Index Fund Calculator India: Estimate SIP & Lumpsum Returns

Shlok Sobti

Index Fund Calculator India: Estimate SIP & Lumpsum Returns

You've picked index funds for their low costs and market-matching returns, smart move. Now you want to know exactly how much your money could grow over 5, 10, or 20 years. That's where an index fund calculator India becomes your best planning companion. It takes the guesswork out of projecting your SIP or lumpsum investment outcomes.

Whether you're investing ₹5,000 monthly or parking a ₹5 lakh lumpsum, knowing your potential corpus helps you set realistic financial goals. But calculators only show projections, they don't tell you which index fund suits your risk profile or how to optimize your portfolio for tax efficiency.

At Invsify, we combine AI-powered insights with SEBI-registered advisory expertise to help you go beyond calculations. This guide walks you through how index fund calculators work, the formulas behind them, and how to use these projections to make informed investment decisions.

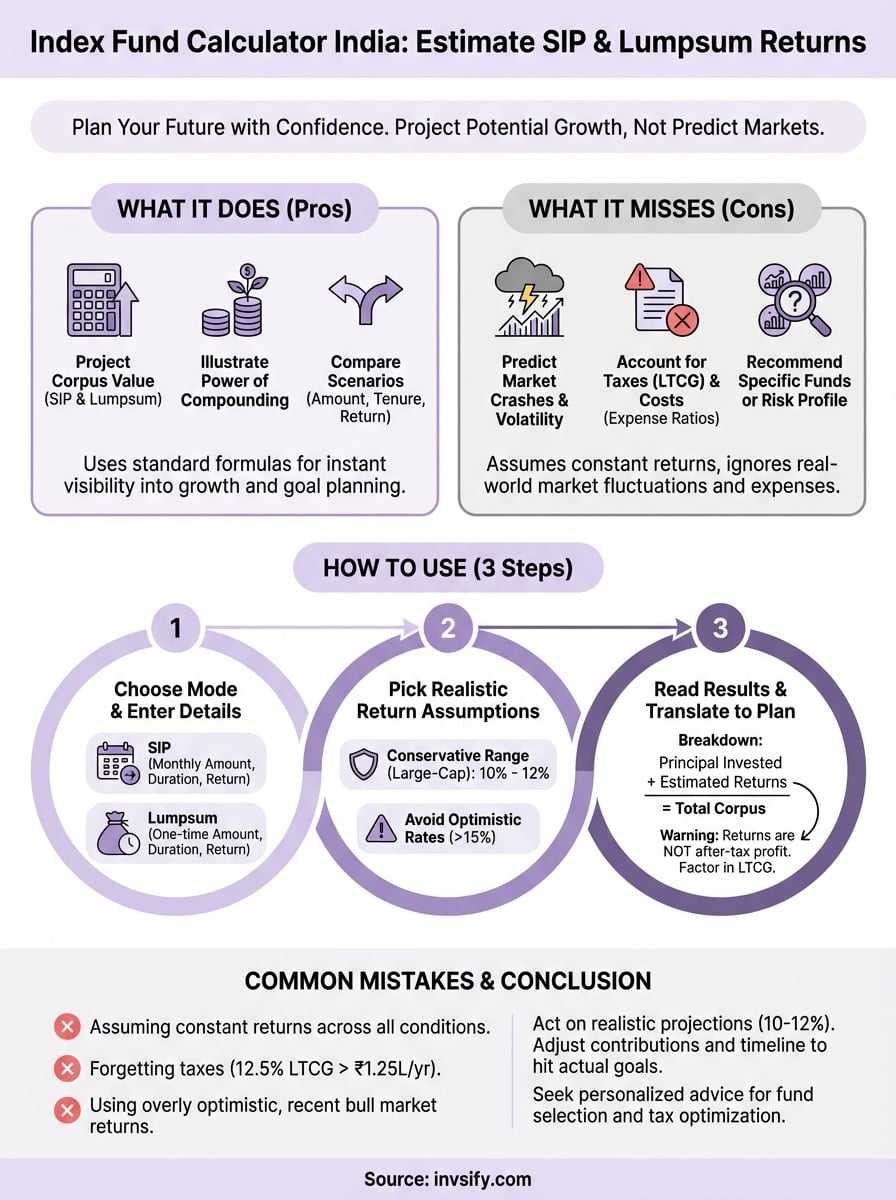

What an index fund calculator in India can and cannot do

An index fund calculator gives you a mathematical projection of how your investment could grow, nothing more, nothing less. You input your investment amount, duration, and expected returns, and it shows you a maturity value based on compound interest formulas. This clarity helps you set financial targets, but the tool can't predict market crashes, sector rotations, or how your actual fund will perform against its benchmark.

What calculators do well

Calculators excel at projecting corpus values for both SIP and lumpsum investments using standard formulas. They show you how ₹10,000 monthly at 12% annual returns becomes ₹23.23 lakh in 10 years, or how a ₹5 lakh lumpsum grows to ₹15.52 lakh in the same period. You get instant visibility into the power of compounding without opening a spreadsheet or learning finance formulas yourself.

These tools also let you compare different scenarios quickly. Change the investment amount, tenure, or return rate, and you see new projections in seconds. This flexibility helps you plan whether to increase your SIP or extend your investment horizon to hit specific goals like ₹1 crore for retirement or ₹50 lakh for a down payment.

Calculators show potential outcomes, but they cannot guarantee returns or replace personalized financial advice.

What calculators miss

