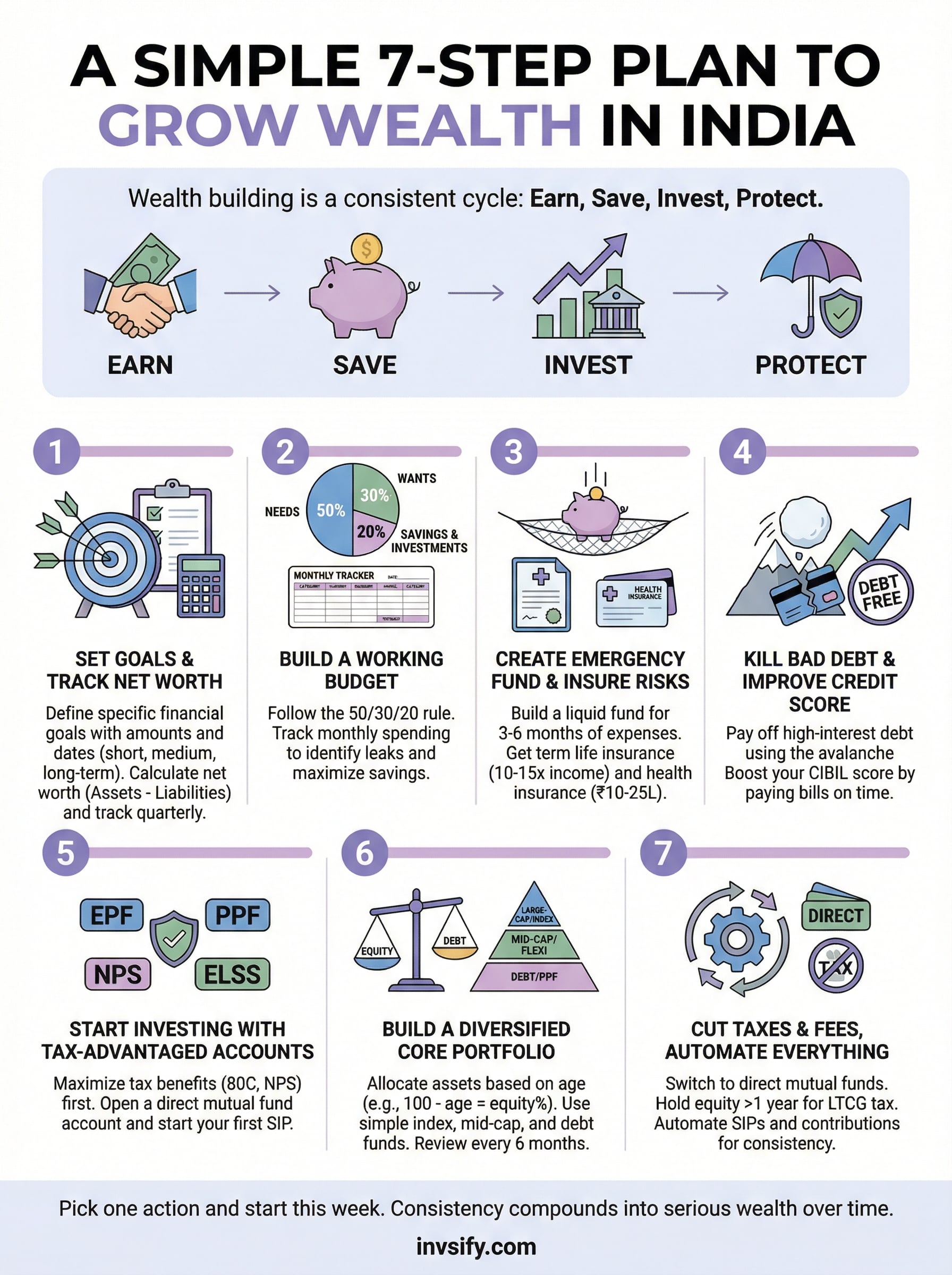

How To Grow Wealth In India: A Simple Step-By-Step Plan

Shlok Sobti

How To Grow Wealth In India: A Simple Step-By-Step Plan

Most people in India earn enough to build real wealth, they just don't have a clear plan for it. Between conflicting advice on social media, pushy distributors with hidden commissions, and an overwhelming number of financial products, figuring out how to grow wealth in India can feel unnecessarily complicated. But it doesn't have to be. Wealth building comes down to a set of repeatable, disciplined steps that anyone with a steady income can follow.

