Investment Planning Calculator India: How To Use It In 2026

Shlok Sobti

Investment Planning Calculator India: How To Use It In 2026

You have a goal, maybe it's retiring at 50, buying a house in five years, or simply building a corpus that lets you sleep well at night. The gap between that goal and your current savings? That's exactly what an investment planning calculator India helps you figure out. It takes your numbers, monthly SIP amount, expected returns, time horizon, and shows you whether your plan actually adds up or needs a rethink.

But here's the thing most people miss: a calculator gives you projections, not a plan. The real value comes from acting on those numbers with the right guidance. That's where Invsify fits in. As a SEBI Registered Investment Advisor, we combine AI-powered recommendations with conflict-free advice to help you move from "I ran the numbers" to "I'm actually on track." No hidden commissions, no guesswork.

This article breaks down what an investment planning calculator does, how to use one effectively in 2026, the inputs that actually matter, and how to avoid the common mistakes that lead to unrealistic expectations. Whether you're starting your first SIP or optimizing an existing portfolio, you'll walk away with a clear framework to plan smarter.

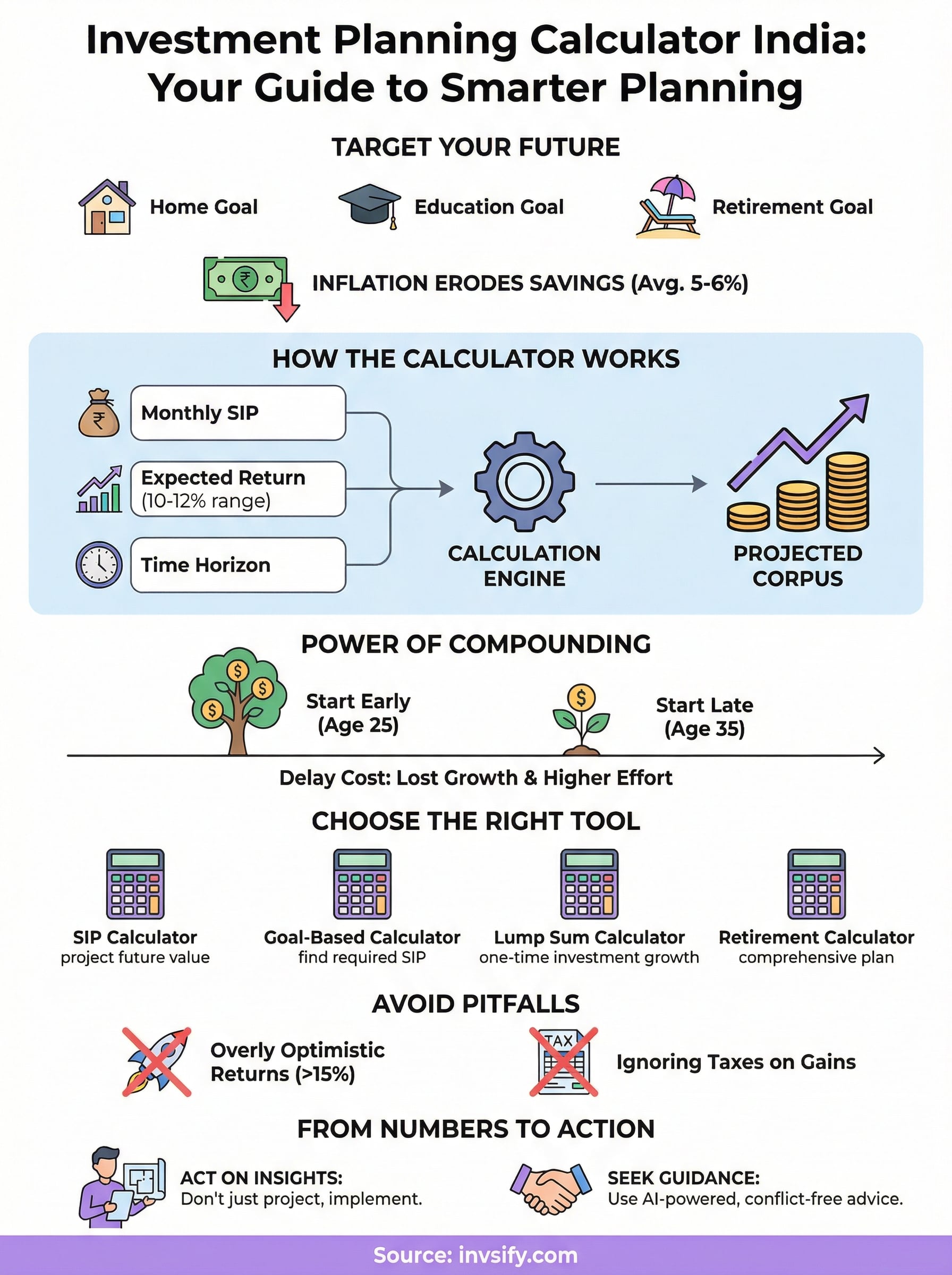

Why investment planning calculators matter in India