No index fund calculator India tool accounts for expense ratios, exit loads, or tax implications like long-term capital gains at 12.5% above ₹1.25 lakh annually. The maturity value you see assumes a constant return rate, which never happens in real markets. You might face years of 25% returns followed by periods of negative 8%, and calculators ignore this volatility completely.

Calculators also don't tell you which index fund matches your risk profile or whether you should invest in Nifty 50, Nifty Next 50, or sectoral indices. They assume you've already made the right choice, which most first-time investors haven't.

Step 1. Enter SIP or lumpsum details the right way

Most index fund calculator India tools give you two input modes, SIP (Systematic Investment Plan) or lumpsum. Your choice depends on whether you're investing a fixed amount monthly or parking a one-time corpus. Enter the wrong mode, and your projections become useless. Start by deciding which investment method matches your cash flow, then follow the specific input requirements for that mode.

For SIP investments

Open any SIP calculator and you'll see three fields: monthly investment amount, investment duration, and expected annual return. Enter the exact monthly amount you plan to invest, like ₹5,000 or ₹15,000, not a rounded estimate. For duration, use the actual number of years you intend to stay invested, 10 years for a child's education fund or 20 years for retirement. Most calculators convert years to months automatically, so you'll see 120 months or 240 months displayed.

SIP calculators assume you invest on the same date each month without skipping payments or changing amounts mid-way.

Your investment tenure determines compounding cycles, so adding even one extra year significantly boosts your final corpus. A ₹10,000 monthly SIP at 12% returns gives you ₹23.23 lakh in 10 years but ₹69.97 lakh in 15 years.

For lumpsum investments

Lumpsum calculators require only your one-time investment amount, time horizon, and expected return rate. Enter the exact corpus you're investing today, whether it's ₹1 lakh, ₹5 lakh, or ₹50 lakh. The duration field works identically to SIP calculators, input the number of years you'll leave this money untouched before withdrawal.

Step 2. Pick realistic return assumptions for Indian index funds

The return rate you enter in any index fund calculator India tool directly shapes your projected corpus, so using wishful thinking here ruins your entire plan. Most investors plug in 15% or 18% because they've heard success stories, but historical averages don't guarantee future performance. You need to base your assumptions on actual index returns over the last 10 to 15 years, adjusted for realistic market conditions.