The real challenge isn't a lack of options, it's knowing which ones actually work for your income, goals, and risk appetite. A salaried professional in Pune and a freelancer in Bangalore have very different needs, yet most generic advice treats them the same. What you need is a structured approach backed by data, not opinions from anonymous Reddit threads. That's exactly why we built Invsify, a SEBI Registered Investment Advisor that combines AI-driven insights with conflict-free advice to help you make smarter financial decisions without the guesswork.

This guide breaks down a step-by-step plan to grow your wealth in India, from fixing your savings habits and budgeting basics to choosing the right investment vehicles like SIPs, mutual funds, and equity. Whether you're just starting out or looking to optimize an existing portfolio, you'll walk away with a clear, actionable roadmap you can start using right away.

How wealth grows in India: the fundamentals

Understanding how wealth actually grows is the first step before you pick any product or strategy. Wealth doesn't come from a single lucky investment or a windfall bonus. It comes from a repeatable cycle: you earn, you save a portion, you invest that savings into assets that grow faster than inflation, and you protect what you've built. Get that cycle right consistently, and time does the heavy lifting for you. This is true whether you're starting with ₹5,000 a month or ₹50,000.

The compounding effect: why every year you wait costs you more

Compounding is the process where your returns generate their own returns. If you invest ₹10,000 today at a 12% annual return, after 10 years you have roughly ₹31,000. Wait five extra years to start and you'd need to invest almost double to reach the same result. That's the cost of delay, and it's one of the most concrete things to understand when you think about how to grow wealth in India as a salaried professional.

The single most powerful variable in your wealth-building plan is how early you start, not how much you earn.

Here's how ₹5,000 per month invested via SIP at a 12% annualized return grows depending on when you start:

Investment Period | Total Invested | Estimated Value |

|---|---|---|

10 years | ₹6,00,000 | ~₹11.6 lakh |

20 years | ₹12,00,000 | ~₹49.9 lakh |

30 years | ₹18,00,000 | ~₹1.76 crore |

These figures use a 12% annualized return assumption. Actual returns vary based on fund category and prevailing market conditions, but the directional story holds true across most equity instruments.

The three levers that drive all wealth building

Every strategy in this guide connects back to three core levers: saving rate, investment return, and time horizon. Increase your saving rate and you have more capital to deploy. Choose higher-quality investments and you lift your return. Start early and time amplifies everything. Pull all three levers together and the result is far better than pulling any single one.

Most people focus only on finding the "right" fund or stock, but your saving rate is the most controllable lever in your early years. A person saving 30% of a modest income and putting it into a straightforward index fund will typically build more wealth than someone saving 5% and chasing high-return tips on social media.

Why inflation and taxes make investing non-optional

India's retail inflation has historically averaged around 5 to 6% per year. Money sitting in a savings account earning 3 to 4% interest is actively losing purchasing power each year. Your ₹1 lakh today will have the spending power of roughly ₹60,000 a decade from now if it earns below inflation, even without touching the principal.

Taxes compound this problem further. Short-term capital gains, dividend income, and interest from fixed deposits are all taxable, and they shrink your net returns if you don't plan around them. This is why tax-efficient instruments like ELSS funds under Section 80C, the National Pension System for retirement savings, and the indexation benefit on certain debt fund investments matter so much for Indian investors. The goal isn't just to earn returns; it's to keep as much of those returns as possible working for you.

Step 1. Set goals and track net worth

You can't build wealth without knowing where you're going or where you currently stand. Vague goals like "save more money" don't work because they give you nothing concrete to act on. Every wealth-building decision you make, from choosing a mutual fund to setting a SIP amount, needs to connect back to a specific target with a number and a date attached to it.

Define your financial goals with numbers and dates

Start by listing your goals across three time horizons: short-term (under 3 years), medium-term (3 to 7 years), and long-term (beyond 7 years). Each goal needs a target amount in today's rupees and the approximate year you want to reach it. This forces you to be specific instead of abstract.

A goal without a number and a deadline is just a wish.

Here's a simple template you can fill in right now:

Goal | Target Amount (₹) | Target Year | Time Horizon |

|---|---|---|---|

Emergency fund | 3,00,000 | 2027 | Short-term |

Home down payment | 20,00,000 | 2030 | Medium-term |

Child's education | 40,00,000 | 2035 | Long-term |

Retirement corpus | 3,00,00,000 | 2050 | Long-term |

Replace these numbers with your own figures. Once you have your personal targets on paper, you can work backwards to calculate exactly how much you need to invest each month, which is the foundation of any serious plan for how to grow wealth in India.

