How To Plan Early Retirement In India: Corpus & SIP Math

Shlok Sobti

How To Plan Early Retirement In India: Corpus & SIP Math

Most people assume retirement is something you deal with in your 50s. But if you're a salaried professional in India earning well today, there's a real question worth asking: what if you didn't have to work until 60? Figuring out how to plan early retirement in India isn't just a fantasy exercise, it's a math problem. And once you run the numbers on corpus requirements, SIP contributions, and inflation-adjusted expenses, the path becomes surprisingly concrete.

The challenge, though, is that early retirement in India comes with unique variables. You're dealing with rising healthcare costs, no universal social security safety net, and an inflation rate that quietly eats into your purchasing power every single year. Retiring at 45 instead of 60 means your money needs to last 15+ extra years, and that changes everything about how much you need to save and where you invest.

This guide breaks down the actual math behind early retirement, the corpus you'll need, the SIP amounts to get there, and the investment strategy that ties it all together. No vague motivational advice, just numbers and actionable steps. At Invsify, we build AI-powered advisory tools specifically for Indian investors who want clarity on decisions like these, from personalized portfolio recommendations to conflict-free, SEBI-registered investment advice that helps you plan with confidence, not guesswork.

Let's get into the specifics.

What early retirement means in India

Early retirement in India doesn't mean sitting idle at 45 with nothing to do. It means financial independence, the point where your investment income covers your lifestyle without needing a salary. This concept is often called FIRE (Financial Independence, Retire Early), and while it originated in Western personal finance circles, it translates directly to the Indian financial reality with a few important local modifications you need to understand before running any numbers.

What FIRE actually means for Indian professionals

The FIRE framework splits into variations that matter based on your lifestyle expectations. Lean FIRE means retiring with a smaller corpus and living frugally, cutting expenses significantly. Fat FIRE is the version most Indian salaried professionals in metro cities actually aim for - retiring with enough that you don't have to cut back on travel, healthcare, or your children's education. Your cost structure is already built around a certain standard of living that doesn't easily compress, which makes Fat FIRE the relevant target for most people reading this.

The version of FIRE you're targeting determines everything, from the corpus size to the monthly SIP amounts you need to commit to today.

When you think about how to plan early retirement in India, the FIRE goal isn't to stop being productive. Many early retirees continue consulting, running passion projects, or building side income streams. The core difference is that work becomes optional rather than financially necessary. That shift changes how you negotiate, take career risks, and make lifestyle decisions.

Common retirement age targets in India

Most people who seriously pursue early retirement in India set one of three target ages: 40, 45, or 50. Each carries a different corpus requirement and savings timeline because your expected retirement duration changes dramatically between them. Retiring at 40 with Indian life expectancy pushing toward 75-80 means your money must last 35-40 years. At 50, it's 25-30 years. That 10-year difference in start age can mean a 30-40% gap in the total corpus you need to build from day one.

Target Retirement Age | Expected Retirement Duration | Corpus Requirement |

|---|---|---|

40 | 35-40 years | Highest |

45 | 30-35 years | High |

50 | 25-30 years | Moderate |

The India-specific variables you can't ignore

India has no universal social security or government pension for private-sector employees beyond EPF and NPS contributions. Once you stop working, there's no monthly state payment arriving in your account. Your entire retirement income depends on the corpus you build, which is fundamentally different from retirement planning in countries where government pensions provide a meaningful income floor. That single fact raises the stakes considerably for Indian early retirees.

Healthcare inflation in India runs at roughly 14% annually, which is nearly double general CPI inflation. If you retire at 45, you're facing 30+ years of compounding healthcare costs without employer group insurance coverage. Tax treatment also shifts post-retirement because your income mix changes from salary to dividends, capital gains, and interest income, each taxed differently under Indian income tax rules. These realities mean early retirement in India requires a more layered and precisely calibrated plan than simply saving aggressively and hoping for the best.