India's financial landscape is unlike most other countries. Inflation in India has historically averaged 5-6% annually, and real estate, education, and healthcare costs have grown even faster. If you're planning for a goal 15 or 20 years from now without accounting for this, you're almost certainly underestimating what you'll need. An investment planning calculator India-focused tool helps you factor in these local realities, so your projections actually reflect what your money will be worth when you finally need it.

The gap between saving and investing

Most salaried individuals in India save money, but fewer invest it with a clear purpose. Keeping funds in a savings account earning 3-4% interest while inflation runs at 5-6% means you're losing purchasing power every single year without realizing it. A calculator forces you to confront this gap by showing you two numbers side by side: where you'll end up if you keep doing what you're doing now, and where you actually need to be. That contrast alone changes behavior more than any amount of generic financial advice.

The real danger isn't losing money in the market. It's letting inflation quietly erode your savings while you think you're being careful.

Why Indian goals are harder to price than they look

When you say you want to retire comfortably or fund your child's education, those goals sound clear enough. But they're not. The cost of a postgraduate degree in India 12 years from now is not what it costs today, and neither is the monthly income you'll need in retirement after accounting for medical expenses, lifestyle inflation, and longevity. Calculators help you translate vague goals into specific, inflation-adjusted rupee targets, which makes them actionable rather than aspirational.

