Investment Portfolio Growth: Build, Track & Boost In India

Shlok Sobti

Investment Portfolio Growth: Build, Track & Boost In India

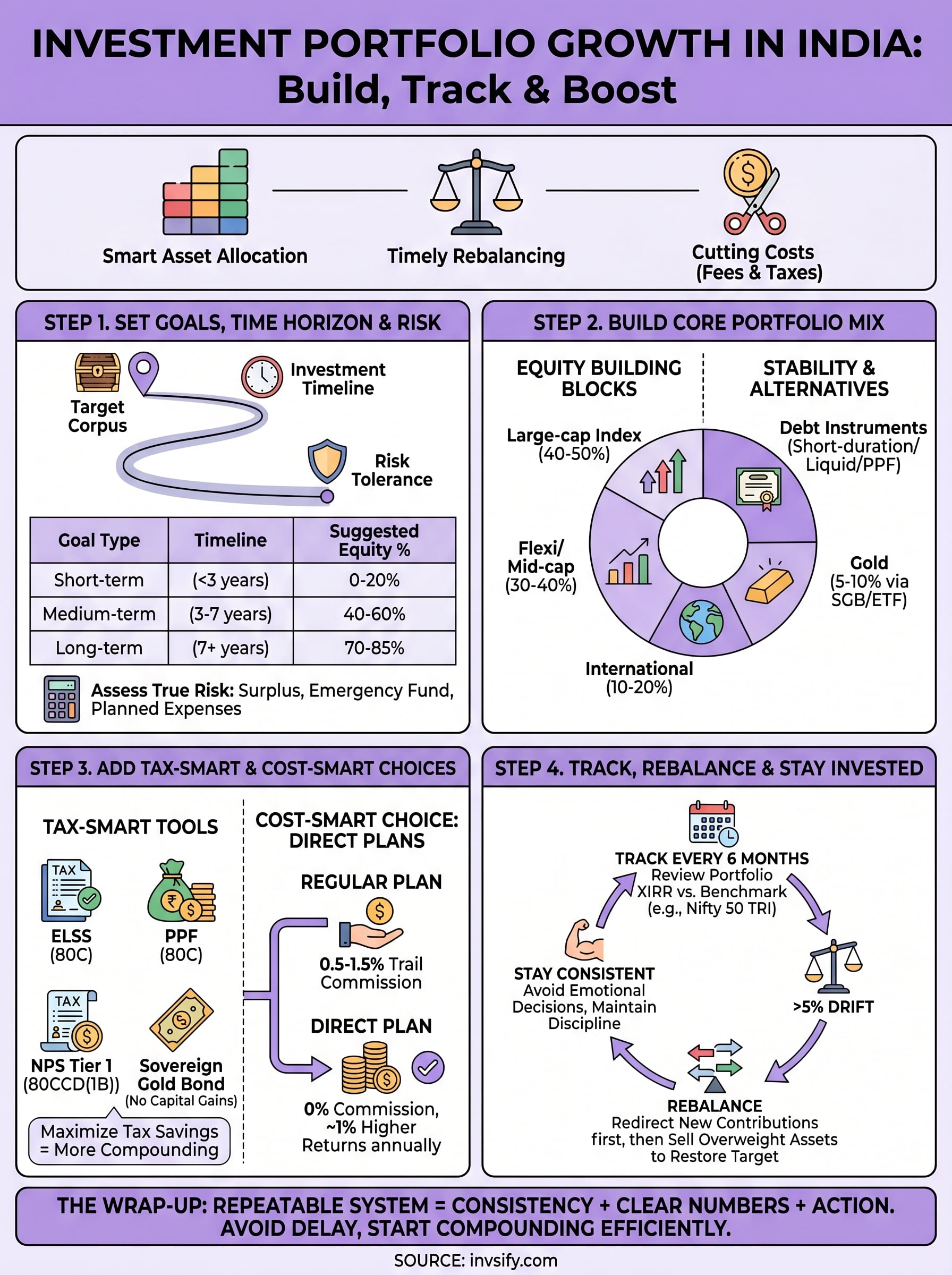

Most Indian investors start with the right intentions, SIPs, a few stocks, maybe some fixed deposits. But over time, their portfolios stagnate. The gap between parking money and achieving real investment portfolio growth comes down to three things: smart asset allocation, timely rebalancing, and cutting the costs that silently eat into your returns.