Calculate your net worth right now

Your net worth is the most honest scorecard of your financial life. It is simply your total assets minus your total liabilities. Knowing this number gives you a clear baseline to measure progress against every quarter.

Use this formula and plug in your own figures:

Net Worth = Total Assets - Total Liabilities

Assets: savings account balance, fixed deposits, mutual fund and stock portfolio value, EPF and PPF balance, gold, property market value

Liabilities: home loan outstanding, car loan, personal loan, credit card balance

Calculate this number today and record it in a simple spreadsheet. Then revisit it every three months. Watching your net worth grow consistently, even slowly at first, is one of the most reliable ways to stay disciplined with your investment habits over the long term.

Step 2. Build a budget that actually works

A goal and a net worth number give you direction, but a budget gives you fuel. Without a clear picture of where your money goes each month, saving consistently becomes nearly impossible, regardless of how much you earn. Budgeting is not about restricting yourself; it is about making sure your money moves toward your goals rather than disappearing into untracked spending.

Use the 50/30/20 rule as your starting point

The 50/30/20 framework is one of the most practical budgets for salaried professionals figuring out how to grow wealth in India. It splits your take-home pay into three categories: needs, wants, and savings or investments. You spend no more than 50% on needs, 30% on wants, and direct at least 20% toward savings and investments.

The 20% you allocate to investments each month is the number that actually builds your wealth over time.

Here's how this breaks down for a monthly take-home salary of ₹80,000:

Category | Allocation | Amount (₹) |

|---|---|---|

Needs (rent, food, utilities, EMIs) | 50% | 40,000 |

Wants (dining out, subscriptions, travel) | 30% | 24,000 |

Savings and investments | 20% | 16,000 |

If your rent or EMI load pushes needs above 50%, treat the 20% savings target as non-negotiable and cut your discretionary spending to compensate. The ratio is a guide, not a rigid rule, but the savings floor should always hold.

Track your spending with a monthly template

Knowing your budget ratio means nothing if you don't measure actual spending against it. Use a simple monthly tracker to log every rupee you spend, either in a spreadsheet or a notes app. Here is a basic template you can copy and fill in today:

Category | Budgeted (₹) | Actual Spent (₹) | Difference (₹) |

|---|---|---|---|

Rent | 20,000 | 20,000 | 0 |

Groceries | 8,000 | 9,200 | -1,200 |

Transport | 4,000 | 3,500 | +500 |

Dining and leisure | 6,000 | 8,400 | -2,400 |

SIP and investments | 16,000 | 16,000 | 0 |

Review this table at the end of each month and identify the two or three categories where you consistently overspend. Small recurring leaks in your budget compound into large shortfalls over a year, and plugging them directly increases the capital you can invest each month.

Step 3. Create an emergency fund and insure big risks

Before you put a single extra rupee into equity or mutual funds, you need a financial safety net in place. Without one, any unexpected expense, a job loss, a medical bill, or a major repair, forces you to break your investments early, often at a loss. Building an emergency fund and covering your big risks with insurance is not a detour on your path to growing wealth in India; it is a foundation that keeps everything else standing when life gets unpredictable.

Investing without an emergency fund is like building a house without a foundation. One bad event can undo years of progress.

Build a liquid emergency fund first

Your emergency fund should cover three to six months of your essential monthly expenses, not your full salary. Calculate your monthly essentials, rent, groceries, utilities, insurance premiums, and loan EMIs, and multiply by at least three. For most salaried professionals in India, this lands somewhere between ₹1.5 lakh and ₹5 lakh, depending on your city and responsibilities.

Park this money somewhere safe, liquid, and separate from your regular account so you are not tempted to spend it. Here are the best options to hold your emergency fund:

Option | Liquidity | Approximate Return |

|---|---|---|

High-interest savings account | Instant | 3 to 4% |

Liquid mutual fund | 1 to 2 business days | 5 to 7% |

Sweep-in fixed deposit | Instant on sweep | 5 to 6% |

Build this fund before increasing your SIP contributions. Once it is fully funded, leave it alone and only touch it for genuine emergencies, not discretionary purchases.

Get the right insurance before you invest more

Insurance is not an investment product; it is risk protection that prevents a single event from wiping out your net worth. Two policies are non-negotiable for any salaried professional working out how to grow wealth in India: a term life insurance policy and a comprehensive health insurance plan.

For term insurance, buy coverage of at least 10 to 15 times your annual income. For health insurance, a ₹10 lakh to ₹25 lakh family floater plan is a reasonable starting point. Avoid mixing insurance with investment through ULIPs or endowment plans; keep them separate to get better returns from your investments and better coverage from your insurance.