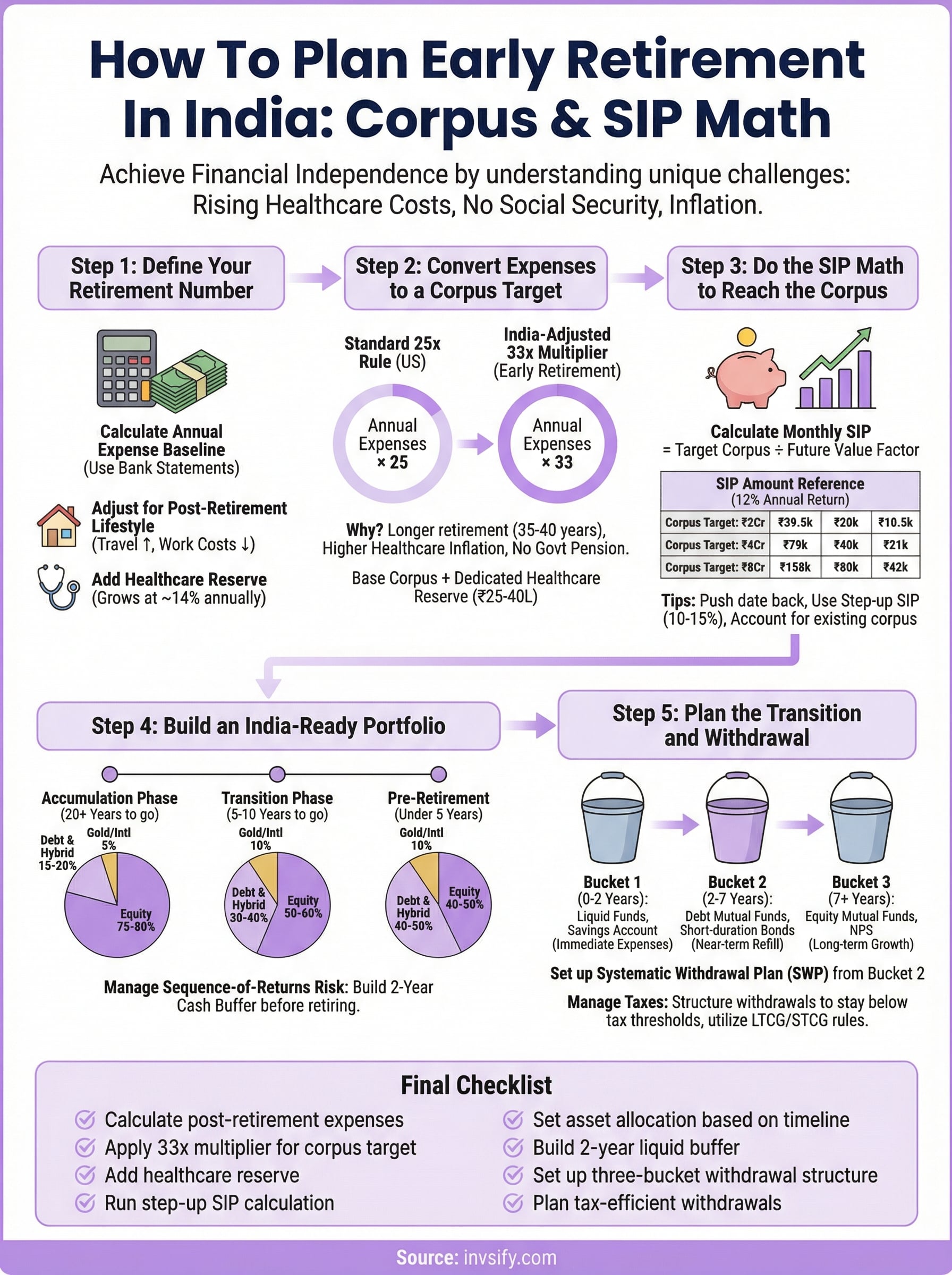

Step 1. Define your retirement number

Your retirement number is the total corpus you need on the day you stop working, large enough that returns from it cover your annual expenses indefinitely. Everything else in early retirement planning flows from this single figure, which is why getting it right matters more than any other step. Most people skip this calculation and start investing vaguely, which is exactly how you end up either over-saving for decades or running short of money at 60.

