Portfolio Rebalance: How To Rebalance A Portfolio In India

Shlok Sobti

Portfolio Rebalance: How To Rebalance A Portfolio In India

You started investing with a plan, maybe 60% equity, 30% debt, 10% gold. Six months later, equity markets rallied, and now your portfolio sits at 75% equity without you buying a single extra share. Your risk exposure has quietly drifted, and your original strategy no longer reflects how to rebalance a portfolio back to its intended allocation. This drift happens to almost every investor, and ignoring it can undo years of careful planning.

Rebalancing is the process of realigning your portfolio's asset mix to match your target allocation. It's not about chasing returns, it's about managing risk and staying disciplined when markets move. Whether you rebalance quarterly, annually, or based on threshold triggers, the approach you pick matters. This guide breaks down exactly when and how to rebalance, step by step, with a focus on what works for Indian investors dealing with tax implications, exit loads, and multiple asset classes.

At Invsify, our AI-powered advisory tracks your portfolio in real time and flags when your allocation drifts beyond acceptable limits. Instead of manually crunching numbers across mutual funds, stocks, and fixed deposits, you get clear, conflict-free recommendations on what to adjust, backed by data, not commissions. Let's walk through everything you need to know to keep your portfolio aligned with your goals.

What portfolio rebalancing means in India

Portfolio rebalancing is the act of selling and buying assets to bring your portfolio back to the allocation percentages you originally set as your target. In India, this applies across a wide range of instruments, including equity mutual funds, direct stocks, gold ETFs, Public Provident Fund (PPF), and the National Pension System (NPS). When one asset class grows faster than others, it takes up a larger slice of your portfolio than you planned, which increases your overall risk level even if you haven't made a single new decision.

Rebalancing is not a performance strategy. It's a risk management tool that keeps your portfolio aligned with your goals and your actual tolerance for loss.

Why Indian portfolios drift faster

Indian equity markets have historically shown higher short-term volatility compared to developed markets, which means your allocation can shift significantly within a single quarter. For example, if Nifty 50 rises 18% in a year while your debt funds return 7%, a starting allocation of 60% equity and 40% debt could shift to nearly 67% equity and 33% debt without you making a single trade. This drift quietly increases the downside risk you carry, especially heading into periods of market correction.

Beyond market movements, India-specific products add complexity. ELSS lock-in periods of three years, NPS exit restrictions, and exit loads on liquid or short-duration funds mean you cannot always rebalance freely. Knowing which assets you can touch, and when, is a core part of understanding how to rebalance a portfolio within the Indian financial system.

How rebalancing differs from active trading

Rebalancing is not the same as actively picking winners. Active trading means making frequent decisions based on short-term price forecasts or market news. Rebalancing means restoring pre-set ratios regardless of which asset looks attractive right now. The goal is mechanical discipline, not prediction.

When you sell an outperforming equity fund and move the proceeds into an underperforming debt fund to restore your original targets, you are doing the opposite of what feels instinctive. That discomfort is precisely what makes rebalancing valuable as a long-term strategy. It enforces buy-low-sell-high behavior systematically, without requiring you to time the market.

