Top 4 LIC Annuity Plans 2026: Rates, Pros & How to Choose

Shlok Sobti

Top 4 LIC Annuity Plans 2026: Rates, Pros & How to Choose

You have worked hard for decades, saved diligently, and now you want guaranteed monthly income after retirement. But when you search for LIC annuity plans, you find dozens of options—Jeevan Akshay VII, New Jeevan Shanti, Saral Pension, Smart Pension—each with different rates, payout options, and conditions. Which one gives you the highest monthly pension? Should you choose immediate or deferred annuity? What about joint life cover or return of purchase price? The confusion can push you toward wrong decisions or delay your retirement planning altogether.

This guide cuts through the noise. We compare the top 4 LIC annuity plans in 2026, showing you exact rates, eligibility criteria, and real-life payout examples. You will understand which plan suits your age, corpus size, and family situation. We also show you how Invsify's AI-powered tools can help you model different scenarios, calculate tax implications, and make the smartest annuity choice—without hidden fees or biased advice. By the end, you will know exactly which LIC annuity plan to buy and why.

1. Invsify for LIC annuity planning

Before you lock your retirement corpus into any LIC annuity plan, you need to understand how much monthly pension you will actually receive, what the tax implications are, and how the plan compares to other investment options. Most investors make this decision based on incomplete information or advice from commission-driven distributors. Invsify changes that by giving you AI-powered, unbiased analysis of every annuity option, tailored to your exact financial situation and retirement goals.

How Invsify helps with LIC annuity decisions

You enter your retirement corpus, age, and monthly income needs into Invsify's annuity calculator. The platform instantly compares all major lic annuity plans across their payout rates, tax treatment, and death benefit structures. You see exactly which plan gives you the highest monthly pension for your specific purchase price and age bracket. The AI analyzes whether immediate or deferred annuity makes more sense based on your retirement timeline and liquidity needs.

Invsify's conversational AI explains complex annuity features in simple language. You can ask questions like "Should I choose joint life annuity or single life with return of purchase price?" and get clear, data-backed answers within seconds. The platform shows you real-life scenario models where you can adjust variables like purchase price, deferment period, or annuity option to see how your monthly pension changes.

Key features for retirement and pension planning

Your personalized Wealth Wellness Score reveals whether you have saved enough to maintain your current lifestyle after retirement. The score factors in your existing corpus, expected expenses, inflation, and potential annuity income. If there is a shortfall, Invsify suggests how much more you need to save or which higher-yielding annuity option could bridge the gap.

The platform's portfolio tracking consolidates all your retirement assets in one view. You see your provident fund balance, mutual fund holdings, fixed deposits, and existing insurance policies alongside potential annuity purchases. This holistic view prevents you from over-committing to annuities when you already have sufficient passive income sources. Daily audio snippets keep you updated on any policy changes, new annuity launches, or rate revisions by LIC that could affect your decision.

Taxation, NPS use and integrating LIC annuities

Annuity income is taxable as per your income slab, but Invsify's tax calculator shows you the exact post-tax monthly income for each plan option. The platform factors in your other income sources to determine your effective tax liability on annuity payouts. You understand whether a higher gross annuity rate actually translates to more take-home income after taxes.

If you are an NPS subscriber, PFRDA mandates using at least 40% of your corpus to buy an immediate annuity at retirement. Invsify integrates this requirement into your planning. The AI compares LIC's NPS-approved annuity plans (Jeevan Akshay VII and Smart Pension) with other insurers empanelled by PFRDA. You see which provider offers the best rates for your specific NPS corpus and chosen annuity option.

Your retirement is too important to trust generic advice or outdated calculators.

Who should use Invsify before buying an annuity

You should use Invsify if you are within five years of retirement and have accumulated a lump sum between ₹10 lakh and ₹2 crore. The platform is built for salaried professionals, self-employed individuals, and HNIs who want to maximize their retirement income without hidden fees eating into their corpus. If you currently rely on online forums or unverified sources for annuity advice, Invsify gives you SEBI-registered, professional guidance.

Investors who have already purchased mutual funds or ULIPs but are confused about annuity allocation will find the portfolio integration valuable. Those comparing LIC annuities with fixed deposits, senior citizen savings schemes, or post office monthly income plans get side-by-side comparisons. If you want to understand the true cost of buying through traditional distributors, Invsify's hidden fee calculator reveals the exact commission drag on your returns.

