How To Get Conflict-Free Investment Planning Advice (India)

Shlok Sobti

How To Get Conflict-Free Investment Planning Advice (India)

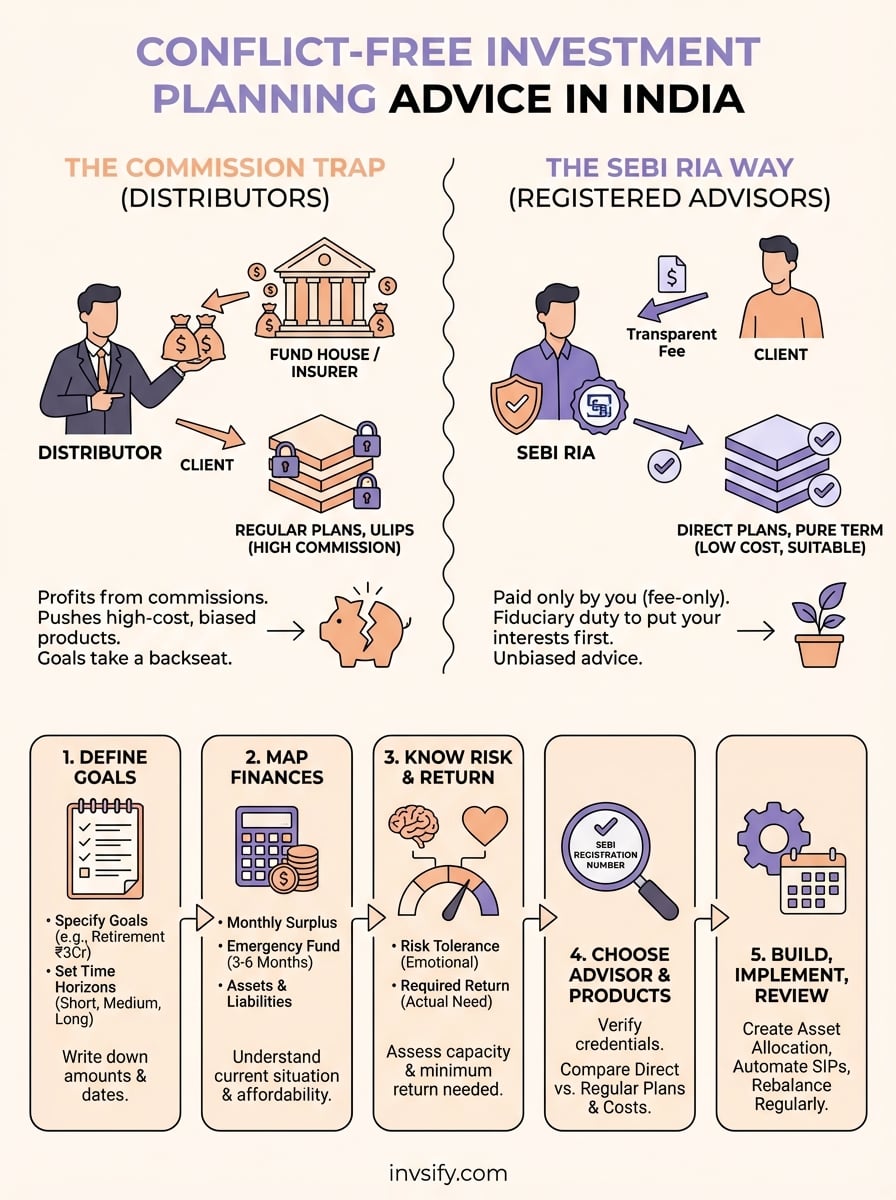

You research mutual funds online. You compare returns. You read expert predictions. Then someone convinces you to buy a product that earns them a fat commission while you pay hidden fees for decades. This happens because most investment advisors in India are actually distributors who profit from selling specific products. They present themselves as advisors but get paid by the companies whose products they push. Your financial goals take a backseat to their incentive structure.

A SEBI Registered Investment Advisor works differently. They charge you a transparent fee and recommend products based only on what helps you. No commissions from fund houses. No pressure to buy high cost plans. Just advice aligned with your wealth goals.

