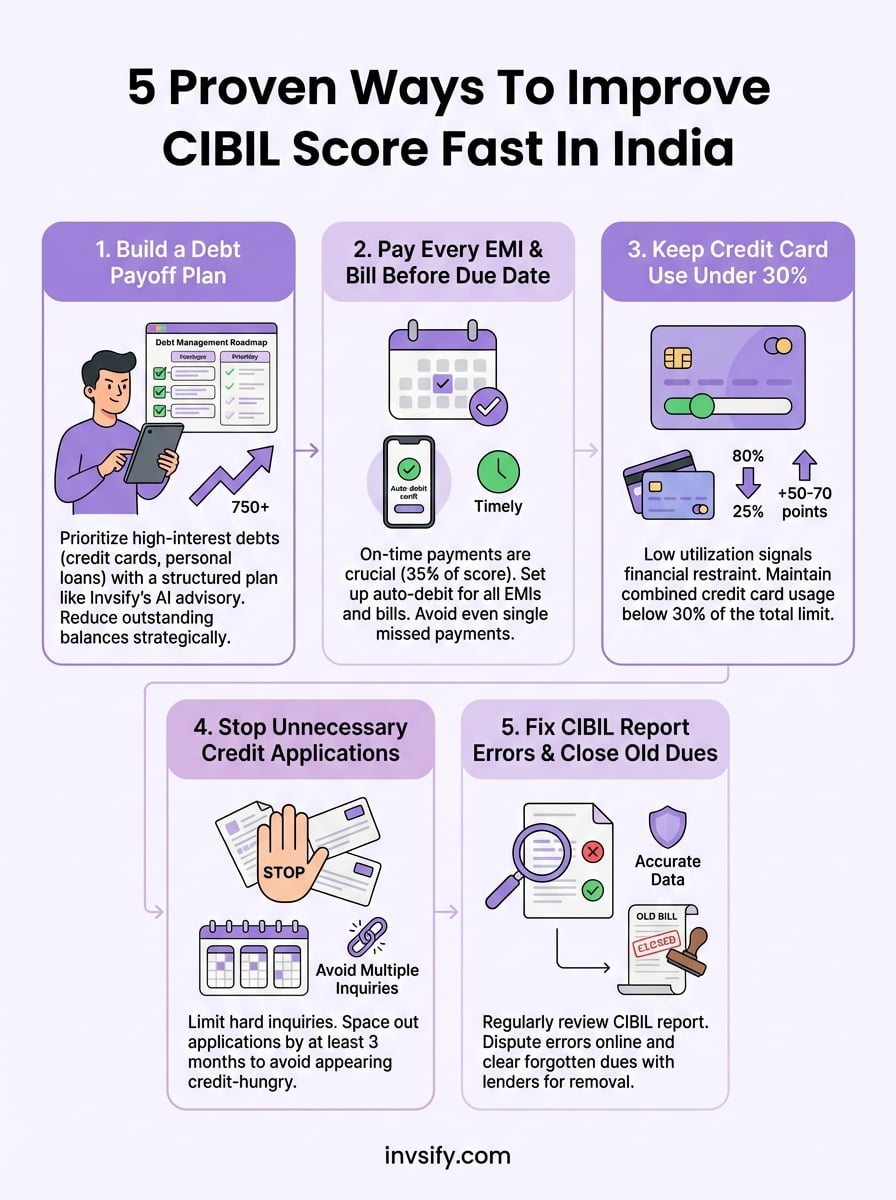

5 Proven Ways To Improve CIBIL Score Fast In India (2026)

Shlok Sobti

5 Proven Ways To Improve CIBIL Score Fast In India (2026)

A low CIBIL score can shut doors, loan rejections, higher interest rates, and limited financial options. If you're searching for how to improve CIBIL score fast, you're not alone. Lakhs of Indians face this challenge every year, often unsure where to begin.

The good news? Your credit score isn't permanent. With the right strategies and consistent action, you can push your score toward that 750+ mark that unlocks better loan terms and credit card approvals.

At Invsify, we help salaried individuals in India make smarter financial decisions through AI-powered advisory. Improving your CIBIL score is one of the essential steps toward building long-term wealth. Here are 5 proven methods to get your score moving upward, fast.