This guide breaks down exactly how to build a portfolio designed for growth, track its performance with the right metrics, and make adjustments that actually move the needle. You'll find step-by-step strategies alongside practical calculations you can apply whether you're managing ₹5 lakhs or ₹5 crores. No vague tips, just actionable frameworks backed by data.

At Invsify, we built our AI-powered advisory platform around this exact problem. As a SEBI Registered Investment Advisor, we help salaried professionals grow their wealth through conflict-free, transparent recommendations, without the hidden commissions that traditional distributors charge. Everything you'll read here reflects the principles we apply daily for our users.

What drives investment portfolio growth in India

Three variables determine how fast your portfolio grows: what you invest in, how long you stay invested, and how much you lose to fees and taxes. Most investors in India focus only on returns while ignoring the second and third variables. That imbalance is why many portfolios underperform benchmarks like the Nifty 50, which has delivered roughly 12-13% CAGR over the past two decades.

Asset allocation and market returns

India's financial markets offer a wider range of growth assets than most investors actually use. Equity mutual funds across large-cap, mid-cap, and flexi-cap categories form the highest-returning core of most well-built portfolios. Historically, large-cap funds have tracked around 11-13% CAGR, while mid-cap funds have averaged 14-16% over rolling 10-year periods, with higher short-term volatility attached.

Your split between equity, debt, and alternatives like gold or REITs directly determines your expected return and downside risk. A 25-year-old with a 30-year horizon can hold a 75-80% equity allocation comfortably. A 45-year-old protecting accumulated wealth should shift toward 50-60% equity, with fixed income instruments providing the stability buffer.

The single biggest driver of long-term investment portfolio growth is not stock-picking, it is asset allocation done consistently over time.

Compounding and the cost drag problem

Compounding works in both directions. Positive compounding on your returns builds wealth exponentially over time. But cost drag through fees, commissions, and avoidable taxes erodes that same base quietly, every single year.

Consider the numbers directly: a 1% annual expense difference on a ₹25 lakh portfolio over 20 years, assuming 12% gross returns, results in approximately ₹22 lakhs less at maturity. Traditional mutual fund distributors in India earn trail commissions of 0.5-1.5% per year from regular plans, pulled straight from your returns without a visible invoice.

Switching to direct plans and working with a SEBI Registered Investment Advisor who charges a transparent flat fee eliminates this drag entirely. Over a 20-year horizon, the difference in terminal wealth can exceed the size of your original principal. That is the most reliable lever you control outside of your monthly contribution amount.

Step 1. Set goals, time horizon, and risk

Before you build anything, you need three numbers: your target corpus, your investment timeline, and your risk tolerance. Without these, every allocation decision you make is guesswork. Every fund you pick and every SIP amount you set should trace directly back to what you lock in during this step.

Define your goal and timeline

Your goal determines the return rate you need, and your timeline determines how much volatility you can absorb. A ₹1 crore corpus for retirement in 25 years requires roughly a 10% CAGR on a ₹5,000 monthly SIP. A 5-year goal for a house down payment demands lower equity exposure because a 30% market drawdown two years before you need the money is not a recoverable situation.

Use this framework to categorize your goals before choosing any asset:

Goal Type | Timeline | Suggested Equity % |

|---|---|---|

Short-term | Under 3 years | 0-20% |

Medium-term | 3-7 years | 40-60% |

Long-term | 7+ years | 70-85% |

Your time horizon is the most important input in planning for investment portfolio growth because it determines how much risk you can actually afford to take.

Assess your risk tolerance honestly

Risk tolerance is not just emotional comfort during a market dip. It is also your financial capacity to absorb losses without disrupting your life plans. Before setting your equity allocation, calculate your monthly surplus, confirm you hold a 6-month emergency fund, and account for any large planned expenses in the next 24 months. These three numbers define your true risk floor.

Step 2. Build your core portfolio mix

Once you have your goals and risk profile set, you can build a portfolio structure that matches them. The goal here is not to pick the best-performing fund of last year. You want a diversified allocation that captures broad market growth while limiting concentration risk in any single sector or asset class.

