How To Make Smart Investment Decisions In India In 2026

Shlok Sobti

How To Make Smart Investment Decisions In India In 2026

Most Indians start investing with a tip from a colleague, a trending stock on social media, or a mutual fund their bank pushed on them. None of that qualifies as knowing how to make smart investment decisions, and the gap between guessing and deciding well is where most wealth gets quietly destroyed. In 2026, with new tax rules, shifting market dynamics, and an overwhelming number of investment products, that gap is only getting wider for salaried individuals trying to grow their money with intention.

The good news? You don't need a finance degree to invest well. You need a clear framework, one that covers goal-setting, risk assessment, diversification, and ongoing portfolio management. That's exactly what this guide breaks down, step by step, with a focus on what actually works for Indian investors right now.

At Invsify, we built our SEBI Registered AI-powered advisory platform specifically to help people move from confusion to clarity when it comes to their money. This article reflects the same principle: actionable, conflict-free guidance that helps you make decisions based on data and goals, not noise. Let's walk through everything you need to get this right.

What smart investment decisions mean in India in 2026

Understanding how to make smart investment decisions starts with defining what that phrase actually means for your situation. In India in 2026, smart investing is not simply chasing the highest returns; it's about making deliberate choices that align with your goals, your risk capacity, and the current tax and market environment. A well-reasoned decision remains smart even if the market moves against you in the short term. Outcomes and decision quality are two different things, and confusing them is one of the most common traps Indian investors fall into.

The regulatory and market landscape has shifted

The Union Budget 2025 changed the rules significantly. Long-term capital gains (LTCG) tax on equity investments now sits at 12.5%, and the indexation benefit for debt mutual funds was removed. Both changes directly reduce what you actually keep after your returns come in. On top of that, inflation in India consistently runs between 5% and 6%, which means a bank fixed deposit earning 7% delivers a real return of barely 1 to 2% before taxes. Knowing this context is not optional; it's the foundation of every rational investment choice you make.

In 2026, a smart investment decision accounts for after-tax, after-inflation returns, not just the headline rate your bank or distributor shows you.

Process beats outcome every time

Most people confuse a good result with a good decision. Your neighbor who doubled money on a small-cap stock in 2023 may have taken a poorly calculated risk that happened to work out. Smart investing runs on repeatable, process-driven logic: you know why you're buying a product, what role it plays in your portfolio, and under what conditions you would exit.

Here's a quick framework to test whether a choice qualifies as a smart decision or a hopeful guess:

Question | Smart decision | Hopeful guess |

|---|---|---|

Why are you buying this? | Tied to a clear goal and asset match | "It looks promising" |

What is your exit plan? | Defined trigger or time horizon | No plan exists |

Does it fit your risk profile? | Confirmed through analysis | Not considered |

Have you checked the tax impact? | Yes, factored into expected return | Ignored |