Pricing, access and how to get started

Invsify offers unlimited AI chatbot access and basic annuity calculators for free. You can model different LIC annuity scenarios, compare plans, and get initial recommendations without paying anything. Premium features like personalized wealth wellness scores, weekly insights, and human advisor consultations start at affordable subscription tiers designed for middle-income investors.

Getting started takes less than 10 minutes. You complete a digital KYC process and answer questions about your risk profile and retirement goals. The platform immediately generates your personalized dashboard with annuity recommendations. If you need urgent help choosing between two annuity options, you can request a 30-second callback from a human advisor who reviews your situation and provides quick resolution.

Practical FAQs about LIC annuity planning

Can Invsify help you choose between Jeevan Akshay VII and New Jeevan Shanti? Yes, the AI compares immediate versus deferred payout structures based on your retirement timeline. Should you spread your corpus across multiple annuity plans? The platform shows you diversification strategies that balance payout rates with death benefit protection. What if LIC launches a new annuity plan mid-year? You receive instant notifications with comparison analysis against your existing shortlist.

2. LIC Jeevan Akshay VII immediate annuity

LIC Jeevan Akshay VII stands as one of the most popular immediate annuity plans in India because you start receiving pension from the very first month after purchase. You pay a lump sum amount once, and LIC guarantees lifelong monthly income without any deferment period. This plan suits you if you have just retired, received a gratuity or provident fund payout, and want to convert that corpus into regular cash flow immediately. The plan offers ten different annuity options covering single life, joint life, guaranteed periods, and return of purchase price scenarios.

Overview and key features

You purchase LIC Jeevan Akshay VII by paying a single premium amount with no future payment obligations. The annuity rates are locked at purchase and remain guaranteed for your entire lifetime, protecting you from future rate cuts or market volatility. LIC calculates your monthly pension based on your age, chosen annuity option, and the purchase price you invest. Older purchasers receive higher annuity rates because their statistical life expectancy is shorter.

The plan operates as a non-linked, non-participating policy, meaning your pension amount does not fluctuate with LIC's investment performance or bonus declarations. You know exactly how much you will receive every month for the rest of your life. The policy comes with no survival period requirements, so your pension starts immediately after the first premium payment is processed.

Annuity options and payout frequencies

Jeevan Akshay VII offers you ten distinct annuity options to match your family structure and financial priorities. Option A provides a basic lifetime annuity with no return of purchase price at death. Options B through E add guaranteed payment periods of 5, 10, 15, or 20 years respectively, ensuring your nominees receive the pension for the remaining guaranteed term even if you pass away early. Option F returns your full purchase price to nominees on death while maintaining lifetime pension for you.

Option G gives you an increasing annuity that grows at 3% annually, helping you combat inflation over long retirement periods. Options H, I, and J cover joint life scenarios where your spouse continues receiving 50% or 100% of the annuity after your death. Option J also returns the purchase price after both you and your spouse have passed away, maximizing wealth transfer to children.

You choose your payout frequency from monthly, quarterly, half-yearly, or annual modes. Monthly pension typically offers slightly lower annual rates compared to annual mode because LIC faces higher administrative costs processing twelve payments instead of one. The pension credit happens on the same date every period through direct bank transfer.

Eligibility, minimum purchase and entry ages

You can purchase Jeevan Akshay VII from age 30 to 85 years for most annuity options, though some joint life variants extend eligibility up to age 100. The minimum purchase price stands at ₹1 lakh with no maximum limit, allowing both middle-income retirees and HNIs to participate. For joint life options, both you and your spouse must meet the age criteria, and typically LIC requires the primary annuitant to be older than the secondary annuitant.

Special provisions exist for disabled dependents where the minimum purchase price reduces to ₹50,000 under certain conditions. You do not need to undergo any medical examination regardless of the purchase amount, making the buying process quick and paperwork-light compared to traditional life insurance policies.

Indicative annuity rates with example calculations

A 60-year-old male purchasing Jeevan Akshay VII with ₹10 lakh receives approximately ₹6,620 monthly under Option A (basic lifetime annuity). The same purchase price under Option F (lifetime annuity with return of purchase price) drops the monthly pension to around ₹5,600 because LIC must reserve funds to return the corpus on death. Under Option G (increasing annuity at 3% annually), the starting monthly pension falls to approximately ₹4,910 but grows every year.

