Index Investing Explained: How It Works, Pros, And Risks

Shlok Sobti

Index Investing Explained: How It Works, Pros, And Risks

Most mutual fund managers in India fail to beat their benchmark index over a 10-year period. That's not opinion, it's what the SPIVA India Scorecard has shown repeatedly. So when you have index investing explained with real data behind it, the question shifts from "why index funds?" to "why not?" For Indian salaried professionals looking to grow wealth without paying steep fees or relying on a fund manager's gut feeling, index investing offers a straightforward, low-cost path that's hard to ignore.

But straightforward doesn't mean there's nothing to learn. You still need to understand how index funds actually work, where they fall short, what risks come with them, and how to pick the right one for your portfolio. Getting these basics right is the difference between a confident investor and someone just following the crowd. That's exactly the kind of clarity Invsify is built to provide, conflict-free, AI-powered investment guidance registered with SEBI, designed to help you make informed decisions rather than guesswork-based ones.

This guide breaks down everything you need to know, from what index investing is and how it compares to active management, to practical steps for getting started and the risks you should weigh before putting your money in. Whether you're a first-time investor or someone rethinking their current strategy, you'll walk away with a clear, actionable understanding of index investing and whether it fits your financial goals.

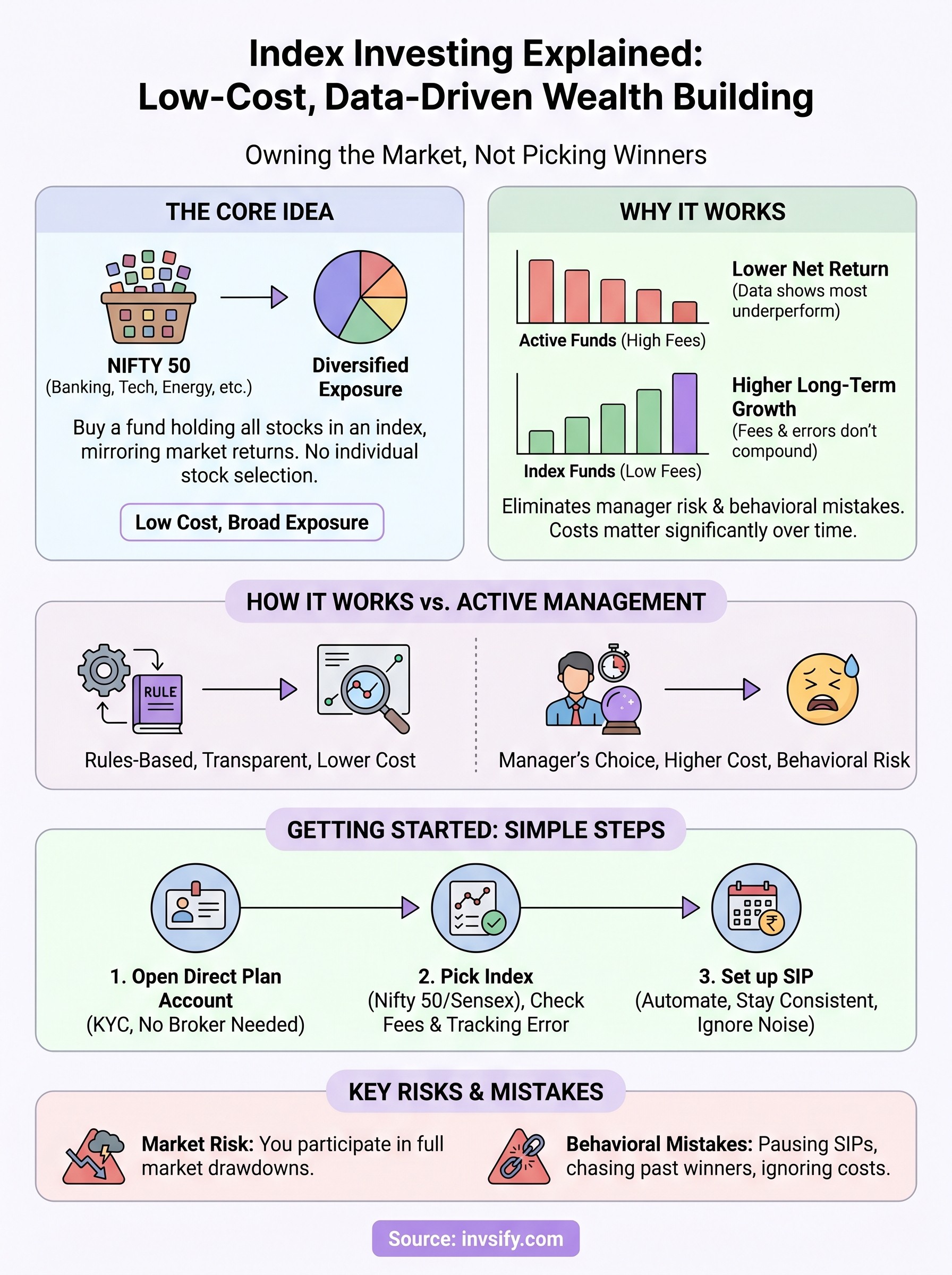

What index investing is and what it is not

At its core, index investing means buying a fund that holds every stock, or a representative sample, in a specific market index, in the same proportions the index uses. When the Nifty 50 rises by 2%, your index fund rises by roughly 2%. When it falls, you fall with it. There's no fund manager selecting individual stocks, no research team trying to predict the next big winner. You own the market, or a defined slice of it, and your returns mirror what that market actually delivers.

The core idea: owning the market, not picking winners

Most investors spend a lot of time thinking about which stocks or funds will outperform. Index investing flips that question entirely. Instead of asking "which fund manager will beat the market this year?", you ask "how do I capture what the market delivers at the lowest possible cost?" That shift is fundamental. A Nifty 50 index fund holds shares in 50 of India's largest listed companies across sectors, from banking and energy to technology and consumer goods. When you invest in it, you automatically get diversified exposure to all of them without making a single stock-picking decision.

When you stop trying to beat the market and focus on matching it efficiently, you eliminate one of the biggest risks most investors overlook: the compounding cost of being wrong about who will outperform.

The index itself is just a structured list with clear rules. The S&P BSE Sensex, for example, tracks 30 of the largest and most actively traded stocks on the Bombay Stock Exchange. The Nifty 50 tracks the 50 largest on the NSE. Independent bodies maintain these indexes and set firm criteria for which stocks qualify, how they're weighted, and when they're replaced. An index fund follows those rules mechanically, which is exactly why operating costs stay so low compared to actively managed funds.