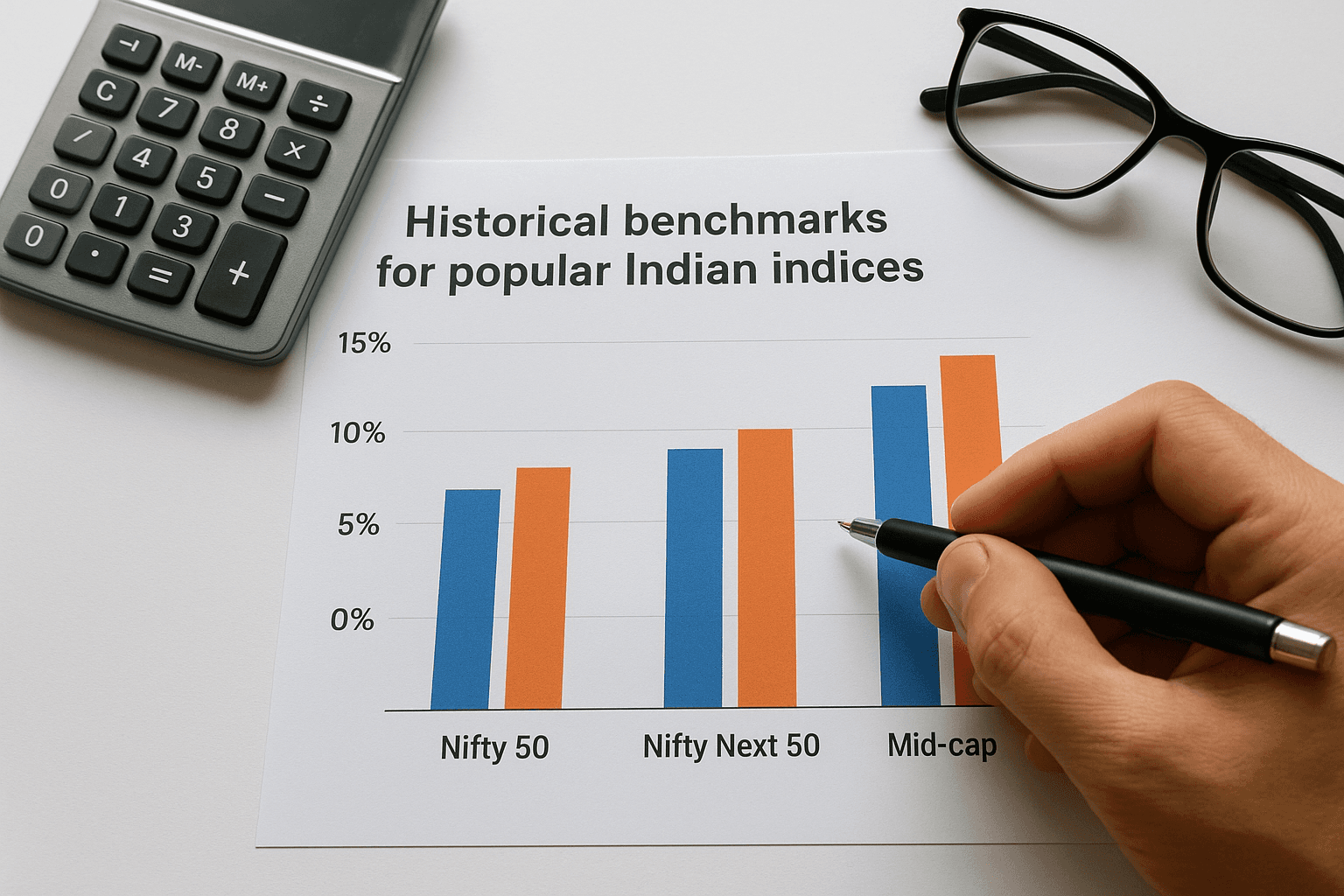

Historical benchmarks for popular Indian indices

Nifty 50 has delivered approximately 12% to 13% annual returns over the past 15 years, including periods of market crashes and bull runs. If you're investing in a Nifty 50 index fund, using 12% as your expected return gives you a conservative baseline. For Nifty Next 50 or mid-cap indices, historical returns hover between 13% to 15%, but these come with higher volatility that calculators don't show.