For joint life scenarios, a 60-year-old male with a 55-year-old female spouse receives about ₹6,290 monthly under Option H (50% to spouse after death) or ₹5,990 under Option I (100% to spouse) for the same ₹10 lakh investment. These rates reflect 2026 actuarial tables and can vary based on your exact age in months at purchase.

The gap between highest and lowest payout options reaches nearly 35% for the same purchase price.

Women typically receive slightly lower monthly rates than men of the same age because female life expectancy statistically exceeds male longevity. A 60-year-old female gets approximately ₹6,200 monthly under Option A versus ₹6,620 for a male, reflecting this mortality difference.

Pros, cons and best fit investors

Jeevan Akshay VII gives you immediate cash flow from month one, perfect when you have just retired and need to replace your salary income quickly. The guaranteed lifetime payments eliminate longevity risk where you might outlive your savings. Ten annuity options provide flexibility to match your specific family structure and legacy goals. LIC's sovereign guarantee backing adds credibility that smaller private insurers cannot match.

The plan's major limitation lies in fixed payment amounts that do not adjust for inflation beyond Option G's basic 3% increase. Medical inflation and general price rises often exceed this rate, eroding your purchasing power over 20 or 30 year retirement spans. You cannot withdraw or surrender the policy once purchased, locking your corpus permanently. Tax treatment adds another disadvantage as the entire annuity income becomes taxable as regular income without any exemption benefits.

Best fit investors include those aged 60 to 75 who have accumulated ₹15 lakh to ₹1 crore in retirement savings and want to convert 30% to 50% of that corpus into guaranteed monthly income. You should consider this plan if you have no other pension sources like employer pensions or rental income. Avoid putting your entire retirement corpus here because the low inflation adjustment and illiquidity create long-term risks.

When to prefer Jeevan Akshay VII over other LIC annuities

Choose Jeevan Akshay VII when you need pension payments to start within 30 days rather than waiting months or years. This immediacy beats New Jeevan Shanti's deferred annuity structure if you have already retired or are retiring this month. The plan works better than Saral Pension when you want more than six annuity options to fine-tune your payout structure, especially if you need increasing annuity or specific guaranteed periods.

Prefer Jeevan Akshay VII over Smart Pension when you want simpler option structures without complex return of purchase price variants at specific ages like 75 or 80. The ten options here cover most family situations without overwhelming you with 21 different choices. If you are an NPS subscriber mandated to buy an immediate annuity at retirement, Jeevan Akshay VII stands as one of only two LIC plans approved by PFRDA for this purpose, making it your default choice alongside Smart Pension.