What index investing is not

Getting index investing explained properly also means knowing what it isn't, because there's a lot of confusion here. Index investing is not a guaranteed profit strategy. If the Nifty 50 drops 30% in a bear market, your fund drops with it. You're not shielded from market downturns simply because you're invested passively. The whole market can and does go through extended rough patches, and you need to be prepared to stay invested through them without panic-selling at the bottom.

Index investing is also not the same as randomly owning a collection of stocks. Some investors assume that buying a diversified fund means they're being careless about their financial future. In reality, choosing the right index, the right fund that tracks it, and the right asset allocation for your specific goals requires deliberate decisions. Passive investing does not mean passive planning, and confusing the two leads to poorly built portfolios.

Finally, index investing is not a new or complicated concept reserved for sophisticated investors. In India, index funds have been available for decades, and their popularity has grown significantly as more investors have become aware of how expense ratios and hidden distributor commissions quietly erode long-term returns. The category has matured considerably, with multiple fund houses now offering Nifty 50, Nifty Next 50, and Sensex trackers at very low costs. What's changed most is the quality of data available, and that data increasingly shows active funds struggling to consistently keep pace with their benchmarks after fees are accounted for.

Why index investing works for most investors

The argument for index investing doesn't rely on theory alone. Decades of performance data across markets consistently show that most actively managed funds fail to outperform their benchmarks after fees are factored in. For Indian salaried investors with limited time to research stocks or track fund manager decisions, that reality makes a strong case for simply tracking the market rather than trying to beat it.

The math that works against active management

Every rupee paid in fees is a rupee that doesn't compound over time. An actively managed large-cap fund in India might charge an expense ratio of 1.5% to 2% annually, while a comparable Nifty 50 index fund charges as little as 0.10% to 0.20%. That gap may look small in year one, but over 20 or 30 years it creates a significant difference in your final portfolio value.

A 1.5% annual fee difference on a ₹10 lakh investment compounding at 12% per year means you could end up with roughly ₹20 to ₹30 lakhs less over 30 years compared to the lower-cost alternative.

Beyond fees, active fund managers face a structural challenge: to beat an index, they must consistently make better calls than every other professional investor operating in the same market. Markets are not perfectly efficient, but they're efficient enough that sustained outperformance is rare. Most active funds that beat their benchmark in one period fail to repeat it in the next.

Behavioral advantages that most investors overlook

Index investing also reduces one of the biggest threats to long-term wealth: your own behavior under pressure. When you own an actively managed fund, every quarter's underperformance raises a question in your head: should I switch? That constant temptation to exit, compare, and re-enter funds costs investors real money through poor timing decisions and transaction friction.

