Investopedia Asset Allocation: Meaning, Strategy, Examples

Shlok Sobti

Investopedia Asset Allocation: Meaning, Strategy, Examples

If you've ever searched for Investopedia asset allocation, you probably landed on a solid overview, but one written for a global audience with little relevance to Indian tax structures, mutual fund categories, or SEBI regulations. Asset allocation is the single most important decision you'll make as an investor, yet most explanations skip the practical details that actually matter when you're building a portfolio in India.

At its core, asset allocation is about dividing your money across different asset classes, equity, debt, gold, real estate, based on your risk tolerance, financial goals, and time horizon. Get it right, and your portfolio can weather market downturns without derailing your long-term plans. Get it wrong, and you're either taking on risk you can't afford or leaving returns on the table by being too conservative.

This guide breaks down everything Investopedia covers on asset allocation, meaning, strategies, and examples, while adding the context Indian salaried investors actually need. We'll walk through age-based models, risk-based approaches, and how to rebalance without unnecessary tax hits. At Invsify, as a SEBI Registered Investment Advisor, we use AI-driven portfolio analysis to help investors find the right allocation for their specific situation, conflict-free and transparent. Whether you're just starting out or rethinking an existing portfolio, this article gives you the framework to make smarter allocation decisions.

What Investopedia means by asset allocation

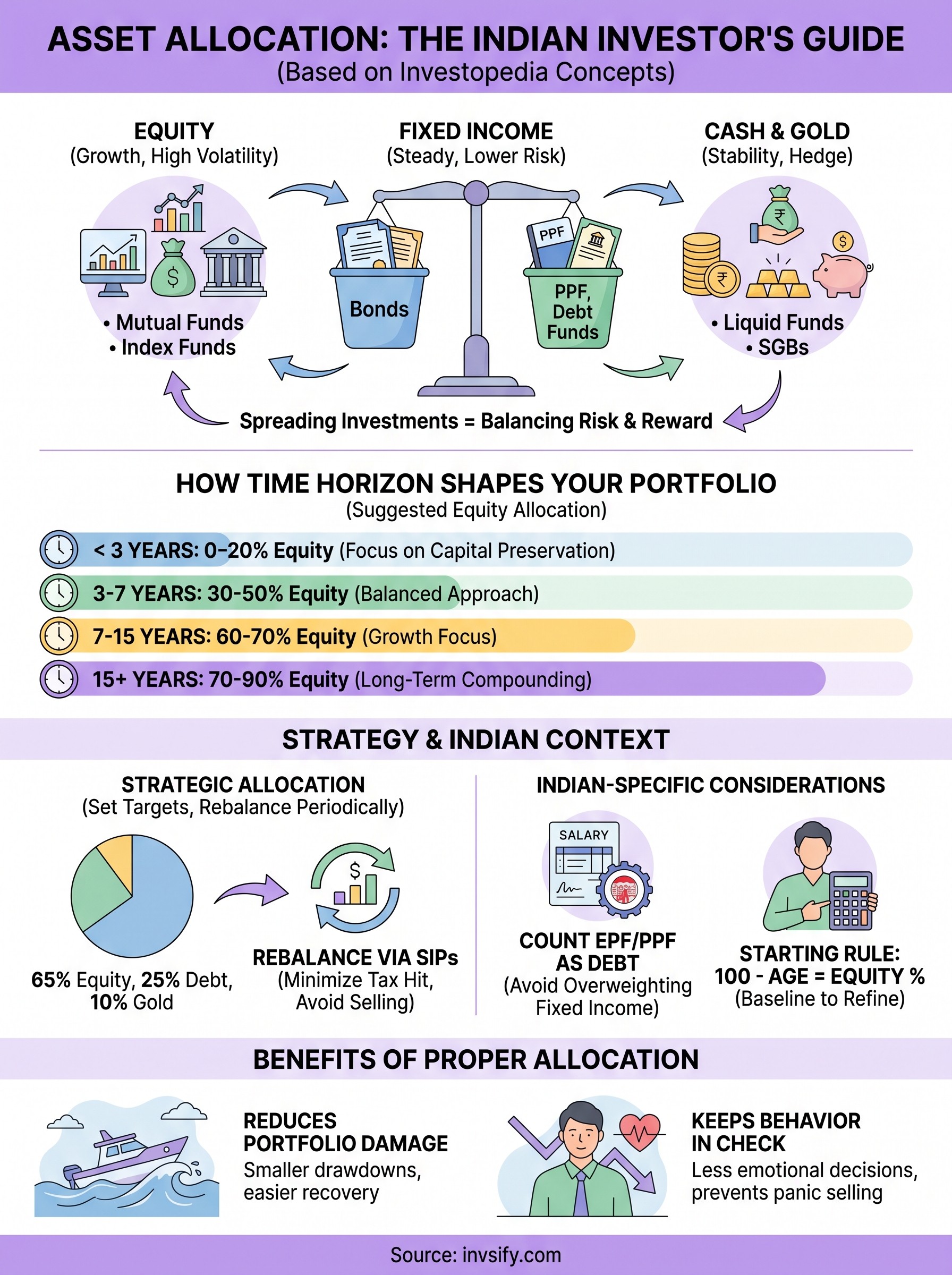

Investopedia defines asset allocation as the process of spreading your investments across different asset classes to balance risk and reward according to your personal goals, risk tolerance, and investment timeline. When you study investopedia asset allocation, you'll notice the explanation centers on three broad categories: equities (stocks), fixed income (bonds), and cash or cash equivalents. The logic is straightforward: different asset classes react differently to the same market conditions, so holding a mix reduces the damage any single rough year can do to your overall portfolio.

The goal of asset allocation isn't to pick the best-performing asset class; it's to hold a combination that matches what you can afford to lose and what you actually need to gain.

The three core asset classes Investopedia focuses on

Investopedia consistently organizes its allocation content around three primary building blocks: equities, fixed income, and cash. Equities offer the highest long-term growth potential but carry the most volatility. Fixed income instruments provide steadier, more predictable returns at lower risk. Cash or cash equivalents sit at the lowest-risk end but lose purchasing power over time due to inflation.

For Indian investors, these categories map directly onto familiar products:

Equities: Direct stocks, equity mutual funds, index funds, ETFs

Fixed income: PPF, EPF, fixed deposits, debt mutual funds, government bonds

Cash equivalents: Liquid funds, savings accounts, short-duration FDs

Understanding these three buckets helps you see why no single product covers your entire financial picture. Your portfolio needs all three working together in the right proportions, not just the one that delivered the best returns last year.