3. LIC New Jeevan Shanti deferred annuity

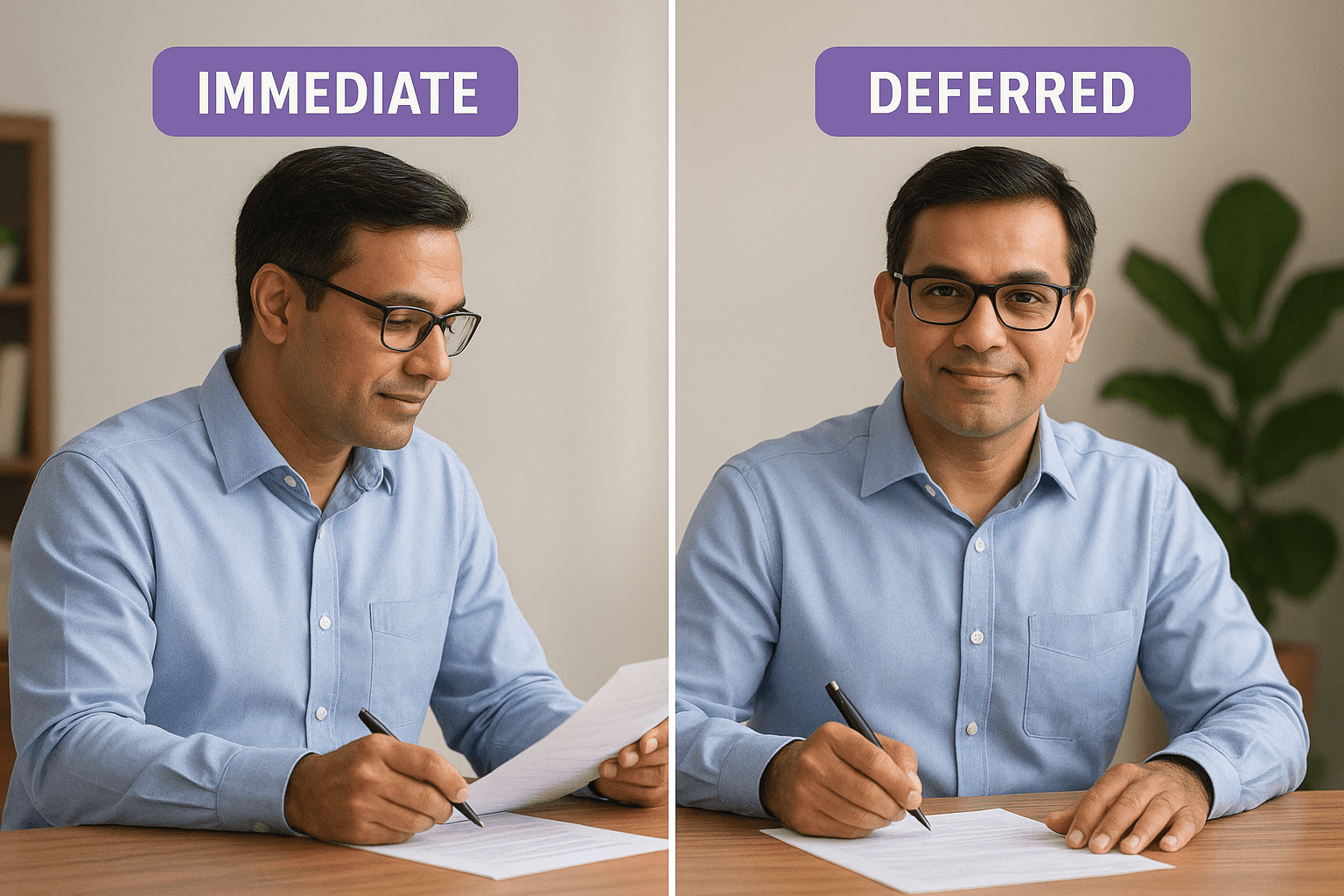

LIC New Jeevan Shanti gives you the flexibility to start receiving pension either immediately after purchase or after a deferment period of up to 20 years. This dual-option structure makes it unique among lic annuity plans because you can buy it today while still working and activate the pension payouts only when you actually retire. During the deferment period, LIC adds guaranteed additions to your purchase price, effectively increasing the corpus that generates your eventual pension. This plan suits you if you are 5 to 15 years away from retirement and want to lock in today's annuity rates while building a larger pension base.

Overview and key features

You purchase New Jeevan Shanti with a single premium payment ranging from ₹1.5 lakh to unlimited amounts. The plan operates as a non-linked, non-participating policy where your pension calculations depend on fixed actuarial tables rather than market performance. LIC guarantees the annuity rates at the time you buy the policy, protecting you from future rate reductions that might happen due to falling interest rates or changing mortality assumptions.

The policy offers you both immediate and deferred variants within the same plan structure. You choose at purchase whether to start receiving pension from the next month or defer it for 1 to 20 years. During any deferment period, LIC credits guaranteed additions to your account annually, compounding your effective purchase price. These additions typically range from ₹50 to ₹75 per ₹1,000 of purchase price per year, depending on the deferment duration you select.

Immediate versus deferred annuity options

When you select the immediate annuity variant, New Jeevan Shanti functions similarly to Jeevan Akshay VII with your first pension payment arriving within 30 days. You access the same ten annuity option structures including single life, joint life, guaranteed periods, and return of purchase price scenarios. The immediate variant works when you have already retired or are retiring within weeks and need cash flow to start quickly.

Choosing the deferred variant delays your pension start date by your selected deferment period from 1 to 20 years. During this waiting period, you receive no cash payouts but LIC accumulates guaranteed additions that boost your eventual pension amount. A 45-year-old purchasing ₹10 lakh with a 15-year deferment receives pension starting only at age 60, but the accumulated guaranteed additions might have grown the effective purchase price to ₹15 lakh or more. This enhanced corpus then generates a significantly higher monthly pension compared to buying an immediate annuity at age 60 with just the original ₹10 lakh.

The guaranteed additions during deferment can increase your eventual monthly pension by 40% to 60% compared to immediate annuity rates.