With a clear index fund strategy, your decision-making load drops sharply. You know exactly what you own, how it's weighted, and why. There's no need to track a fund manager's tenure, style drift, or latest calls. That simplicity makes it much easier to stay invested through volatility, which is where most of the long-term return is actually earned. For investors who want their money working consistently without constant intervention, understanding index investing explained in this way makes the appeal immediately obvious.

How market indexes are built and tracked

Understanding how indexes are constructed gives you a much clearer picture of what you actually own when you invest in an index fund. Indexes are not random collections of stocks; they follow documented, rule-based criteria managed by independent index providers. In India, major indexes like the Nifty 50 and S&P BSE Sensex are maintained by NSE Indices Limited and Asia Index Private Limited respectively, both of which publish their methodology openly so you can evaluate exactly what you're buying before you commit a single rupee.

How stocks get selected and weighted

Each index uses defined criteria to decide which stocks qualify and how much weight each one receives. For the Nifty 50, a stock must have traded on the NSE for at least six months, meet a minimum average market capitalization threshold, and demonstrate sufficient liquidity. Stocks that fail these standards get removed during periodic reviews, typically held every quarter. That systematic review process keeps the index current and representative of the actual large-cap market without any subjective calls from a portfolio manager.

Once you grasp how index construction works, index investing explained at this level is really about trusting a transparent, rules-based process rather than an individual's judgment.

Most Indian indexes use free-float market capitalization weighting. This means each stock's weight reflects only the shares available for public trading, excluding shares held by promoters or locked-in institutional blocks. A company with a larger free-float market cap carries a bigger weight in the index, which is why banking and financial stocks tend to dominate the Nifty 50's composition at any given time. That concentration is worth knowing before you assume an index fund gives you perfectly balanced sector exposure.

How index funds track the index

An index fund manager's job is to replicate the index as closely as possible. The primary method is full replication, where the fund buys every stock in the index in the same proportions the index specifies. For a liquid index like the Nifty 50, full replication is straightforward because all 50 stocks trade at high volumes with minimal transaction friction.

The metric that tells you how well a fund is doing this job is tracking error, which measures the gap between the fund's actual returns and the index's returns over a set period. A lower tracking error means the fund is closely mirroring its benchmark. When you compare index funds, tracking error alongside the expense ratio is one of the most useful data points to check, because a fund with a marginally higher cost but tighter tracking can still outperform a cheaper but sloppier alternative over the long run.

Index funds vs ETFs in India

Both index funds and ETFs (Exchange Traded Funds) track the same benchmarks, such as the Nifty 50 or the Sensex, but they work differently in practice. Understanding that difference matters because the right vehicle depends on how you invest and what kind of account access you have. For anyone getting index investing explained in an Indian context, this distinction often gets skipped over, yet it has real consequences for your convenience, costs, and ability to invest consistently over time.

How they differ in structure and access

An index mutual fund works the same way any mutual fund does. You buy or redeem units at the end-of-day NAV (Net Asset Value), and you don't need a demat account to get started. This makes index funds particularly practical for salaried investors who want to set up a monthly SIP and automate the process entirely. Your money goes in on a fixed schedule, units get allotted at that day's NAV, and there's no brokerage fee involved.

For most salaried investors in India, the ability to run a systematic investment plan without a demat account or active trading interface makes index mutual funds the more practical starting point.

Unlike index funds, an ETF trades on the stock exchange throughout the day, just like a share. To buy an ETF, you need both a demat account and a trading account with a registered broker. Prices fluctuate intraday based on demand, which means you can potentially buy at a more favorable price at a specific moment, but you also introduce brokerage charges and the risk of buying at a premium to the fund's actual underlying value.

Feature | Index Mutual Fund | ETF |

|---|---|---|

Trading | End-of-day NAV | Real-time on exchange |

Demat account needed | No | Yes |

SIP availability | Yes | Not directly |

Brokerage cost | None | Applicable |

Intraday flexibility | No | Yes |

Which one fits your situation better

ETFs often carry slightly lower expense ratios than comparable index mutual funds, which appeals to investors already comfortable with a demat account and willing to monitor liquidity. The trade-off is that many ETFs in India have relatively low daily trading volumes, which means the bid-ask spread can quietly erode your effective returns even when the headline expense ratio looks attractive.

For most people building wealth through consistent monthly contributions, index mutual funds offer the cleaner experience: no demat requirement, full SIP automation, and straightforward execution. If you actively trade through a broker account already and prefer the marginal cost advantage of ETFs, they make sense, but only when you pick funds with high trading volumes and consistently tight spreads.