This guide walks you through getting conflict free investment planning advice that actually serves your interests. You will learn how to define your goals clearly, assess your current finances, understand your risk appetite, choose the right advisor model, and build a plan you can stick with. By the end you will know exactly how to avoid biased recommendations and create an investment strategy that grows your wealth without hidden costs eating into your returns.

What conflict-free investment advice is in India

Conflict-free investment planning advice means your advisor gets paid only by you and not by the companies whose products they recommend. This fundamental difference changes everything about the advice you receive. When an advisor earns commissions from mutual fund houses or insurance companies, they face pressure to recommend products that pay them the most rather than products that serve you best. A conflict-free advisor eliminates this problem by charging you a transparent fee and staying legally prohibited from accepting any commissions.

SEBI (Securities and Exchange Board of India) created the Registered Investment Advisor (RIA) framework in 2013 to solve exactly this problem. An RIA must register with SEBI and follow strict rules that prevent them from selling products or earning commissions. You pay them directly through a fee structure you both agree on upfront. They recommend products based solely on what fits your financial situation, risk appetite, and goals.

The commission trap most investors fall into

Traditional distributors typically earn 1 to 2 percent annual commission from the mutual funds they sell you. This commission comes from your investment returns every single year. A distributor who puts you in a regular mutual fund plan earns money as long as you stay invested. The longer you hold the fund, the more they make. This creates an obvious incentive to recommend funds that pay higher commissions rather than funds with the best performance or lowest costs.

The difference between a regular plan and a direct plan of the same mutual fund can cost you 30 to 40 percent of your total returns over 20 years.

Insurance products create even worse conflicts. A distributor can earn 40 to 100 percent of your first year premium when they sell you a ULIP or traditional insurance policy. They push these high commission products as investment solutions when you actually need term insurance and separate investments. You end up locked into expensive products for 10 to 15 years while they pocket massive upfront payments.

What SEBI registration guarantees

A SEBI Registered Investment Advisor operates under legal fiduciary duty to put your interests first. They must disclose all fees upfront. They cannot receive any payment from product manufacturers. They cannot hold your money or securities. SEBI audits their compliance and can suspend or cancel their registration if they violate these rules.

RIAs charge through different fee models you can evaluate:

Fee Model | How It Works | Best For |

|---|---|---|

Flat annual fee | Fixed amount regardless of portfolio size | Investors with smaller portfolios |

Percentage of assets | 0.5 to 1.5% of assets under advisory | Investors with larger portfolios |

Hourly consultation | Pay per hour of advice | One-time financial planning needs |

Retainer fee | Monthly or quarterly fixed fee | Ongoing advisory relationship |

You can verify any advisor's SEBI registration by checking their registration number on the SEBI website. Look for advisors who display their SEBI RIA registration number prominently and provide clear documentation of their fee structure before you engage them.