Deferment period, purchase rules and sample payouts

You select your deferment period from 1 year up to a maximum of 20 years at the time of policy purchase. LIC does not allow you to change this period later, so you must accurately estimate your retirement timeline before buying. The entry age ranges from 30 to 79 years for deferred annuity options, with the age at vesting (when pension starts) capped at certain limits depending on the specific annuity option you choose.

For a 50-year-old male purchasing ₹20 lakh with a 10-year deferment, the guaranteed additions accumulate approximately ₹1 lakh to ₹1.25 lakh in total over the waiting period. At age 60 when vesting happens, the effective purchase price becomes ₹21 lakh to ₹21.25 lakh. This enhanced corpus generates around ₹14,000 to ₹15,000 monthly under a basic lifetime annuity option, whereas buying Jeevan Akshay VII at age 60 with just ₹20 lakh would yield only ₹13,200 monthly. The deferment strategy delivers a permanent 10% to 15% pension boost throughout your retirement.

Death benefits, liquidity and loan features

If you die during the deferment period before vesting, your nominees receive the purchase price plus all accumulated guaranteed additions as a lump sum death benefit. LIC ensures the death benefit never falls below 110% of your original purchase price, protecting your family even if you pass away shortly after purchase. Once the policy vests and pension payments begin, death benefits depend on which annuity option you selected, following the same structures as Jeevan Akshay VII.

New Jeevan Shanti provides loan facilities during the deferment period under specific annuity options. You can borrow up to 75% of the accumulated guaranteed additions after the policy has run for at least three years. The loan interest rate follows LIC's prevailing rates, typically ranging from 9% to 10% annually. This liquidity feature helps you access funds during emergencies without surrendering the policy, though surrender itself remains restricted with only partial surrender options available under certain conditions.

Pros, cons and best fit investors

New Jeevan Shanti allows you to plan ahead by purchasing retirement income products while still earning a salary, spreading your financial planning across multiple years rather than scrambling at retirement. The guaranteed additions during deferment effectively give you higher returns than keeping money idle in savings accounts while waiting to buy an immediate annuity later. Ten annuity options at vesting provide the same flexibility as Jeevan Akshay VII once your pension starts.

The plan's complexity creates confusion because you must decide on deferment periods, annuity options, and future pension needs all at once during purchase. Guaranteed additions, while beneficial, grow at modest rates that may not beat inflation or equity market returns over long periods. You sacrifice liquidity by locking funds for years before receiving any income, which becomes problematic if you face unexpected expenses or medical emergencies before vesting.

Best fit investors include those aged 40 to 60 who have accumulated surplus savings beyond their immediate needs and want to convert a portion into future guaranteed income. You benefit most if you can confidently predict your retirement date 5 to 15 years in advance and do not need the invested corpus for any purpose during the deferment period. Avoid this plan if you might need the funds before vesting or if you prefer keeping retirement corpus invested in growth assets until the actual retirement date.

When to choose New Jeevan Shanti instead of Jeevan Akshay

Select New Jeevan Shanti when you are still working and your retirement date lies 5 or more years in the future. The guaranteed additions during deferment justify the choice over buying Jeevan Akshay VII immediately and losing potential growth. Choose this over Saral Pension when you want the option to defer pension start dates rather than being forced into immediate annuity structures, giving you timing flexibility that Saral's simpler framework does not accommodate.

Prefer New Jeevan Shanti when you want to lock in current annuity rates while you are younger and rates might be more favorable than future projections. Insurance companies periodically revise annuity rates downward as interest rates fall, so purchasing a deferred annuity today protects you from those future reductions. The plan also works better than Smart Pension when you prioritize guaranteed additions during accumulation rather than Smart Pension's more complex increasing annuity and return of purchase price variants at specific ages.

4. LIC Saral Pension simple annuity plan

LIC Saral Pension emerged from a regulatory mandate by the Insurance Regulatory and Development Authority of India (IRDAI) to create a standardized, easy-to-understand annuity product across all life insurers. The plan eliminates complexity by offering just six annuity options instead of the ten or more found in other lic annuity plans, making your decision process straightforward. You pay a single premium and receive immediate pension payments starting from the very next month without any waiting periods or deferment complications. This regulatory backing ensures uniform features across insurers, allowing you to compare rates purely on payout efficiency rather than getting confused by different product structures.