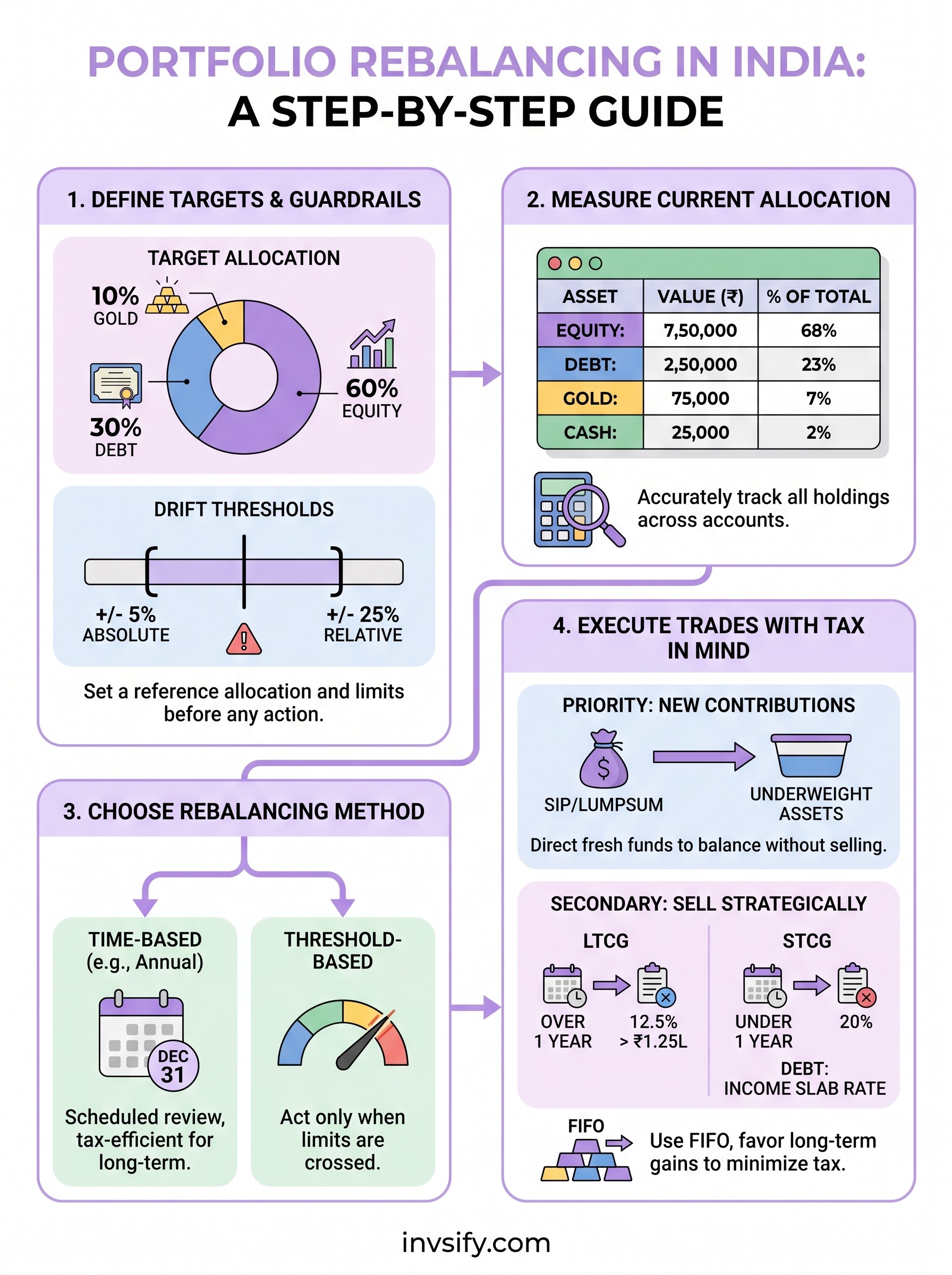

Before you rebalance: set targets and guardrails

Before you touch a single trade, you need two things locked in: a written target allocation and a set of drift thresholds that tell you when rebalancing is actually necessary. Without these, you end up either rebalancing too often (triggering unnecessary taxes and costs) or not often enough (letting risk accumulate silently). Setting these upfront removes emotion from the decision entirely.

Define your target allocation

Your target allocation should reflect your investment horizon, risk tolerance, and financial goals, not what performed best last year. A common starting point for a salaried Indian investor in their 30s might look like this:

Asset Class | Target Allocation |

|---|---|

Equity mutual funds / direct stocks | 60% |

Debt mutual funds / FDs | 25% |

Gold ETFs / Sovereign Gold Bonds | 10% |

Cash / Liquid funds | 5% |

Write this down and treat it as a reference document. Every rebalancing decision you make should be measured against this table, not against market sentiment or recent news.

Set your drift thresholds

A drift threshold defines how far an asset class can move from its target before you act. A widely used rule is the 5/25 rule: rebalance if an asset class drifts by more than 5 percentage points in absolute terms, or more than 25% of its original allocation in relative terms, whichever comes first.

Setting a threshold prevents you from rebalancing on every minor market fluctuation, which keeps transaction costs and tax liabilities manageable.

For example, if equity is targeted at 60%, you would only rebalance if it crosses 65% (absolute) or 75% (relative). Apply this rule consistently across all asset classes in your portfolio.

Step 1. Measure your current allocation

You cannot know where your portfolio actually stands until you have a complete, accurate snapshot of every holding you own. Pull the current market value of each position, group them by asset class, and calculate the percentage each group represents of your total portfolio. This single step is what makes the rest of how to rebalance a portfolio actionable rather than guesswork.