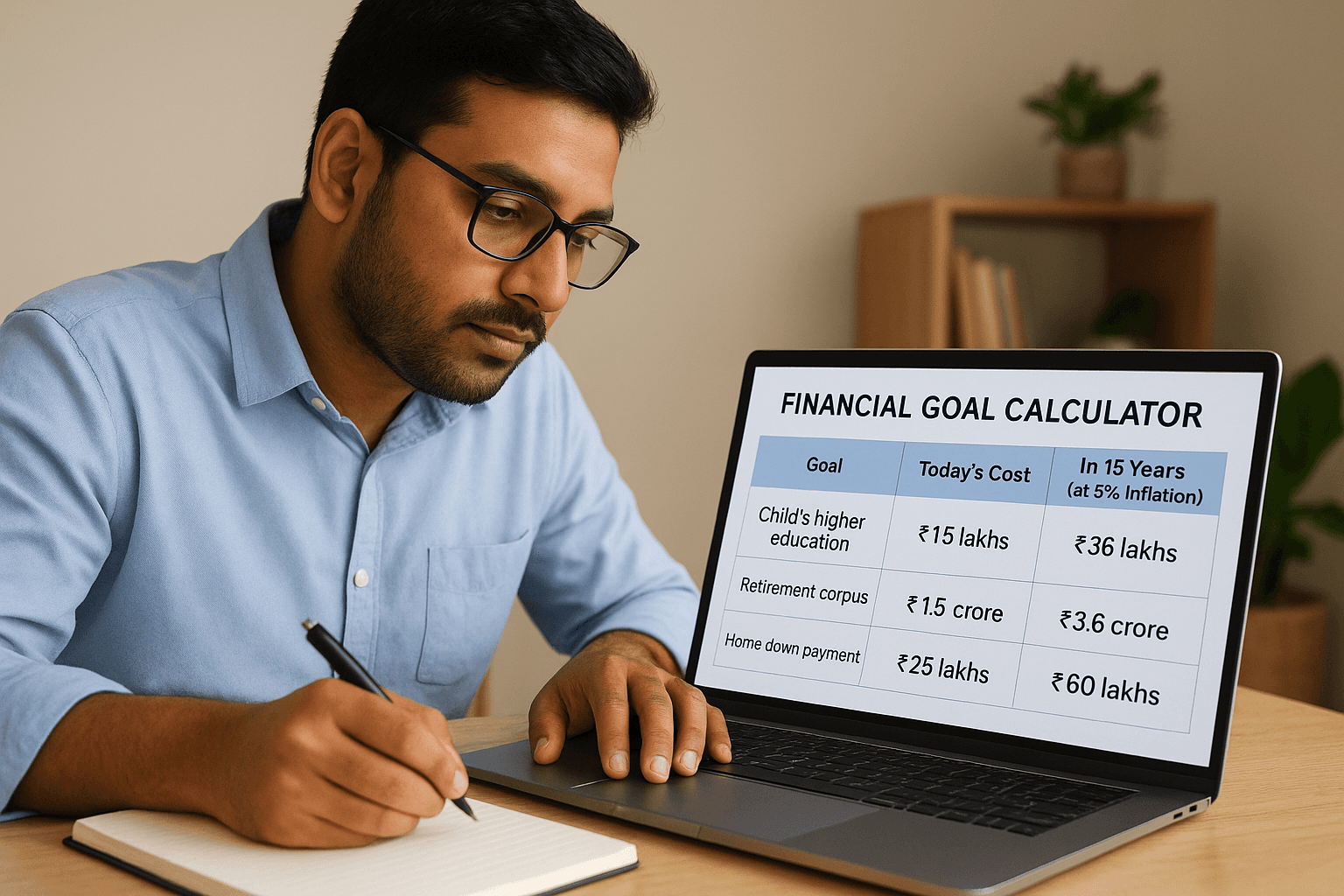

Here's a quick example of how inflation reshapes your target:

Goal | Today's Cost | In 15 Years (at 6% inflation) |

|---|---|---|

Child's higher education | ₹15 lakhs | ₹36 lakhs |

Retirement corpus (monthly need ₹50,000) | ₹1.5 crore | ₹3.6 crore |

Home down payment | ₹25 lakhs | ₹60 lakhs |

These numbers shift significantly over time. Planning without a calculator means you're likely targeting a figure that's already outdated before you've even started.

The compounding window is shorter than you think

India has one of the youngest working populations in the world, which sounds like an advantage, and it is, but only if you start investing early. Most working professionals begin serious investing in their early 30s after managing EMIs, lifestyle upgrades, and family expenses through their 20s. That delay matters enormously. Losing even five years at the start of your investment journey can reduce your final corpus by 30-40%, depending on your assumed rate of return.

A calculator makes this visible immediately. You can enter your current age, your target retirement age, and your monthly SIP amount, and see within seconds how a five-year delay affects your outcome. Seeing the numbers change in real time is a far more persuasive argument for starting now than any rule of thumb you've read online. That's the core reason these tools matter: they replace vague financial anxiety with specific, actionable data that you can actually do something about.

What an investment planning calculator includes

Every investment planning calculator India tool is built around the same core architecture: you put in a set of inputs, it runs the math, and you get a projected outcome. But knowing exactly what those inputs mean and how they interact with each other changes how useful the result is for you. Most people fill in the fields quickly and accept the number at the bottom without questioning what drove it. That's a problem, because a misunderstood input leads to a misleading projection.

Core input fields

The inputs are the foundation of everything. Every calculator will ask for your monthly investment amount, your investment duration in years, and an expected rate of return. Some will also include your current age, your target retirement age, or the specific goal amount you're working toward. The expected return field is often where people default to an optimistic number without checking what's realistic for their chosen asset class.

Here are the standard inputs you'll find across most calculators:

Monthly SIP or lump sum amount you plan to invest

Expected annual rate of return (typically 10-12% for equity mutual funds, 6-7% for debt)

Investment duration in years

Existing corpus, if you're adding to a portfolio you've already started

Inflation rate, to calculate the real purchasing power of your future corpus

Goal amount in today's value, which the calculator then adjusts for inflation

The rate of return field carries more weight than any other input. Even a 2% difference in your assumed return can change your projected corpus by lakhs over a 20-year period.

