How To Make Investment Decisions: A Step-By-Step Framework

Shlok Sobti

How To Make Investment Decisions: A Step-By-Step Framework

Most people don't struggle with wanting to invest, they struggle with knowing how to make investment decisions that actually align with their life. Should you pick mutual funds or stocks? Go aggressive or play it safe? Follow what your colleague did or chart your own path? Without a clear framework, every choice feels like a coin toss, and that uncertainty costs real money over time.

The truth is, good investment decisions aren't about luck or market timing. They come down to a repeatable process, one that factors in your financial goals, your risk tolerance, your time horizon, and the data behind each option. Once you have that structure, the noise fades and the right moves become obvious.

That's exactly what this guide walks you through. We've broken down the decision-making process into clear, actionable steps, from evaluating where you stand financially to choosing the right instruments for your goals. And if you want AI-backed, conflict-free support along the way, Invsify's advisory platform is built to help salaried professionals in India do exactly this, make smarter investment decisions with data, not guesswork.

Before you invest: set your baseline

Before you even think about which fund to pick or how to make investment decisions that actually build wealth, you need a clear picture of where you stand today. Jumping into investments without this baseline is like navigating without a map. You might move, but you won't know if you're heading anywhere useful.

Map your income, expenses, and liabilities

Start by listing your monthly take-home income and every fixed expense you carry, including rent or EMI, insurance premiums, existing SIPs, and utility bills. Then subtract your variable expenses like food, transport, and discretionary spending. What remains is your investable surplus, and that number drives every decision you make from here.

Here's a simple baseline snapshot you can fill in right now:

Category | Monthly Amount (₹) |

|---|---|

Take-home income | |

Fixed expenses (rent, EMIs) | |

Variable expenses (food, transport) | |

Existing SIPs / investments | |

Investable surplus |

This exercise takes about 20 minutes and gives you one number that anchors your entire investment plan. Without it, you're guessing at how much you can actually commit each month, and that guess tends to be optimistic.

Check your emergency fund and insurance coverage

Before you deploy any surplus into markets, confirm you have an emergency fund covering at least 3 to 6 months of expenses sitting in a liquid account, such as a savings account or a liquid mutual fund. This buffer ensures a job loss or medical bill doesn't force you to sell investments at the worst possible time.

If you don't have an emergency fund yet, build that first. Investing without one is a risk that no asset allocation strategy can fix.

Health and term insurance also belong at this stage, not later. If you're underinsured, a single large expense can wipe out years of compounded returns. Verify your health cover is adequate for your city and family size. Confirm your term cover is at least 10 to 15 times your annual income. Only after these two foundations are solid should you move forward and start building your actual investment portfolio.