Calculate your annual expense baseline

Start with your current monthly household expenses and track every category for at least three months. Don't estimate from memory; use your bank statements. Add up rent or EMI, groceries, utilities, transport, insurance premiums, school fees, dining, travel, and discretionary spending. Multiply the monthly total by 12 to get your annual expense baseline.

Here's a simple template to build that baseline:

Expense Category | Monthly (₹) | Annual (₹) |

|---|---|---|

Housing (rent/EMI) | ||

Groceries & household | ||

Utilities & subscriptions | ||

Transport | ||

Education (children) | ||

Healthcare & insurance | ||

Travel & leisure | ||

Clothing & personal | ||

Miscellaneous | ||

Total |

Fill this out honestly. The number that comes out is your starting point for understanding how to plan early retirement in India accurately.

Adjust for post-retirement lifestyle

Retirement expenses don't mirror working-life expenses exactly. Some costs drop, some rise significantly, and a few new ones appear. Work-related expenses like commuting, professional clothing, and office lunches disappear. Your children's education costs may already be settled by the time you retire at 45 or 50. But travel spending typically increases in early retirement because you now have the time to actually use it.

The biggest expense adjustment most Indian early retirees underestimate is healthcare. Build in a separate healthcare budget that grows at 14% annually, not at general CPI inflation.

Factor in a healthcare reserve that starts at roughly ₹1.5-2 lakh annually at age 45 and grows from there. Once you account for all adjustments, you'll arrive at your post-retirement annual expense figure, which is the number that drives your corpus calculation in Step 2. For most salaried professionals in metro cities, post-retirement annual expenses typically land between ₹8 lakh and ₹24 lakh depending on lifestyle, family size, and city tier.

Step 2. Convert expenses to a corpus target

Once you have your post-retirement annual expense figure from Step 1, the next task is to translate that number into a total corpus target using a sustainable withdrawal rate. This is the bridge between knowing what you spend and knowing what you need saved, and it's the most critical calculation in figuring out how to plan early retirement in India.

The 25x Rule and Why India Needs an Adjustment

The most widely referenced framework for corpus calculation is the 4% Safe Withdrawal Rate (SWR), derived from the Trinity Study conducted by US academics. The logic is that if you withdraw no more than 4% of your corpus annually, your portfolio historically survives a 30-year retirement without being exhausted. Flip that around and you get the 25x rule: multiply your annual expenses by 25 to arrive at your target corpus.

The 4% rule was built on US market data with a 30-year retirement window. Retiring at 40 or 45 in India stretches that window to 35-40 years, and that single factor alone is reason enough to use a more conservative multiplier.

For Indian early retirees, a 3% to 3.5% withdrawal rate is more appropriate. Your retirement is longer, healthcare inflation compounds at roughly 14% annually, and there's no government pension backing you up if your portfolio underperforms. A 3% withdrawal rate translates to a 33x multiplier instead of 25x. If you plan to retire before 50, build your plan around 33x as the baseline.

Apply the Formula to Your Numbers

Run your annual expense figure through both multipliers to see your corpus range clearly. The table below maps common expense levels to corpus targets using both the standard 25x and the India-adjusted 33x:

Annual Expenses (₹) | Corpus at 25x (₹) | Corpus at 33x (₹) |

|---|---|---|

8,00,000 | 2,00,00,000 | 2,64,00,000 |

12,00,000 | 3,00,00,000 | 3,96,00,000 |

18,00,000 | 4,50,00,000 | 5,94,00,000 |

24,00,000 | 6,00,00,000 | 7,92,00,000 |

Use the 33x column as your primary working target if you're retiring before 50. If your target retirement age is 50 or later, 25x to 30x is a workable range depending on whether you expect any part-time income during retirement.