Costs that matter: fees, tracking, and taxes

When people get index investing explained at a surface level, they focus entirely on fund selection and miss the cost layer underneath. Three specific cost factors shape your actual returns: the expense ratio, tracking error, and taxation. Getting each one right matters, and ignoring any single one quietly reduces what you actually keep from your investment over time.

Expense ratios and their long-term impact

The expense ratio is the annual fee a fund house charges to manage the fund, expressed as a percentage of your invested amount. For direct index mutual funds in India, this typically ranges from 0.10% to 0.25% for Nifty 50 or Sensex trackers. That figure sounds small, but compounded over 20 to 30 years on a growing portfolio, even a 0.5% difference in costs translates to a meaningful gap in your final corpus.

The difference between a regular plan and a direct plan of the same index fund can range from 0.5% to 1% annually, and that extra charge goes to distributors without adding a single rupee of investment return to you.

Always invest through direct plans, which you can access through fund house websites or registered investment advisors. Regular plans carry a higher expense ratio because they embed distributor commissions in the cost structure, and those commissions reduce your compounding base every single year without providing you any additional value.

Tracking error: the hidden cost of poor replication

Tracking error measures how closely a fund's actual performance matches its benchmark index. A low tracking error, typically below 0.10% to 0.20% annualized, tells you the fund is replicating the index accurately. A higher tracking error means the fund drifts from its benchmark due to factors like cash drag, delayed rebalancing, or internal transaction costs, all of which come out of your pocket indirectly.

When comparing two index funds with similar expense ratios, tracking error and tracking difference become the deciding factors. Check the fund's factsheet directly on the AMC's website before you commit, because a slightly costlier fund with tighter tracking can still deliver better net returns.

Taxes on index fund returns in India

Short-term capital gains (STCG) apply when you sell index fund units within 12 months of purchase, and these are taxed at 20% under the current regime. Hold beyond 12 months and long-term capital gains (LTCG) at 12.5% apply, with gains up to ₹1.25 lakh per financial year exempt from tax entirely.

Staying invested for the long term is not just sound strategy; it also keeps your effective tax rate lower, which means more of your compounded growth stays in your portfolio rather than going to the government.

Risks and common mistakes to avoid

Index investing does not eliminate risk; it changes the type of risk you carry. With a Nifty 50 index fund, you absorb the full movement of the market, both up and down. Understanding where real losses come from in this strategy, and what behavioral mistakes amplify them, is the part of index investing explained that most beginner guides skip over.

Market risk and concentration you may not expect

Your biggest exposure with a broad index fund is market-wide drawdowns. If Indian equity markets fall 30% to 40% during a recession or global crisis, your index fund falls by roughly the same amount. There's no active manager stepping in to reduce equity exposure or rotate to safer assets. You carry the full swing of the market, and that requires both financial and psychological preparation before you invest.

The investors who lose money in index funds are almost never those who picked the wrong fund; they're the ones who sold during a downturn and re-entered too late.

Sector concentration is another real risk worth knowing before you build your portfolio. The Nifty 50 has heavy exposure to financial services, which has consistently made up 30% or more of the index weight. If banking or financial stocks face a systemic shock, your "diversified" fund takes a disproportionate hit. Pairing a Nifty 50 fund with a mid-cap or international index fund can reduce this concentration without introducing active management into your portfolio.

Mistakes that quietly damage your returns

Several common behavioral and structural mistakes erode the advantage that index funds are supposed to give you. Knowing them in advance keeps your strategy intact when markets get turbulent.

Stopping SIPs during market downturns: This is the most damaging mistake. Falling markets mean you buy more units at lower prices, which is exactly when rupee-cost averaging works in your favor. Pausing your SIP removes that benefit entirely.

Chasing last year's top-performing index: Investors often switch to whichever index category did best recently, like mid-caps after a strong rally, right before a correction hits. Recency bias drives this decision, not logic.

Ignoring tracking error when selecting funds: Picking an index fund based only on brand name and missing a high tracking error means your returns quietly lag the benchmark over years.

Investing in regular plans instead of direct plans: The distributor commission embedded in regular plans compounds against you every year with no benefit to your actual returns.

Over-diversifying across too many index funds: Holding five Nifty 50 funds from different AMCs adds zero diversification and only creates tax and administrative complexity.

How to start index investing step by step

Getting started with index investing is simpler than most people expect, but the sequence matters. Skipping steps or rushing decisions leads to the common mistakes covered in the previous section. Follow this process in order and you'll have a working portfolio set up in under a week.