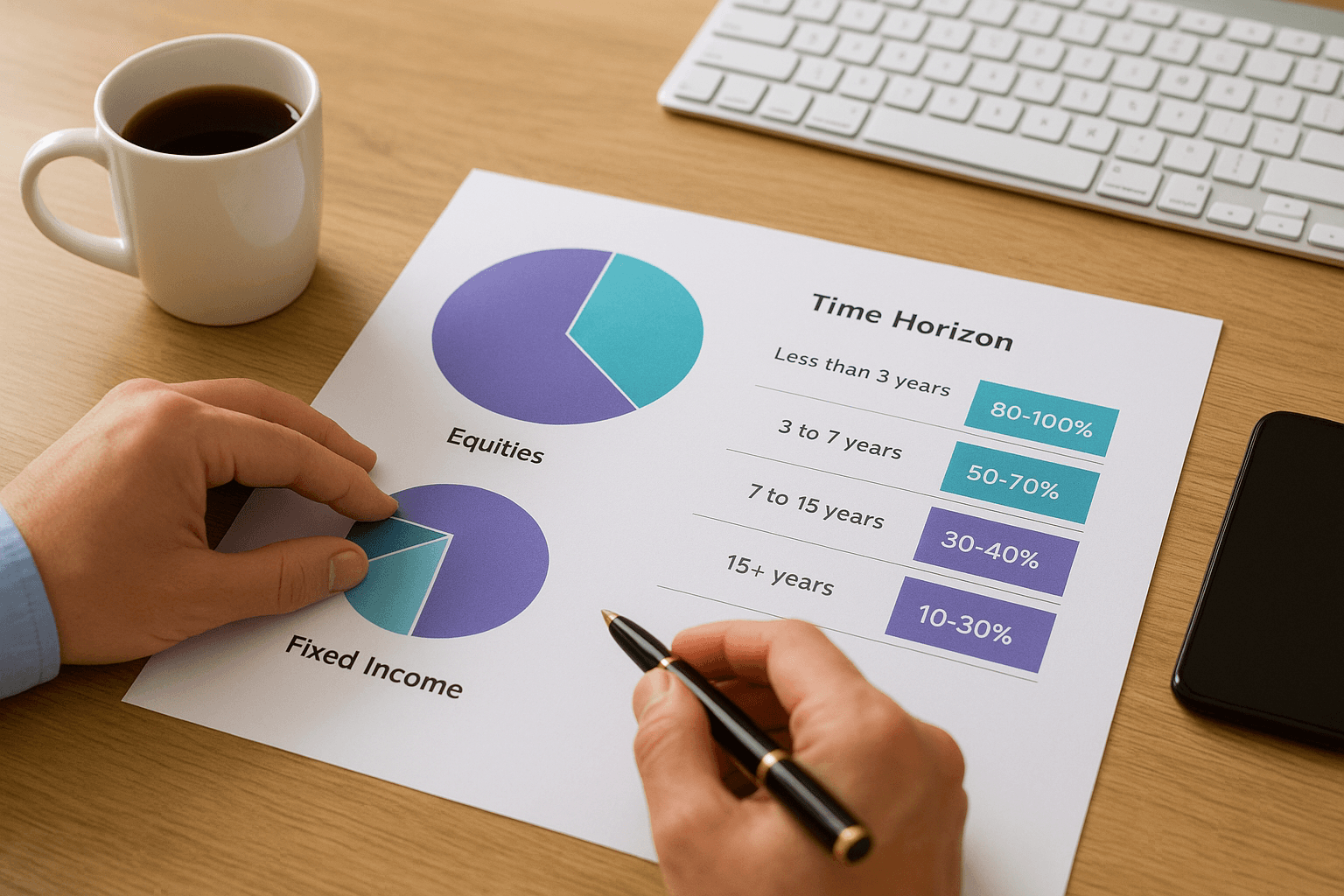

How time horizon changes everything

Investopedia places heavy emphasis on investment time horizon as the primary driver behind allocation decisions. If you have 25 years before you need the money, you can absorb significant short-term volatility in exchange for higher long-term equity growth. If you need the funds within three years, capital preservation becomes more important than chasing returns.

A simple framework based on time horizon gives you a starting reference point:

Time Horizon | Suggested Equity Allocation | Suggested Debt + Cash Allocation |

|---|---|---|

Less than 3 years | 0-20% | 80-100% |

3 to 7 years | 30-50% | 50-70% |

7 to 15 years | 60-70% | 30-40% |

15+ years | 70-90% | 10-30% |

These are starting points, not rigid rules. Your actual allocation also depends on income stability and existing liabilities, along with how you personally respond to seeing your portfolio drop 20% in a single bad quarter.

Why asset allocation matters for investors

Most investors focus on picking the right stock or fund, but research consistently shows that asset allocation drives the majority of your long-term portfolio returns, not individual security selection. When you spread your money across asset classes that don't move in sync, a sharp drop in equities doesn't wipe out your entire portfolio. Your debt holdings and gold act as a cushion, keeping you financially stable and mentally calm enough to stay invested.

It reduces the damage from market swings

A portfolio invested 100% in equities can fall 40% or more in a single bad year. The same portfolio with a 30% debt allocation would typically fall far less, because debt instruments like government bonds and PPF tend to hold their value or even gain when equity markets crash. That difference matters more than most investors realize. A smaller drawdown means you need a smaller recovery to get back to your starting point, which protects your compounding curve over the long run.

Losing 40% requires a 67% gain just to break even. Losing 20% only requires a 25% gain. Asset allocation is how you control which scenario you're dealing with.

It keeps your behavior in check

Even experienced investors make emotional decisions when their portfolios drop sharply. If your equity allocation is too high for your actual risk tolerance, you're more likely to panic-sell at the worst possible time, locking in losses permanently. A well-structured asset mix reduces that emotional pressure by making large swings less frequent. When you study how investopedia asset allocation frameworks are built, you'll notice they consistently treat behavioral risk as seriously as market risk. The right allocation isn't just about numbers on a spreadsheet; it's about building a portfolio you can actually hold through difficult markets without making costly mistakes.

How to choose your asset mix in India

Choosing your asset mix in India involves a few extra steps compared to the generic framework you'll find in a standard investopedia asset allocation guide. The Indian financial landscape has products and tax rules that directly affect how you should structure your portfolio. Before you pick any percentage split, you need an honest picture of your monthly obligations, existing assets, and tax bracket, because all three shape what the right allocation actually looks like for you.