Beyond this base corpus, add a dedicated healthcare reserve of ₹25-40 lakh on top, kept in liquid or short-duration instruments. This buffer absorbs large medical expenses without forcing you to draw down your core investment corpus at the wrong time.

Step 3. Do the SIP math to reach the corpus

You now have a corpus target from Step 2. The next question is how to turn that number into a monthly SIP commitment you start today. This is where understanding how to plan early retirement in India gets concrete: you're working backwards from a future value to a present action. The math uses the future value of a SIP formula, and once you run it, you'll know exactly how much to invest each month at a given expected return.

The Formula Behind the Numbers

The calculation that drives everything here is:

Monthly SIP = Corpus Target ÷ {[(1 + r)^n - 1] ÷ r × (1 + r)}

Where r is the monthly return (annual return divided by 12) and n is the total number of months until your target retirement date. You don't need to run this manually; any SIP calculator handles it. But understanding the inputs helps you see how time and return rate interact. An extra 5 years of investing reduces your required monthly SIP by roughly 40-50%, which is why starting early is the single most powerful lever you have.

Increasing your return assumption from 10% to 12% sounds small, but across a 20-year horizon it can reduce your required monthly SIP by nearly 25%.

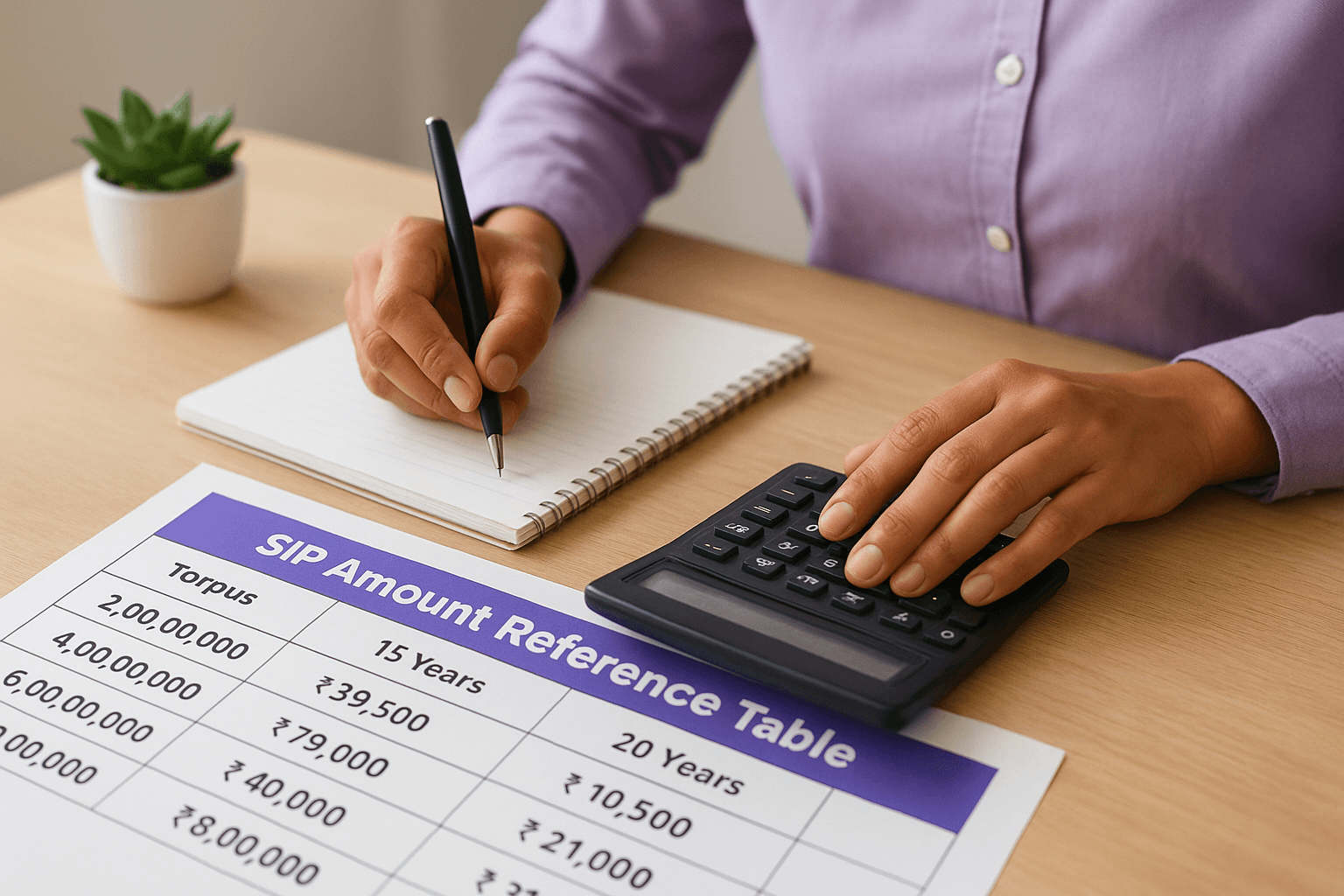

SIP Amount Reference Table

The table below shows approximate monthly SIP requirements to reach common corpus targets at 12% annualized returns, which is a reasonable long-term assumption for a diversified equity-heavy Indian mutual fund portfolio:

Corpus Target (₹) | 15 Years | 20 Years | 25 Years |

|---|---|---|---|

2,00,00,000 | ₹39,500 | ₹20,000 | ₹10,500 |

4,00,00,000 | ₹79,000 | ₹40,000 | ₹21,000 |

6,00,00,000 | ₹1,18,500 | ₹60,000 | ₹31,500 |

8,00,00,000 | ₹1,58,000 | ₹80,000 | ₹42,000 |

What to Do If the Numbers Feel Too Large