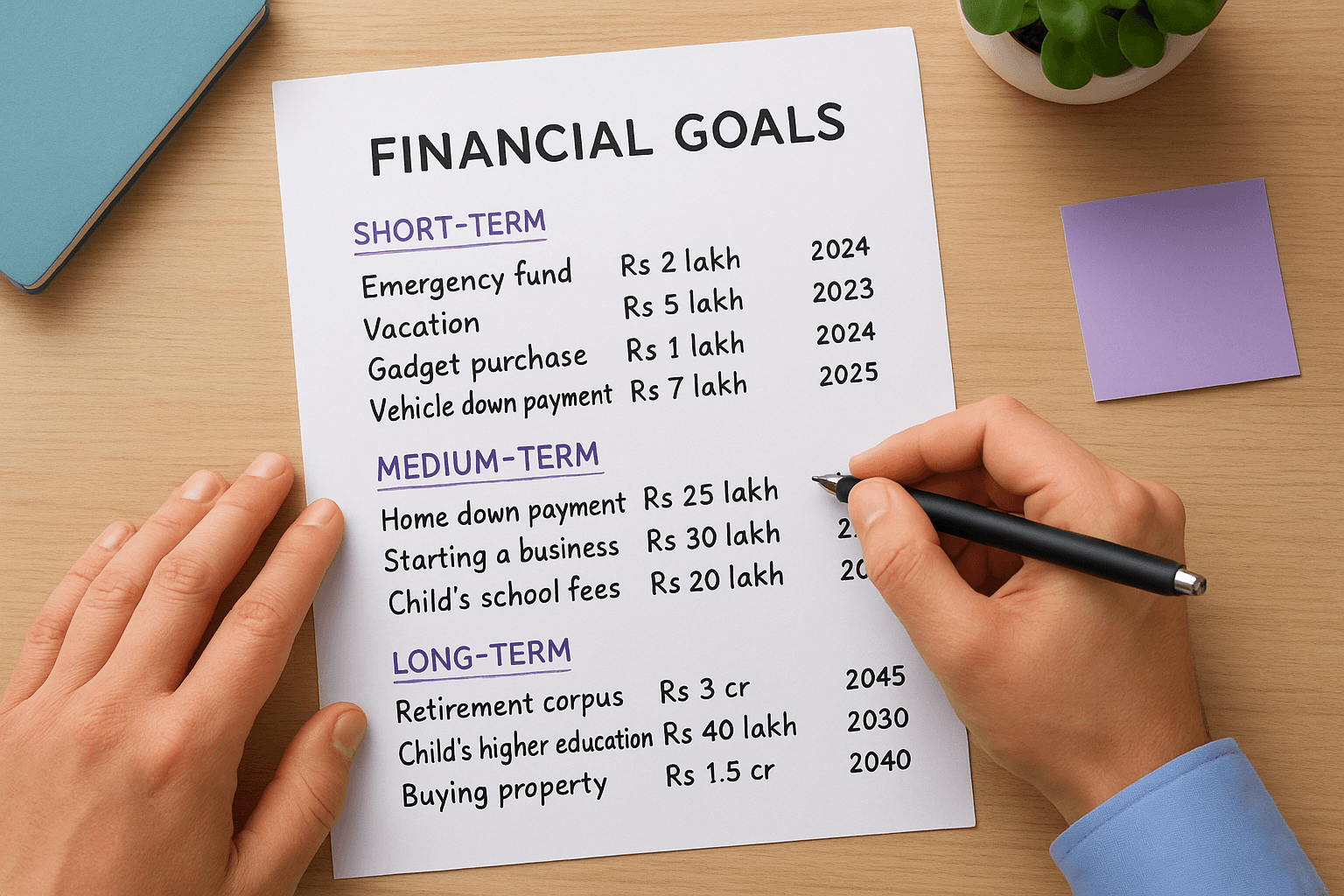

Step 1. Define your goals and time horizons

Investment planning advice only works when you know exactly what you want your money to do for you. You cannot build a sensible investment strategy without clear targets. Most people skip this step and jump straight to picking products, which leads to buying investments that do not match their actual needs. Start by writing down your financial goals in concrete terms with specific amounts and dates attached to each one.

Write down specific financial goals

Create a document where you list every financial goal you want to achieve. Do not use vague phrases like "save for retirement" or "build wealth." Instead write "accumulate Rs 3 crore by age 60 for retirement" or "save Rs 15 lakh in 3 years for home down payment." The specificity forces you to think through what you actually need rather than what sounds good.

Your goals document should include:

Short term goals (1 to 3 years): Emergency fund, vacation, gadget purchase, vehicle down payment

Medium term goals (3 to 7 years): Home down payment, starting a business, child's school fees

Long term goals (7+ years): Retirement corpus, child's higher education, buying property

The clearer your goals, the easier it becomes to choose investments that actually help you reach them.

Assign time horizons to each goal

Time horizon determines everything about how you should invest for a goal. A goal you need to achieve in 2 years requires completely different investments than one you have 20 years to work toward. Markets fluctuate in the short term but tend to reward patient investors over longer periods. You cannot take market risk with money you need next year.

Match your goals to the right time buckets using this framework:

Time Horizon | Risk Level | Suitable Investments |

|---|---|---|

0 to 3 years | Very low | Liquid funds, ultra short term debt funds, FDs |

3 to 7 years | Low to moderate | Short term debt funds, balanced advantage funds, conservative hybrid funds |

7 to 15 years | Moderate to high | Large cap equity funds, index funds, balanced hybrid funds |

15+ years | High | Diversified equity funds, mid cap funds, small cap funds |

Write the target amount, target date, and time horizon next to each goal in your document. This creates your investment planning roadmap that any conflict-free advisor can use to build your portfolio.

