital protection and predictable returns from debt instruments to fund near-term expenses without selling equities at the wrong time. Use the table below as your first reference point:

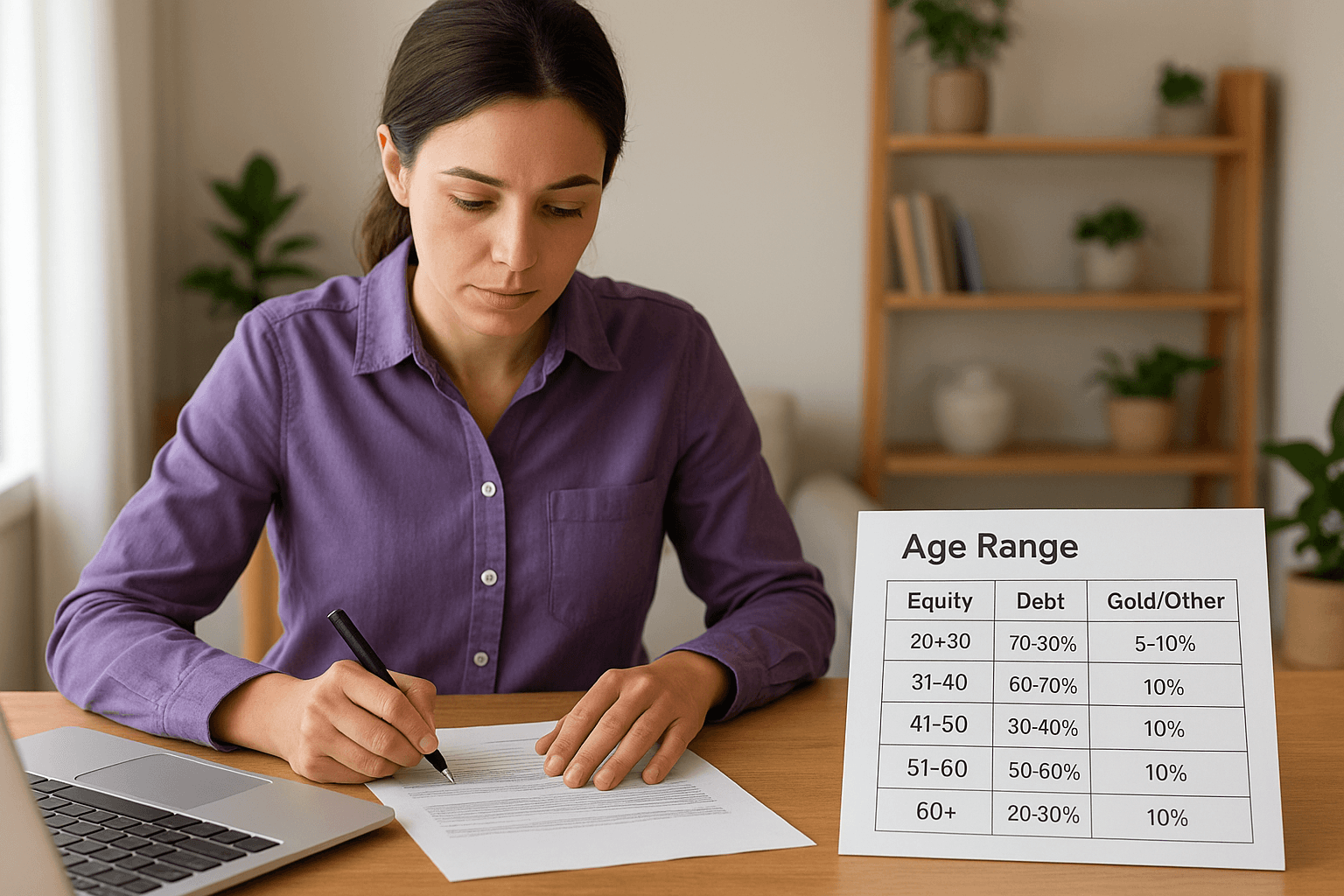

Age Range | Equity | Debt | Gold/Other |

|---|---|---|---|

20-30 | 70-80% | 15-20% | 5-10% |

31-40 | 60-70% | 20-30% | 10% |

41-50 | 50-60% | 30-40% | 10% |

51-60 | 30-40% | 50-60% | 10% |

60+ | 20-30% | 60-70% | 10% |

When to move away from the standard rule

The age-based formula is a starting point, not a final answer. Your specific circumstances can justify shifting significantly from this baseline in either direction. For example, if you are 45 with a stable government job, no outstanding loans, and a 20-year retirement horizon, a 65% equity allocation still makes sense even though the table points to 50-60%.

The age formula sets your floor and ceiling, but your income stability, liabilities, and goal timeline determine exactly where within that range you should land.

Cross-reference this table with your goals list from Step 1. If your single largest goal sits more than 10 years away, you have room to push equity higher than the formula suggests. If multiple goals fall within the next 3 years, pull equity down and shift more into debt and liquid instruments to protect that capital from short-term market swings.

Step 4. Diversify, implement, and rebalance

You have your goals, your risk level, and your age-based starting mix. Now comes the part where you build the actual portfolio and keep it on track over time. This is where knowing how to do asset allocation moves from theory into real action, and the decisions you make here determine whether your allocation holds up through market conditions or collapses the first time volatility hits.

Diversify within each asset class

Picking "60% equity" is not enough on its own. You need to spread that equity allocation across market caps and fund categories to avoid concentration risk. Within your equity bucket, consider splitting across large-cap index funds and mid-cap or flexi-cap funds. On the debt side, mix short-duration and medium-duration instruments rather than locking everything into a single fixed deposit.

Use this as a starting allocation checklist:

Equity, large-cap (60-70% of equity bucket): Nifty 50 or Sensex index fund