Pull the current value of every holding

Start by logging into each platform you use, such as your mutual fund registrar (CAMS or KFintech), your demat account, and your bank, and record the current market value of each position. For illiquid assets like PPF or Sovereign Gold Bonds, use the current accrued balance. List every holding in a single spreadsheet before you do any math.

Accuracy matters here. Missing even one account will distort your allocation percentages and lead you to make the wrong trades.

Calculate each asset class as a percentage

Add up the values within each asset class, then divide by your total portfolio value and multiply by 100. Use this template as your starting point:

Asset Class | Current Value (₹) | % of Total |

|---|---|---|

Equity | 7,50,000 | 68% |

Debt | 2,50,000 | 23% |

Gold | 75,000 | 7% |

Cash / Liquid | 25,000 | 2% |

Total | 11,00,000 | 100% |

Compare the "% of Total" column directly against your target allocation table from the previous section. Any asset class sitting outside your drift threshold is a candidate for rebalancing in the next step.

Step 2. Choose a rebalancing method

Once you know where your current allocation stands, you need to pick how often and under what conditions you will rebalance. Two methods work well for most Indian investors: time-based rebalancing and threshold-based rebalancing. The right choice depends on how actively you want to monitor your portfolio and how sensitive your holdings are to short-term tax implications.

Time-based rebalancing

Time-based rebalancing means you review and adjust your portfolio on a fixed schedule, typically quarterly or annually, regardless of how much the allocation has drifted. Annual rebalancing is the most tax-efficient option for most Indian investors because it reduces the number of redemptions that trigger short-term capital gains tax (STCG), especially in equity funds where STCG applies to holdings under one year.

Annual rebalancing strikes the right balance between keeping risk in check and minimizing unnecessary tax events for long-term investors.

Threshold-based rebalancing

Threshold-based rebalancing is more precise. You act only when your portfolio drifts past the guardrails you set in the previous step, such as the 5/25 rule. This method suits investors who want to know how to rebalance a portfolio in response to actual market conditions rather than a fixed calendar date. Use the table below to match your situation to the right approach:

Your Situation | Recommended Method |

|---|---|

Prefer simplicity and low effort | Time-based (annual) |

Active investor with volatile equity exposure | Threshold-based |

Large portfolio with significant tax exposure | Time-based (annual) |

Portfolio with equity allocation above 65% | Threshold-based |

Step 3. Execute trades with taxes in mind

Once you know your drift and have chosen your method, you need to execute the actual trades in a sequence that minimizes your tax bill. In India, the order in which you sell matters because equity mutual funds held under one year attract STCG tax at 20%, while holdings beyond one year are taxed at 12.5% LTCG above ₹1.25 lakh per year. Selling strategically can save you a meaningful amount on every rebalancing cycle.

Direct new contributions to underweight assets first

Before you sell anything, check whether incoming SIP installments or fresh lump-sum investments can close the gap. If your debt allocation is 7 percentage points below target, redirect your next few SIPs entirely into debt funds. This approach lets you understand how to rebalance a portfolio without triggering a single redemption, which means zero tax liability on the rebalancing move itself.

Using fresh contributions to rebalance is always cheaper than selling existing units, especially within the first year of holding.

Sell strategically when redemptions are unavoidable

When you must sell, prioritize units that have crossed the one-year mark to qualify for LTCG treatment on equity funds. Use the FIFO (first in, first out) method that registrars like CAMS apply by default, and confirm the holding period before placing each redemption. For debt funds, all gains are taxed at your income slab rate regardless of holding period since April 2023, so factor your tax bracket into the decision.

Redemption Type | Tax Rate | Holding Period |

|---|---|---|

Equity STCG | 20% | Under 1 year |

Equity LTCG | 12.5% above ₹1.25L | Over 1 year |

Debt funds | Income slab rate | Any period |

Next steps

You now have a complete framework for how to rebalance a portfolio in India, from setting targets and drift thresholds to executing trades in the most tax-efficient sequence. The process works best when you treat it as a routine maintenance task rather than a reaction to market news. Pick your method, set a reminder, and follow the steps each time your portfolio drifts past its guardrails.

Doing this manually across multiple accounts, funds, and tax lots takes time and leaves room for error. Invsify tracks your portfolio in real time and alerts you the moment your allocation drifts past your thresholds, so you always know exactly what to adjust and when. Instead of juggling spreadsheets, you get clear, conflict-free recommendations backed by AI and SEBI-registered advisors who work for you, not for commissions.

Start managing your portfolio with Invsify and take the guesswork out of rebalancing for good.