Step 4. Kill bad debt and improve your credit score

Bad debt is one of the fastest ways to destroy wealth before you even start building it. A personal loan at 16% interest or a credit card balance at 36% annually cancels out any investment returns you might be earning on the other side of your balance sheet. If you carry high-interest debt while simultaneously investing, you are paying more in interest than you are earning from most equity instruments. Clearing bad debt is not a separate task from learning how to grow wealth in India; it is a core part of the process.

Paying off a 36% credit card balance is the equivalent of earning a guaranteed 36% return on that money. No mutual fund matches that risk-free.

Prioritize high-interest debt using the avalanche method

The debt avalanche method directs every extra rupee you have toward the debt with the highest interest rate first, while paying minimums on everything else. Once the most expensive debt is gone, you roll that payment into the next highest-rate balance. This approach saves you the most money in interest over time compared to any other repayment sequence.

Here is an example of how to order your repayments:

Debt Type | Outstanding Balance (₹) | Interest Rate | Priority |

|---|---|---|---|

Credit card | 80,000 | 36% p.a. | 1st |

Personal loan | 2,00,000 | 16% p.a. | 2nd |

Car loan | 5,00,000 | 9% p.a. | 3rd |

Home loan | 40,00,000 | 8.5% p.a. | Last |

Home loans sit at the bottom because the interest rate is low, the interest is partially tax-deductible under Section 24(b), and foreclosing early rarely makes financial sense versus investing the surplus.

Improve your CIBIL score with consistent habits

Your CIBIL score directly affects your borrowing costs for years to come. A score above 750 qualifies you for lower interest rates on home loans and credit products, which translates into real savings over a multi-decade loan. Two actions move the needle most reliably: pay every EMI and credit card bill in full before the due date and keep your credit utilization ratio below 30% of your total credit limit at all times.

Check your CIBIL score for free once a year through the official CIBIL website. If your score is below 700, avoid applying for new credit until it recovers, because each hard inquiry temporarily lowers your score further.

Step 5. Start investing with the right accounts

With your emergency fund in place, bad debt cleared, and a working budget, you are ready to put money into investments. The biggest mistake most first-time investors make is jumping straight into individual stocks or chasing the latest trending fund without first using the tax-advantaged accounts the Indian tax code already gives you. Choosing the right account structure before picking any product saves you real money every year and keeps more of your returns compounding on your behalf instead of going to the government.

Use tax-advantaged accounts before anything else

Every salaried professional in India should fill these accounts first before investing in taxable instruments. They give you legally guaranteed tax deductions or tax-free growth, which directly improve your net return without requiring you to take on more risk.

The single most efficient investment you make each year is the one that reduces your taxable income before your money even touches a market.

Here is a quick overview of the core tax-advantaged accounts available to Indian investors:

Account | Annual Limit | Tax Benefit | Best For |

|---|---|---|---|

EPF (via employer) | 12% of basic salary | Tax-free returns up to certain limits | Retirement, forced savings |

PPF (Public Provident Fund) | ₹1.5 lakh | Section 80C deduction, tax-free returns | Long-term risk-free savings |

ELSS mutual funds | ₹1.5 lakh (80C) | Section 80C deduction, LTCG applies after 1 year lock-in | Equity growth with tax benefit |

NPS (National Pension System) | ₹50,000 additional (80CCD(1B)) | Extra deduction beyond 80C limit | Retirement corpus |

Max your Section 80C limit of ₹1.5 lakh each year through a combination of EPF contributions, PPF, and ELSS before you invest a single rupee in a regular taxable account.

Open a direct mutual fund account and start your first SIP

Once your tax-advantaged slots are filled, open a direct mutual fund account through the AMC's own website or through the MFCentral platform to avoid distributor commissions entirely. Direct plans of the same fund consistently deliver 0.5% to 1% higher annual returns than regular plans because the distribution commission is removed.

Set up your first SIP with a fixed date aligned to your salary credit date, ideally within two to three days after your salary hits your account. This removes the decision entirely and makes investing automatic, which is exactly how consistent wealth gets built over time when you are figuring out how to grow wealth in India on a regular salary.

Step 6. Build a diversified core portfolio

Picking individual stocks or doubling down on a single asset class is one of the most common mistakes Indian investors make once they have money to deploy. Diversification is not about spreading money thin; it is about building a portfolio where different asset classes behave differently under the same market conditions, so a crash in one does not wipe out everything else. This is the structural step that separates investors who build lasting wealth from those who lose ground in bad market years.