Factor in your Indian-specific financial commitments

Your EPF and PPF contributions already count as debt allocation, even if you don't think of them that way. Many Indian salaried investors underweight equity because they mentally separate their retirement savings from their "investment portfolio," but treating everything as one unified picture gives you a far more accurate view of your current exposure. If your EPF already covers a significant portion of your target debt allocation, you have room to push your mutual fund or direct equity allocation higher without taking on undue risk.

Your EPF balance is a debt instrument. Count it when you calculate your current allocation, or you'll end up holding more fixed income than you planned and less equity than you need.

Use a simple rule as your starting point

A widely used starting framework for Indian investors is 100 minus your age equals your equity allocation percentage. A 35-year-old would target roughly 65% in equity and 35% in debt and gold. This is a blunt tool, but it gives you a baseline to refine based on your actual income stability, dependents, and existing liabilities. If your job involves variable income or you carry a large home loan EMI, you should likely hold more in liquid and debt instruments than this formula suggests.

Asset allocation strategies Investopedia covers

When you dig into investopedia asset allocation content, you'll find that it groups allocation strategies into distinct approaches, each with a different level of flexibility and hands-on involvement. Knowing which strategy fits your situation helps you avoid one of the most common mistakes investors make: switching strategies mid-cycle when markets move against them.