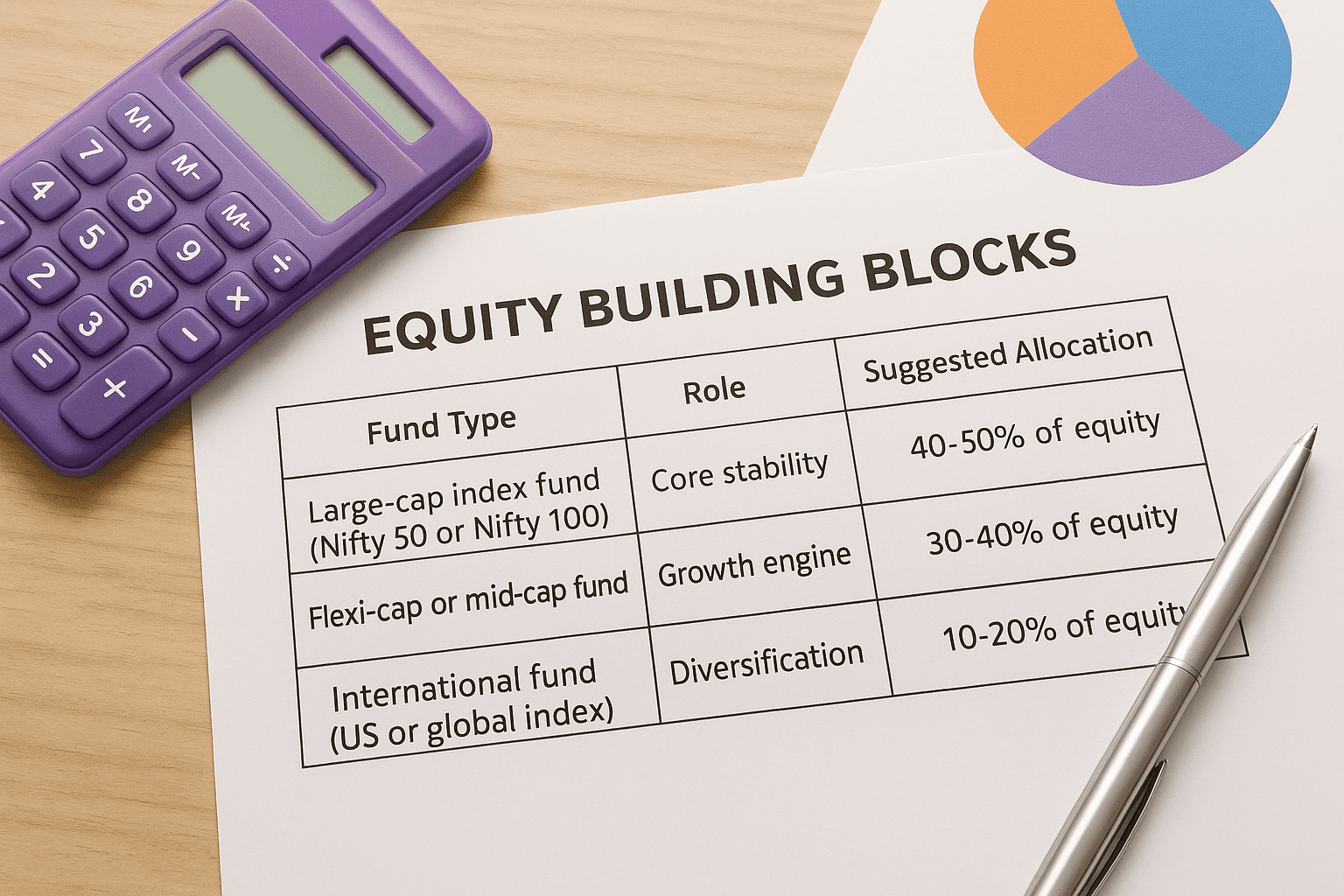

Choose your equity building blocks

Your equity sleeve drives the bulk of your investment portfolio growth over the long run. For most salaried investors in India, a three-fund equity core covers the full market efficiently without overwhelming complexity.