What the output actually tells you

The output is typically a projected corpus figure at the end of your investment period, along with the total amount you invested versus the total returns generated. This split matters because it shows you how much of your final number came from compounding rather than your own contributions. In a well-structured long-term SIP, the returns should significantly outpace what you actually put in.

Some advanced calculators also show a year-by-year growth table, which lets you see the compounding curve rather than just the end figure. That breakdown helps you spot whether your current SIP amount is sufficient or whether you need to step up contributions as your income grows over time.

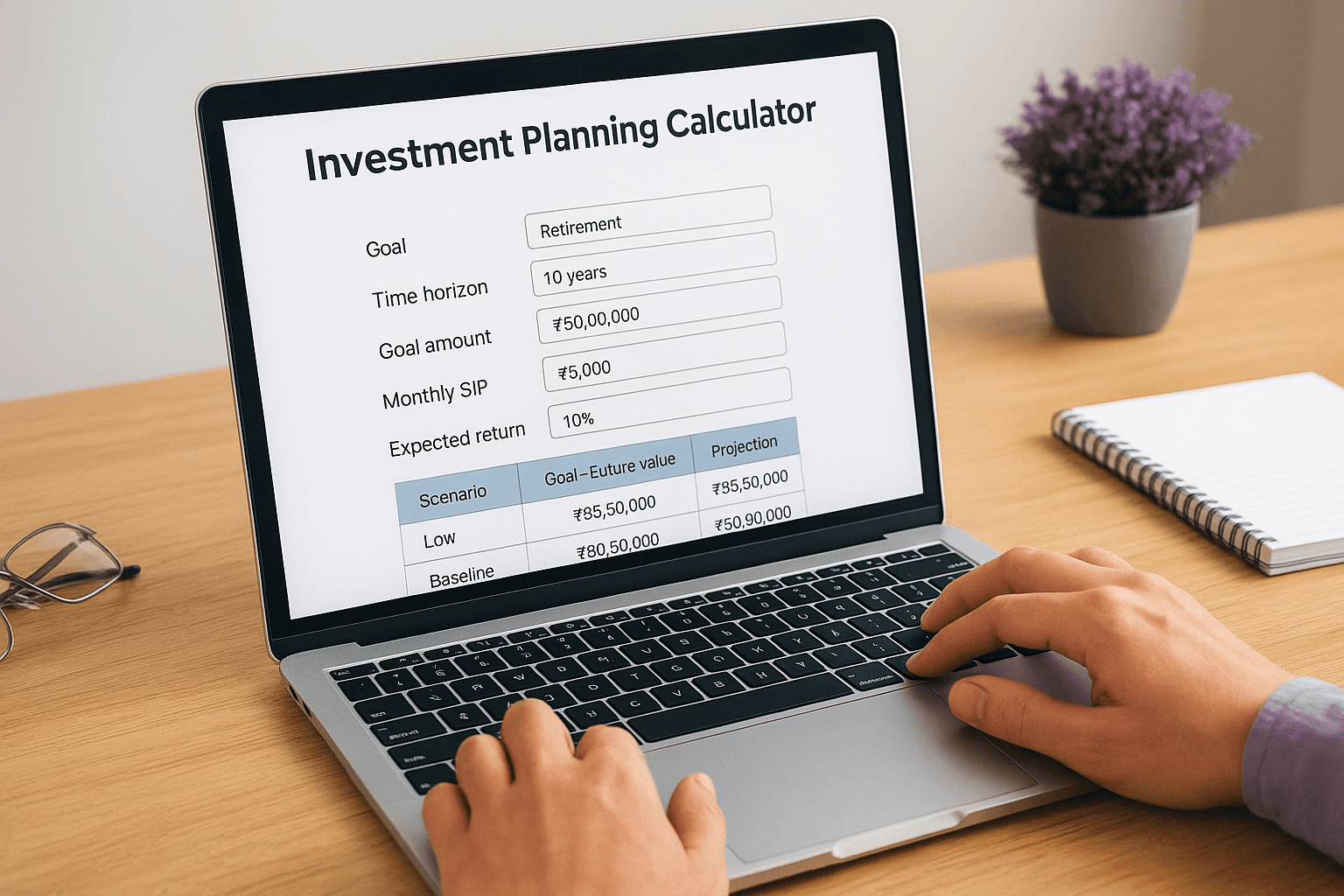

How to use an investment planning calculator in 2026

Using an investment planning calculator India tool is straightforward in theory, but most people rush through it and end up with a number that feels reassuring rather than accurate. The goal is not to get a big number at the end; it's to get an honest projection you can actually build a plan around. That means slowing down on each input, using realistic assumptions, and stress-testing the output before you treat it as a target.

Set your goal before you open the calculator

Before you enter a single number, define what you're actually planning for. Is it retirement, a child's education, a property down payment, or general wealth creation? Each goal has a different time horizon, a different required corpus, and a different acceptable level of risk. Going into a calculator without a defined goal means you're just doing math in the dark. Write down the goal, estimate what it costs in today's value, and let that guide every input you make.

Clarity on the goal is what separates a useful projection from a number you'll forget about by next week.

Enter inputs in a specific order

Start with your time horizon first, then your goal amount in today's value. Let the calculator apply an inflation rate to that figure to give you the future value of your goal. Next, enter your current savings or existing corpus if you're not starting from zero. Only after those anchor inputs are set should you enter your monthly SIP amount and expected return. This sequence keeps you goal-focused rather than return-focused, which is a healthier way to approach the math.

Run the numbers at least three times

One projection is not enough. Run your first scenario with a conservative return assumption, typically 10% for equity mutual funds, then run a second at 8% to account for underperformance, and a third at 12% if you want to see the upside. This gives you a range, not a single number. If the 8% scenario still gets you to your goal, your plan has a reasonable margin of safety. If only the 12% scenario works, your plan depends on perfect conditions, which is a signal to either increase your SIP or extend your timeline.