Step 2. Map your current finances and safety net

You cannot get meaningful investment planning advice without knowing where you stand financially right now. Most investors skip this critical step and start investing before they have secured their basic financial foundation. Your advisor needs to see your complete financial picture to recommend investments that actually fit your situation. This step involves three specific tasks that reveal whether you can afford to invest and how much you should allocate to different goals.

Calculate your monthly cash flow

Track every rupee that comes in and goes out for at least one full month to understand your spending patterns. Use a simple spreadsheet where you record your salary, freelance income, rental income, and any other money you receive. On the expense side, write down everything you spend including rent, EMIs, groceries, utilities, entertainment, subscriptions, and discretionary purchases.

Create a cash flow statement using this structure:

Income Category | Amount (Rs) | Expense Category | Amount (Rs) |

|---|---|---|---|

Salary | 80,000 | Rent | 20,000 |

Freelance work | 15,000 | EMIs | 18,000 |

Groceries | 8,000 | ||

Utilities | 3,000 | ||

Other expenses | 22,000 | ||

Total Income | 95,000 | Total Expenses | 71,000 |

Surplus | 24,000 |

The surplus amount tells you how much you can realistically invest each month without stretching your finances. If you spend more than you earn, you need to fix that problem before considering any investments. Your advisor will use this surplus figure to calculate how much to allocate toward each of your goals.

Build your emergency fund first

Set aside three to six months of essential expenses in liquid savings before you invest a single rupee in equity or long term products. Essential expenses mean rent, utilities, groceries, insurance premiums, and EMIs that you must pay regardless of what happens. Do not include entertainment, dining out, or discretionary spending in this calculation.

Calculate your emergency fund target by adding up just your non negotiable monthly expenses and multiplying by six. For example, if your essential expenses total Rs 40,000 per month, you need Rs 2.4 lakh sitting in a savings account or liquid fund. Park this money in an instrument you can access within 24 to 48 hours without penalties. Never invest your emergency fund in equity mutual funds or fixed deposits with lock in periods.

No investment planning advice makes sense if you lack the buffer to handle job loss, medical emergencies, or unexpected expenses without selling your long term investments at a loss.

List all assets and liabilities

Create a personal balance sheet that shows everything you own and everything you owe as of today. On the asset side, list your bank balances, existing mutual fund investments, PPF balance, EPF accumulation, insurance cash values, property values, and vehicle values. Write down the current market value, not what you paid for these assets.

Your liabilities sheet needs every loan you carry with its outstanding principal, interest rate, and monthly EMI. Include home loans, car loans, personal loans, credit card outstanding balances, and any money you borrowed from friends or family. Note the remaining tenure for each loan.

This balance sheet reveals whether you carry expensive debt that you should pay off before investing. Any loan charging more than 12 percent interest typically deserves faster repayment over new investments. Your net worth equals total assets minus total liabilities, which gives both you and your advisor a baseline to measure your wealth building progress over time.

Step 3. Know your risk profile and return needs

Your risk tolerance determines which investments suit you and which ones will keep you awake at night worrying about market crashes. Investment planning advice means nothing if it recommends products that make you panic and sell at the worst possible time. You need to understand both how much risk you can emotionally handle and how much return you actually need to achieve your goals. These two factors together guide which asset allocation works for your situation rather than following generic portfolio templates that ignore your specific circumstances.

Assess your psychological risk capacity

Answer these specific questions honestly to gauge your emotional response to market volatility. How would you react if your Rs 5 lakh investment dropped to Rs 3.5 lakh in three months because of a market correction? Would you stay invested, add more money at lower prices, or sell immediately to prevent further losses? Your honest answer reveals more about your risk profile than any theoretical questionnaire.

Think through your actual behavior during past financial stress. Did you withdraw money from equity funds during March 2020 when markets crashed 40 percent? Did you panic when your portfolio showed deep red numbers? Those reactions matter more than what you think you would do. People who stayed calm and held their equity investments during previous crashes can genuinely handle higher equity allocation.