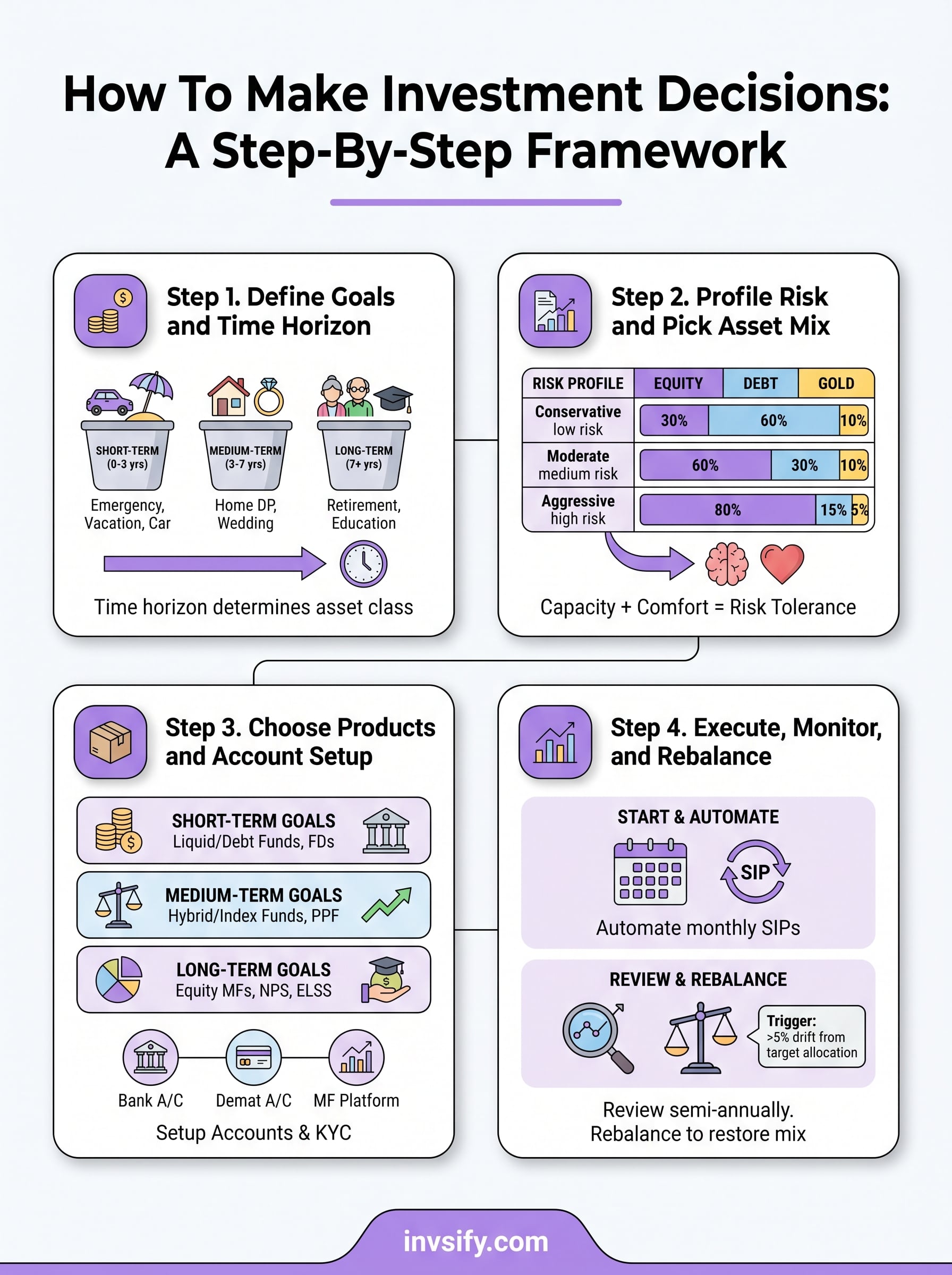

Step 1. Define goals and time horizon

Every sound investment decision starts with a specific goal. Vague targets like "grow my wealth" won't cut it because they give you no way to measure progress, pick the right product, or decide how much to invest. Knowing how to make investment decisions that actually hold up means translating intentions into concrete, measurable goals with a number attached and a deadline to match.

Name and classify each goal

Write down every financial goal you have and assign each one a clear target amount and a year by which you want to reach it. Then group them into three time buckets:

Time Horizon | Range | Example Goals |

|---|---|---|

Short-term | 0 to 3 years | Emergency top-up, vacation, car |

Medium-term | 3 to 7 years | Home down payment, wedding |

Long-term | 7+ years | Retirement corpus, child's education |

The time horizon on a goal is not optional detail; it is the single biggest factor that determines which asset class belongs in your portfolio.

Align the investment amount to each goal

Once you have your goals listed, work backward to find the monthly SIP or lump sum amount needed to hit each target. Divide the target amount by the months remaining and adjust upward for expected returns from your chosen asset class. Here's a quick reference for a ₹10 lakh target at a 10% annual return:

Timeline | Monthly SIP Required (approx.) |

|---|---|

3 years | ₹25,400 |

5 years | ₹12,900 |

7 years | ₹8,200 |

Step 2. Profile risk and pick asset mix

Your goals tell you where you want to go; your risk profile tells you how you can get there. Knowing how to make investment decisions that you'll actually stick with depends on matching your portfolio to what you can genuinely tolerate, both financially and emotionally. An aggressive portfolio that keeps you up at night leads to panic selling at the worst moment, which destroys returns faster than any market correction.