Inputs that change your results the most

Not all inputs carry equal weight in an investment planning calculator India tool. Some fields nudge your result by a few thousand rupees; others shift it by lakhs or even crores. Understanding which inputs drive the biggest swings lets you focus your attention on the variables that actually matter, rather than spending time fine-tuning numbers that make almost no difference to the final projection.

Expected rate of return

This is the single most impactful input in any calculator. A 2% difference in your assumed annual return can alter your final corpus by 30-50% over a 20-year period, which in rupee terms can mean the difference between reaching your goal and falling well short of it. Equity mutual funds in India have historically delivered 10-12% returns over long horizons, but past performance does not guarantee future results. Use 10% as your base case, run the numbers again at 8%, and only rely on a 12% assumption to understand the ceiling, not to build your entire plan around it.

Treating your expected return as a wish rather than a realistic estimate is the fastest way to build a plan that fails in real life.

Investment duration

Starting five years earlier has more impact on your final corpus than doubling your monthly SIP amount in most long-term scenarios. This is because compounding does its heaviest lifting in the later years of your investment period. Every year you delay is a year of compounding you cannot recover, regardless of how aggressively you invest later.

Here is what that looks like in practical terms for a ₹10,000 monthly SIP at 10% annual return:

Start Age | End Age | Total Invested | Projected Corpus |

|---|---|---|---|

25 | 60 | ₹42 lakhs | ₹3.8 crore |

30 | 60 | ₹36 lakhs | ₹2.3 crore |

35 | 60 | ₹30 lakhs | ₹1.3 crore |

SIP step-up rate

Most people enter a fixed monthly SIP amount and leave it static for the entire projection period. Adding an annual step-up of even 5-10%, in line with your salary increments, dramatically changes the output because more principal enters the compounding cycle at progressively earlier points each year. If your calculator has a step-up field, use it.

The step-up rate, the return assumption, and your start date are the three inputs that shape roughly 80% of your final number. Everything else is a rounding adjustment.

The main calculator types and when to use them

Not every investment planning calculator India tool works the same way, and picking the wrong type for your situation gives you numbers that don't actually answer your question. Each calculator type is built for a specific problem, so matching the tool to your goal is the first step before you enter any numbers.