Choose the right asset allocation for your stage

Your asset allocation, the percentage split between equity, debt, and other assets, is the single biggest driver of your long-term returns and your ability to sleep at night during a market downturn. A simple rule of thumb to start with: subtract your age from 100 to get your equity percentage. A 30-year-old holds roughly 70% in equity and 30% in debt. As you approach retirement, you shift progressively toward safer instruments.

Your asset allocation matters more than which specific fund you pick inside each category.

Here is a starting allocation template based on age group:

Age Group | Equity | Debt | Gold / Alternatives |

|---|---|---|---|

20 to 30 years | 70 to 80% | 15 to 25% | 5% |

31 to 45 years | 60 to 70% | 25 to 30% | 5 to 10% |

46 to 55 years | 45 to 55% | 35 to 45% | 5 to 10% |

56 years and above | 30 to 40% | 50 to 60% | 5 to 10% |

Build the core portfolio with simple, proven instruments

Once your allocation is set, keep your core portfolio simple and low-cost. Most salaried investors doing research into how to grow wealth in India overcomplicate their portfolios with 12 or more funds that overlap almost entirely. A focused three-fund structure covering large-cap equity, mid-cap equity, and debt covers the core of what most investors actually need.

Large-cap index fund or Nifty 50 fund: forms the stable anchor of your equity allocation

Mid-cap or flexi-cap fund: adds growth potential with slightly higher risk

Short-duration debt fund or PPF: provides stability and capital preservation

Review your portfolio allocation once every six months, not every week. Rebalance only when your equity allocation drifts more than 5 percentage points from your target. Frequent tinkering costs you in taxes and transaction friction, both of which quietly eat into your returns over time.

Step 7. Cut taxes and fees, then automate everything

Tax drag and fund fees are two of the quietest wealth destroyers in any Indian investor's portfolio. You might be building a well-diversified portfolio and hitting your savings targets every month, but unnecessary taxes and high expense ratios chip away at your compounding returns year after year without any visible single-line deduction. Fixing these two leaks, and then automating your entire investment process, is the final step that locks in everything you have built so far when learning how to grow wealth in India.

Reduce the tax drag on your investment returns

Every rupee you keep from the taxman is a rupee that continues compounding for you. The most effective way to reduce tax drag is to hold equity mutual funds for more than one year before selling, which shifts your gains from short-term capital gains tax at 20% to long-term capital gains tax at 12.5% above the ₹1.25 lakh annual exemption. For debt funds, consider the timing of redemptions carefully since gains are now taxed at your income slab rate regardless of holding period.

Keeping your fund expense ratios low and your holding period long are the two most reliable ways to improve your net return without changing your asset allocation at all.

Here are the key fee and tax levers you can act on immediately:

Action | What You Save |

|---|---|

Switch from regular to direct mutual funds | 0.5 to 1% per year in distributor commission |

Hold equity funds over 1 year | STCG at 20% drops to LTCG at 12.5% |

Max Section 80C via ELSS, EPF, PPF | Up to ₹46,800 in tax savings annually |

Use NPS for extra ₹50,000 deduction (80CCD(1B)) | Up to ₹15,600 additional tax saving |

Automate your investments so discipline is built in

Automation removes the single biggest risk in any investment plan: your own inconsistency on a bad month. Set your SIP dates to trigger two or three days after your salary credit date so the money moves before you can redirect it toward discretionary spending. Link your PPF contribution to a standing instruction from your bank account so it transfers automatically in April each year, which fills your annual limit without requiring a single manual decision on your part.

Once your SIPs, PPF transfers, and NPS contributions run automatically, your only active job is reviewing your portfolio allocation every six months. Remove the friction from investing and consistency becomes the default, which is exactly how long-term wealth gets built on a regular salary.

A simple plan you can start this week

You now have a complete roadmap for how to grow wealth in India on a regular salary. Every step in this guide builds on the one before it: set clear goals, track your net worth, budget with intention, protect your finances with an emergency fund and insurance, eliminate high-interest debt, fill your tax-advantaged accounts, build a diversified portfolio, and automate the entire system. None of these steps require a high income or special connections, just consistent action taken in the right order.

Pick one action from this guide and complete it before the week ends. Calculate your net worth, open a direct mutual fund account, or set up your first SIP. Small moves compound into serious results when you repeat them consistently. If you want personalized, conflict-free guidance built around your specific goals and income, get started with Invsify and let AI-powered advice do the heavy lifting for you.