Determine your risk tolerance

Two factors shape your risk tolerance: your capacity to absorb losses (financial risk) and your comfort with seeing your portfolio value fluctuate (behavioral risk). Capacity is objective, based on your income stability, liabilities, and time horizon. Comfort is personal. Answer these three questions honestly to identify which profile fits you:

Question | Low Risk | Medium Risk | High Risk |

|---|---|---|---|

How long before you need this money? | Under 3 years | 3 to 7 years | 7+ years |

How would you react to a 20% portfolio drop? | Sell immediately | Hold and review | Buy more |

Is your income stable and predictable? | No | Mostly | Yes |

Your time horizon is the strongest override here: even a risk-averse investor can hold equity-heavy portfolios if the goal is 10+ years away.

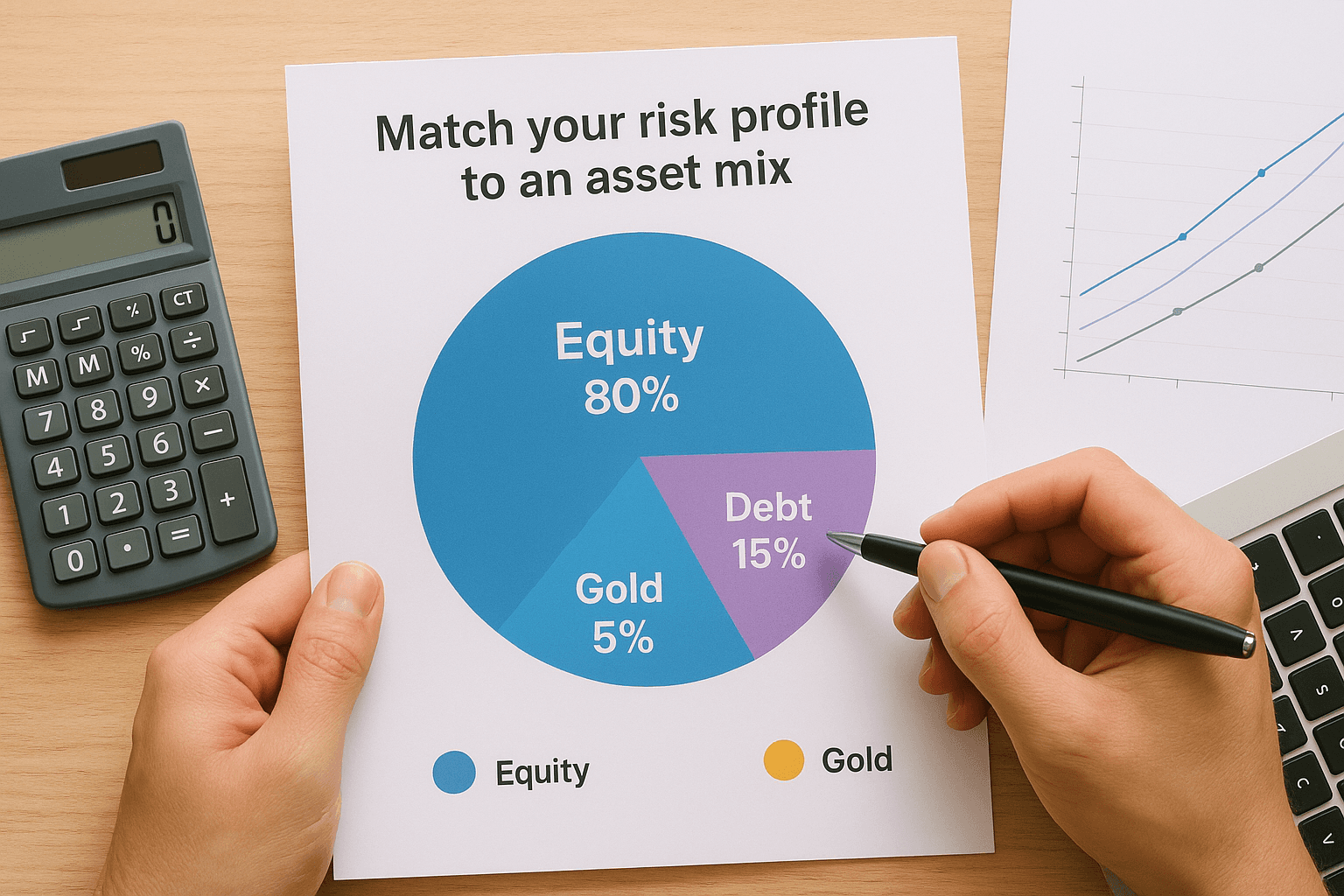

Match your risk profile to an asset mix

Once you have your profile, translate it into a concrete allocation across equity, debt, and gold. Use the table below as your starting point, then adjust based on your specific goals:

Risk Profile | Equity | Debt | Gold |

|---|---|---|---|

Conservative | 30% | 60% | 10% |

Moderate | 60% | 30% | 10% |

Aggressive | 80% | 15% | 5% |

Review this allocation every 12 months or after any major life change, such as a salary hike, a new dependent, or a large purchase. Your risk profile is not static.

Step 3. Choose products and account setup

With your risk profile and asset allocation in hand, you now need to match each goal to the right investment product. This is where knowing how to make investment decisions moves from theory into action. The Indian market gives you plenty of options, so the goal here is to simplify, not overcomplicate.

Match products to each goal bucket

Different goals need different instruments, and picking the wrong one, such as a small-cap fund for a 2-year goal, can leave you selling at a loss when you need the money most. Use the table below to map your goal buckets to the right products:

Goal Type | Recommended Products |

|---|---|

Short-term (0 to 3 years) | Liquid mutual funds, short-duration debt funds, FDs |

Medium-term (3 to 7 years) | Hybrid funds, index funds, PPF |

Long-term (7+ years) | Diversified equity mutual funds, NPS, ELSS |

Always prioritize low-cost index funds for your equity allocation before adding actively managed funds; expense ratios compound just like returns do.

Open the right accounts before you invest