Overview and regulatory background of Saral Pension

IRDAI introduced Saral Pension in 2021 to address consumer complaints about opaque annuity structures and difficult comparison shopping across insurance companies. Every life insurer must offer this standardized product with identical features, though each company sets its own annuity rates based on their actuarial assumptions. LIC launched its version as Plan 862, maintaining the regulatory framework while leveraging its distribution network to reach pensioners across urban and rural India.

The plan operates as a non-linked, non-participating immediate annuity policy where your pension amount stays fixed throughout your lifetime based on the purchase price and your age at entry. You receive no bonuses or market-linked returns, ensuring predictable cash flows without any performance uncertainty. The standardization means you can easily compare LIC's Saral Pension rates with offerings from HDFC Life, SBI Life, or other insurers to identify who provides the highest monthly payout for your specific age and purchase amount.

Available annuity options and payout modes

Saral Pension limits your choices to six annuity options designed to cover the most common retirement scenarios without overwhelming you with excessive variants. Option 1 provides a basic lifetime annuity with no return of purchase price at death. Option 2 adds a joint life structure where your spouse receives 100% of the pension after your death until they pass away. Option 3 returns your purchase price to nominees on death while maintaining lifetime pension for you.

Option 4 combines joint life with return of purchase price, continuing full pension to your spouse and then returning the corpus after both deaths. Option 5 offers an increasing annuity that grows at 3% annually, helping you combat inflation during long retirement periods. Option 6 provides lifetime pension for you, then transfers to your spouse at 50% of the original rate until their death. These six structures handle most family situations from single retirees to married couples concerned about surviving spouse income.

You select your payout frequency from monthly, quarterly, half-yearly, or annual modes at the time of purchase. Monthly payments suit you if you need regular cash flow to cover living expenses, while annual mode typically offers slightly higher total yearly amounts because LIC processes fewer transactions. The pension credits directly to your bank account on the same date each period through electronic transfer.

Eligibility, purchase price and example annuity rates

You must be between 40 and 80 years old to purchase LIC Saral Pension, with the plan designed specifically for near-retirees and retirees rather than younger investors. The minimum purchase price stands at ₹1 lakh with no maximum limit, though purchasing amounts beyond ₹50 lakh may require additional documentation for anti-money laundering compliance. LIC does not mandate medical examinations regardless of your purchase amount or age.

A 60-year-old male buying Saral Pension with ₹10 lakh receives approximately ₹6,500 monthly under Option 1 (basic lifetime annuity). The same purchase under Option 3 (lifetime with return of purchase price) drops the monthly pension to around ₹5,500 because LIC reserves funds to return the corpus on death. For Option 5 (increasing annuity), the starting monthly payment begins at approximately ₹4,800 but grows by 3% each year.

The standardized structure lets you compare exact rates across insurers within minutes rather than decoding different product features.

Death benefits, surrender rules and loan availability

If you die while receiving Saral Pension, death benefits depend entirely on which option you purchased. Options 3, 4, and 6 return your full purchase price as a lump sum to nominees after applicable pension payments cease. Options 2 and 4 continue pension payments to your surviving spouse until their death. Option 1 provides no death benefits beyond stopping the pension, making it suitable only if you have no financial dependents.

LIC allows limited surrender options after six months from policy commencement, though surrendering permanently stops all future pension payments. You receive the prevailing surrender value, which typically falls significantly below your original purchase price due to mortality charges and administrative costs deducted. This penalty structure discourages early exits and protects LIC's actuarial assumptions.

The plan permits loan facilities after six months, allowing you to borrow up to 75% of the surrender value during financial emergencies. Loan interest rates follow LIC's standard lending rates, usually ranging from 9% to 10.5% annually. You repay the loan with interest to maintain your full pension amount, or LIC deducts the outstanding loan balance from any death benefits payable to your nominees.

Pros, cons and best fit investors

Saral Pension's standardized structure eliminates confusion by offering just six clear options instead of the ten or more found in Jeevan Akshay VII or New Jeevan Shanti. You compare rates across multiple insurers easily because everyone follows the same product framework, empowering you to find the best payout rates without decoding complex feature differences. IRDAI oversight provides regulatory confidence that product terms remain transparent and consumer-friendly.