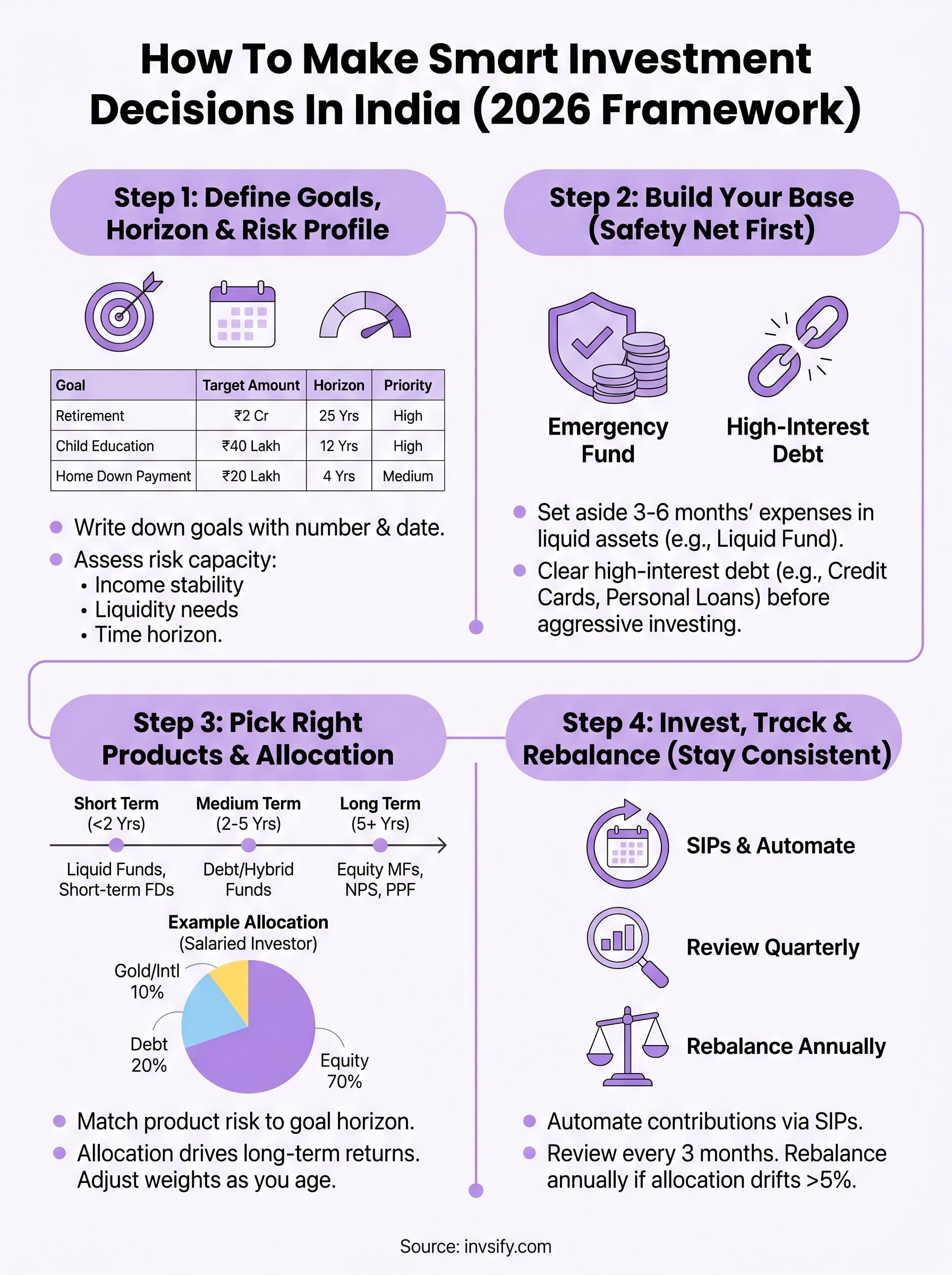

Step 1. Define goals, horizon, and risk profile

Before you look at a single product, knowing why you're investing is the most important step in how to make smart investment decisions. Without a goal and a timeline, every choice becomes arbitrary. You end up picking products based on advice or trends rather than what your situation actually demands.

Write down your goals with a number and a date

Vague goals produce vague portfolios. Instead of "save for retirement," write: "accumulate ₹2 crore by age 55." Instead of "child's education," write: "₹40 lakh needed in 12 years." Attaching a number and a deadline turns an aspiration into a planning input you can act on.

Use this simple template to structure your goals:

Goal | Target amount | Time horizon | Priority |

|---|---|---|---|

Retirement corpus | ₹2,00,00,000 | 25 years | High |

Child's education | ₹40,00,000 | 12 years | High |

Home down payment | ₹20,00,000 | 4 years | Medium |

International trip | ₹3,00,000 | 2 years | Low |

Assess your risk capacity honestly

Your risk profile is not just about how much volatility you can stomach emotionally; it also depends on your income stability, existing liabilities, and how soon you need the money. A 28-year-old salaried professional with no dependents can absorb more short-term market swings than a 45-year-old with a home loan and two children in school.

Your time horizon is the single biggest driver of how much risk your portfolio should carry.

Rate your risk capacity on three factors: income stability, liquidity needs, and investment horizon. This combination determines whether you lean toward equity-heavy, balanced, or debt-heavy allocations.

Step 2. Build your base: emergency fund and debt

Before you learn how to make smart investment decisions, you need a financial base that keeps you from being forced to liquidate investments at the wrong time. Investing without an emergency fund is like building a house on sand: one job loss or medical bill and you're selling equity at a market low just to cover expenses. This step is non-negotiable, regardless of your income level.

Set aside 3 to 6 months of expenses

Your emergency fund should cover 3 to 6 months of essential expenses, including rent, EMIs, groceries, and utilities. Keep this money in a liquid instrument, such as a high-yield savings account or a liquid mutual fund, not in equity or locked-in fixed deposits.