Equity, mid-cap (20-30% of equity bucket): Flexi-cap or mid-cap fund

Debt: Liquid fund for short goals and emergencies, plus a short-duration bond fund for medium goals

Gold: Sovereign Gold Bonds or Gold ETF, capped at 10% of your total portfolio

Put your allocation into action

Start by completing your KYC through a SEBI-regulated platform before you invest. Then map each goal from your Step 1 table to a specific fund or instrument. Set up systematic investment plans (SIPs) for every long-term equity goal so you invest consistently without trying to time the market.

For short-term debt allocations, a lump sum into a liquid fund or short-duration fund works well. For equity goals beyond 7 years, monthly SIPs remove the emotional decision-making entirely and let compounding do the heavy work.

Rebalance on a schedule

Markets shift your allocation over time without you doing anything. Review your portfolio every 6 to 12 months and compare your current split against your original target percentages. If equity has grown from 60% to 73% after a strong rally, move the surplus into debt to bring your mix back in line with your plan.

Rebalancing is not about chasing returns; it is about enforcing discipline so your portfolio still matches your actual goals and risk level.

Trigger a rebalance whenever any asset class drifts more than 5 percentage points from its target, even if your scheduled review date has not arrived yet.

Wrap it up and take the next step

Understanding how to do asset allocation gives you a framework that works across every market cycle, every life stage, and every financial goal you set for yourself. The process comes down to four repeatable steps: define your goals and timelines, set your real risk tolerance and cash buffer, pick an age-based starting mix, then diversify within each asset class and rebalance regularly. None of these steps require a finance degree, just honest answers about what you need and when you need it.

Your next move is to actually build that allocation rather than leaving this as a plan on paper. Start with your goals list today, run the numbers against your age-based baseline, and set up SIPs for each long-term bucket. If you want personalized, conflict-free guidance backed by AI and SEBI-registered advice, get started with Invsify and put your portfolio on a clear, goal-driven track from day one.