The limited option set becomes a disadvantage when you need specific features like 15-year or 20-year guaranteed periods that exist in Jeevan Akshay VII but not in Saral Pension. You cannot defer pension start dates, forcing immediate annuity structure even if you might benefit from waiting a few years. The surrender value penalties and illiquidity match other annuity products, locking your corpus permanently once you complete the purchase.

Best fit investors include those aged 60 to 75 who want a simple, straightforward annuity without complex decision trees. You benefit from Saral Pension if you find yourself overwhelmed by the ten options in Jeevan Akshay VII and need just basic lifetime or joint life coverage. The plan works when you want to quickly compare rates across multiple insurers before committing, using the standardized structure to identify which company offers the highest monthly payout for your age bracket.

When Saral Pension works better than other LIC annuities

Choose Saral Pension over Jeevan Akshay VII when you need only basic annuity structures like lifetime, joint life, or return of purchase price without guaranteed period complexities. The six-option framework suffices for most retirees and saves you from analysis paralysis created by ten different choices. Select this plan when you want to benchmark LIC's rates against other insurers easily, since every company offers identical Saral Pension features allowing pure rate comparison.

Prefer Saral Pension over New Jeevan Shanti when you need immediate pension flow rather than deferment periods and guaranteed additions. The simplicity beats New Jeevan Shanti's complexity if you have already retired and do not want to understand accumulation phases or vesting rules. Saral Pension also works better than Smart Pension's 21 options when you know you only need a straightforward lifetime or joint life structure without age-based return variants or multiple increasing annuity percentages cluttering your decision process.

5. LIC Smart Pension flexible annuity plan

LIC Smart Pension (Plan 879) delivers the most extensive choice among all lic annuity plans by offering 21 different annuity options compared to the 10 options in Jeevan Akshay VII or 6 in Saral Pension. You get variations on increasing annuity rates, return of purchase price at specific ages like 75 or 80, and percentage-based corpus returns spread over multiple years. This flexibility helps you fine-tune your retirement income strategy to match complex family situations, phased legacy planning, or specific inflation protection needs that simpler plans cannot address. The plan functions as an immediate annuity where pension payments start from the next month after your single premium purchase, and LIC approved it specifically for NPS subscribers who must convert their retirement corpus into annuity products.

Overview and key features

You purchase Smart Pension with a single premium payment starting from ₹1 lakh with no upper limit, though amounts below ₹50,000 apply only for disabled dependents under special provisions. The plan operates as a non-linked, non-participating immediate annuity policy where your monthly pension depends on actuarial calculations based on your age, gender, chosen option, and purchase amount. LIC guarantees the rates at purchase time, protecting you from future rate reductions throughout your lifetime.

The entry age ranges from 18 to 100 years depending on which annuity option you select, making it the most age-flexible among major LIC pension products. Single life options accommodate purchasers up to age 100, while joint life variants typically cap primary annuitant age at 80 to 85 years. You do not undergo medical examinations regardless of purchase amount, streamlining the buying process to document verification and payment processing only.

Single and joint life annuity options

Smart Pension provides you with seven single life annuity options covering basic lifetime pension (Option A), guaranteed periods of 5, 10, 15, or 20 years (Options B1 through B4), increasing rates at 3% or 6% annually (Options C1 and C2), and return of purchase price on death (Option F). Option D adds a unique feature where LIC returns only the balance purchase price after deducting all pension payments already made to you, ensuring your nominees receive at least some corpus even after decades of pension withdrawals.

Joint life structures span seven options from G1 through J, letting you configure how much pension transfers to your spouse and whether the corpus returns after both deaths. Options G1 and G2 provide either 50% or 100% continuation of your pension to the surviving spouse without any corpus return. Options H1, H2, I1, and I2 combine increasing annuity rates of 3% or 6% with either 50% or 100% spousal continuation. Option J maintains 100% pension to the last survivor and then returns the full purchase price to your children or other nominees.

Increasing annuity variants and return of purchase price

You access four increasing annuity options within Smart Pension compared to just one in Jeevan Akshay VII or Saral Pension. Options C1 and C2 increase your single life pension by 3% or 6% every year respectively, with the higher rate starting from a lower base amount but catching up within 8 to 10 years. Options H1, H2, I1, and I2 apply the same 3% or 6% annual increases to joint life structures, protecting both you and your spouse against inflation erosion over 20 or 30 year retirement spans.