SIP Calculator

A SIP calculator is the most widely used type. You enter a monthly investment amount, an expected annual return, and a time horizon, and it tells you the projected corpus at the end. Use this when you already know how much you can invest each month and want to understand what that commitment will grow into. It's forward-looking: you start with what you have and project outward.

Goal-Based Calculator

This type works in reverse. You start with a target corpus or goal amount, and the calculator tells you how much you need to invest each month to reach it. This is the right tool when you have a fixed goal, such as funding a child's education or building a retirement corpus of ₹2 crore, and need to work backward to find the required SIP. Goal-based calculators are more useful for structured financial planning because they connect your investment behavior directly to a specific outcome rather than an open-ended projection.

If you don't know what you're building toward, a SIP calculator gives you a number. A goal-based calculator gives you a direction.

Lump Sum Calculator

When you receive a bonus, inheritance, or a large one-time inflow, a lump sum calculator tells you what that single investment will grow into over time at an assumed rate of return. The math is simpler than a SIP calculator because there's no monthly compounding of new contributions, but the results can still be striking over a 10 to 15-year horizon. Use this alongside your SIP projections when you want a complete, accurate picture of your total portfolio's growth potential.

Retirement Calculator

A retirement calculator is the most comprehensive type. It factors in your current age, target retirement age, expected post-retirement expenses, and inflation to give you a specific corpus target. Many versions also let you input existing provident fund balances or other fixed income sources so you can isolate exactly how much your investments still need to contribute. Use this when you want a single, unified projection for retirement rather than running separate calculations for each piece.

Mistakes to avoid and quick sanity checks

Running an investment planning calculator India tool takes five minutes. Running it badly takes the same five minutes but leaves you with a plan built on flawed assumptions. The most dangerous projections are the ones that feel accurate, because they give you false confidence. A few specific mistakes come up repeatedly, and a handful of quick checks can catch them before they cost you years of progress.

Using an inflated return assumption

Most people enter 15% or higher as their expected annual return because they've seen that number in conversations about equity funds. Equity mutual funds in India have historically delivered 10-12% over long periods, but that average includes years of sharp underperformance that most people conveniently ignore when running projections. If your entire plan depends on a 14% or 15% return to work, you have no margin for error when markets deliver a weaker decade.

Base your plan on 10%. Run a second scenario at 8%. Only use 12% to understand the ceiling, not to set your targets.

Use the conservative number as your primary scenario and treat the optimistic number as a bonus, not a baseline.

Forgetting to account for tax on your returns

Your projected corpus is a pre-tax number. Long-term capital gains on equity mutual funds in India above ₹1.25 lakh per year are taxed at 12.5%, and debt fund gains are taxed at your income slab rate. Most basic calculators do not factor this in, which means your actual take-home corpus at redemption is lower than the figure on your screen. Factor this into your planning by setting a slightly higher goal amount to absorb the tax impact.

Skipping the sanity check after you run the numbers

After you get your projected corpus, run three quick checks before you accept the number:

Does the corpus cover your inflation-adjusted goal, or just today's cost of that goal?

Is your monthly SIP amount genuinely affordable, or did you enter an aspirational number?

Does your assumed return match the actual asset class you plan to invest in, or is it too optimistic for your chosen fund category?

These three checks take under two minutes and will immediately surface whether your projection reflects your real situation or a version of it you wish were true.

Conclusion

An investment planning calculator India tool does one thing well: it replaces guesswork with math. You now know which inputs drive the biggest swings in your projection, which calculator type fits your specific goal, and which mistakes quietly destroy an otherwise reasonable plan. The framework is straightforward once you understand what each number actually means and how it connects to your real-world outcome.

But a projection is only as useful as what you do with it next. Running the numbers without acting on them gets you nowhere closer to your goal. That's where having the right advisor makes the difference. At Invsify, you get SEBI-registered, conflict-free guidance backed by AI-powered recommendations, so your plan goes from a calculator output to an actual investment strategy built around your specific situation. No hidden fees, no generic advice.

Start building your investment plan with Invsify today and take the first step toward a portfolio that actually keeps up with your goals.