ICICI Prudential Retirement Fund: NAV, Returns, Lock-In

Shlok Sobti

ICICI Prudential Retirement Fund: NAV, Returns, Lock-In

Planning for retirement requires choosing the right investment vehicle, and the ICICI Prudential Retirement Fund has emerged as a popular option among Indian investors. With multiple plan variants offering different risk-return profiles, this solution-oriented scheme deserves a closer look before you commit your hard-earned savings to it.

Whether you're comparing the Pure Equity Plan against the Hybrid Aggressive Plan or trying to understand the mandatory lock-in period, getting clarity on NAV movements and historical returns is essential. At Invsify, we help investors cut through the noise with AI-powered insights that make evaluating such funds straightforward and conflict-free.

This article breaks down everything you need to know, from current NAV figures and return performance across timeframes to the specific features that set this retirement fund apart. By the end, you'll have a clear picture of whether this fund aligns with your retirement goals.

Why the ICICI Prudential Retirement Fund matters

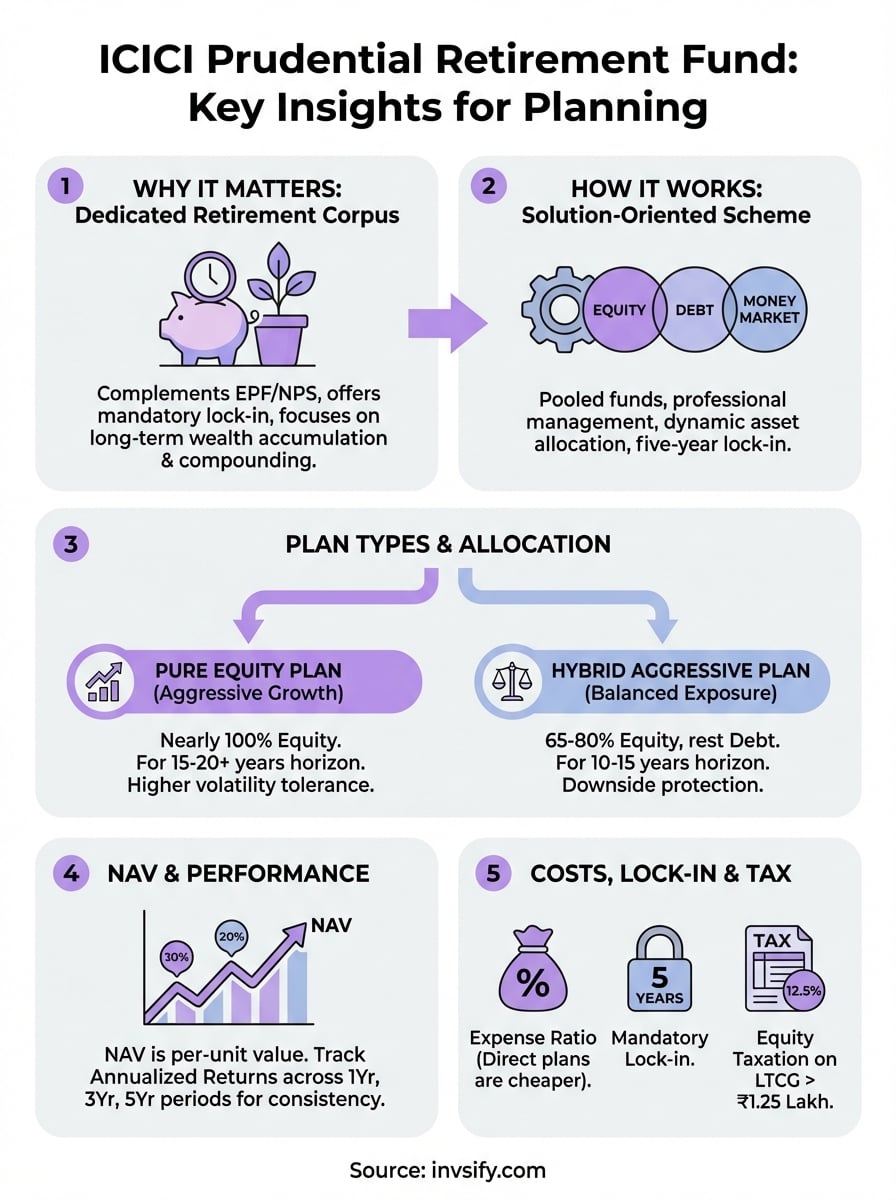

You need a dedicated retirement corpus because your EPF contributions and pension plans may not be enough to maintain your lifestyle after you stop working. The ICICI Prudential Retirement Fund addresses this gap by offering solution-oriented retirement schemes with mandatory lock-in periods that discourage early withdrawals and keep your long-term goals on track.

The retirement funding challenge most Indians face

Most salaried individuals underestimate how much they need for a comfortable retirement, often relying solely on employer-provided benefits like EPF or NPS. However, inflation erodes purchasing power over decades, and lifestyle expenses rarely decrease after retirement. This fund helps you build a separate retirement bucket that complements your existing savings, giving you multiple income sources when you eventually exit the workforce.

Building wealth for retirement requires discipline, and mandatory lock-in periods remove the temptation to withdraw funds prematurely.

What makes this fund a retirement-focused solution

Unlike regular mutual funds where you can redeem anytime, the icici prudential retirement fund imposes a five-year lock-in period, forcing you to stay invested through market cycles. This structure aligns with retirement planning principles that prioritize long-term wealth accumulation over short-term liquidity. The fund also offers multiple plan types, ranging from aggressive equity-heavy portfolios to balanced hybrid options, letting you choose a risk profile that matches your age and retirement timeline. By keeping your money invested longer, you benefit from compounding returns that can significantly boost your final corpus compared to schemes where frequent withdrawals disrupt growth.