Return of purchase price mechanisms vary across multiple options beyond the standard full-corpus-on-death structure. Options E1 through E5 introduce age-triggered returns where you receive 50% or 100% of your purchase price when you reach specific ages like 75 or 80 while your pension continues. Option E5 distributes 5% of the purchase price every year from age 76 to 95, creating a phased withdrawal pattern that gives you access to your own capital during later retirement stages while maintaining pension income.

The age-triggered return options let you reclaim your corpus gradually while still receiving monthly pension until death.

Eligibility, purchase rules and indicative payout levels

You qualify for Smart Pension from age 18 onwards for basic single life options, though most purchasers fall in the 40 to 80 age range when retirement planning becomes urgent. Joint life options require both you and your spouse to meet age criteria, with secondary annuitants typically capped at 5 to 10 years younger than the primary purchaser. The minimum monthly pension you can receive stands at ₹1,000 across all options, translating to minimum purchase prices varying by age and chosen structure.

A 60-year-old male purchasing ₹20 lakh under Option A (basic lifetime annuity) receives approximately ₹13,200 monthly, matching Jeevan Akshay VII rates for the same age and amount. Switching to Option F (lifetime with return of purchase price) drops the monthly payment to around ₹11,200. Option C2 (increasing at 6% annually) starts at just ₹9,600 monthly but grows to over ₹17,000 by year 10 and ₹30,000 by year 20, eventually surpassing fixed rate options if you live into your 80s or 90s.

Pros, cons and best fit investors

Smart Pension delivers unmatched flexibility with 21 options covering every conceivable family structure, inflation concern, and legacy planning scenario. The age-triggered return variants let you access your own capital during later retirement without surrendering the policy or stopping pension flow. Increasing annuity options at both 3% and 6% rates provide better inflation protection than the single 3% option in other plans, particularly valuable during periods of persistent price increases.

The overwhelming number of options creates decision paralysis for many retirees who struggle to compare 21 different structures and pick the optimal one. Some options deliver lower starting pension rates that take 15 to 20 years to catch up with simpler alternatives, requiring you to live well into your 80s or 90s to benefit fully. Tax treatment remains unfavorable as all annuity income becomes taxable at your slab rate without exemptions, and the illiquidity matches other annuity products once you complete the purchase.

Best fit investors include those aged 55 to 75 with retirement corpus between ₹20 lakh and ₹2 crore who want sophisticated retirement income engineering rather than basic lifetime pension. You benefit most if you understand actuarial concepts well enough to model different scenarios across the 21 options. The plan suits you when you need specific features like 6% increasing annuity or 5% annual corpus distribution that other LIC products simply do not offer.

How to decide between Smart Pension and other LIC annuities

Choose Smart Pension over Jeevan Akshay VII when you specifically need 6% annual increases or age-triggered return of purchase price mechanisms that Jeevan Akshay's ten options cannot provide. The extra 11 option variants justify the added complexity only if you actually require those specialized structures for your family situation. Select this over New Jeevan Shanti when you need immediate pension flow rather than deferred accumulation, as Smart Pension does not offer any waiting period or guaranteed addition features.

Prefer Smart Pension over Saral Pension when you want comprehensive customization beyond Saral's basic six options and you feel confident analyzing trade-offs across 21 different structures. The plan works better than others for NPS subscribers because PFRDA specifically approved Smart Pension alongside Jeevan Akshay VII as eligible annuity products for mandatory retirement corpus conversion. You gain flexibility that NPS rules require while accessing advanced features other PFRDA-approved insurers may not match at competitive rates.

Key takeaways

You now have the complete picture of the top four lic annuity plans available in 2026. Jeevan Akshay VII works when you need immediate monthly income starting next month with ten option variants. New Jeevan Shanti suits you if retirement lies 5 to 15 years ahead and you want guaranteed additions boosting your eventual pension by 40% to 60%. Saral Pension delivers simplicity with just six standardized options, making cross-insurer rate comparisons effortless. Smart Pension provides the most flexibility through 21 different structures including 6% annual increases and age-triggered corpus returns.

Your retirement corpus deserves more than guesswork or commission-driven advice. Use Invsify's AI-powered annuity calculator to model exact scenarios across all four plans, compare post-tax income, and understand which option maximizes your monthly pension based on your specific age and purchase amount. Start your free annuity analysis on Invsify and make your LIC annuity decision with complete clarity before committing your hard-earned retirement savings.