Use this framework to categorize your risk tolerance:

Risk Profile | Portfolio Loss Tolerance | Equity Allocation | Typical Investor |

|---|---|---|---|

Conservative | Cannot stomach more than 10% loss | 20 to 30% | Near retirement, needs capital protection |

Moderate | Can handle 15 to 25% loss | 40 to 60% | Mid career, balanced approach |

Aggressive | Comfortable with 30%+ loss | 70 to 90% | Young investor, long time horizon |

Calculate the returns you actually need

Work backward from your financial goals to determine the minimum annual return required to reach each target. Take your goal amount, subtract what you have already saved for it, and use the future value formula to find the return needed given your monthly contribution and time horizon. Many investors chase 15 percent returns when they only need 10 percent to meet their goals, which pushes them to take unnecessary risk.

Calculate your required return using this method: If you need Rs 50 lakh in 15 years for your child's education and you can invest Rs 10,000 monthly, you need approximately 11 to 12 percent annual returns. You can achieve this with a balanced portfolio of 60 percent equity and 40 percent debt without taking extreme risk in small cap funds. Your advisor should show you these calculations for each goal and recommend appropriate asset allocation that matches both your risk tolerance and return requirements rather than pushing high risk products because they assume everyone wants maximum returns.

The gap between the return you need and the return you chase often determines whether you succeed or fail at reaching your financial goals.

Step 4. Choose the right advisor and products

Finding the right advisor separates investors who reach their goals from those who waste decades in expensive products that primarily benefit distributors. You need to verify credentials, ask pointed questions, and evaluate every recommendation through a lens of cost and suitability. This step protects you from biased investment planning advice that serves someone else's commission targets rather than your wealth building objectives. Your choice of advisor determines whether you pay transparent fees for genuine guidance or hidden costs that compound against you for years.

Verify SEBI RIA credentials properly

Check the advisor's SEBI registration number on the official SEBI website before you share any financial information or pay any fees. Go to the SEBI website, navigate to the intermediaries section, and search for Registered Investment Advisors. The database shows the advisor's registration number, registration date, and current status. Only work with advisors whose registration shows as active and valid with no pending violations or suspensions.

Ask the advisor for their IA certificate issued by SEBI and verify the details match what appears in the official database. Look for their business address, email, phone number, and fee structure disclosed in their registration. SEBI requires RIAs to maintain a minimum net worth and carry professional indemnity insurance, which protects you if the advisor makes errors. Legitimate advisors display their SEBI registration prominently and provide documentation without hesitation when you request it.

Ask these specific questions before hiring

Schedule an initial consultation where you evaluate whether the advisor's approach fits your needs. Ask them directly: "Do you receive any commissions, referral fees, or payments from mutual fund companies, insurance providers, or other financial product manufacturers?" The answer must be an unqualified no. Any hesitation or explanation about how referral fees benefit you should immediately disqualify them.

Probe their process by asking: "How will you assess my financial situation and develop recommendations?" Quality advisors describe a systematic process that starts with understanding your goals, analyzing your current finances, determining your risk profile, and then recommending specific products. They should explain their fee structure in rupee terms, show you examples of what you will pay annually, and put everything in writing before you commit.

An advisor who spends more time selling their services than understanding your financial situation probably prioritizes their revenue over your outcomes.

Request references from existing clients in similar life stages to yours and ask those clients about their experience. Find out if the advisor responds promptly to queries, provides regular portfolio reviews, and adjusts recommendations when circumstances change. Your relationship with an advisor spans years or decades, so you need someone who commits to ongoing support rather than collecting a fee and disappearing.

Evaluate product recommendations objectively

Every investment your advisor recommends should directly connect to a specific goal in your financial plan. When they suggest a mutual fund, ask "Which goal does this fund address and why is this particular fund appropriate?" The answer should reference your time horizon, risk tolerance, and return requirements for that specific goal. Generic recommendations that ignore your documented needs signal the advisor operates from templates rather than personalized analysis.

Compare costs using this framework before accepting any recommendation:

Product Type | What to Check | Red Flag |

|---|---|---|

Mutual funds | Direct plan vs regular plan | Recommending regular plans |

Insurance | Pure term vs investment plans | Pushing ULIPs or endowment policies |

Debt products | Expense ratio and exit load | Products with >1% expense ratio |

Advisory fee | Total cost as % of portfolio | Fees exceeding 1.5% for portfolios under Rs 50 lakh |

Verify that recommended mutual funds appear as direct plans with low expense ratios and strong long term track records. Your advisor should explain why each fund fits your portfolio rather than relying on recent past performance. Reject any recommendation to buy insurance products as investments or suggestions to invest in instruments with high exit loads or lock in periods that do not match your goal timelines.