You need three accounts in place before your first rupee moves: a bank account linked for SIP mandates, a Demat account for direct equity or ETFs, and a mutual fund platform account. Complete your KYC through SEBI-registered platforms using your PAN and Aadhaar. Most platforms finish this in under 24 hours. Once your accounts are active, automate your SIPs on the day after your salary credit so you invest before you spend.

Step 4. Execute, monitor, and rebalance

Setting up your portfolio is only half the job. Knowing how to make investment decisions that compound over time means you also need to track performance regularly and adjust when your allocation drifts from your target. Markets move, life changes, and a portfolio left unchecked for years can quietly shift into a risk profile that no longer matches yours.

Start investing and set a review schedule

Automate your SIPs on the same date every month, ideally within two days of your salary credit. This removes the temptation to time the market and builds discipline without effort. Beyond that, schedule two portfolio reviews per year, roughly every six months, and block time in your calendar now so it actually happens.

Reviewing too often, like daily or weekly, leads to emotional decisions. Reviewing too rarely means small misalignments grow into big ones.

Know when to rebalance

Rebalancing means selling a portion of the over-performing asset class and moving those funds into the underperforming one to restore your target allocation. Use this simple trigger system:

Trigger | Action Required |

|---|---|

Any asset class drifts over 5% from target | Rebalance to original allocation |

Major life change (new job, marriage, child) | Re-profile risk and reset allocation |

Goal achieved or deadline within 12 months | Shift that goal's funds to capital-safe instruments |

Rebalancing is not about chasing returns; it is about staying aligned with the plan you built in the earlier steps.

What to do next

You now have a complete framework for how to make investment decisions that hold up over time. Start with your baseline, set specific goals, match your risk profile to the right asset mix, pick products that fit each goal bucket, and review your portfolio twice a year. Each step builds on the one before it, so skipping any part weakens the whole plan.

The biggest mistake most salaried investors make is waiting until they feel "ready." You don't need more information. You need to run the numbers on your current situation and take the first step. That means calculating your investable surplus today and naming at least one financial goal with a target amount and a deadline.

If you want AI-backed, conflict-free guidance through every step of this process, Invsify is built exactly for this. Start your investment journey with Invsify and get personalized advice grounded in data, not commissions.