1. Use Invsify to build a debt payoff plan

Debt weighs down your CIBIL score faster than most other factors. Multiple unpaid loans or high-interest credit card balances signal financial stress to credit bureaus, dragging your score into the danger zone. The key to recovery is a structured payoff plan that tackles your debts strategically.

Invsify's AI-powered advisory helps you map your entire debt portfolio and prioritize which loans to clear first. Our platform analyzes your income, expenses, and debt mix to create a custom roadmap. This isn't guesswork, it's data-backed planning designed for salaried Indians who want real results.

Why it moves your CIBIL score

Your credit utilization ratio and payment history account for over 60 percent of your CIBIL score. When you reduce outstanding debt systematically, both factors improve immediately. Clearing high-interest debts first frees up cash flow, which you can then redirect toward other dues.

Paying down debt consistently shows lenders you can manage credit responsibly.

Bureaus track how much you owe relative to your total credit limit. Lower balances mean better scores, often within 30 to 60 days of consistent payments.

Steps to do it in India

Start by connecting your bank accounts to Invsify's portfolio tracker. The platform pulls your debt data automatically and calculates your total outstanding amount. You'll see which loans carry the highest interest rates and which are eating into your monthly budget.

Next, use Invsify's debt optimizer to generate a payoff sequence. Target credit cards and personal loans first, as they typically carry rates above 15 percent. Set up automated payments through your bank's netbanking portal to ensure you never miss a due date.

Mistakes to avoid

Don't scatter your payments across all debts equally. Focus on one high-interest debt at a time while maintaining minimum payments on others. Avoid taking new loans to pay old ones unless the interest rate drops significantly.

Many people close credit cards immediately after clearing balances. Keep old accounts open to maintain your credit history length, which also impacts your score.

How fast you can see results

You'll notice movement in 45 to 60 days if you stick to the plan. CIBIL updates monthly, so consistent debt reduction shows up in the next reporting cycle. Larger debts take longer, but even a 10 percent reduction can lift your score by 20 to 30 points.

2. Pay every EMI and bill before the due date

Payment history is the single most powerful factor in how to improve CIBIL score, accounting for 35 percent of your total score. Every late payment, whether it's an EMI or a credit card bill, sends a red flag to credit bureaus. The solution is simple but requires discipline: pay everything before the deadline.

Why it moves your CIBIL score

Lenders use your payment track record to predict future behavior. On-time payments prove you're reliable, while missed deadlines suggest financial instability. CIBIL records every delay, even if it's just two days late.

A single missed payment can drop your score by 50 to 100 points.

Bureaus flag accounts as delinquent after 30 days, but damage starts accumulating from day one. Repeated delays create a pattern that takes months to reverse, making timely payments your fastest route upward.

Steps to do it in India

Set up auto-debit for all EMIs through your bank's netbanking portal. This guarantees payments process automatically on the due date. For credit cards, use the auto-pay option available in most banking apps, selecting either minimum due or full amount.

Create calendar reminders three days before each deadline as a backup. Check your account balance the day before to ensure sufficient funds are available.

Mistakes to avoid

Never pay just the minimum due on credit cards if you can avoid it. Interest compounds quickly, and carrying balances month after month hurts your utilization ratio. Avoid partial payments on EMIs, as lenders report these as delayed or missed.

How fast you can see results

Your score responds within 30 to 45 days of consistent on-time payments. CIBIL updates monthly, so three consecutive clean cycles can lift your score by 30 to 50 points. The longer your streak, the stronger your profile becomes.

3. Keep credit card use under 30 percent

Your credit utilization ratio is the second most powerful lever in how to improve CIBIL score, right after payment history. This ratio measures how much of your total credit limit you're actually using. High utilization signals desperation to lenders, even if you pay on time. Keeping your usage below 30 percent shows financial restraint and boosts your score fast.

Why it moves your CIBIL score

Bureaus interpret high credit card balances as a warning sign of potential default risk. When you max out cards or consistently use more than 30 percent, your score drops automatically. Lower utilization proves you're not dependent on borrowed money for daily expenses.

Reducing utilization from 80 percent to 25 percent can lift your score by 50 to 70 points in one cycle.

The calculation spans all your cards combined. If you hold three cards with a total limit of ₹3 lakh, keep your combined balance under ₹90,000 at all times.