Never assume returns above 15% for broad market indices, even during bull markets, because one bad decade can erase years of gains.

Conservative ranges to enter in calculators

Enter 10% to 12% for large-cap index funds like Nifty 50 or Sensex trackers. Use 11% to 13% for mid-cap indices and 9% to 11% if you're mixing debt funds with your index portfolio. Lower assumptions protect you from disappointment and help you plan for realistic financial goals instead of chasing inflated projections.

Step 3. Read the results and translate them into a plan

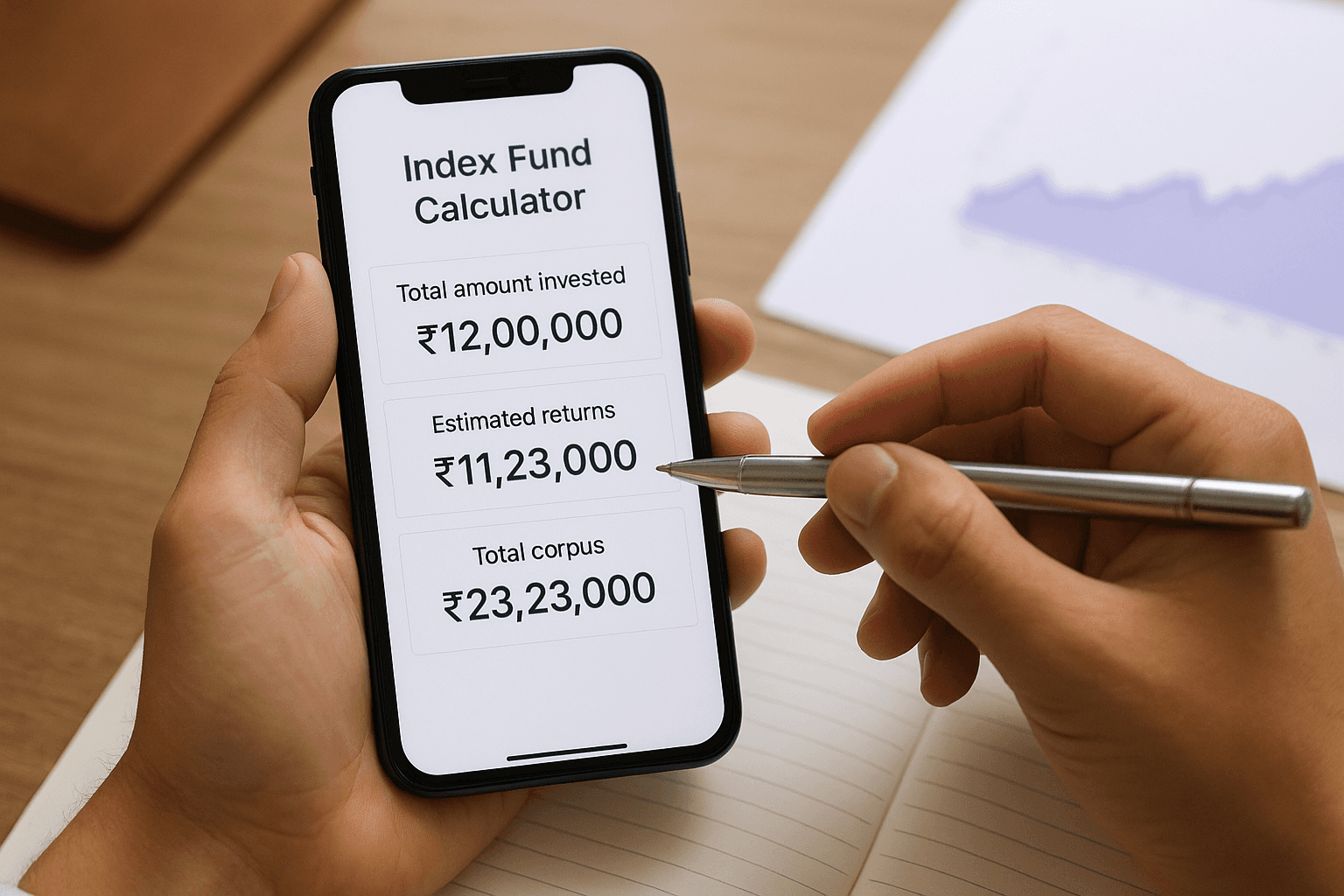

Once your index fund calculator India tool displays the maturity value, don't just screenshot it and move on. You need to extract actionable insights from those numbers and map them against your actual financial goals. The calculator shows you two key figures: the total amount invested and the estimated maturity value, the difference between these is your projected wealth gain through compounding.

Breaking down the calculator output

Most calculators display your results in three parts: principal invested, estimated returns, and total corpus. For a ₹10,000 monthly SIP at 12% over 10 years, you'll see ₹12 lakh as principal, ₹11.23 lakh as returns, and ₹23.23 lakh as total value. That ₹11.23 lakh gain represents your compounding benefit, not guaranteed profit, and you need to subtract taxes on withdrawal to get your actual take-home amount.

Your maturity value before taxes isn't your actual wealth, factor in 12.5% LTCG on gains above ₹1.25 lakh annually.

Mapping results to specific goals

Take your projected corpus and match it against your actual financial target. If you need ₹30 lakh for a house down payment in 10 years but your calculator shows only ₹23.23 lakh, increase your monthly SIP to ₹13,000 or extend your timeline to 12 years to bridge that gap.

Quick examples and common mistakes to avoid

You've learned how index fund calculator India tools work, now you need real-world scenarios to test your understanding. Running a few practice calculations helps you spot errors before they mess up your actual financial planning. Most investors make the same three mistakes when using these calculators, and fixing them takes 30 seconds once you know what to look for.