Fund Type | Role | Suggested Allocation |

|---|---|---|

Large-cap index fund (Nifty 50 or Nifty 100) | Core stability | 40-50% of equity |

Flexi-cap or mid-cap fund | Growth engine | 30-40% of equity |

International fund (US or global index) | Diversification | 10-20% of equity |

Keeping your equity core simple with index-linked options reduces fund manager risk and lowers the overall expense ratio of your portfolio.

Add stability with debt and alternatives

Debt instruments like short-duration funds, liquid funds, or PPF provide the ballast that keeps your portfolio from collapsing during sharp equity corrections. Allocate based on the percentage you determined in Step 1, then add 5-10% in gold through a sovereign gold bond or gold ETF to hedge against currency depreciation and inflation spikes. This three-layer structure, equity plus debt plus gold, forms a resilient foundation you can build on consistently.

Step 3. Add tax-smart and cost-smart choices

Two investors can hold the same portfolio and end up with vastly different wealth after 20 years, purely because one managed taxes and costs better. This step is where sustained investment portfolio growth either gets protected or quietly eroded. The changes here are structural, not speculative, and they compound just as reliably as returns do.

Use tax-saving instruments strategically

India's tax code gives you several legitimate tools to reduce your annual tax liability while building wealth at the same time. The most efficient ones for salaried investors are:

Instrument | Tax Benefit | Annual Limit |

|---|---|---|

ELSS Mutual Fund | Section 80C deduction | ₹1.5 lakhs |

PPF | Section 80C + tax-free maturity | ₹1.5 lakhs |

NPS Tier 1 | Additional ₹50,000 under 80CCD(1B) | ₹50,000 |

Sovereign Gold Bond | No capital gains tax if held to maturity | Based on availability |

Maximizing Section 80C and 80CCD(1B) together saves up to ₹46,800 annually in taxes for someone in the 30% bracket, which is money that stays invested and compounds.

Switch from regular to direct plans

Regular mutual fund plans pay a trail commission to your distributor every year, typically 0.5% to 1.5% of your assets. Direct plans of the same fund cut this cost entirely and credit those returns back to you. Log into your AMC's website or use the MF Central portal at mfcentral.com to initiate a switch. On a ₹30 lakh portfolio, saving 1% annually adds roughly ₹3 lakhs in returns over 10 years at 12% CAGR.

Step 4. Track, rebalance, and stay invested

Building your portfolio is only half the work. Consistent tracking and disciplined rebalancing are what keep your investment portfolio growth on course over years and decades. Without regular check-ins, drift happens quietly. Your equity allocation can balloon from 70% to 85% after a strong bull run, loading your portfolio with far more risk than you originally planned.

Set a rebalancing schedule

Check your portfolio allocation once every 6 months, not daily. Daily monitoring triggers emotional decisions that hurt long-term returns. Use a simple threshold rule: if any asset class drifts more than 5% from your target allocation, redirect new SIP contributions toward underweight categories before selling anything, which avoids triggering capital gains tax unnecessarily. If contributions alone cannot close the gap, then sell from the overweight asset to restore your original mix.

Rebalancing is not about chasing returns. It is about maintaining the risk level you set in Step 1 so your portfolio performs exactly the way you planned.

Track the right metrics

Avoid fixating on daily NAV movements. Instead, review XIRR (Extended Internal Rate of Return) on your overall portfolio every 6 months, since it accounts for the timing of each SIP contribution accurately. Compare your XIRR against a relevant benchmark like the Nifty 50 TRI over the same period. If you consistently underperform by more than 2% annually, investigate whether fund selection or cost drag is the cause. Your AMC portal can generate an XIRR report within minutes at no cost.

Wrap-up and next step

Investment portfolio growth in India follows a repeatable system: set clear goals, build a diversified core, cut tax and cost drag, then track your XIRR every six months and rebalance when allocations drift. None of these steps require market timing or complex financial products. What they require is consistency and a clear-eyed approach to the numbers that actually move your wealth forward over time.

The biggest risk you face is not a market correction. It is spending another year with a portfolio that was never structured to grow efficiently in the first place. Every month you delay switching to direct plans, maximizing 80C, or aligning your allocation to your actual goals is a month of compounding you cannot recover. The framework in this guide gives you everything you need to start.

Start building a smarter portfolio with Invsify and get conflict-free, AI-powered advice from a SEBI Registered Investment Advisor, with no hidden commissions.