Step 5. Build, implement, and review your plan

Your financial plan only creates value when you convert it from a document into actual investments and monitor progress consistently. Building the plan means creating a detailed asset allocation strategy that maps each rupee to specific goals and products. Implementation involves opening accounts, completing KYC, and executing transactions in the right sequence. Regular reviews ensure your plan stays aligned with changing circumstances and market conditions rather than becoming an outdated document you ignore for years.

Create your asset allocation strategy

Write down exactly how you will split your monthly surplus across different goals and asset classes. Take your Rs 24,000 monthly surplus example and allocate it based on goal priority and time horizon. Your emergency fund gets first allocation until you complete it, followed by simultaneous investments toward your short term, medium term, and long term goals.

Structure your allocation document like this:

Goal | Monthly Investment | Product Type | Specific Product |

|---|---|---|---|

Emergency fund (Rs 2.4L) | Rs 10,000 for 6 months | Liquid fund | Parag Parikh Liquid Fund Direct |

Home down payment (3 years) | Rs 5,000 | Short term debt fund | ICICI Prudential Short Term Fund Direct |

Child education (15 years) | Rs 6,000 | Diversified equity fund | Nifty 50 Index Fund Direct |

Retirement (25 years) | Rs 3,000 | Equity fund | Parag Parikh Flexi Cap Direct |

Your allocation should show product names with direct plan specifications rather than generic categories. This level of detail transforms vague investment planning advice into executable instructions that eliminate confusion when you actually start investing. Document your rationale for each product selection so you remember why you chose it when markets test your conviction later.

Execute the plan systematically

Complete your KYC process first before attempting any investments. Get your PAN card verified, complete your In-Person Verification (IPV), and link your bank account to the platforms you will use for investing. Most mutual fund platforms and brokerage accounts accept digital KYC through video verification, which takes 15 to 20 minutes compared to days with physical paperwork.

Set up systematic investment plans (SIPs) on specific dates that align with your salary credit day. If your salary arrives on the 1st of each month, schedule all SIPs for the 5th to ensure funds remain available. Auto debit through your bank mandate prevents you from skipping investments when you feel tempted to spend instead.

The gap between planning to invest and actually investing represents the difference between financial goals you achieve and goals that remain wishes.

Start with your emergency fund and complete it before adding other investments. This sequencing protects you from taking premature risk or withdrawing long term investments during emergencies, which destroys your compound growth potential. Your advisor should provide implementation support including account opening assistance and transaction guidance rather than abandoning you after delivering a plan document.

Set review checkpoints

Schedule portfolio reviews every six months on fixed dates like January 1st and July 1st to assess whether your investments perform as expected and your circumstances changed. During each review, compare your actual portfolio value against the projected value from your financial plan. Calculate whether you stay on track to reach each goal or need to adjust monthly contributions.

Rebalance your portfolio when any asset class drifts more than 10 percentage points from target allocation. If your plan calls for 60 percent equity and 40 percent debt but equity gains push it to 72 percent equity, sell some equity and buy debt to restore balance. This disciplined approach forces you to sell high and buy low rather than letting emotions drive timing decisions.

Document changes to your income, expenses, or goals immediately and update your plan accordingly. When you receive a salary increase, decide in advance how much of that increase goes toward investments rather than lifestyle inflation. Your advisor should conduct formal annual reviews where they reassess your complete financial situation and recommend adjustments based on your progress and any life changes.

Bringing it all together

You now have a complete framework for getting conflict-free investment planning advice that serves your financial goals instead of someone else's commission targets. The five steps covered in this guide work together to protect you from biased recommendations while building a portfolio that actually matches your needs, timeline, and risk tolerance. Start by documenting your specific goals with amounts and dates, then assess your current finances to determine how much you can realistically invest each month.

Most investors waste years locked in expensive products because they skipped the advisor verification step or accepted recommendations without questioning costs and suitability. You can avoid that trap by checking SEBI registration credentials and demanding transparency about fees before you commit your money. The difference between direct mutual fund plans and regular plans alone saves you lakhs over two decades.

Sign up with a SEBI Registered Investment Advisor who provides AI-powered insights and conflict-free recommendations that put your wealth goals first.