Example calculations you can try right now

Open any calculator and enter these scenarios to verify your outputs. For a ₹5,000 monthly SIP at 12% over 15 years, you should see ₹25 lakh invested and ₹75 lakh total corpus. Try a ₹10 lakh lumpsum at 11% over 8 years, which projects ₹23.04 lakh maturity value. Change only one variable at a time, increase SIP to ₹7,500 or extend tenure to 18 years to see how each factor impacts your final amount differently.

Most calculation errors happen because you change multiple inputs simultaneously without tracking which variable affected your results.

Three mistakes that ruin your projections

First, assuming constant returns across all market conditions when actual index fund performance fluctuates between negative 10% and positive 30% in different years. Second, forgetting to account for taxes on your projected gains, which reduces your actual take-home corpus by 12.5% on LTCG. Third, using overly optimistic return rates above 15% based on recent bull market performance instead of long-term historical averages.

Conclusion

You now know how to use an index fund calculator India tool to project your SIP or lumpsum returns, but these projections only become valuable when you act on them. Run your calculations with realistic return assumptions between 10% to 12%, adjust your monthly contributions or investment timeline to match your actual financial goals, and remember that calculators show estimates, not guarantees.

Your next step goes beyond calculations. You need to pick the right index funds, optimize your portfolio for tax efficiency, and adjust your strategy as markets change. Most investors waste months reading conflicting advice online or stick with outdated portfolios because they lack personalized guidance.

Invsify combines AI-powered insights with SEBI-registered advisory expertise to help you move from projections to actual wealth building. You get real-time portfolio tracking, conflict-free recommendations, and human support when you need quick answers. Start your free Wealth Wellness Score assessment to see exactly where your current investments stand and what adjustments will get you to your goals faster.