Open a direct plan account with a registered platform

You don't need a demat account to buy index mutual funds through direct plans. You can open an account directly on an AMC's website or through a SEBI Registered Investment Advisor platform that offers direct plan access without embedding distributor commissions. Before investing a single rupee, complete your KYC (Know Your Customer) verification online using your PAN card, Aadhaar, and bank account details. The whole process typically takes one to two business days, and most platforms walk you through it step by step.

Pick your index and find the right fund

Once your account is ready, decide which index you want to track based on your risk appetite and investment horizon. For most first-time investors, the Nifty 50 or Sensex is the right starting point because both track large, stable companies with long performance histories. After picking the index, compare funds that track it by looking at two numbers: the expense ratio and tracking error. A lower expense ratio with a tighter tracking error is what you want. Check the fund's factsheet on the AMC's website directly rather than relying on third-party summaries, since those numbers can lag by weeks.

With index investing explained at this level, you have everything you need to evaluate funds on the facts that actually drive your returns, not marketing material.

Set up a SIP and automate contributions

Lump-sum investing works, but a monthly SIP removes the timing problem entirely. You don't need to predict market highs or lows; your fixed monthly amount buys fewer units when prices are high and more units when prices fall, which averages your cost over time. Set your SIP amount to a figure you can sustain without strain even during months when money feels tight, because consistency over years matters far more than the size of your first investment. Link it to your salary account and set the debit date a few days after your pay credit date so the transfer happens automatically without requiring your attention each month.

Verify your KYC status before starting

Select a direct plan, not a regular plan

Cross-check both expense ratio and tracking error

Set a SIP date that aligns with your pay cycle

Review your portfolio once every six months, not every week

Sample portfolio frameworks for Indian goals

No single index fund allocation works for every investor in India. Your age, income stability, existing liabilities, and specific financial goals all shape how much you put into which index, and in what combination. The frameworks below are starting points, not rigid prescriptions. Use them as a reference to build your own allocation, then adjust based on your actual risk tolerance and timeline.

The early-career investor (age 22 to 32)

At this stage, time is your most powerful asset. You have decades of compounding ahead, which means you can tolerate more short-term volatility in exchange for higher long-term growth. A portfolio weighted heavily toward equity index funds makes sense here, because even a significant market correction has years to recover before you need the money.

The biggest advantage a young investor has is not higher income or market knowledge; it's time, and index funds let you put that time to work at the lowest possible cost.

A practical starting allocation for this stage:

80% Nifty 50 index fund (large-cap stability and broad market exposure)

15% Nifty Next 50 index fund (mid-to-large cap growth with slightly higher volatility)

5% international index fund (global diversification, reduces India-only concentration risk)

The mid-career investor with specific goals (age 33 to 45)

At this stage, you likely have clearer financial targets: a child's education in 10 years, a home upgrade in 7 years, or a retirement corpus target you've actually calculated. Your allocation should start reflecting those timelines rather than defaulting to maximum equity exposure. Goals with shorter horizons need progressively lower equity weights and more predictable instruments alongside your index funds.

A workable structure for this stage:

Goal Horizon | Equity Index Allocation | Debt or Liquid Allocation |

|---|---|---|

Under 3 years | 30% | 70% |

3 to 7 years | 60% | 40% |

Over 7 years | 80% | 20% |

The pre-retirement investor (age 46 to 55)

With retirement a decade or less away, capital protection becomes as important as growth. You still want equity exposure because inflation erodes purchasing power faster than most people account for, but with index investing explained in the context of a shorter runway, the priority shifts to reducing the impact of a major market drawdown right before you stop earning. A Nifty 50 allocation of 50% to 60%, paired with debt funds tracking short-duration bond indexes, gives you continued growth potential without betting your retirement on market timing. Review this allocation every two to three years and reduce equity gradually as you approach your target date.

Key takeaways and next steps

With index investing explained from the ground up, you now have what most investors spend years figuring out on their own. Index funds work because they keep costs low, remove behavioral guesswork, and give you reliable market exposure without depending on any fund manager's skill or timing. The data consistently favors this approach over active management for most Indian investors, and the structural advantages only grow stronger over longer time horizons.

Your next step is simple: start with a direct plan Nifty 50 index fund, set up a monthly SIP that fits your income, and leave it alone. Review your allocation every six months and adjust as your goals evolve, but resist the urge to react to short-term market noise. If you want personalized guidance on building the right index fund allocation for your specific goals, get conflict-free, AI-powered advice from Invsify and put a proper plan behind your investing decisions.