Use this checklist to build your emergency buffer:

Calculate your monthly essential expenses (rent + EMIs + food + utilities)

Multiply by 4 if you have a stable salaried job, or by 6 if your income varies

Park the amount in a liquid fund or sweep-in FD with same-day redemption

Review the amount annually as your expenses grow

Clear high-interest debt before investing aggressively

High-cost debt, particularly personal loans and credit card balances charging 18 to 36% per year, destroys wealth faster than any investment can build it. No equity mutual fund will reliably deliver 24% annually, so paying down expensive debt first gives you a guaranteed, risk-free return equal to the interest rate you're eliminating.

Clearing a 24% credit card balance is the highest-return, zero-risk investment available to you today.

Once high-interest debt is gone, redirect those EMI amounts into your investment portfolio systematically.

Step 3. Pick the right products and allocation

Once your base is solid, choosing where to put your money is the next critical piece of how to make smart investment decisions. The Indian market offers dozens of products, but most salaried investors only need a handful. The key is matching each product to a specific goal rather than diversifying for the sake of it.

Match products to goals and horizons

Different time horizons demand different instruments. Short-term goals need capital protection; long-term goals can absorb equity volatility and benefit from compounding. Picking equity for a 2-year goal or a liquid fund for a 20-year retirement plan both destroy value in different ways.

Time horizon | Suitable products | Risk level |

|---|---|---|

Under 2 years | Liquid funds, short-term FDs | Low |

2 to 5 years | Debt mutual funds, hybrid funds | Low-medium |

5+ years | Equity mutual funds (index/flexi-cap), NPS, PPF | Medium-high |

Build an allocation that reflects your risk profile

Your asset allocation is the single biggest determinant of long-term returns, not individual stock picks. A common starting point for a salaried investor in their 30s is 70% equity, 20% debt, and 10% gold or international funds. Adjust those weights based on your goals table from Step 1, giving each goal its own dedicated bucket.

Reduce your equity percentage by roughly 1% for each year closer you get to a major financial goal.

Treat each goal as a separate mini-portfolio with its own allocation, rather than managing one undifferentiated pile of money. This approach keeps your short-term needs protected while allowing your long-horizon investments to grow without unnecessary interference.

Step 4. Invest, track, and rebalance without panic

Knowing how to make smart investment decisions does not stop at picking the right products. Execution matters just as much as strategy. Systematic, automated investing removes emotion from the equation and keeps your portfolio compounding even when markets feel unstable or news headlines push you toward action.

Start with SIPs and automate your contributions

Systematic Investment Plans (SIPs) are the most reliable way to build wealth as a salaried investor in India. They enforce discipline by debiting a fixed amount on a set date each month, so you invest regardless of whether markets are up or down. Set up SIPs aligned to each goal bucket from your allocation plan, and treat each SIP like a fixed monthly bill rather than a discretionary expense you can skip.

Use this quick setup template to get started:

Goal | SIP amount | Fund type | SIP date |

|---|---|---|---|

Retirement | ₹10,000 | Flexi-cap equity fund | 5th of month |

Child's education | ₹5,000 | Index fund | 7th of month |

Home down payment | ₹3,000 | Hybrid fund | 10th of month |

Review quarterly and rebalance once a year

Checking your portfolio too often leads to reactive decisions, which is one of the fastest ways to underperform a simple index fund. Review your allocation every three months to identify drift, and do a full rebalance once a year by trimming overweight assets and topping up underweight ones.

If any asset class has moved more than 5% from your target allocation, treat that as your trigger to rebalance, not a market prediction.

Next steps

You now have a complete picture of how to make smart investment decisions in India in 2026. The framework is straightforward: define your goals, secure your base, match products to timelines, and stay consistent without letting short-term noise push you into bad decisions. The steps work together, so skipping any one of them leaves gaps that compound into real financial damage over time.

Putting this into practice does not require you to figure everything out alone. Invsify gives you AI-powered, SEBI Registered financial advice that is conflict-free, transparent, and built around your actual goals rather than a distributor's commission. You get a personalized Wealth Wellness Score, real-time portfolio tracking, and 24/7 access to a conversational AI that answers your financial questions whenever you need it.

Start applying what you learned today and get your personalized investment plan on Invsify to move from planning to action.