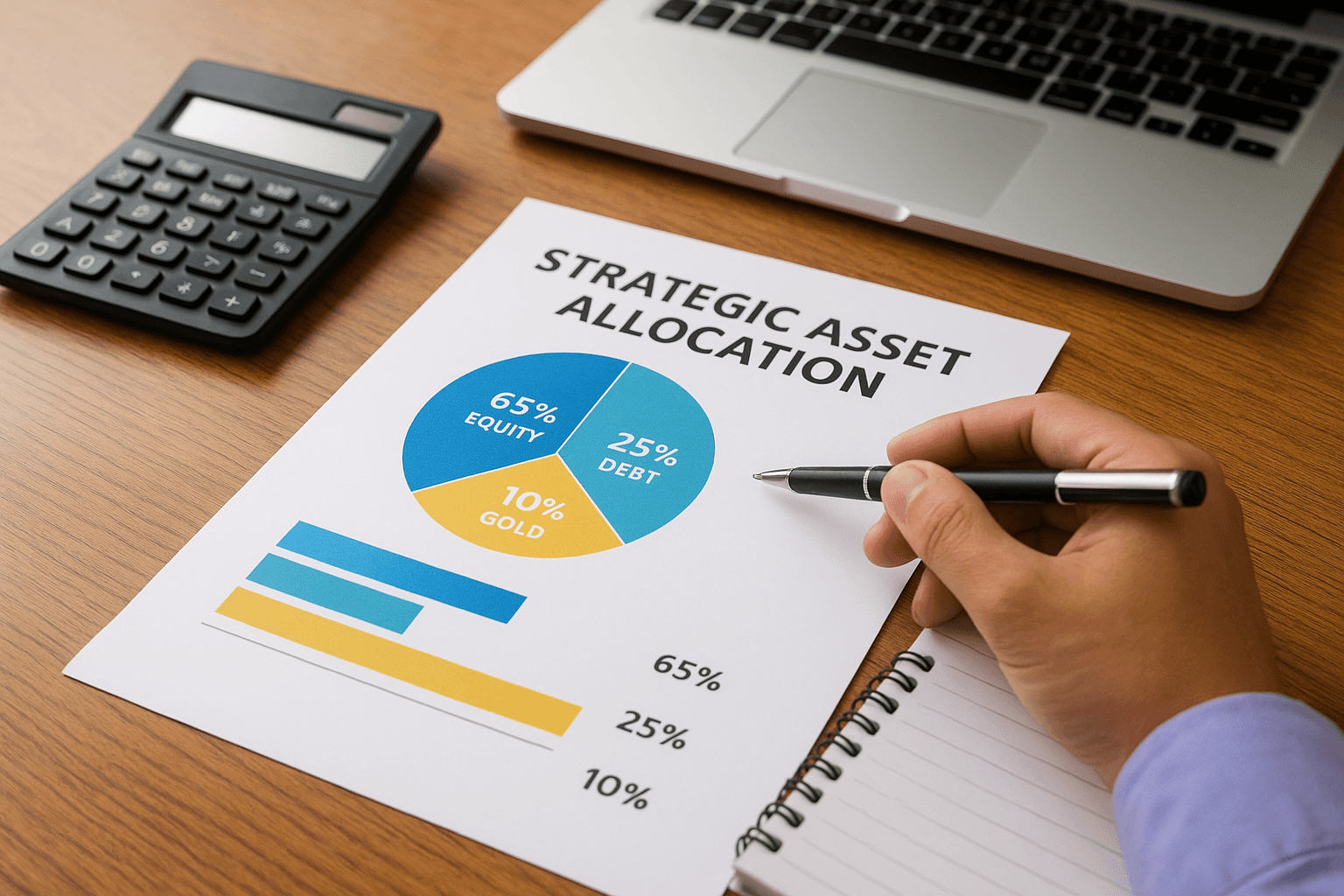

Strategic asset allocation

Strategic asset allocation sets a fixed target percentage for each asset class and holds to it regardless of short-term market movements. You decide, for example, that you want 65% equity, 25% debt, and 10% gold, and you rebalance back to those targets periodically, typically once or twice a year. This approach works well for investors who want a disciplined, low-maintenance framework without constantly second-guessing their portfolio. It removes the temptation to chase last year's winners and keeps your risk profile consistent over time.

Strategic allocation is about committing to a plan and rebalancing back to it, not reacting to headlines.

Rebalancing in India carries a tax cost, particularly when you sell equity mutual funds before the one-year mark and trigger short-term capital gains tax at 20%. To minimize that cost, direct any new SIP contributions toward underweight asset classes before selling existing holdings.

Tactical and dynamic approaches

Tactical asset allocation allows you to temporarily shift your percentages in response to market conditions, say, reducing equity from 65% to 50% when valuations look stretched, then moving back once conditions normalize. Investopedia covers this as a more active strategy that requires stronger market knowledge and clear rules for when to shift. Without those rules, tactical allocation easily turns into emotional market timing.

Dynamic asset allocation, common in many Indian balanced advantage funds, adjusts the equity-debt ratio automatically using a model, removing the behavioral element entirely and making it a practical option for investors who want flexibility without making the calls themselves.

Examples and common mistakes to avoid

Looking at a concrete example makes the investopedia asset allocation framework much easier to apply. Take a 35-year-old salaried professional in Bengaluru earning ₹15 lakhs per year, with a stable job, no dependents, and a 20-year investment horizon. Using the 100-minus-age rule gives a 65% equity target, and since their EPF already contributes roughly 15% toward debt, they only need an additional 20% in debt mutual funds or PPF to reach the remaining 35% fixed income allocation. Counting EPF upfront prevents the accidental over-weighting of fixed income that trips up most salaried investors.

A practical allocation example

Their actual portfolio might look like this:

Asset Class | Instrument | Allocation |

|---|---|---|

Equity | Index funds + mid-cap mutual funds | 65% |

Debt | PPF + debt mutual funds (EPF counted) | 25% |

Gold | Sovereign Gold Bonds | 10% |

This split gives meaningful equity exposure for long-term wealth creation while debt and gold act as a cushion during volatile periods. Rebalancing once a year by directing new SIP contributions toward the underweight asset class, rather than selling existing holdings, keeps the tax bill manageable and the allocation on track without triggering unnecessary short-term capital gains.

Mistakes that derail most investors

The most common mistake is treating your EPF and PPF as entirely separate from your investment portfolio. When you ignore those balances, you unknowingly hold far more debt than intended, which means less equity exposure than your long-term goals actually require. Count every financial account when you assess your current position, or your allocation numbers will mislead you from the start.

Sitting on 50% debt without realizing it because you ignored your EPF is one of the most expensive allocation errors a salaried investor can make.

Another costly error is shifting your allocation during a market downturn. Moving from 65% equity to 30% after a sharp correction locks in permanent losses and removes you from the recovery entirely. Set your target during calm markets and rebalance methodically, not in response to short-term market noise.

Putting it all together

Asset allocation is not a one-time decision you make and forget. The investopedia asset allocation framework gives you a solid conceptual foundation, but applying it effectively in India means accounting for your EPF, your tax bracket, and the specific mutual fund categories available to you. Your goal is a balanced mix across equity, debt, and gold that matches your time horizon and risk tolerance, not the mix that performed best last quarter.

Rebalance once a year by directing new contributions toward underweight asset classes before you sell anything. Count every account, including your EPF and PPF, when you assess your current position. Set your allocation during calm markets, commit to it, and resist shifting when markets move sharply in either direction. If you want a data-backed second opinion on your current portfolio before making any changes, get personalized AI-driven advice from Invsify and build a plan that actually fits your financial life.