Steps to do it in India

Check your current utilization by dividing your total outstanding balance by your total credit limit. If you're over 30 percent, pay down balances immediately or request a limit increase through your bank's app.

Split large purchases across multiple billing cycles instead of one swipe. Pay bills mid-cycle in addition to the due date to keep reported balances low when bureaus update monthly.

Mistakes to avoid

Never close old credit cards to reduce utilization. Closing accounts lowers your total available credit, which pushes your ratio higher. Avoid opening multiple new cards just to inflate your limit, as this triggers hard inquiries that hurt your score.

How fast you can see results

Your score adjusts within 30 to 45 days once utilization drops below 30 percent. CIBIL pulls data monthly, so consistent low usage shows up in the next reporting window. Dropping to 10 percent or less can accelerate gains further.

4. Stop unnecessary credit applications and inquiries

Every time you apply for a loan or credit card, the lender runs a hard inquiry on your CIBIL report. These inquiries stay visible for two years and signal to other lenders that you're actively seeking credit. Multiple applications in a short window make you look financially desperate, dragging your score down by 5 to 10 points per inquiry. Understanding how to improve CIBIL score means knowing when to stop applying.

Why it moves your CIBIL score

Bureaus track how often lenders pull your credit report. Four or more inquiries within six months triggers a red flag, suggesting you're scrambling for funds. Each hard pull directly lowers your score, and the cumulative effect compounds quickly.

Too many credit applications in a short span can drop your score by 30 to 50 points.

Lenders interpret this pattern as high credit risk, making future approvals harder even if you pay existing debts on time.

Steps to do it in India

Apply for credit only when absolutely necessary. Space out applications by at least three months to avoid clustering. Before applying, use pre-qualification tools offered by banks, which perform soft checks that don't impact your score. Research eligibility criteria thoroughly to ensure you meet requirements before submitting formal applications.

Mistakes to avoid

Never apply to multiple lenders simultaneously hoping one approves. Each rejection adds an inquiry with no benefit. Avoid applying for store credit cards at checkout counters just to save 5 or 10 percent, as these inquiries pile up faster than you realize.

How fast you can see results

Your score stabilizes within 30 days once you stop new applications. Inquiries lose impact after six months and disappear completely after two years. Focus on maintaining zero new applications for at least 90 days to see meaningful recovery.

5. Fix errors in your CIBIL report and close old dues

Errors in your credit report can silently destroy your score for months without you realizing it. Incorrect account information, duplicate entries, or outdated dues create a distorted picture of your creditworthiness. Cleaning up these mistakes is one of the fastest ways to see improvement when learning how to improve CIBIL score.

Why it moves your CIBIL score

Bureaus rely on data from lenders, and reporting errors happen more often than you'd think. A wrongly marked late payment or an account that shows active after closure drags your score down unfairly. Disputing and correcting these entries removes negative marks instantly once verified.

A single error correction can lift your score by 30 to 100 points in one cycle.

Steps to do it in India

Request your free CIBIL report once a year through their official website. Review every account, payment history, and personal detail for accuracy. File disputes online through CIBIL's portal for any incorrect information, attaching supporting documents. Contact lenders directly to settle any forgotten old dues and request a no-objection certificate once cleared.

Mistakes to avoid

Never ignore small errors thinking they don't matter. Even a ₹500 unpaid bill from years ago can hurt your score. Avoid disputing accurate negative information, as bureaus reject frivolous claims and your score stays unchanged.

How fast you can see results

Corrections process within 30 days after verification. Your score updates in the next monthly cycle once errors are removed and old dues are marked as closed.

What to do this week

Your CIBIL score won't fix itself. Pick one action from this guide and execute it this week. Order your free credit report and scan for errors. Set up auto-debit for all EMIs and credit card bills. Check your credit card utilization and pay down any balance above 30 percent. Small, consistent moves build momentum faster than waiting for the perfect moment.

Understanding how to improve CIBIL score is just the beginning. Real progress happens when you pair these strategies with a complete financial plan that includes investments, tax optimization, and debt management. At Invsify, our AI-powered platform helps salaried Indians track their financial health in one place, including debt payoff plans that directly lift your score. Start building your personalized financial plan today and take control of your credit future.