If your required monthly SIP looks unmanageable against your current salary, you have three practical levers. First, push your retirement date out by 3-5 years to dramatically reduce the monthly commitment. Second, build in annual SIP step-ups of 10-15% as your salary grows, rather than keeping the SIP flat from year one. Third, account for any existing corpus such as EPF balance, existing mutual funds, or PPF as a head start that reduces the amount your fresh SIPs need to generate.

Run a step-up SIP calculation that increases your contribution by 10% each year. That approach typically reduces your starting SIP requirement by 35-40% compared to a flat SIP, making the numbers feel far more reachable from where you are today.

Step 4. Build an India-ready portfolio

Your corpus target and SIP math are only as good as the portfolio delivering them. An India-ready early retirement portfolio needs to do two things simultaneously: grow aggressively during your accumulation phase and then shift to a reliable income-generating structure the moment you stop working. Getting this balance right is central to understanding how to plan early retirement in India with any real confidence.

The Core Allocation Framework

During the accumulation phase, your portfolio should skew heavily toward equity, since time compounds returns in your favor. Indian diversified equity mutual funds covering large-cap, flexi-cap, and mid-cap categories form the growth engine of the portfolio. Alongside equity, debt instruments like PPF, NPS Tier I, and short-duration bond funds provide stability and cushion volatility as you approach your retirement date. Use this allocation framework based on years remaining:

Years to Retirement | Equity (%) | Debt & Hybrid (%) | Gold/International (%) |

|---|---|---|---|

20+ years | 75-80 | 15-20 | 5 |

10-20 years | 65-70 | 20-25 | 5-10 |

5-10 years | 50-60 | 30-40 | 10 |

Under 5 years | 40-50 | 40-50 | 10 |

Shift your allocation toward debt and hybrid funds in the final 5 years before your target date. This step reduces the risk of a large market correction wiping out your corpus right before you need it most, and it locks in a more predictable income base from day one of retirement.