How the fund works and what it invests in

The icici prudential retirement fund operates as a solution-oriented scheme where your money gets pooled with other investors' contributions and deployed across various asset classes based on the plan you select. Fund managers actively monitor market conditions and rebalance the portfolio to optimize returns while managing risk, ensuring your retirement corpus grows steadily over the mandatory five-year lock-in period.

The asset allocation strategy behind each plan

Your investments flow into a diversified mix of equity stocks, debt securities, and money market instruments depending on the specific plan variant you choose. The Pure Equity Plan channels almost all your money into equity and equity-related instruments, targeting maximum capital appreciation through direct stock holdings and equity derivatives. On the other hand, the Hybrid Aggressive Plan splits your capital between equity (65-80%) and debt instruments, offering a balanced approach that cushions market volatility while still delivering growth potential.

Professional fund management removes the burden of daily portfolio tracking, letting you focus on your career while your retirement savings work in the background.

Fund managers track market trends, economic indicators, and sector performance to make tactical shifts that protect your capital during downturns and capture gains during rallies.

Plan types and options you can choose

The icici prudential retirement fund offers two distinct plan variants that cater to different risk appetites and retirement timelines. You select one plan at the time of investment, and your choice determines the asset allocation strategy that shapes your portfolio's performance throughout the lock-in period.

Pure Equity Plan for aggressive growth

This plan allocates nearly all your capital into equity stocks and equity-related instruments, targeting maximum wealth accumulation over the long term. You should consider this option if you have at least 15-20 years until retirement and can tolerate short-term market volatility without panicking. The fund managers invest across large-cap, mid-cap, and small-cap segments, giving you exposure to companies at different growth stages while managing concentration risk through diversification.

Younger investors with longer time horizons can absorb equity market swings and benefit from the compounding effect of higher returns.

Hybrid Aggressive Plan for balanced exposure

This variant maintains 65-80% equity allocation while parking the remainder in debt securities and money market instruments, offering a smoother ride during market turbulence. You gain downside protection from the debt component without sacrificing too much growth potential, making it suitable if you're within 10-15 years of retirement or prefer moderate risk exposure.

NAV, returns, and how to read performance

You track your investment's progress by monitoring the Net Asset Value (NAV), which represents the per-unit market value of all assets held in the icici prudential retirement fund after deducting liabilities. This figure changes daily based on the underlying portfolio's performance, and you multiply it by the number of units you own to calculate your current investment value.

Understanding NAV movements

NAV fluctuates with market conditions, rising when the fund's equity holdings appreciate or debt instruments perform well, and falling during market corrections. You access the latest NAV through the fund house website, investment platforms, or financial news portals that publish daily updates. Checking NAV alone does not tell you much about performance quality, since a higher NAV simply means the fund has existed longer or delivered better returns historically, not that it costs more to invest.

Regular NAV monitoring helps you spot trends, but remember that short-term volatility is normal for equity-focused retirement funds.

Reading historical returns across timeframes

You evaluate performance by comparing annualized returns across one-year, three-year, and five-year periods, which reveal how consistently the fund delivered growth. Focus on longer timeframes that match your retirement horizon, since a single strong year might mask weaker periods.

Costs, lock-in, exit rules, and taxation

You pay an expense ratio that covers fund management, administrative costs, and distribution charges, which gets deducted from the fund's assets daily before NAV calculation. The icici prudential retirement fund charges different expense ratios for direct and regular plans, with direct plans typically costing 0.5-1% less annually since they skip distributor commissions.

What you pay in fees and expenses

Your returns get reduced by the annual expense ratio, which ranges from 0.75% to 2.25% depending on whether you invest through a distributor or directly with the fund house. Direct plan investors save significantly over decades since lower fees compound into higher corpus values, making it worth bypassing intermediaries if you can research and invest independently.

Lower expense ratios directly translate into better retirement corpus accumulation, especially over 20-30 year horizons.

Lock-in period and withdrawal restrictions

You cannot withdraw any amount before five years from the date of investment, except in rare cases like critical illness or death of the investor. This mandatory lock-in protects your retirement savings from impulsive decisions during market downturns, ensuring your capital stays invested through multiple market cycles.

Tax treatment on withdrawals

Your withdrawals get taxed based on equity taxation rules if you invested in the Pure Equity Plan, with long-term gains above Rs 1.25 lakh taxed at 12.5%. Hybrid plan redemptions follow similar treatment since equity allocation exceeds 65%, making tax planning essential before you start withdrawing funds post-retirement.

Key takeaways before you invest

The icici prudential retirement fund gives you a structured way to build a retirement corpus through mandatory five-year lock-in periods that prevent impulsive withdrawals during market volatility. You choose between the Pure Equity Plan for aggressive growth or the Hybrid Aggressive Plan for balanced exposure, depending on your risk appetite and years until retirement. NAV tracking helps you monitor performance, but focus on annualized returns across longer timeframes rather than daily fluctuations that create unnecessary panic.

Direct plans save you significant expense ratio costs compared to regular plans, and those savings compound into larger retirement corpus over decades. Tax treatment follows equity taxation rules with long-term gains above Rs 1.25 lakh taxed at 12.5%, making post-retirement withdrawal planning essential for tax efficiency. Your investment strategy should align with how many years you have before retirement, with younger investors benefiting more from equity-heavy allocations that maximize compounding potential.

Get AI-powered insights that help you evaluate this fund alongside other retirement planning options without hidden fees or conflicts of interest.