Managing Sequence-of-Returns Risk

Sequence-of-returns risk is the danger that a major market downturn in the first few years after retirement forces you to sell investments at a loss, leaving your corpus too depleted to recover even when markets rebound. This risk hits early retirees particularly hard because your retirement period stretches 30-40 years, giving an early shock far more time to compound negatively.

Building a 2-year cash or liquid fund buffer before you retire protects your corpus from forced withdrawals during a market downturn.

Keep 12-24 months of living expenses in a liquid mutual fund or high-yield savings account so you never sell equity during a crash. Allocating 10% of your total corpus to international equity funds also adds geographic diversification, since Indian and global markets don't always fall simultaneously. These two structural decisions, a cash buffer combined with international exposure, give your portfolio meaningful resilience without overcomplicating the overall structure.

Step 5. Plan the transition and withdrawal

The hardest part of figuring out how to plan early retirement in India isn't building the corpus. It's setting up the withdrawal structure that pays your bills without destroying the corpus in the process. Most people spend years building their portfolio and almost no time thinking about how they'll take money out of it. That planning gap is what causes early retirees to either over-withdraw in the first few years or hold so much in cash that their corpus stops growing.

Build Your Income Ladder Before You Quit

You need an income ladder in place at least 12 months before your last working day. An income ladder separates your corpus into three buckets based on when you'll need the money. This structure prevents you from being forced to sell equity during a downturn to pay monthly expenses.

Bucket | Timeframe | What to Hold | Purpose |

|---|---|---|---|

Bucket 1 | 0-2 years | Liquid funds, savings account | Immediate expenses |

Bucket 2 | 2-7 years | Debt mutual funds, short-duration bonds | Near-term refill |

Bucket 3 | 7+ years | Equity mutual funds, NPS | Long-term growth |

Refill Bucket 1 from Bucket 2 annually, and refill Bucket 2 from Bucket 3 every 3-4 years, letting equity run long enough to smooth out market cycles.

Set up a Systematic Withdrawal Plan (SWP) from a debt or balanced advantage fund into your savings account each month. A monthly SWP of ₹60,000 to ₹80,000 from a ₹2 crore debt corpus delivers consistent, predictable income without requiring you to time markets or sell units manually.

Manage Taxes on Your Withdrawal Income

Your tax profile changes completely once you retire early. Salary income disappears and gets replaced by long-term capital gains (LTCG), short-term capital gains (STCG), and interest income, each taxed at different rates under the Indian Income Tax Act. LTCG from equity mutual funds above ₹1.25 lakh annually is taxed at 12.5%, while debt fund gains are taxed at your applicable slab rate. Planning which funds you withdraw from, and in what sequence, can reduce your annual tax outgo by a meaningful margin.

Structure your annual withdrawals to stay below key tax thresholds wherever possible. If your total income in retirement falls below ₹7 lakh, the rebate under Section 87A brings your liability to zero. Keep bond interest, dividend distributions, and capital gains timed across financial years to avoid unnecessary slab breaches and maintain a lower effective tax rate throughout your retirement.

Final checklist

Knowing how to plan early retirement in India comes down to executing each step in the right sequence. Use this checklist before you commit to a retirement date:

Calculate your post-retirement annual expenses using actual bank statement data

Apply the 33x multiplier to get your India-adjusted corpus target

Add a healthcare reserve of ₹25-40 lakh on top of your base corpus

Run a step-up SIP calculation to find your starting monthly contribution

Set your asset allocation based on years remaining to retirement

Build a 2-year liquid buffer before you retire

Set up a three-bucket withdrawal structure 12 months before your last day

Plan your annual withdrawals to stay below key tax thresholds

If any item on this list feels unclear or the numbers look overwhelming, getting personalized advice from a SEBI-registered advisor makes a real difference. Start your early retirement plan with Invsify and get AI-powered, conflict-free financial guidance built specifically for Indian investors like you.